Sample Category Title

Daily Wave Analysis: GBP/USD Second Bullish Breakout Above 1.33 Resistance Zone

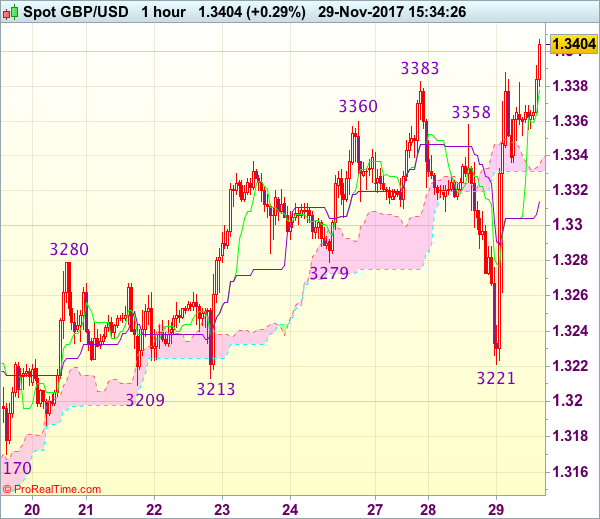

Currency pair GBP/USD

The GBP/USD made a bearish bounce at the resistance (red) zone but then found strong support about half way the range. The bullish bounce is showing strong momentum and price could now be ready for a larger bullish breakout. For the moment the bearish wave 4 of yesterday seems unlikely after this bullish break and price could be ready for a wave 5 (orange).

The GBP/USD could be building a wave 1 (green) within wave 3 (brown).

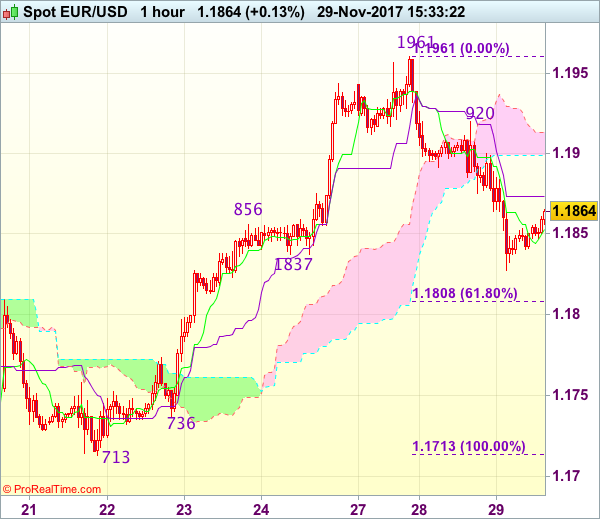

Currency pair EUR/USD

The EUR/USD seems to have completed a wave 1 (pink) and price could now be building a wave 2 retracement (pink).

The EUR/USD completed an ABC (blue) zigzag yesterday but price could extend the correction via WXY (purple) within that wave 2.

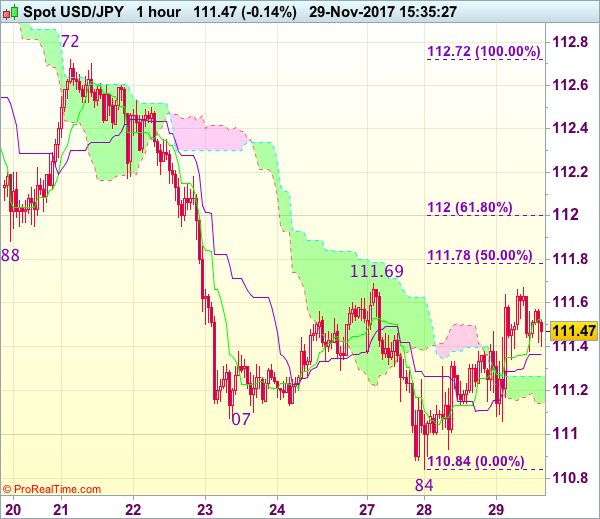

Currency pair USD/JPY

The USD/JPY bounced at the 50% Fibonacci support level and is now at the resistance top of the bearish channel (red).

The USD/JPY could be building a bear flag chart pattern within a larger wave C (blue). A bearish breakout could see price fall towards the Fibonacci targets whereas a bullish break could see price test the Fibonacci levels.

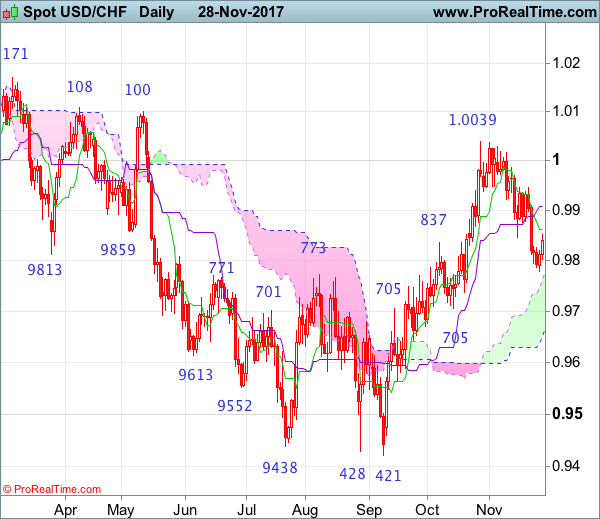

USD/CHF Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Shooting star

• Time of formation: 7 Mar 2017

• Trend bias: Sideways

Daily

• Last Candlesticks pattern: Morning star

• Time of formation: 9 May 2017

• Trend bias: Near term up

USD/CHF – 0.9840

Although the greenback recovered after falling to 0.9778 earlier this week, reckon upside would be limited to the Tenkan-Sen (now at 0.9863) and the Kijun-Sen (now at 0.9909) should remain intact, bring another decline later. Below said support at 0.9778 would extend the corrective decline from 1.0039 towards support at 0.9737 but reckon 0.9700 would hold and bring rebound later. Above the Kijun-Sen would suggest low is possibly formed but break of 0.9950-55 is needed to add credence to this view, bring test of indicated resistance at 1.0018, above there would signal the pullback from 1.0039 has ended, bring retest of this level first.

On the downside, whilst initial fall to 0.9770, then 0.9737 support cannot be ruled out, reckon 0.9700 would hold and bring another rise later. A daily close below previous support at 0.9700 would confirm top has been formed at 1.0039 and bring retracement of recent upmove from 0.9421 to minor support at 0.9670, then 0.9642 (another support) but reckon downside would be limited to 0.9590-00 and support at 0.9565 should remain intact.

Recommendation: Buy at 0.9730 for 0.9930 with stop below 0.9630.

On the weekly chart, last week’s fall from 0.9947 formed another black candlestick, retaining our view that further consolidation below recent high at 1.0039 would be seen and initial downside risk remains for weakness to the Kijun-Sen (now at 0.9730) where renewed buying interest should emerge, bring another rise later, above said resistance at 0.9947 would bring test of 0.9987, break there would suggest the pullback from 1.0039 has ended, bring retest of this level, break there would extend the rebound from 0.9421 low to previous resistance at 1.0100-08, having said that, overbought condition should prevent sharp move beyond previous resistance at 1.0171 and 1.0200-10 should hold from here.

On the downside, although initial pullback to 0.9770 is likely, reckon 0.9730-37 (current level of the Kijun-Sen and previous support) would limit downside and bring another rise later. A weekly close below there would defer and signal top is formed instead, this also suggest first leg of rebound from 0.9737 has ended and bring weakness to 0.9690-00, however, reckon support at 0.9642 would limit downside and price should stay above support at 0.9565 and the greenback shall stage another strong rebound next month.

Currencies: Dollar And Sterling Rebound

Sunrise Market Commentary

- Rates: Developments on balance negative for core bonds

German inflation data have market moving potential especially in case of higher than expected readings. Progress on US tax reforms, Brexit and North Korea will highjack a lot of headlines today. On balance, we think that developments are positive for risk sentiment and negative for core bonds, even if yesterday’s impact on (bond) trading remained limited. - Currencies: Dollar and sterling rebound

The dollar captured a better momentum on positive eco data and progress in the Senate tax bill. Sterling also jumped sharply higher on headlines that a solution on the Brexit divorce bill was almost reached. Today, the focus for USD trading will be on Yellen’s testimony before the JEC. Will she be ‘hawkish’ enough to sustain further USD gains?

The Sunrise Headlines

- US stock markets ended strong (+1%) as progress on US tax reforms outweighed a North Korean threat. Asian stock markets gain ground as well this morning with China underperforming.

- Britain has bowed to EU demands and agreed to fully honour its financial commitments as identified by Brussels, removing one of the biggest obstacles to a Brexit divorce settlement.

- Republican efforts to overhaul the US tax code gained momentum when two key Senate Republicans expressed optimism about supporting the bill and a congressional committee advanced the measure for a vote later this week.

- North Korea said it had successfully tested a powerful new intercontinental ballistic missile (ICBM) that put all of the US mainland within range, declaring it had achieved its long-held goal of becoming a nuclear power.

- Fed Powell, next chairman, has signaled an end to the era of ratcheting up regulation on US banks, saying the existing rules were “tough enough” to ensure a stable system and that there were ways to tailor the regime.

- New Zealand's central bank said it would unwind some restrictions on home loans to partly offset the impact of planned government curbs on the country's housing market, which has cooled in recent months.

- Today’s eco calendar contains German inflation, EC confidence indicators and US pending home sales. Fed Yellen, Dudley, Williams and ECB Weidmann are scheduled to speak. The Fed releases its Beige Book.

Currencies: Dollar And Sterling Rebound

USD gains modestly ground

Yesterday, EUR/USD and USD/JPY trading was initially confined to tight ranges, but USD momentum improved throughout the US session. US confidence data were strong, Fed nominee Powell in a hearing before the Senate advocated continuity and the Republican tax bill will be sent to the Senate. A new North Korea missile test couldn’t spoil the game. US equities set new records and the dollar rebounded, albeit modestly. EUR/USD closed the session at 1.1840 (from 1.1898). USD/JPY finished at 111.48

Overnight, Asian equities are mainly trading in positive territory. China again underperforms as Chinese authorities try to reduce leverage, but reversed earlier losses. Japanese retail data were again soft. USD/JPY touched an intraday top at the time of the publication of the data, but the impact was limited. The dollar eased slightly as the Asian trading evolved. USD/JPY trades currently in the 111.50 area. EUR/USD trades around 1.1855.The kiwi dollar is drifting south as the RBNZ contemplates easing restrictions on home loans. NZD/USD trades near 0.69.

In Europe, the EC economic confidence survey and the German November inflation data will be published. Economic confidence is expected to confirm recent good news from other surveys. German inflation is expected to have risen by 0.3% M/M and 1.7% Y/Y following a surprisingly soft outcome in October. We have no reasons to distance us from consensus. US data, revision of Q3 GDP and pending home sales, are less important. Later in the session, we expect the Fed’s Beige Book to paint an optimistic picture of the economy. Last but not least, Fed’s Yellen will testify before the JEC. She will likely ‘confirm’ that a Dec rate hike is in the pipeline, but recently she spoke cautious on inflation Earlier this week, we advocated not to row against the USD correction as long unless there was a clear positive trigger. Yesterday’s US news was positive, but the USD rebound not convincing. Today’s data are no game-changers, but might be slightly in favour of the euro. The testimony of Yellen and the progress on the tax bill are wild cards. Will she be ‘hawkish ‘enough to raise US yields and the dollar? We’re not convinced. Markets question the Fed’s rate hike intentions beyond December and it is unlikely that Yellen will change this market assessment. Stronger (price) data or other positive events (tax cuts) are needed for markets to reconsider a more USD positive scenario. Over the previous two days price action was a bit more USD constructive, but not good enough to qualify it as a U-turn. We stay dollar neutral.

From a technical point of view, EUR/USD set a post-ECB low mid-November, but on Friday regained the 1.1880 MT correction top. This break opened the way for a full retracement to the 1.2092 top. A return below 1.1713 would signal that the rebound in EUR/USD is aborted. The USD/JPY momentum was positive in October, but deteriorated this month. Last week, USD/JPY dropped below the 111.65 neckline. There was no aggressive follow-through selling, but the break makes the picture outright USD negative.

EUR/USD: rally aborted, but no clear correction signal

EUR/GBP

Sterling profits from positive Brexit headlines

There was no high profile news to guide sterling trading yesterday until late in the session. The BoE’s financial stability review indicated that UK banks will be able to cope with the consequences of a disorderly Brexit even if banks and the UK economy could suffer substantial costs in such a scenario. The Irish deputy Prime minister resigned, reducing chances for snap elections. Initially, this didn’t help sterling. After the European close, press sources indicated that the UK was prepared to go a long way in the direction of EU demands on the Brexit divorce bill. If so it would at least remove one of the key obstacles to start negotiations on the future trade relationship. EUR/GBP tumbled more than one big figure and closed the session at 0.8877. Cable finished the session at 1.3339. The rise was hampered by overall USD strength.

UK money supply and credit data will be published today. However, the focus for sterling trading will be on the Brexit story. An agreement in the divorce bill is an important step. The EU now expects the UK to come with a workable proposition on the issue of the Irish boarders. This won’t be easy, but markets will probably adapt positions for the December EU summit to give the green light for talks on the future relationship. Sterling might make some further progress.

MT view/technical picture. A BoE driven sterling rebound ran into resistance early this month. Sterling declined again as markets anticipated that the rate cycle would be very gradual and limited. EUR/GBP trades in a 0.8733/0.9033 consolidation range. Brexit headlines cause day-to-day gyrations. We changed our ST bias on EUR/GBP from positive to neutral two weeks ago. The 0.9015/33 area might be tough to break short-term. In case of more positive news on Brexit, return action to the 0.8733 (or below) level is possible ST.

EUR/GBP: returning south in the consolidation pattern on positive Brexit headlines

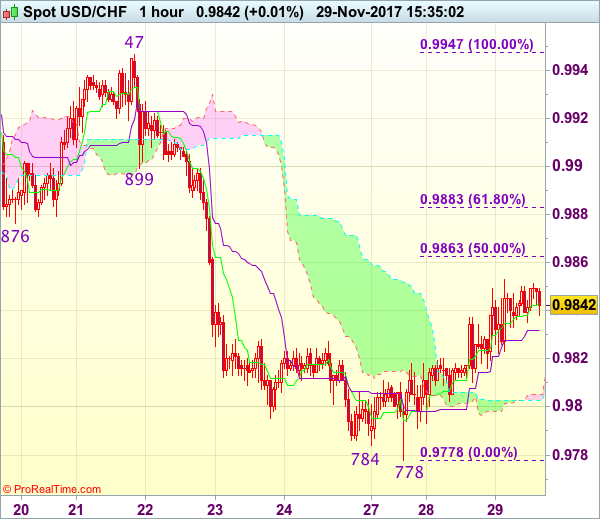

Trade Idea : USD/CHF – Sell at 0.9875

USD/CHF - 0.9839

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9842

Kijun-Sen level : 0.9832

Ichimoku cloud top : 0.9805

Ichimoku cloud bottom : 0.9803

Original strategy :

Sell at 0.9870, Target: 0.9770, Stop: 0.9905

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.9875, Target: 0.9775, Stop: 0.9910

Position : -

Target : -

Stop : -

Dollar’s rebound after falling to 0.9778 earlier this week suggests consolidation above this level would be seen and marginal gain from here cannot be ruled out, however, reckon upside would be limited to 0.9876 (previous support) and bring another decline later, below 0.9810 would bring a retest of said support at 0.9778, break there would extend recent decline from 1.1038 top towards 0.9730-37 support area but reckon support at 0.9705 would hold from here, bring rebound later.

In view of this, we are looking to sell dollar again on further subsequent recovery as previous support at 0.9876 should turn into resistance and limit upside. Only break of 0.9895-00 would defer and signal a temporary low is formed instead, bring a stronger rebound to 0.9920 but price should falter well below resistance at 0.9947.

Trade Idea : GBP/USD – Stand aside

GBP/USD - 1.3399

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.3378

Kijun-Sen level : 1.3314

Ichimoku cloud top : 1.3335

Ichimoku cloud bottom : 1.3331

Original strategy :

Exit long entered at 1.3280

Position : - Long at 1.3280

Target : -

Stop : -

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite falling briefly to 1.3221, as cable found renewed buying interest there and has staged another rally, suggesting the erratic rise from 1.3027 low is still in progress, hence near term upside bias remains for this move to extend father gain to 1.3425-30, however, overbought condition should prevent sharp move beyond previous resistance at 1.2455 and price should falter below 1.2475-80, bring retreat later.

In view of this, would not chase this rise here and would be prudent to stand aside in the meantime. Below 1.3355-60 would suggest an intra-day top is formed instead, bring weakness t the Kijun-Sen (now at 1.3315) but reckon downside would be limited to 1.3260-65, bring another rise later.

Trade Idea : EUR/USD – Hold long entered at 1.1845

EUR/USD - 1.1863

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.1854

Kijun-Sen level : 1.1874

Ichimoku cloud top : 1.1913

Ichimoku cloud bottom : 1.1899

Original strategy :

Bought at 1.1845, Target: 1.1945, Stop: 1.1810

Position : - Long at 1.1845

Target : - 1.1945

Stop : - 1.1810

New strategy :

Hold long entered at 1.1845, Target: 1.1945, Stop: 1.1825

Position : - Long at 1.1845

Target : - 1.1945

Stop : - 1.1825

The single currency met renewed selling interest at 1.1920 yesterday and slipped, however, as this move from 1.1961 is still viewed as retracement of recent rise, reckon downside would be limited to 1.1825-30 and bring another rebound later, above 1.1900 would bring test of said resistance at 1.1920 but break there is needed to signal the retreat from this week’s high at 1.1961 has ended, bring retest of this level first.

In view of this, we are holding on to our long position entered at 1.1845. Below 1.1825-30 would defer and risk weakness to 1.1805-10 (61.8% Fibonacci retracement of 1.1713-1.1961) but break there is needed to signal a temporary top has been formed at 1.1961, bring correction of recent rise to 1.1770-80.

Trade Idea : USD/JPY – Buy at 111.10

USD/JPY - 111.47

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 111.53

Kijun-Sen level : 111.37

Ichimoku cloud top : 111.27

Ichimoku cloud bottom : 111.14

Original strategy :

Buy at 111.00, Target: 112.00, Stop: 110.65

Position : -

Target : -

Stop : -

New strategy :

Buy at 111.00, Target: 112.00, Stop: 110.65

Position : -

Target : -

Stop : -

As the greenback found good support at 110.84 earlier this week and has rebounded, retaining our view that further consolidation above this level would be seen and corrective bounce to previous support at 111.88 is likely, however, reckon upside would be limited to 112.00-10 and price should falter below 112.35-40 and bring another decline later this week.

In view of this, we are still looking to buy dollar on dips. Below said support at 110.84 would signal recent decline is still in progress and may extend weakness to 110.70 and possibly towards 110.50 but loss of momentum should limit downside to 110.20-25 and reckon 110.00 would hold from here.

In The US, The Second Estimate Of GDP Growth In Q3 Is Due Out

Market movers today

Today is slightly more interesting than the past two days with inflation data out of Germany and Spain ahead of the euro inflation release tomorrow. In Europe , we also get consumer and business confidence indicators across countries today. In the US, the second estimate of GDP growth in Q3 is due out and the Fed is due to release its Beige Book.

Also in the US, Fed Chair Janet Yellen is due to appear before the Joint Economic Commit tee of Congress. However, given that markets have already priced in a December rate hike and Yellen is leaving the Fed soon, it is not really a market mover.

In the UK, BoE Governor Mark Carney and t he BoE’s Dave Ramsden are due to speak today.

In Sweden, the FSA is due to publish its Financial Stability Report , which is likely to mirror t he message from the Riksbank’s report published recently. We will also get consumer confidence where we will look for signs of whether the recent development in the housing market is spilling over to confidence.

Selected market news

Fed Chair nominee Jerome Powell’s confirmation hearing yesterday supported the view that he will stick to Yellen’s monetary policy strategy by continuing the gradualhiking cycle and ‘quanti tative tightening’ although admitting tthere may still be more slack left in the labour market. It was interesting that he was more vocal about his own target for the future level of the Fed’s balance sheet , which he thinks is between USD2,500 -3,000bn and should be reached within three to four years. In our view, this may be too optimistic, as we wrote in March earlier this year (see Research US: Fed’s regulatory hurdle for starting quantitative tightening, 13 March 2017).

As expected, the US Senate Budget Committee passed the Senate tax bi l l yesterday, meaning that there can be a full Senate vote as soon as Thursday. This is likely to be a very complicated process, as the Republicans can only afford to lose two votes (see e.g. Bloomberg).

Yesterday, The Telegraph wrote that EU and UK have agreed on the principle of the divorce bill , meaning that the UK is going to pay EU between EUR45-55bn after Brexit due to long-term liabilities, leading to a fall in EUR/GBP. Still, this may not be enough for the EU leaders to say there has been ‘sufficient progress’ in phase 1 of the negotiations (citizens’ rights, the divorce bill and Irish border) due to the increasing tension about the Ireland border issues. So, while the likelihood of a deal at the EU summit has increased, it is still not a given that the negotiations will move to phase 2 (future relationship). We st ill think it is st ill too early to price out Brexit risk premiums, as there are still many unresolved issues about what Brexit really means even if (when?) phase 1 is concluded. We st ill see EUR/GBP within the 0.8650- 0.90 range incoming months with risks becoming more balanced. In the absence of any further posit ive news today, we could see EUR/GBP climbing back above 0.89 again.

Risk sentiment in global financial markets has been mixed overnight following the advance in the US tax bill and North Korea launching another test missile.

Forex: North Korea Missile Test Fails To Rattle Markets

Earlier today, North Korea launched an ICBM that flew higher and further than any previous test firing. The missile was launched from just north of Pyongyang, reaching a height of nearly 3 kilometers and landed 600 miles east, in the Sea of Japan. This latest test firing, 2-months on from the last, is a direct challenge to President Trump, with the US Defense Secretary, James Mattis, commenting that the latest test firing demonstrates that North Korea has the ability to hit 'everywhere in the world'. Early comments from Trump have been that the US 'will handle' the situation. Trump also said, 'We will take care of it,' adding later that North Korea 'is a situation that we will handle.' This latest test appears to have had little effect on the markets with USD holding steady and only a slight demand for safe-haven Gold.

USD received a boost following news that the prospects for a US tax cut have improved after Senate Republicans forcibly pushed forward their bill in a partisan committee vote that set up a full vote by the Senate as soon as tomorrow, although details of the measure remained unclear. Republican leaders admitted that they have yet to round up the votes needed for passage in the Senate, where they hold a slim 52-48 majority.

Data released on Tuesday showed US consumer confidence has surged close to a 17-year high in November, due to a strong labor market, while house prices rose in September, which should underpin consumer spending and boost economic growth. The US Conference Board said its consumer confidence index increased 3.3 points to 129.5 in November, within striking distance of 132.6, which was touched in November 2000.

Jerome Powell, the Fed Chair nominee, appeared before the US Senate confirmation hearing on Tuesday and seemed to be continuing in his predecessor’s steps, stating that the case for a December rate hike 'is coming together'. Powell pledged to continue the Fed’s current approach to monetary policy, by gradually raising interest rates so long as economic growth remains healthy.

EURUSD is little changed overnight, currently trading around 1.1850.

USDJPY is unchanged in early Tuesday at trading around 111.52.

GBPUSD is 0.25% higher in early session trading at around 1.3367.

Gold is 0.15% higher, currently trading around $1,295.75.

WTI is 0.1% lower overnight, currently trading around $57.70.

Major data releases for today:

All Day: OPEC will host a meeting in Vienna, Austria with representatives from 13 oil-rich nations.

At 13:00 GMT: Destatis will release German Harmonized Index of Consumer Prices (YoY) for November. HICP is a measure of prices used by the Governing Council of the EU to define and assess price stability in the euro area as a whole in quantitative terms. The forecast is for a slightly higher release of 1.7%, compared to the previous 1.5%. Any significant deviation from forecast is likely to cause EUR volatility.

At 13:30 GMT: the US Bureau of Economic Analysis will release Gross Domestic Product Annualized for Q3. The forecast is for an improvement to 3.2% from the previous release of 3%. A higher release could see USD move higher, conversely, a lower than forecast release will see USD come under pressure.

Core Personal Consumption Expenditures (QoQ) for Q3 will also be released. As an important indicator of US inflation, forecasts are suggesting a higher release of 1.4% (prev. 1.3%), which will further confirm a growing US economy and a higher probability of a December rate hike from the Fed.

At 14:00 GMT: Bank of England Governor Mark Carney is scheduled to speak at the FMSB – Two Years on From the Fair and Effective Markets Review Event in London.

At 15:00 GMT: Federal Reserve Chair Janet Yellen is scheduled to testify on the economic outlook before the congressional Joint Economic Committee in the US.

At 15:30 GMT: the US Energy Information Administration will release Crude Oil Stocks change for the week ended November 24th. A higher drawdown of -3.150M is expected, compared to the previous draw of -1.855M. With OPEC meeting in Austria, the markets will be looking to see how crude oil stocks have changed in the world’s largest oil consuming nation and how that will affect the price of both WTI and Brent.

Euro At Risk Of Declines Vs Japanese Yen

Key Highlights

- The Euro is trading in a broad range above the 131.20 support area against the Japanese Yen.

- There is a crucial bearish trend line forming with resistance at 133.25 on the 4-hours chart of EUR/JPY.

- Japan's Retail Trade in Oct 2017 was unchanged, whereas the market was looking for a 0.2% rise (MoM).

- The US GDP figure for Q3 2017 will be released today, which is forecasted to grow by 3.2%.

EURJPY Technical Analysis

The Euro struggled to remain above the 133.00 handle against the Japanese Yen. The EUR/JPY pair moved down and remains at a risk of more declines toward 131.40.

Looking at the 4-hours chart of EUR/JPY, there is a crucial bearish trend line forming with resistance at 133.25. The pair recently traded as high as 133.23 and started a downside move. It traded below the 38.2% Fib retracement level of the last wave from the 131.22 low to 133.23 high.

On the downside, there is a major support forming near 132.40 and 131.20. It seems like the pair might continue to trade in a range above the mentioned support levels. On the upside, the pair needs to break the trend line resistance at 133.25-30 to gain bullish traction. On the flip side, a break below 131.00 could ignite further losses in the near term.

Japan's Retail Trade

Recently in Japan, the Retail Trade for Oct 2017 was released by the Ministry of Economy, Trade and Industry. The market was looking for a rise of 0.2% in Oct 2017 compared with the previous month.

However, the actual result was on the lower side as there was no change in the Retail Trade in Oct 2017. In terms of the yearly change, there was a decline of 0.2%, which was disappointing when compared to the last revised increase of 2.3%.

Overall, the result was negative and might help EUR/JPY in the short term.

Economic Releases to Watch Today

Euro Zone Consumer Confidence Nov 2017 – Forecast 0.1, versus 0.1 previous.

Euro Zone Services Sentiment Nov 2017 – Forecast 16.8, versus 16.2 previous.

Euro Zone Industrial Confidence Nov 2017 – Forecast 8.7, versus 7.9 previous.

Euro Zone Economic Sentiment Indicator Nov 2017 – Forecast 114.6, versus 114.0 previous.

German Consumer Price Index for Nov 2017 (YoY) (Prelim) – Forecast +1.7%, versus +1.6% previous.

German Consumer Price Index for Nov 2017 (MoM) (Prelim) – Forecast +0.3%, versus 0.0% previous.

US Gross Domestic Product Q3 2017 (Preliminary) – Forecast 3.2% versus previous 3.0%.

US Personal Consumption Expenditures Prices for Q3 2017 (QoQ) – Forecast +1.5%, versus +1.5% previous.

US Core Personal Consumption Expenditures for Q3 2017 (QoQ) – Forecast +1.4%, versus +1.3% previous.