Sample Category Title

Strong US Data May Fail to Lift Dollar as Tax Plan Concerns Weigh

GDP estimates and data on personal consumption expenditures (PCE) are two keenly awaited releases this week in the United States as the December FOMC meeting approaches when a rate hike is widely anticipated. However, the data will likely get overshadowed by the Senate debate on the Republican tax plan, where a vote could come as early as November 30.

The US dollar remains vulnerable to negative developments on the tax front but solid economic indicators should provide some support at the very least even if they don't manage to lift the currency.

The second estimate of third quarter GDP is due on Wednesday, with an upward revision from 3.0% to 3.2% expected. The US economy has been gaining momentum this year, after growing only moderately in 2016. It is the first time since 2014 that annualized GDP growth has equalled or exceeded 3% for two consecutive quarters after growing by 3.1% in the second quarter.

Faster growth has yet to generate higher price pressures though, at least not according to the Fed's preferred measure of inflation – the core PCE price index. While headline CPI has risen above 2% in recent months, the core PCE price index has eased from 1.9% year-on-year at the start of 2017 to 1.3% in September. It is expected to tick higher to 1.4% in October in Thursday's data – still well below the Fed's 2% objective.

Thursday's PCE data will also include the latest personal income and spending figures. Personal income growth is forecast to moderate slightly from 0.4% to 0.3% month-on-month in October. Personal consumption is expected to see a sharper slowdown from 1% to 0.3%, but the drop is mainly due to the distortion seen in September when motor vehicle sales surged as a result of the damage caused by the hurricanes.

Any upside surprises to this week's data would only reinforce expectations that the Fed will raise the fed funds rate to a target range of 1.25-1.50% when it meets on December 12-13. But with a rate hike next month already priced in and with renewed concerns about a prolonged undershoot of inflation, the longer-term path of interest rates will likely be influenced by whether or not the tax plan is passed by Congress.

Investor angst about a possible delay or watering down of the tax plan has been weighing on the dollar recently, contributing to its month-long decline against the yen and other majors. Having passed the vote in the House of Representatives, the legislation has now moved to the Senate where Republican support is proving much trickier, especially as the party's majority is just two.

Reasons for opposition by some Republican Senators range from concerns about increasing the government deficit by $1.5 trillion over 10 years to demands for bigger tax cuts for pass-through businesses and displeasure for linking the bill with the repeal of the Obamacare individual mandate. It is thought there could be as many as 10 Republican Senators ready to oppose the bill in its current form if the Senate Budget Committee approves for the vote to go ahead on Thursday as expected.

Pressure is high on Republicans to pass the bill before the end of the year as President Trump badly needs a major legislative success for his first year in office. However, the rush to get it done before the year-end could jeopardise the tax plan by not giving lawmakers enough time to debate and improve the bill.

If the Senate postpones the vote this week or fails to pass it, the delay could add further downside pressure to the dollar, forcing a breach of the 111-yen handle. Failure to hold above 111 yen could trigger further declines towards the bottom of its 2017 range around 108 yen.

Consumer Confidence: Let the Party Continue

Consumer confidence surged to the highest level in 17 years, at 129.5 in November. Consensus was expecting a slight decline for the month. The Index was upwardly revised in October, from 125.9 to 126.2.

Consumers Enter the Holiday Season Upbeat

According to the Conference Board's Consumer Confidence Index, American consumers are heading into this year's holiday season with the highest confidence in 17 years. We have to go back to November of 2000 to see a higher consumer confidence level and this is no small feat. However, what is even better today is that consumer confidence back in November 2000 was actually coming down, while today's consumer confidence is still climbing. Not only is consumer confidence the highest in 17 years, it is also still improving compared to what was happening in November 2000.

The Present Situation Index was higher in November, up to 153.9 from a print of 152.0 in October, while the Expectations Index increased from 109.0 in October to 113.3 in November. According to the Conference Board's report, one of the biggest drivers of consumers' expectations was the improvement in the labor market.

Furthermore, both the assessment of business conditions as well as employment conditions improved during the month. Those considering business conditions as "good" improved from 34.4 percent to 34.9 percent, while those indicating business conditions were "bad" declined from 13.5 percent to 12.7 percent. Meanwhile, the assessment of the labor market also continued to improve. Those assessing that jobs were "plentiful" increased from 36.7 percent to 37.1 percent, while those that said jobs were "hard to get" decreased further, from 17.1 percent to 16.9 percent.

Perhaps the biggest issue is not how confident consumers are, but if they are willing to borrow in order to increase holiday purchases this year. Although consumer confidence has improved for several household income segments, it is still not homogeneous.

It is clear that those in the upper levels of income have been the most upbeat since late last year, while those in the lower income levels have had their issues with confidence.

Overall, as shown in the bottom graph, while consumer confidence has continued to improve and income expectations have followed through, disposable income growth has remained muted over the last year or so. Thus, consumers will have to continue to bring down the saving rate, as they have done for more than a year, and/or they will have to demand more credit to make this holiday season as merry as what the consumer confidence index has been indicating. Since, as we pointed out above, we are still in the upswing phase of consumer confidence, the probability that consumers will act on this higher confidence is high today.

EURGBP Advances on Weaker Pound

The cross advances on weaker pound and broke above barrier at 0.8955 (100SM, meeting next target at 0.8973 (Fibo 76.4% of 0.9013/0.8841). Today's action was supported by daily cloud base (0.8916) with fresh advance on track to form bullish outside day and generate signal for fresh upside. Daily techs are turning to full bullish setup and extension towards next targets at 0.9019 (15 Nov high) and more significant 0.9026 barrier (top of thick daily cloud). Sustained break above daily cloud (also former tops of 20/12 Oct) will be strong signal fur bullish continuation pf recovery leg from 0.8732 (01 Nov low). Cloud base is expected to hold and keep bulls in play.

Dollar Moves Higher as US Consumer Confidence Touches 17-Year High; Irish Worries Ease

The day's main release pertained to US consumer confidence figures released late in the session. Those came in at a multi-year high, creating a positive backdrop for the greenback for the remainder of the day. Beyond this, new Fed chief Jerome Powell appearing before US senators, US tax reform deliberations and developments that could affect the outcome of Brexit negotiations were also gathering attention.

Powell's confirmation hearing before the Senate Banking Committee has begun at 1500 GMT, with senators having the opportunity to pose questions; market moving comments are not to be ruled out. Through his prepared remarks, which were released during late US session yesterday, he supported a gradual rise in interest rates, representing an element of continuity from Janet Yellen. He also indicated willingness to move "decisively" against "new and unexpected threats" to the economy, while making reference to flexibility and independence from political interference in policy setting. Powell is set to succeed Fed chair Yellen once her term expires in February.

US tax reform is also on the forefront with President Trump holding discussions with Senate Republicans to steer developments in the direction his administration desires. The US Senate will be debating the tax-cut bill with a vote potentially taking place on Thursday.

The dollar index was 0.3% up on the day at 1532 GMT, distancing itself from yesterday's two-month low of 92.50. Dollar/yen was 0.2% higher at 111.30, but not far above yesterday's two-and-a-half-month low of 110.83. Euro/dollar traded 0.1% lower at 1.1879 after touching 1.1960 on Monday, a level last experienced in late September.

The US Conference Board's consumer confidence index for the month of November surprised to the upside, coming in at 129.5 to hit a fresh 17-year high, contrasting expectations for a minor slowdown to 124.0. October's reading was also revised upwards to 126.2 from 125.9. The US currency recorded gains relative to major rivals following the release.

Earlier in the day, the S&P Case-Shiller home price index showed house prices rising in September with the broadest indicator recording an increase by 6.2% y/y, advancing at a slightly faster pace than analysts' projections of 6.1%. August's respective reading was revised to 5.8% from the previous 5.9%. The index is advancing "at the fastest annual rate since June 2014" said S&P Dow Jones indexes managing director David Blitzer, while stating that indicators support the case for additional gains in home prices. Dollar/yen didn't react much within the first minutes of data release.

Unlike the year before, the Bank of England's stress tests for the current year saw all banks pass. The central bank also said that UK banks can withstand a disorderly Brexit, while acknowledging the costs from such an outcome. In addition, effective next November, the BoE doubled the counter-cyclical buffer large banks must hold to 1.0%. This is to be reviewed next year and is estimated to result in an increase in costs by around 6 billion pounds (close to $8bn).

The Irish border issue, a key consideration and one holding Brexit discussions back from moving to the next level, was getting even more complicated in recent days with the Irish government being at the brink of collapse. The party supporting the minority government was demanding the resignation of deputy prime minister Frances Fitzgerald over a police scandal in order to continue backing the government. Fitzgerald decided to resign today, perhaps easing the UK government's concerns as it was given a December 4 deadline to present improved positions on the key Brexit issues in order for EU leaders to approve the beginning of talks on trade relations between Britain and the EU during the December 14-15 summit. Pound/dollar was last 0.4% down on the day at 1.3262 and euro/pound traded 0.25% up at 0.8955.

Dollar/loonie was 0.3% up on the day and just above the 1.28 handle ahead of the Bank of Canada's Governor Stephen Poloz and Senior Deputy Governor Carolyn Wilkins participating in a press conference at 1630 GMT.

In commodities, gold was flat at $1,294.60 an ounce. Yesterday, it came close to the $1,300 level, recording a one-and-a-half-month high. WTI and Brent crude were lower by 0.1% and 0.3% at $58.04 and $63.64 per barrel respectively. The API weekly report which includes information on US crude stocks is due at 2130 GMT.

Yen Gains Ground, Investors Eyeing Powell Testimony

The Japanese yen has posted gains in the Tuesday session. In North American trade, USD/JPY is trading at 111.31, up 0.18% on the day. In the US, CB Consumer Confidence jumped to 129.5, above the estimate of 123.9 points. Fed Chair Designate Jerome Powell is testifying at his confirmation hearing before the Senate Banking Committee. Later, in the day, Japan releases Retail Sales, which is expected to slow to 0.1%. On Wednesday, the US publishes Preliminary GDP and Pending Home Sales and Janet Yellen will testify before a congressional committee.

The changing of the guard at the Federal Reserve has kicked off on Tuesday, as Jerome Powell is testifying before the Senate Banking Committee. Investors will be listening closely, as Powell faces questions from lawmakers about his plans as head of the powerful central bank. Powell is widely expected to maintain Janet Yellen's cautious monetary stance, which has been marked by small, incremental rate hikes. Powell inherits an economy that is in excellent shape, but persistently low inflation remains a nagging problem. Fed policymakers have differing views on what to do about inflation, with some members proposing that the Fed drop its 2 percent target, in favor of a "gradually rising path" for prices. The Fed remains confounded by low inflation and wage growth, despite a labor market that is at full capacity. Still, the Fed will likely pull the rate trigger next month, and could raise rates up to 3 more times in 2018 if the economy continues to expand at its current pace.

With the Japanese economy showing moderate growth, there has been speculation that the Bank of Japan is giving some thought to tapering its massive stimulus program. Any tapering to the program could give a significant boost to the yen, so the markets are closely monitoring BoJ statements and comments from BoJ policymakers, looking for clues. However, a stronger yen would hurt exports, which has been a catalyst for the stronger economy. Inflation and wage growth remain low, and if we are to take BoJ Governor Haruhiko Kuroda at his word, the Bank will not taper stimulus before inflation moves closer to the BoJ's target of around 2 percent.

Elliott Wave analysis: USDMXN and NZDUSD Update

Good day traders.

USDMXN is trading in a clear bearish impulse, with recent bullish reversal being part of wave 4). This wave 4) can look for resistance near the Fibonacci ratio of 38.2 and 50.0 and near former swing high of one minor degree wave four and there make a new drop lower.

USDMXN, 1H

NZDUSD is recovering, now seen in wave 5 of A) which is approaching the upper line of an EW channel and some Fib. resistance level that can limit current bullish leg. We know that after every five waves market turns, so traders should be prepared on a three wave set-back, lower into wave B).

NZDUSD, 1H

GBPUSD – Penetration of Daily Cloud Signals Extended Correction

Cable remains under pressure in the American session and cracked daily cloud top which marks solid support at 1.3276.

Weakening near-term studies favor firm break through cloud top (cloud is spanned between 1.3276 and 1.3214) and test of next significant support at 1.3260 (converged 10/55SMA's). Daily techs show further room for extended pullback with break below 1.3260 to risk test of cloud base (1.3214) reinforced by daily Kijun-sen).

The latter is required to contain extended correction and keep in play fresh upside attempts as 1.3415 Fibo barrier still acts as valid target.

Res: 1.3276; 1.3300; 1.3357; 1.3382

Sup: 1.3260; 1.3214; 1.3203; 1.3185

USD Decline Halts, For Now

- European equities had a constructive session today, but still stick to a narrow sideways range following a substantial sell-off in the first half of November. US equities open with small gains.

- Loans to businesses across the eurozone increased at their fastest rate since the financial crisis in October, underscoring the recovery in demand across the bloc as the ECB prepares to scale back its stimulus programme. French consumers brightened their outlook in November after four months of declining confidence.

- Raising interest rates before the end of the decade could threaten the long-sought after economic recovery in the eurozone, the OECD has warned. It does not expect the European Central Bank to begin raising rates until 2020 given below-target inflation and continuing slack in local labour markets.

- Ireland averted an election that could have derailed crucial Brexit talks with the U.K., as Deputy Prime Minister Fitzgerald agreed to resign and end a five-day political stand-off

- All OPEC members support extending their oil production cuts until the end of 2018, although Russia hasn't yet committed to the proposal before Thursday's meeting in Vienna, said people familiar with the matter. Brent oil trades at $63.45/barrel, a daily loss of 40 cents.

- The prospect of Brexit will continue to weigh on Britain's economic performance over the next two years, while creating risks and opportunities for other European countries, the OECD said on Tuesday.

Rates

Another sideways trading session

The Bund traded in a tight 20 ticks range between 163.10 and 163.30, now quoted in the middle of that range. The short end slightly underperformed, but the differences are marginal. US Treasuries traded virtual unchanged until a small move higher after a much higher than expected trade deficit was reported. It may weigh somewhat on Q4 GDP growth. However, even this move was negligible even in an intra-day perspective. Other markets gave little impetus. The dollar was fractionally higher, oil lower and European equities moderately higher. None had noticeable impact on core bonds. European data remained encouraging, but were also unable to affect trading. At the time of closing our report, Fed chairman nominee Powell will appear for a hearing before the Senate banking Committee and the consumer confidence (Conference board) will be released. A 7-yr T-Note auction takes place later this evening. Surprises are possible but unlikely.

At the time of writing, the German yield curve shows little moves with yield changes ranging between +0.5 bp (2-yr) and -0.2 bp (10-yr). The US yield curve trades within 1 bp lower across the curve. On intra-EMU bond markets, yield spreads are again virtually unchanged. Irish bonds didn't react to the resolution of the political crisis (which didn't weigh on Irish bonds in the first place).

Currencies

USD decline halts, for now.

EUR/USD and USD/JPY trading was confined to very tight ranges today. Eco data were few and unable to give trading firm direction. The dollar stayed away from yesterday's ST correction low against the euro and the yen, but it's too early to assume that a bottoming out process is in place.

Overnight, the correction on Asian equity markets that started last week slowed. Chinese equities even succeeded a late session rebound and finished the session in positive territory. USD/JPY traded stable in the low 111 area. EUR/USD hovered in the 1.19 area.

European equities initially didn't know which way to go, but finally joined the positive trend from China. However, the developments on the equity markets again failed to give any clear guidance for trading in bonds and FX markets. EMU money supply and lending data were constructive, but broadly as expected. USD/JPY and EUR/USD held extremely tight ranges close to the starting levels in Europe.

The US trade deficit was substantially bigger than expected ($ 68.3 b vs $64.9 b expected) both due to lower exports and higher imports. The higher trade deficit might reduce the Q4 US growth. Evens so, the report had no noticeable impact on the dollar. FX traders are apparently mainly focused on the US tax debate and on more important figures scheduled for release later this week. After the closure of our report, nominee Fed chair Powell will be questioned before the US Senate. US consumer confidence might also still affect the dollar. EUR/USD trades currently in the 1.1890 area. USD/JPY trades near 111.25.

Sterling losing ground in technical trade

There was again no dominant story to guide sterling trading today. The BoE in its financial stability review indicated that UK banks will be able to cope with the consequences of a disorderly Brexit. Still banks and the UK economy could suffer substantial costs in such a scenario. We didn't seen any high profile new insights in today's BoE assessment. In Ireland, the deputy Prime minister resigned, reducing chances for snap elections. This should also avoid additional problems as the EU and the UK seek for a solution for the UK/Irish boarder. However, it didn't help sterling. The UK currency traded with a negative intraday bias. Technical considerations might have been in play. Cable yesterday tested the top of a MT consolidation pattern. This test was rejected. Maybe this caused some profit taking on ST sterling longs. EUR/GBP gradually extended its rebound north of 0.89. The pair trades again in the mid 0.89 area.

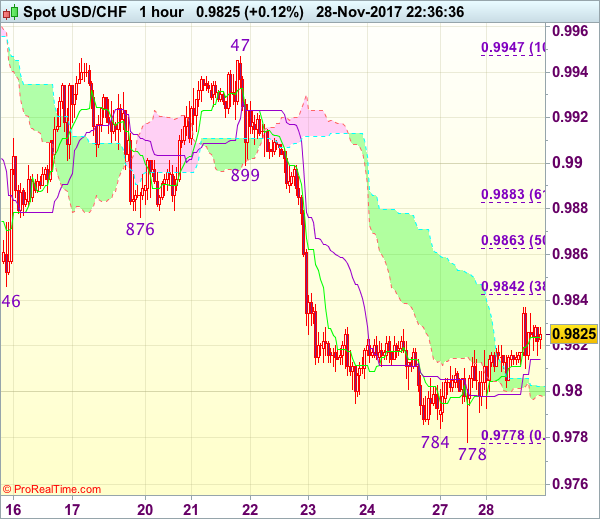

Trade Idea Wrap-up: USD/CHF – Sell at 0.9870

USD/CHF - 0.9833

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9824

Kijun-Sen level : 0.9814

Ichimoku cloud top : 0.9803

Ichimoku cloud bottom : 0.9798

Original strategy :

Sell at 0.9855, Target: 0.9745, Stop: 0.9890

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.9870, Target: 0.9770, Stop: 0.9905

Position : -

Target : -

Stop : -

As dollar has rebounded after falling to 0.9778 yesterday, suggesting consolidation above this level would be seen, however, reckon upside would be limited to 0.9846 (previous support) and 0.9860-70 should hold, bring another decline later, below said support at 0.9778 would extend recent decline from 1.1038 top towards 0.9730-37 support area but near term oversold condition should limit downside and reckon support at 0.9705 would hold from here, bring rebound later.

In view of this, we are looking to sell dollar again on recovery as previous support at 0.9876 should turn into resistance and limit upside. Only break of 0.9895-00 would defer and signal a temporary low is formed instead, bring a stronger rebound to 0.9920 but price should falter well below resistance at 0.9947.

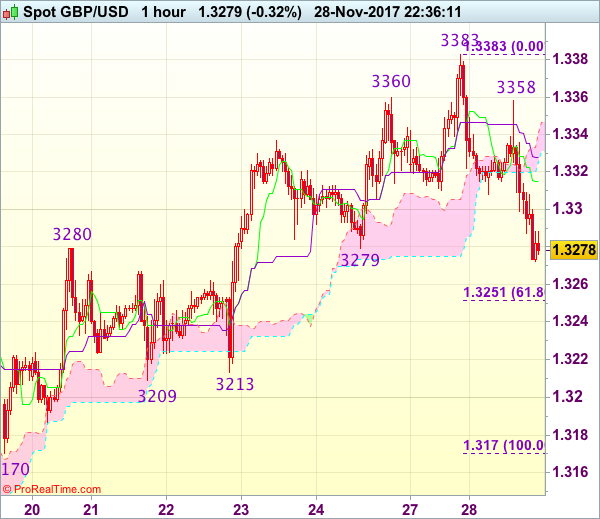

Trade Idea Wrap-up: GBP/USD – Exit long entered at 1.3280

GBP/USD - 1.3275

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.3312

Kijun-Sen level : 1.3325

Ichimoku cloud top : 1.3341

Ichimoku cloud bottom : 1.3326

Original strategy :

Bought at 1.3280, Target: 1.3380, Stop: 1.3245

Position : - Long at 1.3280

Target : - 1.3380

Stop : - 1.3245

New strategy :

Exit long entered at 1.3280

Position : - Long at 1.3280

Target : -

Stop : -

As cable ran into renewed selling interest at 1.3358 and has slipped again, dampening our bullishness and suggesting a temporary top has been formed at 1.3383, hence downside risk remains for weakness to 1.3250-55 (61.8% Fibonacci retracement of 1.3170-1.3383), however, still reckon downside would be limited to 1.3230 and support at 1.3209-13 would hold from here, bring rebound later.

In view of this, would be prudent to exit long entered at 1.3280 and stand aside for now. Above the Tenkan-Sen (now at 1.3312) would bring test of the Kijun-Sen (now at 1.3325) but only break of said resistance at 1.3358 would revive bullishness and signal the retreat from 1.3383 has ended, bring retest of this level first.