Sample Category Title

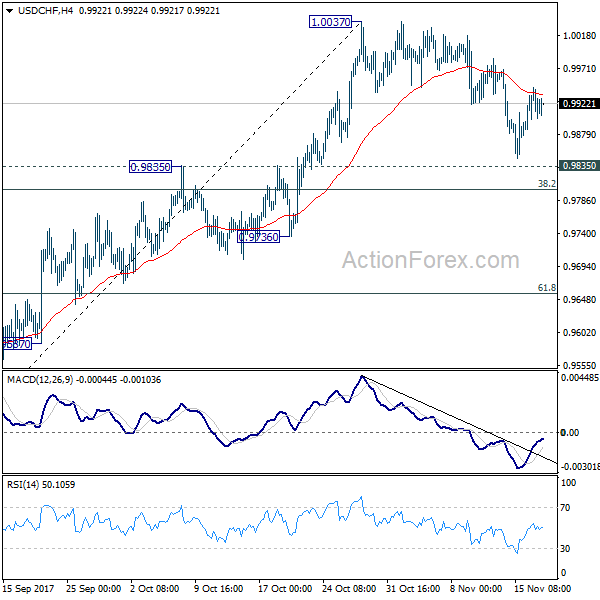

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9899; (P) 0.9922; (R1) 0.9966; More....

Intraday bias in USD/CHF remains neutral for the moment. The rebound ahead of 0.9835 support retained near term bullishness and favors further rally. On the upside, firm break of 1.0037 resistance will extend the rise from 0.9420 and target 1.0342 high. However, firm break of 0.9835 will argue that whole rebound form 0.9420 is completed and turn outlook bearish. In that case, USD/CHF should target 61.8% retracement of 0.9420 to 1.0037 at 0.9565 and possibly below.

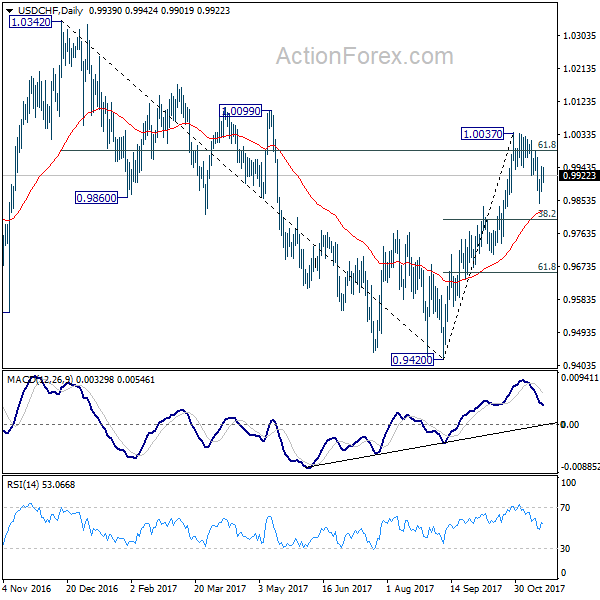

In the bigger picture, current development suggests that USD/CHF has defended 0.9443 (2016 low) key support level again. Rise from 0.9420 could is a medium term up move and should target a test on 1.0342 high. This represents the upper end of a long term range that started back in 2015. On the downside, break of 0.9736 support is now needed to indicate completion of the rise from 0.9420. Otherwise, further rally will remain in favor in medium term.

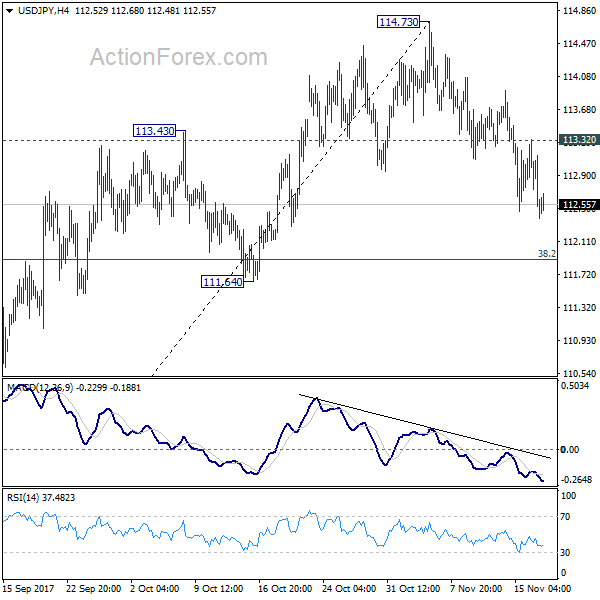

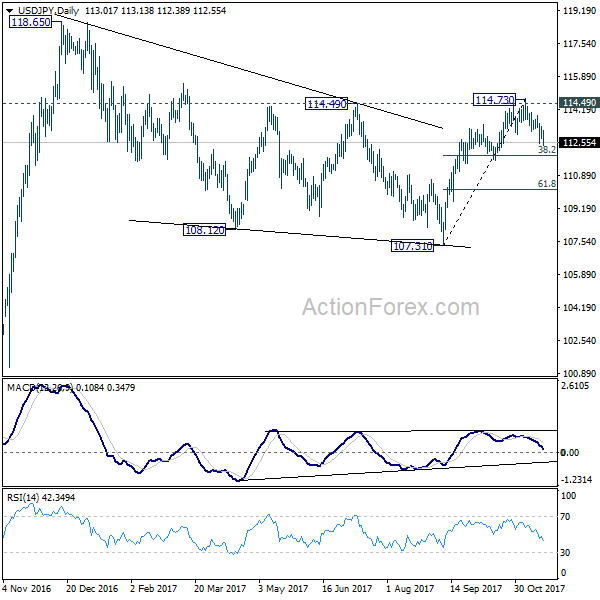

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 112.75; (P) 113.03; (R1) 113.34; More...

Intraday bias in USD/JPY remains on the downside. Correction is in progress for 8.2% retracement of 107.31 to 114.73 at 111.89 first. Sustained break of 111.64 support will now argue that rise from 107.31 has completed. In that case, USD/JPY should target 61.8% retracement at 101.14. On the upside, break of 113.32 minor resistance is needed to confirm completion of the fall. Otherwise, near term outlook will now stay cautiously bearish.

In the bigger picture, medium term rise from 98.97 (2016 low) is not completed yet. It should resume after corrective fall from 118.65 completes. Break of 114.49 resistance will likely resume the rise to 61.8% projection of 98.97 to 118.65 from 107.31 at 119.47 first. Firm break there will pave the way to 100% projection at 126.99. This will be the key level to decide whether long term up trend is resuming. However, firm break of 111.64 support will dampen this view and turn focus back to 107.31 instead.

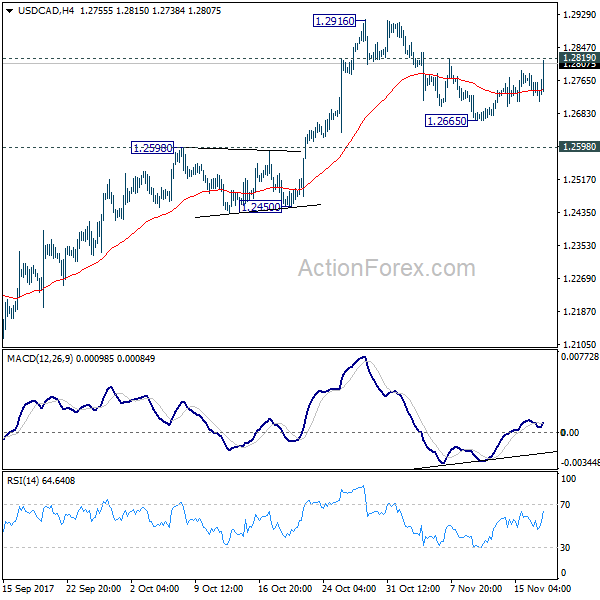

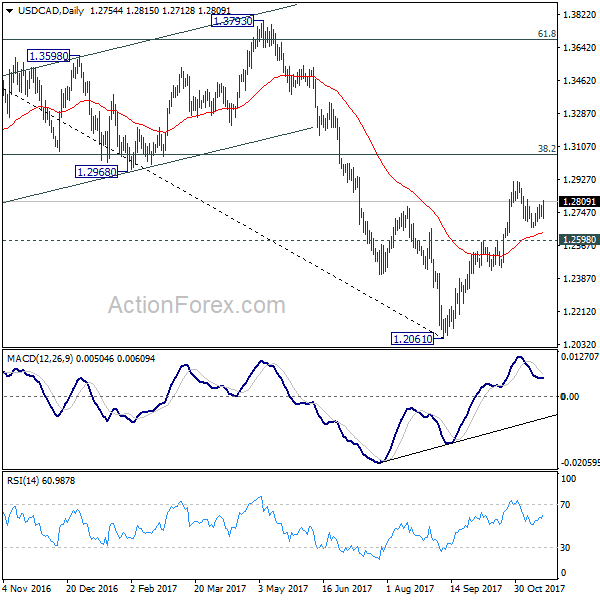

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2728; (P) 1.2755; (R1) 1.2783; More....

USD/CAD rises sharply in early US session and focus is back on 1.2819 minor resistance. Break there will argue that correction from 1.2916 has completed at 1.2665 already. Intraday bias will be turned back to the upside for 1.2916 high first. Break there will extend the rise from 1.2061 to 38.2% retracement of 1.4689 to 1.2061 at 1.3065. In case the correction from 1.2916 extends with another fall, overall outlook will remain bullish as long as 1.2598 resistance turned support holds.

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4689 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Rise from 1.2061 medium term bottom should now target 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Firm break there will target 1.3793 key resistance next (61.8% retracement at 1.3685). We'll now hold on to this bullish view as long as 1.2450 support holds.

Canadian Dollar Soft after Mixed CPI, Other Commodity Currencies Weak Too

Commodity currencies are set to end the week as the weakest ones. While WTI crude oil seems to have defended 55 handle and recovered, Canadian Dollar stays soft after mixed inflation data. Dollar follows closely and continues to display softness against Euro and Yen. Dollar could be supported by progress in tax plan after both House and Senate Finance Committee approved their own versions. Though, strength in the greenback is limited as there are still huge work to reconcile the tax plan between House and Senate. Also, there is some pressure from news that Special Counsel Robert Mueller issued subpoean to President Donald Trump for Russia related documents.

Release from US, housing starts rose to 1.29m annualized rate in October, above expectation of 1.19m. Building permits also rose to 1.30m, above expectation of 1.25m. Canada CPI slowed to 1.4% yoy in October, meeting expectation. CPI core - common accelerated to 1.6% yoy. CPI core trim was unchanged at 1.5% yoy. CPI core median slowed to 1.7% yoy. Elsewhere, Eurozone current account surplus widened to EUR 37.8b in September. New Zealand business manufacturing index dropped to 57.2 in October. PPI input rose 1.0% qoq in Q3, PPI output rose 1.0% qoq too.

ECB Draghi: Recalibration signaled our growing confidence

ECB President Mario Draghi said in a conference in Frankfurt that last month's recalibration of policy aimed to "signal our growing confidence in the euro area economy, while also acknowledging that we must be patient and persistent for inflation to return sustainably to our objective." But he insisted that the asset purchase program could run before the deadline line of next September "if necessary, and in any case until we see a sustained adjustment in the path of inflation." He emphasized that "despite this progress on the real side of the economy, from a monetary policy perspective our task is not complete, as we have not yet seen a sustained adjustment in the path of inflation.

Germany coalition talk could enter into overtime

In Germany, it's reported that the negotiations on the coalition between Chancellor Angela Merkel's CDU/CSU, the Greens and FDP stalled ahead of the self imposed deadline of today. Disagreement on migration policy is believed to be the main show-stopper. The exploratory talks could extend into overtime and even through the weekend. Merkel is set to miss the EU social summit in Sweden. If the so called Jamaica coalition could be approved, the parties will then enter into formal negotiations on the details, including dividing up cabinet posts. However, if the talk failed, Merkel could opt for forming a minority government with Greens. Another choice is to call on Social Democrats again for a reincarnation of the Grand Coalition. Or worst come to worst, a new national elections could be called.

UK Davis: We offered some creative compromises

UK Brexit Secretary David Davis said that UK has been "offering some creative compromises" in negotiations with EU. But UK "not always got them back. He also warned EU not to "put politics above prosperity". Some noted that Davis's comments indicated UK's frustration regarding EU's attitude in the talks. But then, UK has so far refused to respond to EU's request of settling the past before talking about the future. That is, Davis himself has asked EU not to expect any number or formula on the divorce bill before moving on to trade talks. While Davis said that it's "incredibly unlikely" there will be a no-deal Brexit, the gap between the two sides is still huge.

Former BoJ Shirai: Abe's win makes BoJ hard to exit

Former BoJ board member Sayuri Shirai said that Prime Minister Shinzo Abe's recent landslide win in the snap election would make it very difficult for BOJ to exit stimulus. She noted that "when the economy is in good shape like now, the BOJ needs to normalize monetary policy so it has the tools available to fight the next recession." She added that "the BOJ probably wants to slow its asset purchases." However, "that may be difficult because the government puts a high priority on keeping stock prices high and the yen weak."

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2728; (P) 1.2755; (R1) 1.2783; More....

USD/CAD rises sharply in early US session and focus is back on 1.2819 minor resistance. Break there will argue that correction from 1.2916 has completed at 1.2665 already. Intraday bias will be turned back to the upside for 1.2916 high first. Break there will extend the rise from 1.2061 to 38.2% retracement of 1.4689 to 1.2061 at 1.3065. In case the correction from 1.2916 extends with another fall, overall outlook will remain bullish as long as 1.2598 resistance turned support holds.

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4689 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Rise from 1.2061 medium term bottom should now target 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Firm break there will target 1.3793 key resistance next (61.8% retracement at 1.3685). We'll now hold on to this bullish view as long as 1.2450 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business NZ Manufacturing PMI Oct | 57.2 | 57.5 | 57.6 | |

| 21:45 | NZD | PPI Input Q/Q Q3 | 1.00% | 1.20% | 1.40% | |

| 21:45 | NZD | PPI Output Q/Q Q3 | 1.00% | 1.40% | 1.30% | |

| 09:00 | EUR | Eurozone Current Account (EUR) Sep | 37.8B | 30.2B | 33.3B | 34.5B |

| 13:30 | CAD | CPI M/M Oct | 0.10% | 0.10% | 0.20% | |

| 13:30 | CAD | CPI Y/Y Oct | 1.40% | 1.40% | 1.60% | |

| 13:30 | CAD | CPI Core - Common Y/Y Oct | 1.60% | 1.50% | ||

| 13:30 | CAD | CPI Core - Trim Y/Y Oct | 1.50% | 1.50% | ||

| 13:30 | CAD | CPI Core - Median Y/Y Oct | 1.70% | 1.80% | ||

| 13:30 | USD | Housing Starts Oct | 1.29M | 1.19M | 1.13M | |

| 13:30 | USD | Building Permits Oct | 1.30M | 1.25M | 1.23M |

Chinese Debt Potentially Raising Dark Clouds on the Horizon – Analogies to Japan; Who Stands to Lose the Most?

International organizations including the International Monetary Fund and the World Bank have been warning of dangerous debt levels in China. A debt crisis in the world's second largest economy might seem like a frightening prospect for the rest of the world, however a closer look reveals that under the current state of affairs, one such crisis would mostly be of serious detriment to nations whose exports are heavily directed towards China, one such nation being major commodity exporter Australia.

Not too long ago, credit cards were unheard of in China. Nowadays, a credit explosion is being evidenced in the country with consumer debt rising as a proportion of Gross Domestic Product and standing at a multiple – three times – of what it was around ten years ago. If the trend continues, then it is expected than in a few years' time indebted Chinese households would rival those in the US before the 2007-09 global financial crisis.

The IMF is sounding the alarm, anticipating China's non-financial sector debt to stand close to 300% of GDP by 2022. Last year, the fund's projections stood at 242%. Non-financial sector debt includes household, corporate and government debt. Worryingly in its report, the IMF makes reference to "increasing risks of a disruptive adjustment". It should be mentioned though, that not everything is negative in the IMF's annual assessment of the Chinese economy. In particular, the organization points out that China "has potential to sustain strong growth over the medium term". But to safely do so "requires speeding up reforms to make growth less reliant on debt and investment". In addition, the fund acknowledges that the government has begun taking "important initial steps to facilitate private sector deleveraging", however it urges for efforts to "intensify".

Credit expansion is not necessarily a bane for an economy. Given that there are productive investment opportunities craving for funding, then debt can allow them to come to fruition, leading to economic growth. However, perhaps alarmingly so, the efficiency of credit has been declining in recent years, suggesting that productive investments are getting scarcer and that probably money is being put to bad use, fueling overcapacity in industries and hampering productivity. According to the IMF, "in 2008, new credit of about Rmb6.50 trillion was needed to raise nominal GDP by Rmb5tn." This compares to Rmb20tn in new credit in 2016 to achieve the same level of growth. More simply, in 2008, 1.3 renminbi in credit was put to use for each renminbi added to nominal GDP. In 2016, to achieve the same level of growth, 4 renminbi were needed in debt.

Beyond the non-financial sector, total debt in the economy is currently estimated to stand around 250% of GDP with GDP being at around $11 trillion. China's foreign exchange reserves stood at $3.1tr at the end of October, climbing for nine straight months. These serve as valuable ammunition for the government in the event of a banking crisis that forces it to intervene and rescue the system via a recapitalization. However, an additional twist to China's debt problem is the so-called shadow banking system.

The full extent of the debt problem is not really clear due to the shadow banking system's involvement and the inherent lack of data associated with it. Further complicating things, is the fact that shadow banking activities seem to be growing sharply, as well as the increasing interconnection between shadow banks and China's formal banking system. In its October report on the East Asian and Pacific economies, the World Bank stressed that shadow banking might inflict a Chinese debt crisis. In its report, the World Bank says that the most representative shadow banking activities involving loans and bankers' acceptances have "soared from under 7% of GDP in 2005 to over 31% of GDP in 2016." The organization also made reference to the connection between shadow banks and official banks. A crisis stemming from such entities can thus turn into one of systemic nature as was the case with special purpose vehicles (SPVs) in the US during the subprime mortgage crisis.

The lack of a clear picture on the debt issue makes it difficult to assess the problem and thus the government's capacity to respond. A crisis finding the government unable to resolve the problems in a fashion that allows the economy to grow at around the current pace and consequently significantly hampers growth moving forward would surely negatively affect the global economy, wouldn't it? Perhaps surprisingly, this might not be the case. This is where analogies to Japan might help us evaluate the impact of a Chinese crisis on the rest of the world.

One important point to make is that most Chinese debt is internally held, rendering the problem more of a domestic issue. The same was true for Japan when it faced a real estate crash and a banking crisis in the early 1990s. Back then, Japan was dubbed the engine of global growth, just as now and for the past decade China seems to possess that role. And yet when growth rates in the then engine of global growth fell close to zero percent, the rest of the world was not considerably affected by the Japanese slowdown. Moreover, the Japanese economy rebalanced, with its citizens still being considered among the wealthiest in the world. It is not unlikely that China is headed along a similar path.

Despite Chinese problems looking domestic in nature, something which would limit global repercussions should a Chinese banking crisis emerge, still it is expected that there will be some big losers should economic activity significantly decelerate in the world's second largest economy. One of those losers would be Australia, having China as its top trading partner with the bulk of its exports headed to the country. Emerging markets such as Brazil and other major industrial metals producers are also projected to feel the burn from such a slowdown. Such countries are already considered to be impacted by China's efforts to rebalance its growth model away from manufacturing and investment. Market participants, having in mind currency markets as well, will position themselves accordingly should a credit crisis occur in China, "punishing" the Australian dollar and the Brazilian real, with a currency adjustment of course anticipated in the yuan as well.

It should also be pointed out that despite the problem seeming relatively contained for the time being, financial institutions in China are increasingly having global aspirations. Should this trend continue, then a Chinese debt crisis might turn into an international crisis with the global financial system potentially facing another "Lehman moment".

One might argue that warnings about the health of the Chinese economy have been a recurring theme over the last number of years with those sharing their concerns being proved wrong time after time. Will the central government, through its actions, yet again prove them wrong? It remains to be seen. There seem to be hints that the government is indeed acting to address the issues raised by high debt levels.

Important data on October fixed asset investment, industrial production, and retail sales released recently all came in solid, though below expectations and reflecting a slowdown relative to the preceding month. The 6.8% annual GDP growth during the third quarter also reflected a minor slowdown relative to the 6.9% in the first and second quarters. Still, the third quarter's rate of growth was robust, exceeding the government's growth target for 2017 of "around 6.5%". The recent mild deceleration is seen as evidence that the Communist Party's government is attempting to shift focus to the quality of growth rather than merely the quantity, engaging in deleveraging efforts to limit the risks posed by excessive debt. The government's environmental considerations are also seen as shifting growth patterns towards qualitative expansion over quantitative. Should this trend continue, then a gradual reduction in activity is to be expected, but rather a healthy and perhaps necessary one that will minimize the probability of a big crash further ahead.

EURUSD Remains Bullish Above 1.1800 Handle

The euro continues to trade at elevated levels against the U.S dollar, as financial markets turn their focus to U.S dollar index weakness and German politics. The EURUSD pair is currently holding around the key 1.1800 handle, as the German CDU Party remains in tense coalition negotiations with the Free-Democrat Party and the Green Party. German Chancellor Angela Merkel increasingly needs to strike a deal, to stabilize German politics and secure her own political future.

The EURUSD pair remains intraday bullish while trading above the 1.1800 technical level. Further upside towards the 1.1822 and 1.1860 resistance points. Extended euro resistance is found at the 1.1910 and 1.1940 levels.

Should price-action decline below the 1.1800 level, further losses towards the 1.1783 and 1.1767 levels are likely. Extended intraday EURUSD support is also found at the key 1.1710 technical level.

USDJPY Strongly Bearish Beow 112.94 Level

The US dollar continues to decline against the Japanese yen, hitting 112.39 in early Friday trading, as the US dollar index comes under pressure, due to risk-off trading sentiment. The USDJPY pair currently trades around the 112.50 level heading into the US session, as investors flock to perceived safe haven assets, benefitting the Japanese yen currency. Geopolitical and U.S political woes are helping to drive global equities and the US dollar index lower as the trading week comes to a close.

The USDJPY pair remains strongly bearish while trading below the 112.94 level. Further declines towards the 112.28 and 111.89 technical levels should be expected.

Should USDJPY price-action trade above the 112.94 level, further upside towards the 113.24 resistance level seem possible.

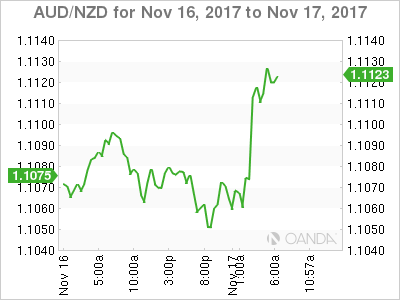

AUDNZD Tests Cloud Top; Neutral to Bullish in Short-Term

AUDNZD followed a downtrend from a 1½ -year high of 1.1288 reached on October 24 to a one-month low of 1.0986 on November 15. Currently, the pair is consolidating around 1.1120, but if the market fails to post a lower low, then the risk would shift to the upside.

The technical indicators give bullish signals in the short-term. The pair is fluctuating above the Ichimoku cloud as well as the 20 and the 50-period simple moving average lines which recorded a bullish cross yesterday. However, upside movements might be restricted in the near term as the SMA lines are trending flat, while the RSI is positively sloping above its neutral zone, but has reached overbought levels in the 1-hour chart. The MACD is marginally above zero and its signal line.

An extension to the upside would first meet the previous top at 1.1138. Any violation of this point, would target the 1.1200 key-level and then the October's top at 1.1288.

Alternatively, If the pair heads down, the 20-period SMA at 1.1064 could be a strong support, as this level has been repeatedly tested the past two weeks and is also the lower bound of the Ichimoku cloud. From here, the scope opens towards the previous low at 1.0986, which if breached would stretch the longer-term downleg. Steeper declines would also shift focus to 1.0876.

Dollar Trumped By Subpoena

Friday November 17: Five things the markets are talking about

The mighty U.S dollar begins the last trading session on the back foot against most of its major peers as a probe into Russian influence on the 2016 U.S election is said to have deepened.

Note: Special Counsel Robert Mueller is said to have served Trump's election campaign a subpoena in mid-October – this suggests that his ongoing criminal investigation is aggressively pursuing links between campaign officials and Russia.

Elsewhere, global equities have produced some mixed results overnight as the EUR (€1.1796) strengthened.

This morning's Canadian CPI data (08:30 am EDT) will be crucial since BoC governor Poloz defended the central bank's upbeat inflation projections in his last speech. The market is pricing in odds of +40% that the BoC hikes in January.

1. Stocks mixed results

In Japan, the Nikkei share average rose to a one-week high overnight, helped by gains in most sectors. The Nikkei ended +0.2%, it's highest closing since Nov. 10. However, it fell -1.3% for the week, snapping a nine-week winning streak. The broader Topix gained +0.1%.

Down-under, Aussie shares rose modestly, trimming the week's slide as the country's big banks provided support. The S&P/ASX 200 rose +0.2%, resulting in a -1.2% weekly drop for the index.

In Hong Kong, stocks followed regional indices higher, with sentiment aided by strong Wall Street earnings and a step forward on U.S tax reform. The Hang Seng index rose +0.6%, while the China Enterprises Index gained +0.7%. For the week, the Hang Seng gained +0.7%, while HSCE lost -1.2%.

In China, stocks have their worst week in three-months amid worries on the domestic economy. The blue-chip CSI300 index rose +0.4% for the day, while the Shanghai Composite Index closed down -0.5%. For the week, the CSI300 was up +0.2% and the SSEC lost -1.5%.

In Europe, stocks have opened largely flat and moved lower as the session progresses. There is attention on the Italian banking sector again as banks are having difficulty raising capital. Elsewhere, energy stocks are supported by crude oil prices.

U.S stocks are set to open in the ‘red' (-0.2%).

Indices: Stoxx50 -0.2% at 3,554, FTSE -0.2% at 7,370, DAX -0.1% at 13,031, CAC-40 -0.2% at 5,325, IBEX-35 -0.4% at 10,043, FTSE MIB -0.6% at 22,073, SMI -0.2% at 9,130, S&P 500 Futures -0.2%

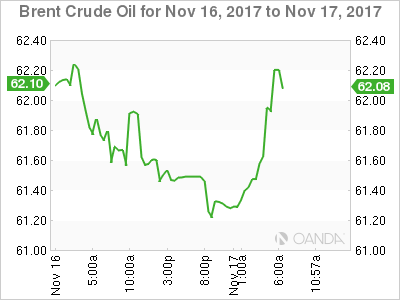

2. Oil set for first weekly fall in six on oversupply, gold higher

Oil prices have rallied overnight, but remained en route for their first week of losses in six, as concerns grew over Russia's support for an extension of the crude output cuts.

Brent crude oil is up +50c at +$61.86 a barrel, while U.S light crude is at +$55.90 a barrel, up +76c.

Note: Prices are set to fall between -2 and -4% for the week as a whole.

An agreement by the OPEC and other producers such as Russia to limit oil production has propped up prices in recent months, with the deal expected to be extended at the group's next meeting on Nov. 30.

However, Russian support for a formalized extension of production cuts at the next OPEC meeting appears questionable, even if only to defer the decision to Q1 next year.

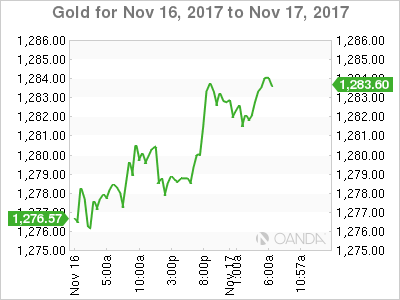

Gold prices rally as the ‘mighty' dollar weakens on report Trump's election campaign has been subpoenaed. Spot gold is up +0.2% at +$1,281.51 per ounce. It is up about +0.5% for the week and is poised to post a second straight weekly gain.

3. Yields curves continue to flatten

U.S bonds continue to ‘flash' some uncomfortable warning signs about the U.S economy, as the gap between longer-term and shorter-term yields narrows even further. The U.S benchmark spread (2/30) is back below +70 bps.

Note: The past seven U.S recessions came following ‘inversions' curve, so the longer the current flattening goes, the more nervous the market becomes.

From here, sovereign yields are expected to range trade for the remainder of this year now that the Fed's rate increase for December is almost fully priced in, and while the ECB has set its course for most of 2018.

The yield on 10-year Treasuries has fallen -1 bps to +2.36%, while in Germany, the 10-year Bund yield has gained +1 bps to +0.39%, the biggest gain in a week. In the U.K, the 10-year Gilt yield has climbed +2 bps to +1.324%.

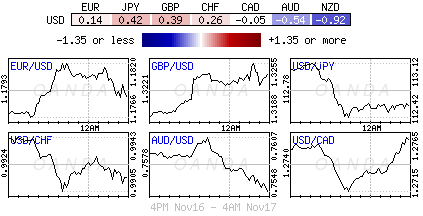

4. Dollar under pressure

The USD is trading softer against its Tier 1 currency pairs, mostly on the back of reports that special counsel Robert Mueller has issued a subpoena to President Trump's election campaign back in mid-Oct in relation to documents on Russia.

Note: This is the first time that Mueller has officially requested information from the campaign.

The EUR/USD higher by +0.2% at €1.1795, while USD/JPY is off by -0.4% at ¥112.55.

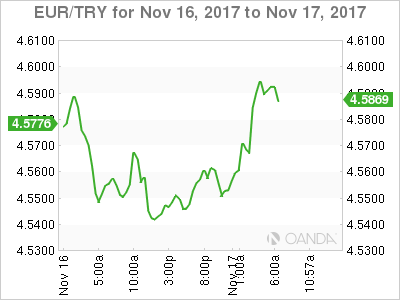

In EM pairs, the Turkish lira (TRY) again trades under pressure after Turkey's President Erdogan again criticized the central bank. The market is pricing in the risk that the CBRT may do something wrong only because its been pressured into further easing. EUR/TRY is trading atop of €4.59 area, higher by +0.9%.

Down-under, both the Aussie (A$0.7544, down -0.4%) and Kiwi (NZ$0.6785, down -0.85%) pairs are again underperforming, pressured by China's growing theme that domestic credit and growth were slowing down and would negatively impact Australia and New Zealand's economy.

5. Draghi's comments

With little data out during the Euro session, the market focused on ECB's Draghi comments from a banking conference in Frankfurt. His comments were in-line with recent October policy statement.

He noted that the Euro region was in the midst of economic recovery with increasing confidence that the robust momentum would continue going forward. He did not see inflation moving steadily away from the very low levels of recent years.

He again reiterated the council's view that they were not at a point where the recovery or inflation could be self-sustained without the current accommodative monetary policy. Extension of QE had anchored rate expectations.

Technical Outlook: Copper – Limited Recovery To Precede Fresh Bears

Bears showed strong indecision above daily cloud which twisted on Thursday and is widening.

Double long-legged Dojis, lest last two days confirm near-term scenario, with fresh recovery attempts on Friday, being so far limited by 55SMA ($3.0673).

Technicals remain firmly bearish on daily chart and favor further downside, as persisting fears over reduced demand from China, keep the price under pressure.

Selling upticks is seen as preferred near-term scenario as reversal of slow stochastic from oversold territory supports the notion, with strong offers seen at $3.0800/40 zone (hourly cloud top / falling 10SMA.

Break above the latter would delay bears for extended correction towards descending 20SMA ($3.1144).

Res: 3.0673, 3.0775, 3.0838, 3.0962

Sup: 3.0475, 3.0324, 3.0110, 3.0000