Sample Category Title

Markets Quiet But Dollar Under Pressure

Another eventful trading week is slowly coming to an end with global stocks mostly mixed today, as investors sit on their hands ahead of the weekend.

Asian markets closed mostly mixed on Friday, while European stocks struggled for direction after the Thanksgiving holiday in the United States on Thursday. Although Wall Street will be open this afternoon, a subdued session is expected thanks to the lingering holiday mood.

Dollar in the dumps

It has certainly been another painful week for the US Dollar which has found itself at the mercy of low inflation concerns.

The Dollar sulked against a basket of major currencies on Friday with prices trading towards 93.00, after the minutes from the latest FOMC meeting expressed concerns among some policymakers over stubbornly low inflation. With uncertainty likely to mount over the US rate outlook beyond 2017, amid Fed inflation concerns, it could translate into more pain for the Dollar. Taking a look at the technical picture, the Dollar Index is under extreme pressure on the daily charts with the next levels of interest at 93.00 and 92.80, respectively.

Sterling offered shaky lifeline

Sterling bulls have found support this week in the form of a vulnerable US Dollar.

Although the GBPUSD is currently trading above 1.3300 as of writing, investors should keep in mind that this has nothing to do with a change of sentiment towards the Sterling. With the Office for Budget Responsibility (OBR) downgrading growth this year as well as coming years through 2022 and Brexit uncertainty weighing on sentiment, Sterling bulls are trapped. It may take more than a vulnerable Dollar to sustain the current uptrend, with technical traders paying close attention to how prices behave around 1.3300. A breakdown below this level may encourage a further decline towards 1.3230 and 1.3150 respectively. Alternatively, if the current upside holds above 1.3300, then 1.3340 and 1.3370 will act as levels of interest.

Commodity spotlight - Gold

Gold hovered above $1289 during Friday's trading session on the back of a depressed US Dollar. With concerns over prolonged periods of low inflation weighing on the prospects of higher US rates beyond 2018, the zero-yielding metal could receive a boost. Taking a look at the technical picture, prices are trading above the 50 Simple Moving Averages, while the MACD has also crossed to the upside. Previous resistance at $1289 could transform into a support that encourages a further incline towards $1300. Alternatively, a failure for bulls to keep above $1289 should open a path back towards $1280.

US oil prices sprint to two-year highs

The shutdown of a major crude pipeline from Canada to the United States has instilled WTI Crude bulls with enough inspiration to send the commodity to its highest level in over two years - above $58.50. Optimism over OPEC members extending production cuts beyond March 2018 has also played a role in oil's incredible resurgence. While further upside could be on the cards short term, it will be interesting to see how markets react to the rising output from US Shale in the longer term.

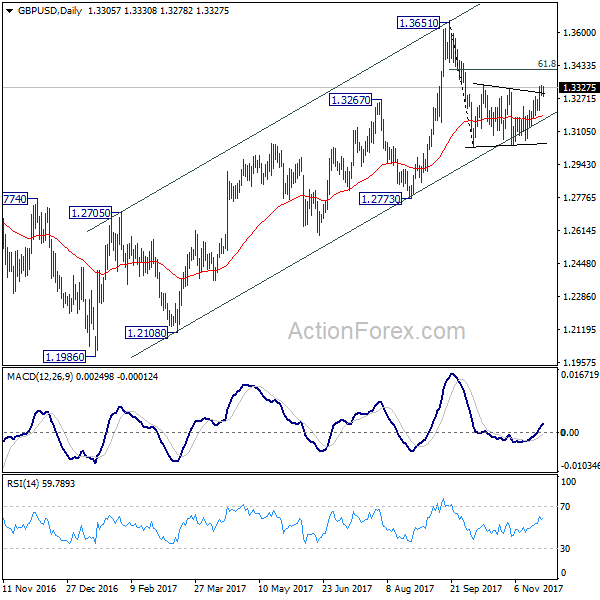

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3277; (P) 1.3307; (R1) 1.3333; More....

Focus in GBP/USD remains on 1.3337 resistance. Firm break there will argue that whole decline from 1.3651 is completed. And further rise should then be seen to 61.8% retracement of 1.3651 to 1.3026 at 1.3412 first. Sustained break there will target a test on 1.3651. On the downside, though, break of 1.3212 minor support will turn bias back to the downside for retesting 1.3026 instead. And in this case, decline from 1.3651 will likely extend lower.

In the bigger picture, as noted before, GBP/USD hit strong resistance from the long term falling trend line. Current development is starting to favor that corrective rebound from 1.1946 low has completed at 1.3651. Decisive break of 1.2773 will confirm this bearish case and target a test on 1.1946 low next, with prospect of resuming the low term down trend. Nonetheless, break of 1.3320 resistance will restore the rise from 1.1946 for 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

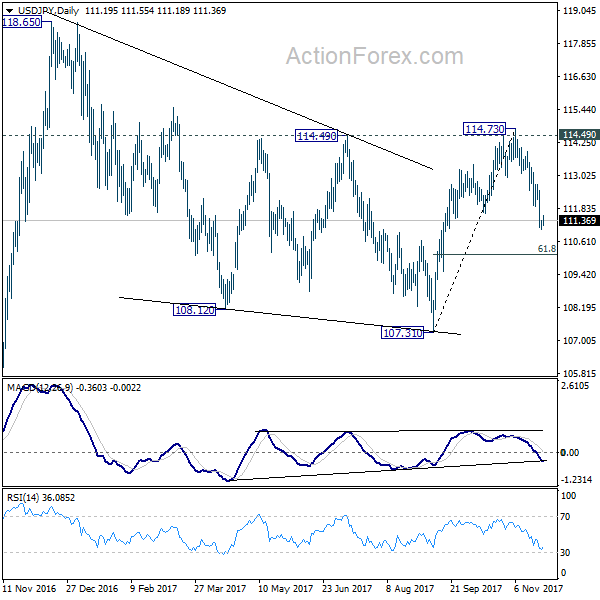

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 111.06; (P) 111.21; (R1) 111.37; More...

At this point, deeper decline is expected in USD/JPY with 112.71 resistance intact. Fall from 114.73 would target 61.8% retracement of 107.31 to 114.73 at 101.14. For the moment, we're still favoring the case medium term corrective pattern from 118.65 has completed at 107.31 already. Hence, we'll looking for bottoming below 101.14 to bring another rise. On the upside, break of 112.71 resistance will indicate that the fall from 114.73 is completed and turn bias back to the upside.

In the bigger picture, medium term rise from 98.97 (2016 low) is not completed yet. It should resume after corrective fall from 118.65 completes. Break of 114.49 resistance will likely resume the rise to 61.8% projection of 98.97 to 118.65 from 107.31 at 119.47 first. Firm break there will pave the way to 100% projection at 126.99. This will be the key level to decide whether long term up trend is resuming. However, firm break of 111.64 support will dampen this view and turn focus back to 107.31 instead.

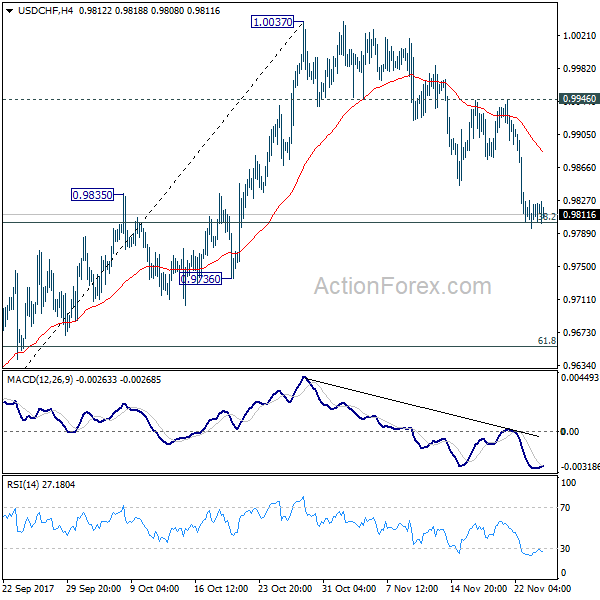

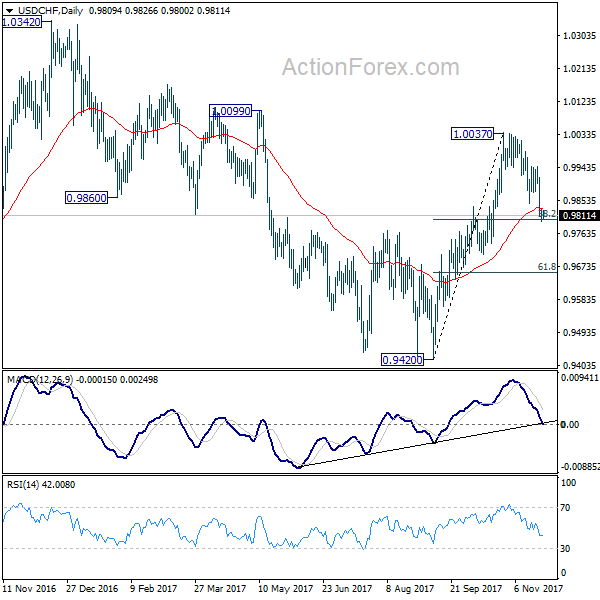

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9795; (P) 0.9811; (R1) 0.9828; More....

Intraday bias in USD/CHF stays on the downside for deeper decline. As noted before, the rebound from 0.9420 could have completed at 1.0037 already. Further fall would be seen to 61.8% retracement of 0.9420 to 1.0037 at 0.9565. We'll look for bottoming again below 0.9565. On the upside, break of 0.9946 resistance will indicate that the decline from 1.0037 has completed and bring retest of this resistance.

In the bigger picture, current development suggests that USD/CHF has defended 0.9443 (2016 low) key support level again. Rise from 0.9420 could be a medium term up move and should target a test on 1.0342 high. This represents the upper end of a long term range that started back in 2015. In case pull back fro 1.0037 extends, we'd still expect the long term support at 0.9420 to hold.

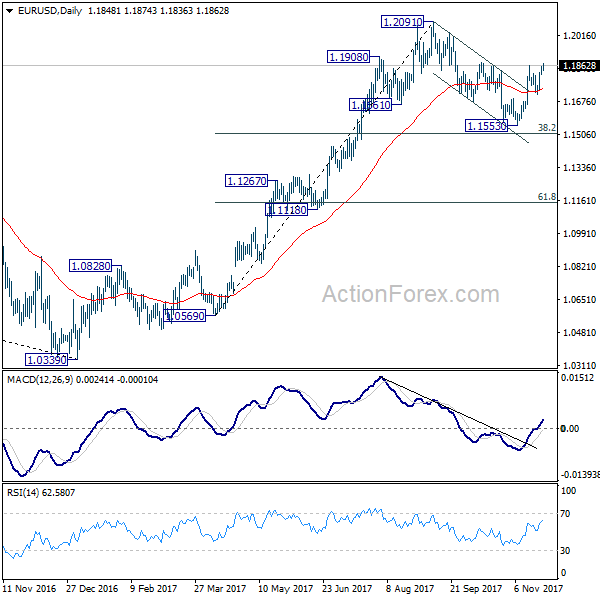

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1822; (P) 1.1839 (R1) 1.1865; More....

Break of 1.1860 resistance indicates that EUR/USD's rally from 1.1553 has completed. Intraday is back on the upside for retesting 1.2091 high. Decisive break there will resume medium term rally from 1.0339. On the downside, break of 1.1712 support is needed to indicate completion of the rebound. Otherwise, outlook will stay bullish in case of retreat.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be cautious on 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA (now at 1.1373) will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

Euro Soars again as German Ifo Hit Record High

Euro strengthens again today as boost by strong confidence data. German Ifo business climate hit a record high. Additionally, there is positive political news out of Germany as the Social Democrats announced to enter into talk with Chancellor Angela Merkel. Dollar pared back some losses against all but Euro and Sterling. But the greenback will still likely end the week as the weakest one. Meanwhile, Japanese Yen lost much ground as risk appetites returned to global markets. Yen and Canadian Dollar could end as the weakest ones together with Dollar.

German Ifo hit record high, economy on track for a boom

German Ifo business climate jumped to 117.5 in November up from 116.8 and beat expectation of 116.5. More importantly, that's the highest reading on record. Expectation gauge rose to 111.0, up from 109.2, beat expectation of 108.8. Current assessment gauge, however, dropped to 124.4, down from 124.8 and missed expectation of 125.0. Ifo head Clemens Fuest said that "sentiment among German businesses is very strong." And, "this was due to far more optimistic business expectations. The German economy is on track for a boom." However, it remains to be seen if the upbeat sentiments could continue as the country is facing some political risks after the collapse of coalition talk.

Social Democrats: Talks have to take place

Euro is also supported by news that Germany's Social Democrats are ready to talk with Chancellor Angela Merkel and her CDU/CSU bloc. SPD announced, after an eight-hour marathon meeting between its leaders, that "the SPD is firmly convinced that talks have to take place. The SPD is not closed to talks." Nonetheless, deputy party leader, Manuela Schwesig emphasized that "just because we say we are open to talks doesn't mean that these are automatically talks about a grand coalition, and it is certainly not a vote in favour of a grand coalition." It's reported that SPD are considering two options. One option is to back Merkel's minority government for certain key votes, like budget and EU poly. Another option is reformation of the grand coalition.

UK May in Brussels to meet EC Tusk

UK Prime Minister arrived in Brussels for a meeting with European Council Donald Tusk. She told reporters after the meeting that "these negotiations are continuing but what I am clear about is that we must step forward together. This is for both the UK and the European Union to move on to the next stage." It's believed that May is willing raise the divorce bill offer but only if EU agrees to start talks on trade agreement and transition period. However, EU leaders could be bounded to consult their national parliaments before making such a guarantee. And most likely, the member states won't be willing to "rubber-stamp" an offer".

UK consumer confidence hit post Brexit referendum low

Staying in UK, a consumer index by YouGov and the Centre for Economics and Business Research sank sharply from 109.3 to 106.6 in November, hitting the lowest level since the Brexit referendum. CEBR economist Christian Jaccarini linked the deterioration to factors like BoE hike and a slowdown in housing. He said that "the first interest-rate hike in over a decade triggered fears that higher borrowing costs will compound the inflation-induced squeeze on household incomes." And. "with these economic headwinds set to persist, and the OBR forecasting weaker growth, households are understandably worried."

Japan PMI manufacturing posted strongest improvement since 2014

Japan PMI manufacturing rose to 53.8 in November, up from 52.8 and beat expectation of 52.6. That's the strongest improvements for 44 months since March 2014. Markit economists Joe Hayes noted that "new orders increased strongly, underpinned by business from abroad amid recent yen weakness. New export orders expanded at the fastest pace in almost four years." However, he also warned that " cheaper yen and higher material prices have intensified cost pressures, as input price inflation increased to a 35-month high in November."

New Zealand trade deficit narrowed despite record imports

New Zealand trade deficit narrowed to NZD -871m in October, larger than expectation of NZD -750m. Imports surged to a record high at USD 5.4b, but that was offset by rise in exports to NZD 4.56b. Jump in imports include intermediate goods, used as ingredients or inputs into the production of other goods and services. Meanwhile dairy and lamb shipments were the key drivers of export growth.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1822; (P) 1.1839 (R1) 1.1865; More....

Break of 1.1860 resistance indicates that EUR/USD's rally from 1.1553 has completed. Intraday is back on the upside for retesting 1.2091 high. Decisive break there will resume medium term rally from 1.0339. On the downside, break of 1.1712 support is needed to indicate completion of the rebound. Otherwise, outlook will stay bullish in case of retreat.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be cautious on 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA (now at 1.1373) will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Trade Balance Oct | -871M | -750M | -1143M | -1156M |

| 0:30 | JPY | PMI Manufacturing Nov P | 53.8 | 52.6 | 52.8 | |

| 9:00 | EUR | German IFO Business Climate Nov | 117.5 | 116.5 | 116.7 | 116.8 |

| 9:00 | EUR | German IFO Expectations Nov | 111 | 108.8 | 109.1 | 109.2 |

| 9:00 | EUR | German IFO Current Assessment Nov | 124.4 | 125 | 124.8 | |

| 14:45 | USD | Manufacturing PMI Nov P | 55 | 54.6 | ||

| 14:45 | USD | Services PMI Nov P | 55.4 | 55.3 |

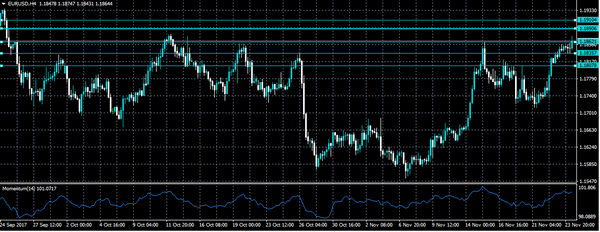

EURO Buyers In Control Above 1.1835 Level

The euro currencies advance against the U.S dollar continued in the European trading session, hitting 1.1874 as buyers stayed heavily long into the U.S session. EURUSD price-action is now holding above the 1.1862 technical support level, with buyers possibly targeting the next up-leg, towards the 1.1900 handle. However, with a distinct lack of high-impact macro-economic data from North America, the daily trading-range for the EURUSD may continue to remain confined, with the weekly price-high already reached.

Should EURUSD price-action break above the 1.1874 level, further upside towards the 1.1890 and 1.1910 level appears most likely.

A loss of the 1.1835 technical level may see EURUSD price-action push-back towards the 1.1807 support level.

GBPUSD Still Intraday Bullish Above 1.3307 Level

The British pound continues to hold above the 1.3307 level against the U.S dollar, as the greenback remains under intense selling pressure headed into the weekend. The GBPUSD pair currently trades around the 1.3320 level, backing slightly away from the 1.3331 daily high. Dip buying demand is still the prevailing weekly theme in pair headed into the U.S session. Depressed trading volumes with North American markets away is currently slowing the advance in the pair, with the next upside hurdle likely to be the 1.3360 technical level.

The GBPUSD pair remains technically bullish while trading above the 1.3307 level. Further intraday upside towards the 1.3360 and 1.3400 levels appears possible today.

Should the GBPUSD pair start to slip much below the 1.3300 technical level, further selling towards the 1.3268 level cannot be ruled out.

Market Update – European Session: German Business Sentiment Hits Fresh Record High

Notes/Observations

Continental European data continues to show growth firing on all cylinders; German Nov Business Survey reading of 117.5 was the highest level since German reunification (Major European PMI Manufacturing hit multi-year highs on Thursday)

UK PM May to meet EU's Tusk to help clarify Brexit stance

Ireland govt faces election threat in Brexit showdown

Asia:

Japan Nov Preliminary Nikkei Manufacturing PMI: 53.8 v 52.8 prior

BoJ announces planned daily bond purchases: Cuts over 25-year JGB purchases to ¥90B from ¥100B prior

China Ministry of Finance (MOF): To adjust import tariff for some consumer goods IN effort to boost consumption, effective Dec 1st

Europe:

ECB's Coeure (France): ECB deposit rate will stay at -0.4% for a long time; EU recovery is robust and homogeneous across countries and sectors

German SPD Party head Schultz said to face calls from his own party to drop his refusal to form a minority Govt

Germany Green Party said to call for Chancellor Merkel to enter coalition with the SPD Party

SNB's Jordan: CHF currency (Franc) currency remains highly valued; SNB currency purchases to weaken the franc are not a deliberate 'beggar-thy-neighbor' strategy

Ireland Ruling Fine Gael Party: Stood behind Deputy PM, did not want election (**Note: Ireland's government was on the verge of collapse after the opposition Fianna Fail party whose votes PM Varadkar depends on to pass laws said it would seek to remove deputy PM Fitzgerald)

Economic Data:

(FI) Finland Oct PPI M/M: 0.5% v 0.5% prior; Y/Y: 3.6% v 4.0% prior

(FI) Finland Oct Preliminary Retail Sales Volume Y/Y: 2.5% v 2.6% prior

(TW) Taiwan Q3 Final GDP Y/Y: 3.1% v 3.1%e

(ES) Spain Oct PPI M/M: 0.8% v 0.6% prior; Y/Y: 2.8% v 3.5% prior

(CZ) Czech Nov Business Confidence: 16.2 v 16.9 prior; Consumer Confidence: 7.8 v 6.3 prior,

(CH) Swiss Q3 Industrial Output Y/Y: 8.6% v 3.2% prior, Industry & Construction Output WDA Y/Y: 7.4% v 3.6% prior

(SE) Sweden Oct PPI M/M: 0.3% v 0.4% prior; Y/Y: 2.5% v 4.3% prior

(DE) Germany Nov IFO Business Climate: 117.5 v 116.7e (record high); Current Assessment: 124.4 v 125.0e, Expectations Survey: 111.0 v 108.8e

(PL) Poland Oct Unemployment Rate: 6.6% v 6.7%e, Q3 Unemployment Rate: 4.7% v 4.8%e

(UK) Oct BBA Loans for Housing Purchases: 40.5K v 40.7Ke

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 flat at 386.9, FTSE -0.3% at 7399, DAX flat at 13013, CAC-40 +0.2% at 5392, IBEX-35 +0.7% at 10098, FTSE MIB +0.5% at 22507, SMI -0.1% at 22505, S&P 500 Futures +0.1%]

Market Focal Points/Key Themes: European indices trade mixed this morning in quiet trade. Outperformance in the Spanish Ibex and FTSE MIB while the FTSE 100 under performs. US futures tick higher after closure yesterday in obervance of Thanks Giving Holiday. On the Earnings front RealDolmen trades higher, while WYG is the notable decliner after guiding FY17 op materially below expectations. Gocompare.com trades lower after ZPG said it doees not intend to make a further offer, Gocompare notes it can deliver superior shareholder value as an independent company. On the M&A front Altice trades lower after reports of a potential sale of Dominican operations, while Clariant met with activist investor White tale

Equities

Industrials: [James Fisher & Sons [FSJ.UK] -4.6% (Earnings) , WYG [WYG.UK] -34% (Profit warning)]

Financials: [Gocompare [GOCO.UK] -2.7% (ZPG confirms no intention to make a further offer)]

Technology: [ RealDolmen [REA.BE] +5% (Earnings)]

Healthcare:[Bayer [BAYN.DE] -0.3% (Phase III INHALE trial fails to meet primary endpoint)]

Speakers

BOE's Tenreyro: Nov rate hike was not premature; saws signs of wage pick-up and domestic inflation pressures. Two rate hikes over the coming three years seemed appropriate; Markets have understood the BOE's message. Policy moves to depend on how the economy develops

ECB could tighten banking sector use of treasury shares

UK PM May: Both EU and Britain must move forward together in the Brexit talks (**Note: PM May will hold fresh talks with EU's Tusk during a summit in Brussels today and is due to travel to the Belgian capital again on December 4th to meet EU Commission president Jean-Claude Juncker in what is being seen as a final opportunity to meet Mr Tusk's deadline of Brexit clarity)

German President Steinmeier said to invite Chancellor Merkel, CDU's Seehofer and SPD's Schultz to meet for talks

German SPD official Schwesig: Schultz has the backing of party leadership (**Note: reports circulated that German SPD leader Schultz could resign in near future)

Germany said to reject part of the EU plans for reducing non-performing loans (NPLs). EU plans that would make it easier to seize collateral are hardly an expedient legal development

German IFO Economists forecasted German Q4 GDP at 0.7% and overall 2017 growth at 2.3%. ECB decision to reduce bond purchases appeared not to have affected business sentiment. German coalition situation to slow down Brexit but believed that either a grand coalition or minority govt could work

Turkey President senior advisor Karahan: Political tensions does increase the uncertainty for the TRY currency (Lira); Dec 4th is a key day. Reiterated view that Central Bank was independent and would tighten policy whenever it needed too

Russia Parliament (Duma) passes 2018-20 draft budget in its 3rd reading

Taiwan govt updated its economic forecasts which cut 2017 inflation from 0.7% to 0.6% while raising 2018 inflation outlook from 0.9% to 1.0%. Raised 2017 GDP growth forecast from 2.1% to 2.6%

Japan PM Advisor Honda: Did not discuss BOJ governor candidates with Abe during lunch

Currencies

The USD maintained a soft tone against most major FX pairs in the aftermath of the Nov FOMC minutes from Wed which showed that some policymakers were unsure about raising interest rates due to low inflation. USD Index was lower by 0.2% at 93.06 for 5-week lows

EUR/USD was trading at 6-week highs above 1.1860 as Continental European economic data continued to show growth was firing on all cylinders; German Nov Business Survey reading of 117.5 was the highest level since German reunification (Major European PMI Manufacturing hit multi-year highs on Thursday.

GBP/USD was holding above the 1.33 level as UK PM May was in Brussels to hold fresh talks with EU's Tusk during a summit. The key deadline on the current stalemate seen as December 4th when she meets EU Commission president Jean-Claude Juncker in what is being seen as a final opportunity to meet Mr Tusk's deadline of Brexit clarity

Fixed Income

Bund futures trades lower by 31 ticks to 162.75 in quiet trade weighed by declines in French OATS as the Bund-OAT spread continues to widen. Continued downside targets 162.61 then 162.38, while upside sees 163.30 then 163.40.

Friday's liquidity reports Thursday's excess liquidity rose to €1.840T from €1.835T prior. USe of the marginal lending facility rose to €343M from €291M prior.

Looking Ahead

Nov 24 EU Barnier's deadline for UK to provide 'sufficient progress'

Nov 24 PM May to meet senior MEPs

(PT) Portugal Finance Ministry Oct YTD Budget - 05:30 (ZA) South Africa to sell combined ZAR900M in I/L 2-25, 2029 and 2050 bonds

05:30 (EU) ECB's Nouy (SSM chief) in Frankfurt

06:00 (UK) DMO to sell combined £4.0B in 1-month, 3-month and 6-month Bills (£1.0B, £1.0B and £2.0B respectively)

06:30 (TR) Turkey Nov Capacity Utilization: No est v 79.7% prior

06:30 (TR) Turkey Nov Real Sector Confidence (Seasonally Adj): No est v 112.2 prior; Real Sector Confidence (unadj): No est v 109.5 prior

06:30 (IN) India Weekly Forex Reserves

06:30 (IS) Iceland to sell bills

06:45 (US) Daily Libor Fixing

07:00 (CL) Chile Oct PPI M/M: No est v -0.6% prior

07:30 (BR) Brazil Oct Total Outstanding Loans (BRL): No est v 3.049T prior; M/M: No est v -0.3% prior, Personal Loan Default Rate: No est v 5.6% prior

07:30 (BR) Brazil Oct Tax Collections (BRL): 116.3Be v 105.6B prior

07:30 (PT) ECB's Constancio (Portugal) in Madrid

08:00 (ES) Spain Debt Agency (Tesoro) announces upcoming issuance

08:00 (IN) India announces upcoming Bill auction (held on Wed)

08:05 (UK) Baltic Dry Bulk Index

08:30 (US) Weekly USDA Net Export Sales

09:00 (MX) Mexico Q3 Final GDP Q/Q: -0.2%e v -0.2% prelim; Y/Y: 1.6%e v 1.6% prelim, GDP Nominal Y/Y: 8.3%e v 8.1% prior

09:00 (MX) Mexico Sept IGAE Economic Activity (Monthly GDP) Y/Y: 1.5%e v 2.3% prior

09:45 (US) Nov Preliminary Markit Manufacturing PMI: 55.0e v 54.6 prior, Services PMI: 55.3e v 55.3 prior, Composite PMI: No est v 55.2 prior

10:00 (MX) Mexico Q3 Current Account: -$6.7Be v -$0.3B prior

11:00 (EU) Potential sovereign ratings after EU close

(ZA) South Africa Sovereign Debt to be rated by Moody's

(ZA) South Africa Sovereign Debt to be rated by S&P

12:00 (FR) France Oct Net Change in Jobseekers: No est v -64.8K prior, Total Jobseekers: No est v 3.48M prior

13:00 (US) Weekly Baker Hughes Rig Count data

13:15 (FR) ECB's Coeure (France) in Paris

15:00 (CO) Colombia Central Bank Interest Rate Decision: Expected to leave Overnight Lending Rate unchanged at 5.00%

weekend

(DE) Greens Hold National Convention to Decide on Coalition Talks

DAX Gains Ground As German Business Climate Sparkles

The DAX index is showing limited movement in the Friday session. Currently, the DAX is at 13,043.50, up 0.27% on the day. On the release front, the week ended on a positive note, as German Ifo Business Climate improved to 117.5, above the estimate of 116.6 points. There are no other events on the schedule.

The ECB changed directions and chopped its asset purchases at the November rate meeting, so analysts were eager to read the details of that meeting. The minutes, published on Thursday, stated that there was “broad agreement” among policymakers that further stimulus was still needed to boost inflation towards the ECB's target of close to 2 percent. The minutes noted that some policymakers wanted the ECB to announce an end date to the asset purchases, but in the end, members decided to extend the program by 9 months, to September 2018.

The DAX continues to hover at high levels, buoyed by a robust German economy. There was positive news on Friday, as business confidence improved in November. On Thursday, German Final GDP in the third quarter accelerated to 0.8%, its strongest quarter since 2014. The manufacturing sector has looked sharp, and German Manufacturing PMI for November improved to 62.5, its highest level since 2010. Eurozone Manufacturing PMI also kept pace, climbing to 60.0, compared to an estimate of 58.3 points. Manufacturing sectors in Germany and the eurozone have been buoyed by an increase in global demand and stronger domestic consumption.