Sample Category Title

AUDUSD Increasingly Bearish After Break Below 200-Day MA

AUDUSD continues its downward trajectory and is hovering at its lowest levels in more than 5 months. The outlook has turned increasingly bearish after the market broke below the 200-day moving average.

The recent bounce off 0.7531 (November 21 low) was capped at the 61.8% Fibonacci retracement level (0.7630) of the 0.7328 – 0.8124 rise. Breaking above this level would ease immediate downside pressure but prices would meet a resistance zone between 0.7693 – 0.7724 (200-day MA and 50% Fibonacci). Only a rise above 0.7900 would indicate the bearish phase has ended. Clearing the 0.8124 peak would see a resumption of the uptrend from May.

Failure to break above 0.7630 in the near term would keep downside momentum in play with scope to target 0.7460 before re-visiting the 0.7328 low and consequently erasing the May – September uptrend. Such a move would confirm the start of a new medium-term downtrend.

Technicals are pointing to a bearish bias. The RSI is below 50. The 50-day MA is falling and there is risk of an imminent bearish crossover with the 200-day MA.

RBA To Hike Benchmark Interest Rate Soon, Predicts OECD

For the 24 hours to 23:00 GMT, the AUD slightly declined against the USD and closed at 0.7600.

Yesterday, the OECD stated that the Australian economy will continue to expand at a robust pace, with the labour market strengthening further and added that the Reserve Bank of Australia (RBA) is expected to hike interest rate soon. The organisation predicted Australia’s GDP growth to be 2.5% in 2017, 2.8% in 2018 and 2.7% in 2019.

LME Copper prices declined 1.3% or $92.0/MT to $6800.0/MT. Aluminium prices declined 0.5% or $9.5/MT to $2100.0/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7584, with the AUD trading 0.21% lower against the USD from yesterday’s close.

The pair is expected to find support at 0.7571, and a fall through could take it to the next support level of 0.7559. The pair is expected to find its first resistance at 0.7608, and a rise through could take it to the next resistance level of 0.7633.

Going ahead, Australia’s HIA new home sales and building approvals data, both for October, scheduled to release overnight, would attract a lot of market attention.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

OECD Boosted Euro-Zone’s And Global Economic Growth Estimates, Urges Higher Business Investment To Maintain Global Growth

For the 24 hours to 23:00 GMT, the EUR declined 0.44% against the USD and closed at 1.1848.

In economic news, Germany's GfK consumer confidence index remained unchanged at 10.7 in December, in line with market expectations.

Meanwhile, the Organisation for Economic Cooperation and Development (OECD), in its latest economic outlook, lifted Euro-zone's growth forecast for this year and next, citing stronger growth in key European countries. The organisation expects the common currency region to grow 2.4% in 2017 and 2.1% in 2018, up from previous projections of 2.1% and 1.9% respectively. However, it further predicted that growth would sink back below 2.0% in 2019. The organisation also warned that the European Central Bank (ECB) should hold on raising interest rates before the end of the decade as raising rates too quickly “could weigh on the recovery in countries with high unemployment and large output gaps”.

Additionally, the OECD indicated that global economic growth in 2017 will be the best in seven years, but raised concerns about the longer-term outlook, citing “clear weaknesses and vulnerabilities”. Moreover, the Paris-based organisation expects the global economy to grow 3.6% in 2017 and 3.7% in 2018, before easing to 3.6% in 2019. Nevertheless, it warned that growth would slow from 2019 without new measures to promote business investment, productivity and more inclusive growth.

The US Dollar climbed against its key counterparts, following upbeat US consumer confidence data.

The CB consumer confidence index surprised to the upside, advancing to a nearly 17-year high level of 129.5 in November, amid optimism over the nation's labour market. In the prior month, the index had registered a revised level of 126.2, while markets had envisaged for a drop to a level of 124.0.

On the other hand, the nation's advance goods trade deficit widened more-than-anticipated to $68.3 billion in October, compared to market expectations for a deficit of $64.9 billion. In the prior month, the nation reported a trade deficit of $64.1 billion. Further, the nation's seasonally adjusted flash wholesale inventories unexpectedly dropped 0.4% on a monthly basis in October, defying market consensus for a gain of 0.4% and compared to an increase of 0.3% in the previous month.

The OECD inched up its growth outlook for the US economy, now expecting the world's largest economy to post a growth of 2.2% this year and 2.5% in 2018, stating that proposed tax cuts would give economic growth a temporary boost. However, growth is forecasted to slip back to 2.1% in 2019.

In the Asian session, at GMT0400, the pair is trading at 1.1854, with the EUR trading marginally higher against the USD from yesterday's close.

The pair is expected to find support at 1.1814, and a fall through could take it to the next support level of 1.1774. The pair is expected to find its first resistance at 1.1907, and a rise through could take it to the next resistance level of 1.1960.

Moving ahead, investors would draw their attention to Germany's flash consumer price inflation figures for November along with the Bundesbank monthly report, both due to release in a few hours. Moreover, the US annualised 3Q GDP, the Beige book report and pending home sales data for October, all set to release later in the day, will garner significant amount of investor attraction. Also, a speech by the Federal Reserve (Fed) Chair, Janet Yellen will keep investors on their toes.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Britain’s Banks Could Survive A ‘Disorderly Brexit’, Says Mark Carney

For the 24 hours to 23:00 GMT, the GBP rose 0.24% against the USD and closed at 1.3354, in the wake of a report which revealed that UK and the European Union (EU) have agreed a deal over Britain's Brexit divorce bill, which could unlock vital trade talks next month.

Meanwhile, the Bank of England (BoE) Governor, Mark Carney stated that leading financial institutions in Britain could cope up and even support Britain through a 'disorderly' Brexit. However, Carney stressed that this would be 'painful' as it would hamper households and businesses and hurt the nation's economic growth.

Separately, the OECD, in its latest global outlook, warned that the UK economy would continue to slow in 2018 and 2019, due to heightened uncertainty around Brexit and the impact of higher inflation on households. Economic growth in Britain is expected to grow 1.5% in 2017, before slipping down to 1.2% in 2018 and 1.1% in 2019.

In the Asian session, at GMT0400, the pair is trading at 1.3361, with the GBP trading a tad higher against the USD from yesterday's close.

The pair is expected to find support at 1.3259, and a fall through could take it to the next support level of 1.3157. The pair is expected to find its first resistance at 1.3425, and a rise through could take it to the next resistance level of 1.3489.

Ahead in the day, market participants would look forward to UK's net consumer credit and mortgage approvals data, both for October, slated to release in a few hours.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

BoJ Should Rethink On Monetary Policy If Inflation Remains Elusive

For the 24 hours to 23:00 GMT, the USD rose 0.41% against the JPY and closed at 111.50.

Yesterday, the OECD, warned that the Bank of Japan (BoJ) should reassess its loose monetary policy if it is unable to meet its inflation target for a prolonged time, otherwise it could end up holding too much government debt. The OECD slightly lowered Japanese economic growth forecast to 1.5% in 2017 and added that the nation’s economic growth is expected to slow from 2018 as the government provides less fiscal stimulus.

In the Asian session, at GMT0400, the pair is trading at 111.45, with the USD trading slightly lower against the JPY from yesterday’s close.

Overnight data revealed that Japan’s retail trade remained flat on a monthly basis in October, against market expectations for a rise of 0.2%. Retail trade had advanced 0.8% in the prior month. Meanwhile, the nation’s large retailers’ sales declined less-than-anticipated by 0.7% in October, compared to a gain of 1.9% in the prior month, while markets were anticipating for a fall of 0.8%.

The pair is expected to find support at 111.12, and a fall through could take it to the next support level of 110.78. The pair is expected to find its first resistance at 111.73, and a rise through could take it to the next resistance level of 112.00.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Swiss Franc Trading Marginally Lower, Ahead Of Swiss ZEW Expectations Data

For the 24 hours to 23:00 GMT, the USD rose 0.26% against the CHF and closed at 0.9838.

In the Asian session, at GMT0400, the pair is trading at 0.9841, with the USD trading a tad higher against the CHF from yesterday’s close.

The pair is expected to find support at 0.9816, and a fall through could take it to the next support level of 0.9792. The pair is expected to find its first resistance at 0.9859, and a rise through could take it to the next resistance level of 0.9878.

Investors would focus on Switzerland’s ZEW expectations index for November as well as the UBS consumption indicator for October, both set to release in a while.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Canada’s Economic Growth Forecasted To Slow Next Year: OECD

For the 24 hours to 23:00 GMT, the USD rose 0.39% against the CAD and closed at 1.2812.

Yesterday, the OECD projected the Canadian economy to accelerate 3.0% this year, before slowing to 2.1% in 2018 and 1.9% in 2019 as the nation's central bank withdraws policy stimulus.

Separately, in its latest financial system review, the Bank of Canada (BoC) warned that risks to the Canadian financial system remain elevated mainly due to vulnerabilities created by the nation's high household debt that are continuing to rise. However, these risks are expected to ease over time as a stronger economy and tighter mortgage requirements would help improve economic conditions.

In the Asian session, at GMT0400, the pair is trading at 1.2819, with the USD trading marginally higher against the CAD from yesterday's close.

The pair is expected to find support at 1.2774, and a fall through could take it to the next support level of 1.2730. The pair is expected to find its first resistance at 1.2844, and a rise through could take it to the next resistance level of 1.2870.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Market Update – Asian Session: Bitcoin Surges Past $10,000, Making Fresh Highs

Headlines/Economic Data

Asian equities markets trade mixed despite sharp gains seen in the US.

Gains in Japan and Korea capped amid North Korean missile and upcoming Bank of Korea policy meeting

Shanghai and Hong Kong markets trade generally lower

Asian steelmakers outperform

Semiconductor names continue to be pinned under Morgan Stanley note on the industry issued Monday

BTC/USD Continues its surge above $10,000 (fresh record high) and continues to extend gains

Japan

Nikkei 225 opened +0.6%; closed +0.5%

TOPIX Securities Index +1.7%; Nomura +1.7% (announced a new ¥100B principal investment fund, buyback)

Nomura: New principle business will provide funding for areas including corporate restructurings and MBOs; To inject up to ¥100B in the investment fund

Megabanks track earlier rise in US financials: Mitsubishi UFJ +2.5%, Mizuho +1.8%, Sumitomo Mitsui +1.5%

TOPIX Iron & Steel Index +2.7%; Steelmakers trade generally higher, JFE +4.5%, Nippon Steel +3.5% (broker commentary)

Some chip-related shares remain under pressure: Tokyo Electron -5.5%, SUMCO -0.7%

Yamaha Motor -3% (Yamaha Corp to lower stake)

Nikkei looks at BOJ's vulnerability to a stock market downturn given the ¥20.3T worth of equity ETFs sitting on its balance sheet

OECD thinks BOJ should maintain easing

JAPAN OCT RETAIL SALES M/M: 0.0% V 0.2%E; RETAIL TRADE Y/Y: -0.2% V 0.2%E

According to Japan Business Federation (Keidanren): to ask for 3% wage increase - Japan press

(JP) Nikkei looks at BOJ's vulnerability to a stockmarket downturn given the ¥20.3T worth of equity ETFs sitting on its balance sheet

Korea

KOSPI opened +0.1%, has since pared gains

Samsung Electronics -0.9%

North Korea: Confirmed fired new type of ICBM at HWASONG-15 that puts entire US in range; launch was successful

South Korea Pres Moon: South Korea will strengthen its capabilities against North Korean provocations

South Korea military conducts drills following earlier North Korea missile launch – South Korean Press

Bank of Korea (BOK) Deputy Gov Yoon: says North Korea impact on markets to be limited – South Korean Press (Note: The BoK is said to have held an unscheduled meeting earlier today amid the North Korean launch)

Looking ahead: The Bank of Korea is due to hold its regularly scheduled policy meeting tomorrow. The central bank is expected to raise rates by 25bps to 1.50%, according to one poll; Bank of Korea last raised rates in 2011

China/Hong Kong

Shanghai Composite opened +0.1%, Hang Seng -0.3%

Markets are currently in negative territory, as of the time of writing

Hang Seng Information Technology Index -1.1%; Semiconductor Manufacturing -2.4% (capital raise), Tencent -1%

Even still, Chinese steelmakers trading generally higher on supply constraints; Baosteel +2.6%

China property names, higher on Moody's report, Rated China property developers' sales rise strongly, amid slower national sales growth

(CN) China Banking Regulatory Commission (CBRC) official Yu Xuejun: China's economy is still facing relatively large downward pressure; economic stimulus measures have been overly strong

(CN) Turkey imposes anti-dumping duty on some China flat sleet products

(CN) China CIRC (Insurance Regulator): Q3 solvency was generally adequate; 167 insurers avg solvency ratio 253%

(CN) NDRC: China to promote long-term coal contract implementation for 2018 – Chinese Press

(CN) PBoC OMO: Injects CNY240B in 7, 14-day, 63-day reverse repos v CNY250B injected in 7,14 and 63-day reverse repos prior; Net: Nil v nil prior (3rd consecutive net nil)

(HK) Hong Kong Dollar (HKD) 1-month HIBOR 1.18927%, up over 5bps (highest since 2008)

Alibaba planning to sell 5.5, 10, 20, 30 and 40 year US dollar denominated bonds

Yuan denominated bond issuance: Originwater Technology [300070.CN] said to cancel CNY1B bond offering on market volatility

Philippines now targeting planned issuance of yuan-denominated ‘Panda Bonds’ in Q1 (had targeted 2017)

(CN) PBoC sets yuan reference rate at 6.6011 v 6.5944 prior

Looking Ahead: China Nov Official Manufacturing and Non-Manufacturing due for release on Thursday

Australia/New Zealand

ASX200 opened -0.1%, pared losses as session progressed; closed +0.4%

ASX 200 Utilities Index +1.6%, Consumer Discretionary +1.2%, Financials +0.7%, Resources +0.7%, Energy +0.7%

(AU) Australia sells A$900M v A$900M indicated in 2.75% Nov 21 2028 Bonds, avg yield, bid to cover 3.4x

(NZ) RBNZ semi-annual Financial Stability Report: financial system remains sound and risks to the system have reduced over the past six months

(NZ) RBNZ Spencer comments following release of Financial Stability Report: Does not have target for house price inflation; Expects extra 5K houses/year from Kiwibuild

OECD expects RBA to tighten in 2018 due to robust economic growth

(NZ) Fitch: New Zealand banks housing risk unlikely to up on easing of curbs

IDX.AU Capitol Health preparing unsolicited takeover offer at A$2.46/shr; +23%

Looking Ahead: Australia Q3 Private New Capital Expenditure data due for release on Thursday

Other Asia

(PH) Philippines Finance Sec Dominguez: Will reset panda bond offering to Q1 (had targeted 2017)

North America

US markets closed higher as Senate Budget Committee advanced tax bill: Russell 2000 +1.5%, Dow +1.1%, S&P500 +1%, Nasdaq +0.5%

S&P 500 Financial Sector +2.6%, Industrials Sector +1.5%

Tax Reform: (US) Senate Budget Committee advanced the tax bill; All 12 Republicans vote 'yes' including Senators Johnson and Corker; the 11 Democrats vote 'no'; The Budget Committee approval moved the bill to the full Senate, which could consider the bill later this week

Politics: (US) Congress unlikely to pass legislation this year to fund government agencies through Sept 30, 2018 – financial press; Therefore, Congress is likely to need a stop-gap, temporary funding legislation at least until late Jan to keep the federal government operating.

(US) Democratic leaders pull out of meeting with Trump on govt funding; will instead seek meeting with GOP leaders in Congress - press

Energy: Reportedly joint OPEC and non OPEC committee to support 9-month production cut extension (through 2018), with an option to review in June (as previously speculated)

(US) Weekly API Oil Inventories: Crude: +1.8M v -6.4M prior

Mexico Central Bank Chief: Board needs to take most recent information into account with decisions; board agrees on need to remain 'vigilant' and to be cautious on inflation outlook

After Market Movers: Marvell Technology [MRVL] +3% (Q3 results above ests, mid-point of Q4 guidance above ests); Autodesk [ADSK] -13% (reported financial results and guidance, announced restructuring measures)

Looking Ahead: Second reading of US Q3 GDP, Fed’s Yellen to testify before Congress, DOE weekly Crude Inventories

Europe

(UK) Reportedly UK and EU agree Brexit divorce bill with tab between €45-55B (vs. EU demands of €60B) - UK Telegraph

(UK) Govt official: do not recognize UK Telegraph newspaper account of Brexit negotiations

(UK) Brexit ministry spokesperson: we are exploring how to build on recent momentum in talks so that we can move negotiations to the next phase

M&A: Cineworld [CINE.UK]: Regal Entertainment confirms merger talks

Looking ahead: Spain and German Nov prelim CPI

Levels as of 01:00ET

Nikkei225 +0.4%, Hang Seng -0.2%; Shanghai Composite -0.5%; ASX200 +0.5%, Kospi -0.1%

Equity Futures: S&P500 -0.1%; Nasdaq100 -0.0%, Dax -0.0%; FTSE100 -0.0%

EUR 1.1856-1.1839; JPY 111.67-111.38; AUD 0.7608-0.7583;NZD 0.6904-0.6884

Dec Gold +0.0% at $1,295/oz; Jan Crude Oil -0.5% at $57.70/brl; Mar Copper +0.5% at $3.11/lb

Elliott Wave View: Dow Future

Dow Future Short term Elliott Wave view suggests that Intermediate wave (4) ended at 23204. The rally from there is proposed to be unfolding as a double three Elliott wave structure. Minute wave ((a)) of 1 ended at 23599 and Minute wave ((b)) of 1 ended at 23432. Near term focus is on 23828 – 23922 to complete Minute wave ((c)), and this should also end Minor wave 1 and cycle from 11/15 low. Afterwards, Index should pullback in Minor wave 2 in 3, 7, or 11 swing to correct cycle from 11/15 low before the rally resumes. We don’t like selling any proposed pullback and expect buyers to appear again once Minor wave 2 pullback is complete in 3, 7, or 11 swing provided pivot at 23204 low stays intact.

YM_F Dow Future 1 Hour Elliott Wave Chart

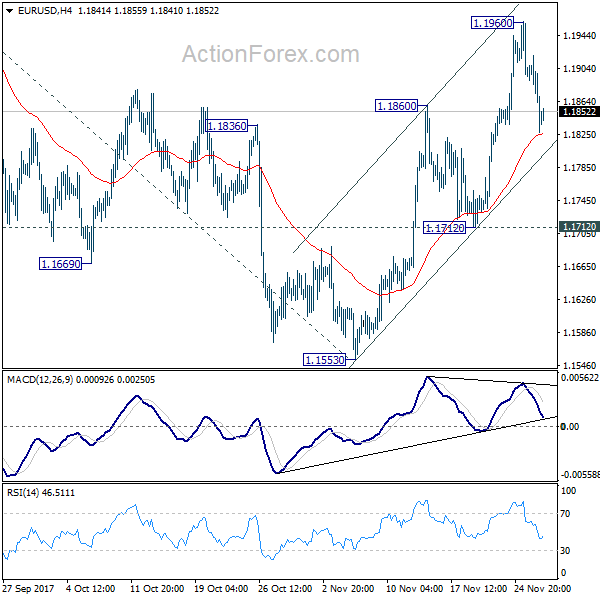

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1806; (P) 1.1863 (R1) 1.1899; More....

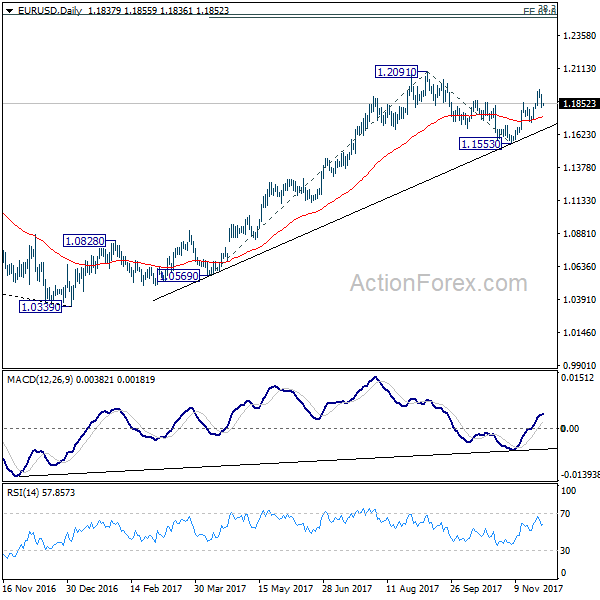

Intraday bias in EUR/USD remains neutral for consolidation below 1.1960 temporary top. As long as 1.1712 support holds, rise from 1.1553 is expected to continue. Above 1.1960 will target 1.2091 high first. Break there will resume medium term up trend from 1.0339 and target 61.8% projection of 1.0569 to 1.2091 from 1.1553 at 1.2494, which is close to 1.2516 long term fibonacci level. We'd expect strong resistance from there to bring reversal. On the downside, break of 1.1712 will indicate completion of the rise from 1.1553 and turn near term outlook bearish.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA (now at 1.1393) will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.