Sample Category Title

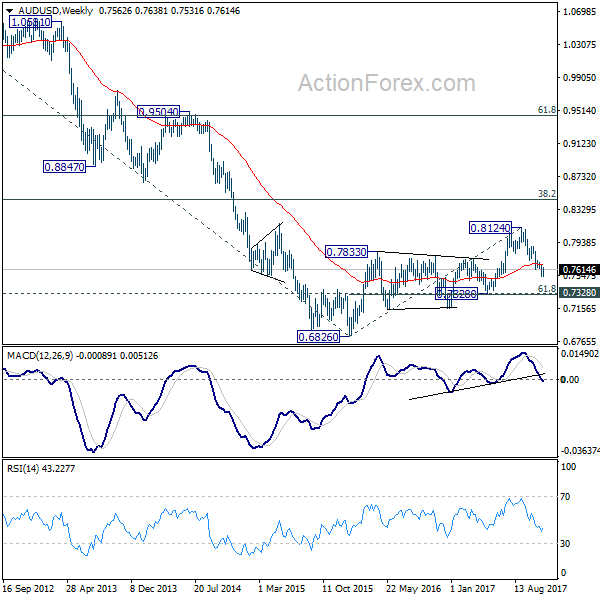

AUD/USD Makes Yet Another Push Lower

We have been expecting AUD/USD to push lower over the last month and as you can see from the daily chart below, price has been following an almost textbook pattern:

AUD/USD Daily:

Take a look at the levels that I've put the markers on. That's pretty obvious previous short term support turned resistance.

The qualifier for this trade is the fact that price is trending down and that the higher time frame resistance level around the 80c psychological level was rejected so heavily.

EURUSD – Looks To Extend Its Upside Pressure

EURUSD - The pair remains biased to the upside leaving risk of more strength in the new week. Resistance comes in at 1.1950 level with a cut through here opening the door for more upside towards the 1.2000 level. Further up, resistance lies at the 1.2050 level where a break will expose the 1.2100 level. Conversely, support lies at the 1.1900 level where a violation will aim at the 1.1850 level. A break of here will aim at the 1.1800 level. Below here will open the door for more weakness towards the 1.1750. All in all, EURUSD faces further recovery threats in the new week.

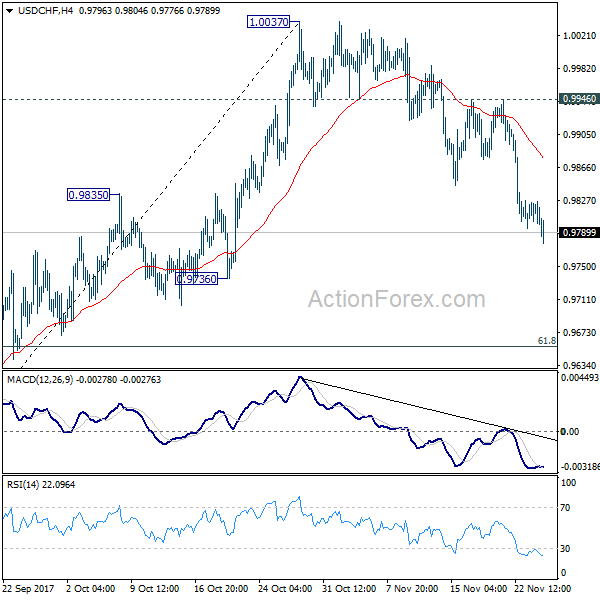

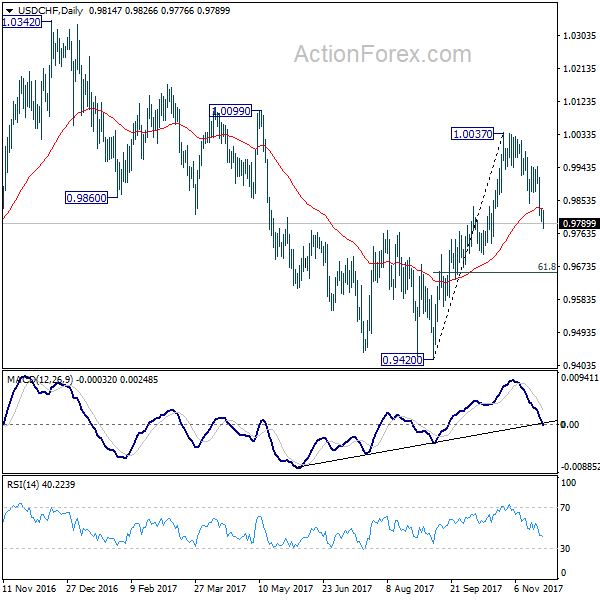

USDCHF – Bear, Risk Remains Lower

USDCHF - The pair remains weak and vulnerable to the downside. On the downside, support lies at the 0.9750 level. A turn below here will open the door for more weakness towards the 0.9700 level and then the 0.9650 level. On the upside, resistance resides at the 0.9850 level where a break will clear the way for more strength to occur towards the 0.9900 level. Further out, resistance comes in at the 0.9950 level. Above here if seen will turn attention to 1.0050. All in all, USDCHF faces further downside pressure.

A Blustery Black Friday For The Greenback

A Blustery Black Friday for the Greenback

The USD quickly got into the Black Friday act, getting sold as rapidly as Playstation Fours were flying off the shelf at the local Walmart.

But Friday's momentum was as much about the strengthening Euro with a convergence of politics and data leading the charge. Momentum continues to build towards another grand coalition while EU economic data continues to crush forecasts.

Its a busy week on tap but at this stage, it's unclear if liquidity, which was sparse last week, will fully recover as the markets veer towards year end which tends to see traders chasing their tail as opposed to taking on risk.

As for the Greenback, the FOMC minutes are too fresh in traders minds to ignore which suggests the weaker dollar narrative should remain intact. And adding fuel to the USD fire sale, the political landscape got even muddier when news leaked that Michael Flynn's legal team is no longer communicating with Trump's. This story may induce severe storm clouds for the dollar as we could see more indictments this week.

It could be a crucial week for the US dollar with October PCE print and more tax reform evolvement unfolding.

Any major inflation print will be a significant point of convergence to determine the Fed path to normalisation even more so in light of the recent Fed minutes which highlighted moderate inflation as a significant concern.

While tax reform remains bogged down in competing priorities, any sign of progress should be a USD-positive surprise. But the Republicans are in a frangible spot as no more than two Senators can dissent. So we should expect significant focus directed to the US Senate this week.

While tax from passage will be equity market positive, the big question is how much of the tax reform benefit is already baked into the dollar sentiment and will the currency market care as the ultimate focus remains on the Fed curve?

The much anticipated OPEC meeting is finally upon us but with the deck stacked for a production cut extension, anything short of a complete buy-in by Russia to roll over the production cut for all of 2018 could spook the markets and may cause oil prices to plummet.The bar has been set very high for any welcome surprises, so downside risks are sizable.

Finally, the Fed Chair Senate hearing is slated this week along with a plethora of Fed speak which will both be carefully observed for any glean on next years policy guidance.

The Australian Dollar

The Australian dollar is opening relatively unchanged versus the USD. On the domestic data front, we have another quiet week ahead, but there may be some interest in Q3 Capex Thursday. But with the Aussie dollar diminishing carry advantage continuing to weigh on the currency, there will be an acute focus on the US PCE print. But barring any major surprises along the Fed curve, the Aussie should sail into year-end relatively unscathed as post the FOMC minutes; the Aussie has remained well entrenched above support levels as significant selling interest is only likely to emerge near the .7675 level.

The Euro

Too many positive developments to ignore suggests the market will set sights on the 1.2000 level where things could get a bit messy. The market continues to underprice the ECB risk, but with the recent string of uproarious EU economic data, surely this will be too difficult for the ECB to ignore and at minimum moderate their lower for longer stance in spite of inflation undershooting expectations.

The Japanese Yen

With the dollar struggling and market chatter accelerating that the BoJ are preparing to shift their bond yield target rate higher, the market could be primed for a test of the critical 111 level this week. At a minimum, I think it's safe to say that given the recent FOMC dovish tack, despite the FOMC confirming the Dec rate hike, topside USDJPY momentum should be a grind at least until the dust settles on US tax reform.

China

China markets induced a bout of indigestion last Thursday when mainland equity market cratered but the market noise subsided on Friday providing relatively smooth sailing into the weekend. China's clampdown on debt triggered the most significant one day fall in the CSI 300.But with regulators intent on deleveraging, this recent market collapse may be a sign of things to come.

As Beijing moves to standardise financial markets, it will likely lead to more short-term capitulations as investors are now required to face the inherent risk from high yielding volatile assets as opposed to relatively risk-free returns as more financial reforms take hold. Given that regulatory changes will have a negative impact on liquidity, equity bulls should keep an eye on Bond Yields after Chinese sovereign yields surpassed 4 % mark last week.

On the economic data front, jam-packed end of the week highlights the diary. China's official manufacturing and non-manufacturing PMI for November are due Thursday. The Caixin manufacturing PMI will follow on Friday. Expect the PMI's to ebb as both deleveraging, and environmental regulations take their toll on activity metrics

The Chinese Yuan

Cheaper US dollar mainland corporate demand could give way to a surging Yuan as USD appetite continues to dwindle as reflected by the US dollar index (DXY) which fell below 92.70 on Friday. Not to mention that market flow remain biased to sell USD despite the market covering shorts ahead of this week's US Tax vote.

FX Asia

After some eye-watering currency moves last week, USDASia traded higher into the weekend as dealers booked profits on shorts ahead of a busy week for the USD and KRW.

Korean Won

Regional focus will fall on the BoK where the market has baked in a 25pbs rike to 1.5 %. But currency traders should be positioned on guard for any possible knee-jerk reaction if the BoK governor offers up a dovish hike to counter the surging KRW and rising bond yields.

Malaysian Ringgit

After the recent rally, consolidation should take hold of the Ringgit markets ahead of the key US PCE data, OPEC and US tax reform vote. Given the abundance of two-way dollar risk this week, I expect dealers to be more reactive to news headlines and economic data releases as opposed to position for a long-term view. So we should expect extended periods of boredom accentuated by abrupt explosions of volatility around headline risk.

Monday Morning Market Musings

Malaysian Ringgit and the domestic CPI

As you would expect, the MYR remains a very hot topic with my Singapore clients, who have significant market exposure and financial obligations in Malaysia. I was inundated with calls after he consumer-price index rose 3.7% from a year earlier compared with a 4.3% year-over-year increase in September. And well below the WSJ poll of 4 %.

Much of the recent strength in the Ringgit, besides the robust domestic demand and positive external sector, is driven by traders progressively pricing in a January rate hike.So does this lower than expected CPI cause me to have second thoughts about my January rate hike call or rethink my year-long bullish view on the Ringgit, absolutely not.

Much of the inflation gyrations occur at the gas pump, and OCT CPI too was tempered by pump -related price restraint which in my view, is far too volatile to include in any inflation metric. But despite the tempering of Octobers inflation data, one of the leading tenets of any Centeral Banker is to get ahead of inflation, and the BNM has already acknowledged this preference. All but suggesting a choice for an interest rate hike sooner rather than later. These type of comments are about as hawkish as a Central Banker can get.

Also, the real OPR has been running negative in 2017 which Gov Ibrahim recently recognised as “too long ” implying BNM is focusing on a neutral real policy rate. Based on this view, it suggests one hike in January with a possible follow up rate hike in 2018 a plausible projection.Finally, the MPC has signalled a preference for a stronger currency to mitigate inflationary pressure and to lower the cost of servicing foreign debt obligations. Keep in mind that monetary policies on distant shores cannot be ignored as weaker currency knock-on effect can raise the cost of servicing foreign currency debt.

All of which keeps this trader running with the Ringgit Bulls

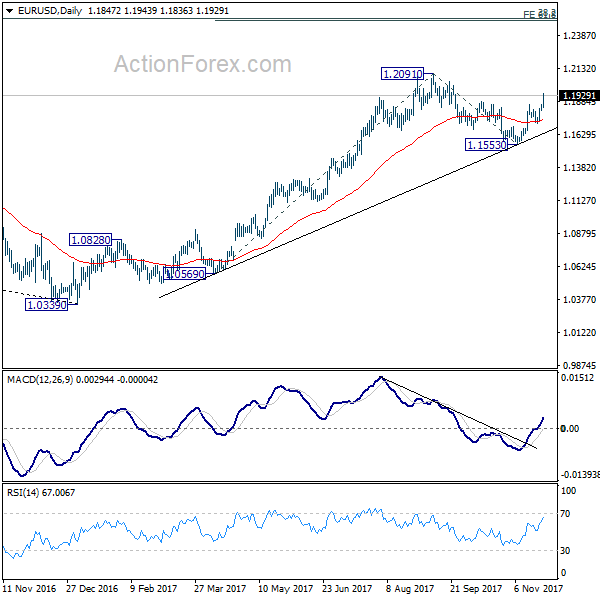

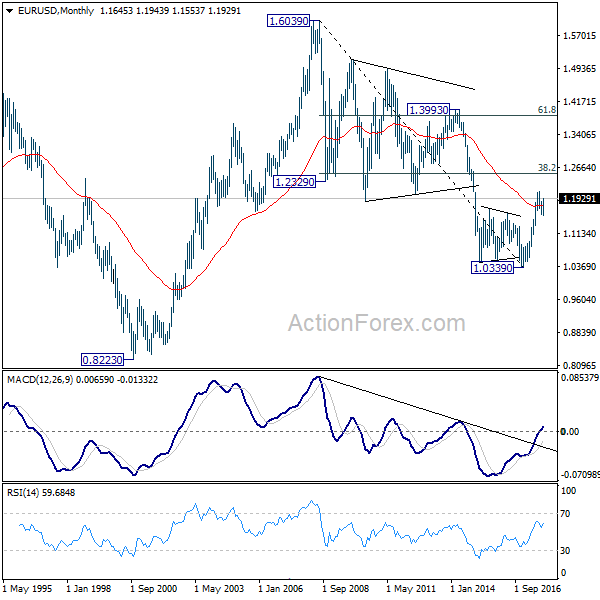

EUR/USD Weekly Outlook

EUR/USD's rise from 1.1553 extended last week after brief pull back and closed strongly at 1.1929. Initial bias remains on the upside this week for 1.2091 first. Break there will resume medium term up trend from 1.0339 and target 61.8% projection of 1.0569 to 1.2091 from 1.1553 at 1.2494, which is close to 1.2516 long term fibonacci level. We'd expect strong resistance from there to bring reversal. On the downside, break of 1.1712 support is needed to indicate completion of rise from 1.1553. Otherwise, outlook will remain cautiously bullish in case of retreat.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA (now at 1.1393) will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

In the long term picture, 1.0339 is now seen as an important bottom as the down trend from 1.6039 (2008 high) could have completed. It's still early to decide whether price action form 1.0339 is developing into a corrective or impulsive move. On the upside, strong resistance could be seen from 38.2% retracement of 1.6039 to 1.0339 at 1.2516. On the downside, we're not anticipating a break of 1.0339 in near to medium term.

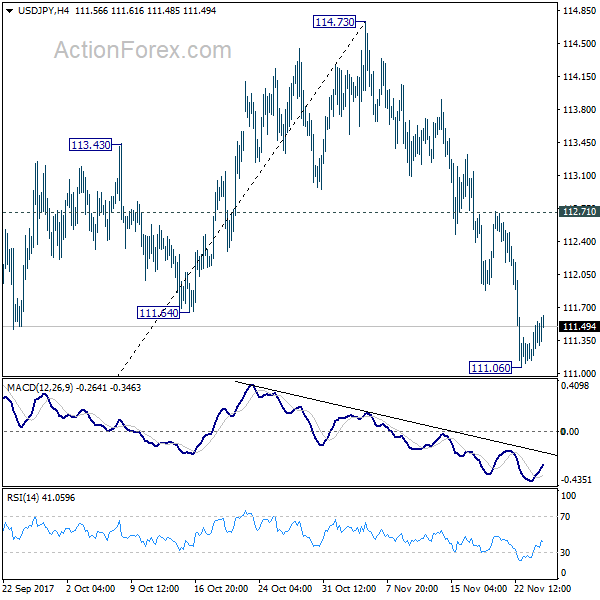

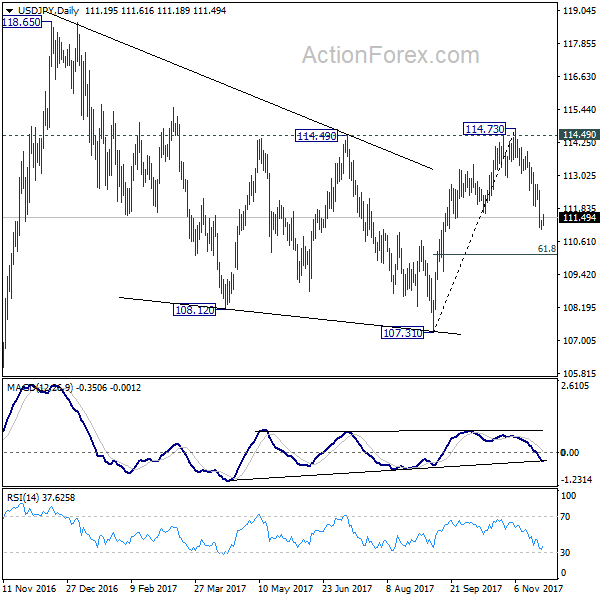

USD/JPY Weekly Outlook

USD/JPY's fall from 114.73 extended to as low as 111.06 last week and recovered after forming a temporary low. Initial bias is neutral this week first. But deeper fall will be expected as long as 112.71 holds. Below 111.06 will target 61.8% retracement of 107.31 to 114.73 at 110.14. For the moment, we're still favoring the case medium term corrective pattern from 118.65 has completed at 107.31 already. Hence, we'll looking for bottoming below 110.14 to bring another rise.

In the bigger picture, medium term rise from 98.97 (2016 low) is not completed yet. It should resume after corrective fall from 118.65 completes. Break of 114.49 resistance will likely resume the rise to 61.8% projection of 98.97 to 118.65 from 107.31 at 119.47 first. Firm break there will pave the way to 100% projection at 126.99. This will be the key level to decide whether long term up trend is resuming. However, firm break of 111.64 support will dampen this view and turn focus back to 107.31 instead.

In the long term picture, the rise from 75.56 (2011 low) long term bottom to 125.85 top is viewed as an impulsive move, no change in this view. Price actions from 125.85 are seen as a corrective move which could still extend. In case of deeper fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77. Up trend from 75.56 is expected to resume at a later stage for above 135.20/147.68 resistance zone.

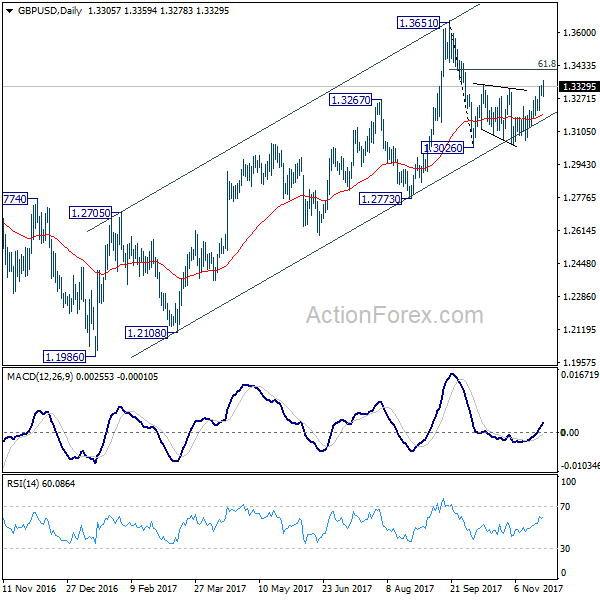

GBP/USD Weekly Outlook

GBP/USD's rise from 1.3038 extended higher last week and breached 1.3337 resistance. Initial bias is now on the upside this week for 61.8% retracement of 1.3651 to 1.3026 at 1.3412. Sustained break there will pave the way to retest 1.3651 high. Nonetheless, rejection from 1.3412, or break of 1.3278 minor support will revive the case that price actions from 1.3026 are merely correction. And intraday bias will be turned back to the downside for 1.3026 low in that case.

In the bigger picture, as noted before, GBP/USD hit strong resistance from the long term falling trend line. Nonetheless, subsequent fall was contained by 55 week EMA (now at 1.3069). Outlook is a bit mixed. For the moment, as long as 1.3835 support turned resistance holds, medium term rise from 1.1946 are viewed as a corrective pattern. That is, we'd expect another leg in the long term down trend through 1.1946 low. However, sustained break of 1.3835 should at least send GBP/USD to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

In the longer term picture, long the outlook is turned a bit mixed as GBP/USD failed to break through falling tend line resistance. We'll stay neutral first and assess the outlook again and price actions unfold.

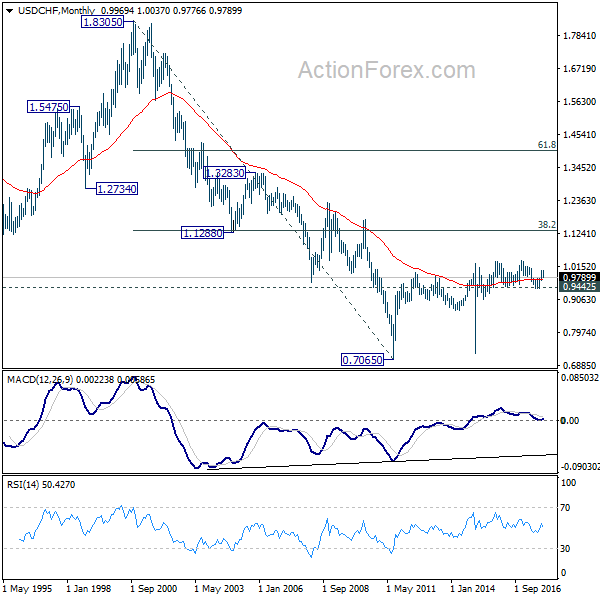

USD/CHF Weekly Outlook

USD/CHF's decline from 1.0037 extended to as low as 0.9776 last week. The development argues that rebound from 0.9420 is completed at 1.0037 already. Initial bias remains on the downside this week for 61.8% retracement of 0.9420 to 1.0037 at 0.9656. We'll look for bottoming again below 0.9656 and above 0.9420. On the upside, break of 0.9946 resistance will indicate that the decline from 1.0037 has completed and bring retest of this resistance.

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore, in case of decline attempt, we don't expect a firm break of this level. Nonetheless, strong break of 1.0342 is also needed to confirm upside momentum. Otherwise, medium term outlook will stay neutral.

In the long term picture, while upside momentum is unconvincing, with 0.9443 key support intact, rise from 0.7065 (2011 low) is still expected to continue. Break of 1.0342 will target 38.2% retracement of 1.8305 (2000 high) to 0.7065 at 1.1359.

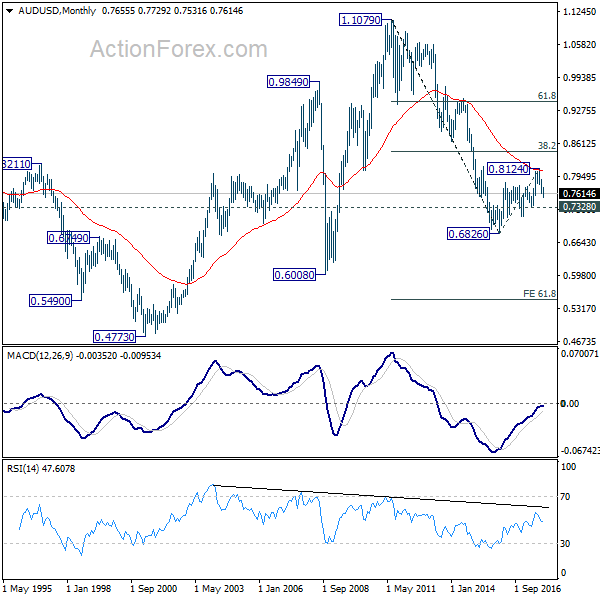

AUD/USD Weekly Outlook

AUD/USD edged lower to 0.7531 last week but formed short term bottom there and recovered. Initial bias remains neutral this week for more consolidation. After all, as long as 0.7729 resistance holds, near term outlook remains bearish and further decline is expected. Break of 0.7531 will resume whole decline from 0.8124 and target next key cluster level at 0.7322/8. . However, considering bullish divergence condition in 4 hour MACD, break of 0.7729 will indicate near term reversal and bring stronger rebound back to 0.7896 resistance and above.

In the bigger picture, corrective rise from 0.6826 medium term bottom is likely completed at 0.8124, after hitting 55 month EMA (now at 0.8049). Decisive break of 0.7328 key cluster support (61.8% retracement 0.6826 to 0.8124 at 0.7322) will confirm. And in that case, long term down trend from 1.1079 (2011 high) will likely be resuming. Break of 0.6826 will target 61.8% projection of 1.1079 to 0.6826 from 0.8124 at 0.5496. This will now be the favored case as long as 0.7729 near term resistance holds.

In the longer term picture, 0.6826 is seen as a long term bottom. Rise from there could either reverse the down trend from 1.1079, or just develop into a corrective pattern. At this point, we're favoring the latter. And, as long as 38.2% retracement of 1.1079 to 0.6826 at 0.8451 holds, we'd anticipate another decline through 0.6826 at a later stage. But strong support should be seen between 0.4773 (2001 low) and 0.6008 (2008 low).

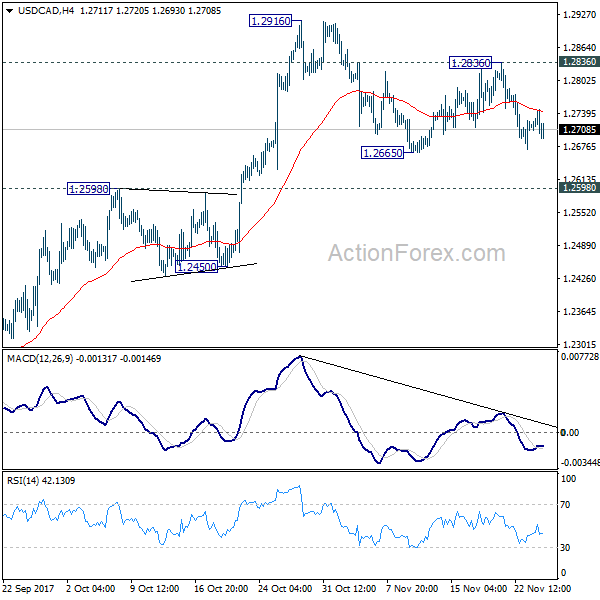

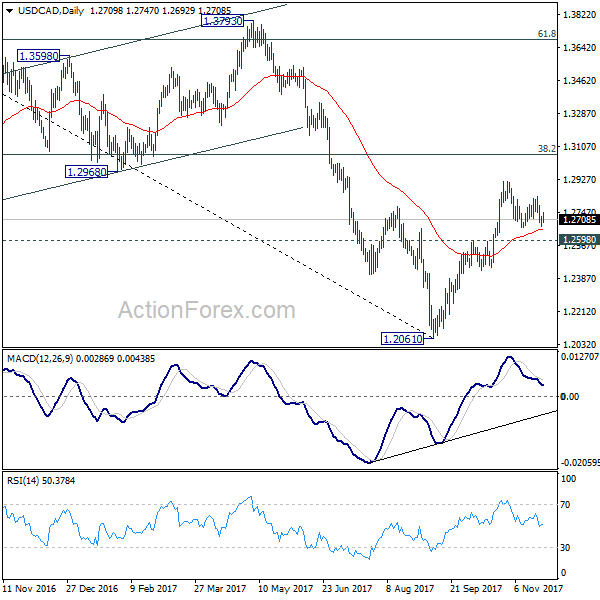

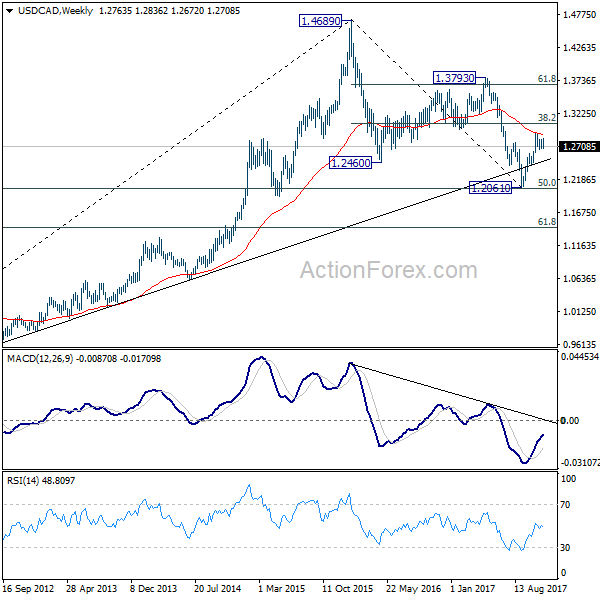

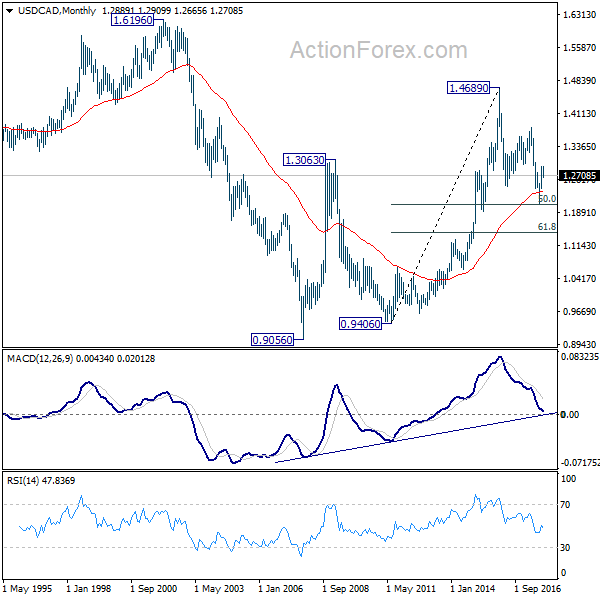

USD/CAD Weekly Outlook

USDCAD stayed in the corrective pattern from 1.2916 last week and outlook is unchanged. Such correction is still in progress and deeper fall might be seen. But we'd expect downside to be contained by 1.2598 resistance turned support and bring rebound. Above 1.2836 minor resistance will turn bias back to the upside for 1.2916 first. Further break of 1.2916 will resume whole rally from 1.2061 to 38.2% retracement of 1.4689 to 1.2061 at 1.3065. However, sustained break of 1.2598 will argue that rebound from 1.2061 has completed after hitting 55 week EMA (now at 1.2895). Near term outlook will be turned bearish in this case.

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4689 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Rise from 1.2061 medium term bottom should now target 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Firm break there will target 1.3793 key resistance next (61.8% retracement at 1.3685). We'll now hold on to this bullish view as long as 1.2450 support holds.

In the longer term picture, current development argues that correction from 1.4689 has completed with three waves down to 1.2061 already. And larger up trend from 0.9056 (2007 low) is still in progress. Firm break of 1.3794 resistance should now indicate up trend resumption through 1.4689 high.