Sample Category Title

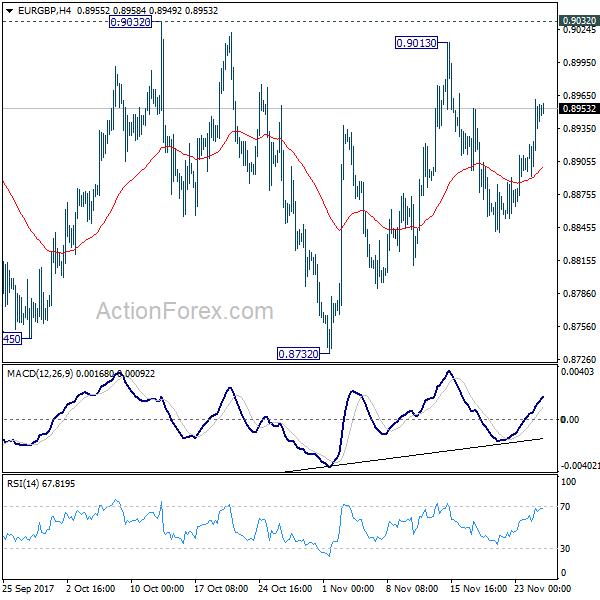

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8896; (P) 0.8929; (R1) 0.8965; More...

EUR/GBP is still bounded in range of 0.8732/9032 and intraday bias remains neutral. With 0.9032 resistance intact, deeper decline is mildly in favor in the cross. Break of 0.8732 will resume the fall from 0.9305 and target 0.8303 key support level. However, on the upside, decisive break of 0.9032 will confirm completion of the decline from 0.9305. In such case, intraday bias will be turned back to the upside for retesting 0.9305 key resistance.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5562; (P) 1.5617; (R1) 1.5717; More....

Intraday bias in EUR/AUD remains on the upside as medium term rise from 1.3624 is in progress. Further rally would be seen to 61.8% projection of 1.3624 to 1.5226 from 1.4949 at 1.5939 first. Break will target 100% projection at 1.6551, which is close to 1.6587 key resistance. On the downside, break of 1.5458 support is needed to indicate short term topping. Otherwise, outlook will remains bullish in case of retreat.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term top (2015 high) has completed at 1.3624. Rise from 1.3624 is expected to extend to retest 1.6587. We'll hold on to this bullish view as long as 1.5226 resistance turned support holds. Firm break of 1.6587 will resume long term rise from 1.1602 (2012 low).

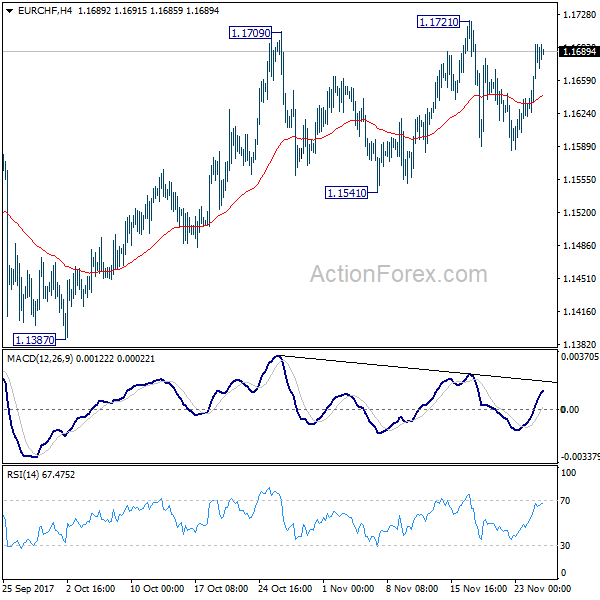

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1599; (P) 1.1619; (R1) 1.1647; More...

EUR/CHF is still bounded in range below 1.1721 and intraday bias remains neural. With 1.1541 support intact, outlook remains bullish for further rise. Decisive break of 1.1721 will resume the medium term tup trend and target 1.2 key level. On the downside, considering bearish divergence condition in 4 hour MACD and daily MACD, decisive break of 1.1541 will confirm topping and turn near term outlook bearish for 1.1355 key support.

In the bigger picture, long term rise from SNB spike low back in 2015 is still in progress. EUR/CHF should now be heading back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.1355 support holds. However, break of 1.1355 will indicate medium term topping. In that case, EUR/CHF should head back to 55 week EMA (now at 1.1142) and possibly below.

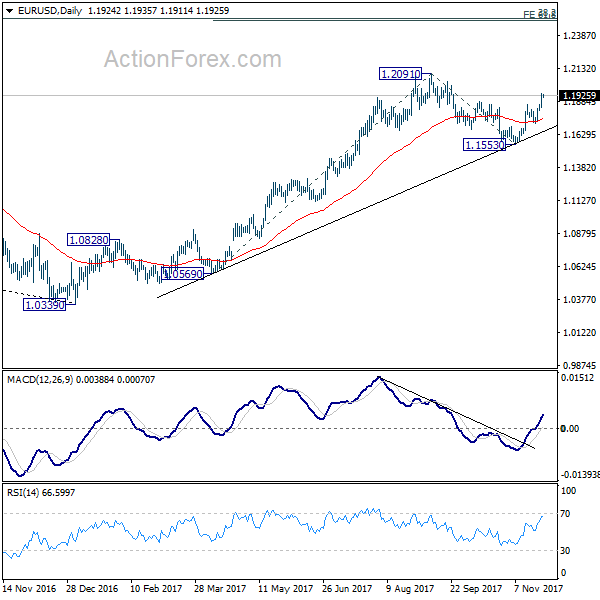

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1859; (P) 1.1901 (R1) 1.1967; More....

Intraday bias in EUR/USD remains on the upside for the moment. Rise from 1.1553 should target a test on 1.2091 high. Break there will resume medium term up trend from 1.0339 and target 61.8% projection of 1.0569 to 1.2091 from 1.1553 at 1.2494, which is close to 1.2516 long term fibonacci level. We'd expect strong resistance from there to bring reversal. On the downside, break of 1.1712 support is needed to indicate completion of rise from 1.1553. Otherwise, outlook will remain cautiously bullish in case of retreat.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA (now at 1.1393) will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3286; (P) 1.3322; (R1) 1.3367; More....

With 1.3287 minor support intact, intraday bias remains mildly on the upside for 61.8% retracement of 1.3651 to 1.3026 at 1.3412. Sustained break there will pave the way to retest 1.3651 high. Nonetheless, rejection from 1.3412, or break of 1.3278 minor support will revive the case that price actions from 1.3026 are merely correction. And intraday bias will be turned back to the downside for 1.3026 low in that case.

In the bigger picture, as noted before, GBP/USD hit strong resistance from the long term falling trend line. Nonetheless, subsequent fall was contained by 55 week EMA (now at 1.3069). Outlook is a bit mixed. For the moment, as long as 1.3835 support turned resistance holds, medium term rise from 1.1946 are viewed as a corrective pattern. That is, we'd expect another leg in the long term down trend through 1.1946 low. However, sustained break of 1.3835 should at least send GBP/USD to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

Market Update – Asian Session: Japan May Have A Near 2.9T Extra Budget

Headlines/Economic Data

General Trend: Asian equity markets are generally lower. Shanghai Large-caps decline, while downgrade of Samsung weighs on chip-related names; Copper down over 0.7%

Sony and Fast Retailing rise ahead of Cyber Monday

Japan

Nikkei225 opened +0.5%, later pared gains; Closed -0.2%

Chip-related companies trade lower as Samsung declines: SUMCO Corp -3%, Tokyo Electron -1.7%

Fast Retailing +1% amid reports of record online sales on Black Friday

Sony +1.3% (PlayStation4 seen among the top sellers on Black Friday, according to analysts and consultants)

Mitsubishi Materials -1.3% (follow-through selling amid recent data falsification disclosure)

Olympus -1.2% (Japanese banks to place shares in the firm in secondary offering)

Japan Govt will compile FY17/18 extra budget of €2.7-2.9T; with construction bond issuance of ~¥1T, this is up from the prior speculated ¥2.0-2.5T

Japan may lower taxes for smaller companies in M&A deals – Japanese Press

Morgan Stanley expects BoJ to raise its yield-curve control target in Q3 2018 (Note: JPMorgan made similar comments last week)

JAPAN OCT SERVICES PPI Y/Y: 0.8% V 0.9%E

Japan PM Abe Cabinet approval rating declines by 2 pct points to 52% - Nikkei Poll

Japan LDP official Nikai said to plan to visit China in December – Japanese Press

Korea

Kospi opened flat, has moved lower as the session progressed

Chip-related companies trade generally lower amid Morgan Stanley’s downgrade of Samsung Electronics, sees chip boom peaking: Korea: Samsung -4%; Hynix -2.9%; Japan: SUMCO Corp -3%, Tokyo Electron -1.7%; Taiwan: Taiwan Semi -1.8%, UMC -0.6%

Korean Won (KRW) -0.3%

(KR) South Korea Fin Min: Currency moves should be market oriented; sees GDP at 3% this year

Bank of Korea sells 3-month monetary stabilization bonds at 1.55%

Bank of Korea (BOK) sells KRW600B in 1-yr monetary stabilization bonds; avg yield 1.91% v 1.87% prior

South Korea sells KRW1.0T in 3-yr govt bonds at 2.16%

(KR) Bank of Korea (BOK) sells KRW600B in 1-yr monetary stabilization bonds; avg yield 1.91% v 1.87% prior

China/Hong Kong

Shanghai Composite opened -0.2%, Hang Seng opened flat

Both indices have weakened as the session has progressed

Large-cap CSI 300 Index -1% (extends volatility seen in prior week)

Hang Seng Conglomerates Index -0.8%, Consumer Goods -0.5%, Property/Construction Index -0.6%Information Technology Index -0.5%; Materials +0.9%

(CN) CHINA OCT INDUSTRIAL PROFITS Y/Y: 25.1% V 27.7% PRIOR

(CN) China Banking Regulatory Commission (CBRC) reports Oct banking sector total assets CNY241.6T, +10% y/y

(HK) Hong Kong SFC planning a consultation on active EFTs – SCMP

(CN) PBoC OMO: Injects CNY140B v CNY50B injected in 7,14 and 63-day reverse repos prior, injects match maturities

(CN) Lower China M2 growth is good for preventing financial risks - Chinese press

(HK) 1-month HK$ HIBOR 0.9225% (highest since 2008)

China 10-year bond yield -1bp

(CN) China MOF sells Special 5-year Treasury Bond: avg yield 3.8837%

Alibaba proposed to issue an indeterminate amount of US dollar denominated bonds

(CN) PBoC sets yuan reference rate at 6.5874 v 6.5810 prior

(CN) China MOF sells Special 5-year Treasury Bond: avg yield 3.8837%

Australia/New Zealand

ASX 200 opened flat, Closed +0.2%

ASX 200 Energy Index -0.6%, Resources -0.5%; Utilities +1%

Gas producer Santos -0.6%; Said to have hired adviser for takeover defense (Australian press)

Gold miner Newcrest Mining -1.3% (cautious broker commentary)

New Zealand NZX-50 closes +0.6% (record high)

Aussie and Kiwi underperform amid declines in Chinese equities and Copper prices

Other Asia

(PH) Philippines sells PHP0B (nil) for 3-month, 6-month and 1-year bills (rejects all bids)

North America

Retail: (US) According to ShopperTrak, shopper visits to brick-and-mortar retail stores on Thanksgiving Day and Black Friday -1.6% y/y (combined)

(US) According to Adobe Analytics, Black Friday and Thanksgiving online sales totaled $7.9B (record), +17.9% y/y; In terms of Cyber Monday, Adobe sees $6.6B in online sales (up ~17% y/y), which would be a new record day for US online shopping.

The US National Retail Federation (NRF) to release its Black Friday and Cyber Monday sales data on Tuesday, Nov 28th.

M&A: Meredith confirms to acquire Time for $18.50/share cash for $2.8B

Roark speculated to raise bid for Buffalo Wild Wings to ~$155/share (versus >$150 speculated on Nov 13th) - US financial press

Tax Reform: (US) US President Trump: 'Big week' for tax cuts; bill getting 'better and better'; - Senate GOP will hopefully come through on measures

(US) White House: US President Trump to meet with members of the Senate Finance Committee on Monday

Politics: (US) White House says budget director Mick Mulvaney will be acting director of the Consumer Financial Protection Bureau (CFPB); Officials say the President has the power to name an acting chief under a 1998 law regarding federal vacancies, despite outgoing CFPB director Cordray naming his deputy as his interim replacement this week

(MX) Mexico Fin Min Meade said to step down soon - Mexico press

(CA) Canada PM Trudeau to visit China from Dec 3-7

Europe

(DE) German Chancellor Merkel: Europe needs a strong Germany, so it needs a new govt in place as soon as possible; The caretaker govt will be able to carry out the day to day business of the govt; Still ready to talk with the Social Democrats party (SPD) about a grand coalition (comments from Nov 25th)

ECB’s Constancio (Portugal): Expects Basel III agreement by year's end; no decision on buying more corp bonds from January - speaking in Rome; Recent economic data are encouraging

(UK) Qiagen and MSD are expected to announce investments in the UK on Monday – financial press

Shell: Expected to restore cash dividend this week - UK press

Looking Ahead this week:

Later today comments from Fed’s Yellen; Tuesday RBNZ financial stability report, API, Japan retail sales; Wednesday South Korea industrial production, Japan industrial production, China Manufacturing and non-manufacturing PMI, Australia building permits, BOK rate decision

Levels as of 01:00ET

Nikkei225 -0.3%, Hang Seng -0.6%; Shanghai Composite -0.9%; ASX200 +0.1%, Kospi -1.3%

Equity Futures: S&P500 -0.1%; Nasdaq100 -0.1%, Dax -0.1%; FTSE100 -0.2%

EUR 1.1941-1.1912; JPY 111.69-111.32; AUD 0.7623-0.7593;NZD 0.6889-0.6854

Dec Gold +0.2% at $1,289/oz; Jan Crude Oil -0.4% at $58.73/brl; Dec Copper -1.8% at $3.14/lb

Aussie Trading On A Weaker Footing This Morning

For the 24 hours to 23:00 GMT, the AUD declined 0.1% against the USD and closed at 0.7619 on Friday.

LME Copper prices rose 1.0% or $72.0/MT to $6967.5/MT. Aluminium prices rose 0.7% or $14.0/MT to $2104.0/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7606, with the AUD trading 0.17% lower against the USD from Friday’s close.

Earlier today, data showed that in China, Australia’s largest trading partner, industrial profits climbed 25.10% on a yearly basis in October, after recording a gain of 27.7% in the previous month.

The pair is expected to find support at 0.7590, and a fall through could take it to the next support level of 0.7575. The pair is expected to find its first resistance at 0.7624, and a rise through could take it to the next resistance level of 0.7643.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

German Business Confidence Strengthened To An All-Time High In November

For the 24 hours to 23:00 GMT, the EUR rose 0.64% against the USD and closed at 1.1926 on Friday, after recent data showed that German business morale surged to a record high in November.

The Ifo business climate index in Germany unexpectedly advanced to a record high level of 117.5 in November, suggesting that firms are gaining increased confidence over the robust momentum in the Euro-zone’s largest economy. In the prior month, the index had recorded a revised level of 116.8, while markets had expected for a drop to a level of 116.7. Moreover, the nation’s Ifo business expectations index surprised to the upside, jumping to a level of 111.0 in November, and defying market consensus for a fall to a level of 108.8. The index had recorded a revised level of 109.2 in the previous month.

On the other hand, the nation’s Ifo current assessment index registered an unexpected drop to a level of 124.4 in November, compared to a reading of 124.8 in the previous month.

The common currency got further boost, on the back of news that Germany’s Social Democrats’ agreed to hold talks with Chancellor, Angela Merkel on resolving the political crisis by renewing their outgoing coalition government.

Macroeconomic data released in the US indicated that the flash Markit services PMI unexpectedly eased to a four-month low level of 54.7 in November, against market expectations for the index to remain steady at a level of 55.3 registered in the previous month. Further, the nation’s preliminary Markit manufacturing PMI surprisingly declined to a level of 53.8 in November, expanding at its weakest pace in two months. The PMI had registered a level of 54.6 in the prior month, while investors had envisaged for a rise to a level of 55.0.

In the Asian session, at GMT0400, the pair is trading at 1.1926, with the EUR trading flat against the USD from Friday’s close.

The pair is expected to find support at 1.1861, and a fall through could take it to the next support level of 1.1795. The pair is expected to find its first resistance at 1.1968, and a rise through could take it to the next resistance level of 1.2009.

Ahead in the day, investors would look forward to the release of Italy’s consumer confidence index for November. Moreover, the US new home sales data for October, due to release later in the day, will also attract a lot of market attention.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

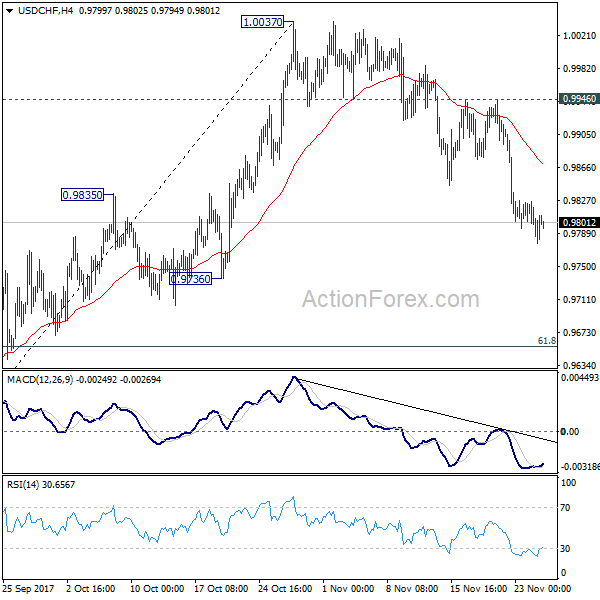

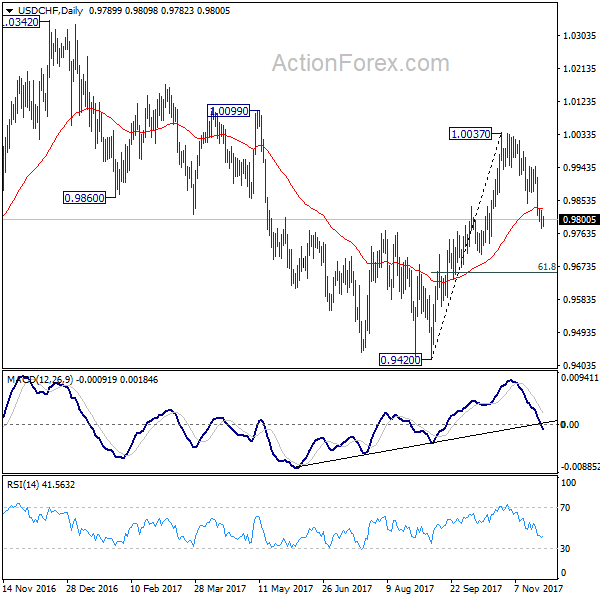

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9772; (P) 0.9799; (R1) 0.9817; More....

USD/CHF's fall from 1.0037 is still in progress and intraday bias remains on he downside for 61.8% retracement of 0.9420 to 1.0037 at 0.9656. We'll look for bottoming again below 0.9656 and above 0.9420. On the upside, break of 0.9946 resistance will indicate that the decline from 1.0037 has completed and bring retest of this resistance.

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore, in case of decline attempt, we don't expect a firm break of this level. Nonetheless, strong break of 1.0342 is also needed to confirm upside momentum. Otherwise, medium term outlook will stay neutral.

Britain’s Mortgage Approvals Hit Lowest Level In 13 Months In October

For the 24 hours to 23:00 GMT, the GBP rose 0.18% against the USD and closed at 1.3333 on Friday.

On the macro front, data revealed that UK's BBA mortgage approvals declined to a level of 40.49K in October, dropping to its lowest level since September 2016. Markets were anticipating mortgage approvals to drop to a level of 40.65K, after recording a revised reading of 41.58K in the previous month.

Meanwhile, the European Union (EU) handed the UK Prime Minister, Theresa May, a 10-day deadline to improve her Brexit divorce bill in order to start further negotiations on a transition period.

In the Asian session, at GMT0400, the pair is trading at 1.3317, with the GBP trading 0.12% lower against the USD from Friday's close.

The pair is expected to find support at 1.3277, and a fall through could take it to the next support level of 1.3238. The pair is expected to find its first resistance at 1.3358, and a rise through could take it to the next resistance level of 1.3400.

In the absence of any major economic releases in the UK today, investor sentiment would be governed by global macroeconomic factors.

The currency pair is trading below its 20 Hr moving average and showing convergence with its 50 Hr moving average.