Sample Category Title

Weekly Economic and Financial Commentary: Data Supportive of Fed Funds Hike in December

U.S. Review

Data Supportive of Fed Funds Hike in December

- Three of the leading U.S. inflation indicators, the consumer price index, the producer price index and the import price index, collectively showed a firming of inflation in October.

- Industrial production growth surged in October, but the gain was overstated by rebound effects from Hurricanes Harvey and Irma.

- Retail sales rose 0.2 percent in October. Over the past year, sales are up 4.6 percent amid strength in building supplies and non-store retailers.

Data Supportive of Fed Funds Hike in December

A slew of economic data were released in the United States ahead of the short holiday week. Three of the leading U.S. inflation indicators, the consumer price index, the producer price index and the import price index, collectively showed a firming of price growth in October (see chart on front page). Although the headline CPI decelerated slightly in October, the slowdown reflected a decline in energy prices as the supply disruptions surrounding Hurricanes Harvey and Irma abated. Excluding food and energy, inflation was noticeably stronger. Core services have been the primary source of inflation weakness this year, but services prices rose 0.3 percent in the month, while core goods prices also posted a rare increase.

For the second consecutive month, the PPI for final demand beat expectations, rising 0.4 percent in October. Core producer prices, excluding energy, food and trade services, reached a fresh record high for this relatively new (2013) series. In addition, the import price index showed the strongest rate of nonfuel import price inflation in more than five years. On balance, inflation has not rebounded sharply from its recent slowdown, but neither has it continued to fall. As a result, the stabilization of price growth and our expectation that it will slowly pick up should keep the FOMC on the path of gradual rate increases in the months ahead.

Industrial production jumped 0.9 percent in October, led by a 1.3 percent surge in manufacturing output, which matched the largest monthly increase since 2010. The factory sector has been held back over the past few months as Hurricanes Harvey and Irma knocked some capacity offline that has only now begun to swing back in full force. The Federal Reserve, which produces the industrial production statistics, estimates that, excluding the effects of the hurricanes, output advanced just 0.3 percent for the total index and 0.2 percent for manufacturing. Although the output data have been noisy recently, the trend remains broadly upward. Industrial production and manufacturing output are up 2.9 percent and 2.7 percent year over year, respectively, a clear improvement from the past couple years (top chart).

Retail sales rose 0.2 percent in October, and September's surge was revised higher to 1.9 percent. This was stronger than expected, as consensus had penciled in a flat month of sales as the boost from gas prices, building supplies and auto sales associated with the hurricanes eased from September. Control group sales— which exclude autos, food, gasoline and building materials—were less impacted by the hurricanes in September, and were up a stronger 0.3 percent in October. Over the past year, retail sales are up 4.6 percent, with continued strength in building supplies and non-store retailers (middle chart).

Housing starts rose 13.7 percent in October, halting a streak of three consecutive monthly declines and ending the week of data on a high note. The volatile multifamily component surged 36.8 percent, overstating some of the headline strength, but single-family starts posted a 5.3 percent increase as well. Year to date, single-family starts have risen 8.4 percent (bottom chart).

U.S. Outlook

Existing Home Sales • Tuesday

Resales increased in September after three consecutive months of decline. The continued strain from lean inventories has brought the year-to-year comparisons into negative territory, however. Existing home sales were down 1.5 percent over the year, but inventories were off even more, down 6.4 percent.

Data were also impacted in September as hurricanes shut down active markets in the South, though sales in other regions were enough to offset the decline. Pending home sales, which measure signed contracts and tend to lead existing sales by 1-2 months, were flat in September following a decline in August. Softness was largely in the South suggesting the hurricane effects have not fully flushed out in the resales data, which bears watching in coming months. Still, demand is strong in the housing market and recent weakness is largely due to the lack of available homes for sale.

Previous: 5.39M Wells Fargo: 5.38M Consensus: 5.40M

Durable Goods • Wednesday

Recent data from the factory sector have been largely positive. The final statistics for September durable goods showed a 2.0 percent increase on the month. Data for August and September have been impacted to some degree by the hurricanes and some payback may be in the offing in October. Looking through the disruptions, the road ahead looks generally positive for upcoming factory orders. Core orders in September were up 1.7 percent and running at a very strong 12.4 percent annualized pace, which supports our outlook for a healthy pace of equipment spending through year end.

The ISM manufacturing index for October softened only slightly from September's recent high but remained in solid expansion character. The new orders index also pointed to expansion in October. Still, there will likely be some payback from the distortion resulting from the hurricanes in October, but we remain upbeat about the underlying trend.

Previous: 2.0% Wells Fargo: 0.1% Consensus: 0.3% (Month-over-Month)

Consumer Sentiment • Wednesday

The University of Michigan's measure of consumer sentiment hit a cycle high in October on broad based optimism both about current conditions and expectations for the future. Over half of the consumers surveyed expected good times to continue for the next year, and 51 percent expected uninterrupted expansion for the next five years. Consumers had good reason for optimism, as the low unemployment rate reinforced confidence in the job market and income prospects. The continued uptrend in the stock market also gave reason for financial optimism. Recent data for personal spending suggest consumers are indeed spending more, though income gains continue to lag—making the current trend unsustainable in the long term unless income growth starts to pick up. The first look at consumer sentiment in November showed a slip from October but remained in elevated territory.

Previous: 100.7 Consensus: 99.0

Global Review

Steady Growth in the Global Economy

- The global economy has continued to show signs of steady economic growth even though growth varies across countries. Case in point was this week's release of Russia's economic performance during the third quarter of the year, which came in lower than market expectations, up only 1.8 percent on a year-earlier basis.

- Meanwhile, the Eurozone reported that industrial production was down 0.6 percent in September on a sequential basis after a strong result in August, up 1.4 percent sequentially.

Steady Growth in the Global Economy

The global economy has continued to show signs of steady economic growth even though growth varies across countries. Case in point was this week's release of Russia's economic performance during the third quarter of the year, which came in lower than what markets were expecting, up only 1.8 percent on a year-earlier basis. As we pointed out on our report on Russia's Q3 GDP, while personal consumption seems to have remained relatively strong in Q3 the probable culprit for the slowdown in economic activity was probably due to a slowdown in investment spending. More detailed results on Russia's GDP numbers will be ready later in the year.

Meanwhile, in China, industrial production increased a slightly weaker than expected 6.2 percent in October compared to a growth rate of 6.6 percent in September of this year, year over year. Markets were expecting a 6.3 percent reading for the index in October. On the other hand, Chinese retail sales increased 10.0 percent in October versus a year earlier versus an increase of 10.3 percent in September. Markets were expecting a growth rate of 10.5 percent. That is, these two measures of activity showed the Chinese economy a bit weaker in October of this year compared to September's readings.

Also in Asia, Japan released its Q3 GDP results and although it was weaker than the print reported in Q2 the economy grew for seven quarters, back to back which, for Japan, is not something that has come easy since the first days of the depression that started in the 1990s. This time, the Japanese economy increased 1.4 percent in annualized terms. Furthermore, growth was motorized by the export sector in Q3 rather than by domestic consumption, which was the case in Q2. In fact, personal consumption expenditures were negative during the quarter.

Meanwhile, the Eurozone reported that industrial production was down 0.6 percent in September on a sequential basis after a strong result for August, up 1.4 percent sequentially. Markets were expecting a payback due to the strong print reported the previous month. On a more current release, the Eurozone ZEW Survey of expectations was up to 30.9 in November compared to 26.7 in October, which points to continuous improvement in the Eurozone economy going forward.

In South America, the Brazilian economy continues to make slow but sustained forward progress even if the political environment remains uncertain. Brazilian retail sales increased a strong 0.5 percent in September after falling 0.4 percent the previous month. On a year-earlier basis retail sales were also strong, up 9.3 percent compared to rate of 7.7 percent in August. Of course, for a while we are going to see very strong numbers coming from Brazil because the base of comparison is so slow that any uptick in economic activity will show as if the economy were booming.

Having said this, the improvement in consumption is probably related to the strong slowdown in inflation and the appreciation of the Brazilian currency over the last several years, which is helping the purchasing power of Brazilian consumers.

Global Outlook

Brazil Economic Activity Index • Monday

The Brazilian economy endured a deep recession in 2015 and 2016, but real GDP growth has turned positive again on a sequential basis this year. Data on the economic activity index, which has a high degree of correlation with real GDP growth, are slated for release next week. The data will be for September, which will give analysts an opportunity to sharpen their GDP growth estimates for the third quarter.

Brazil has a few different measures of consumer price inflation, and some of them are on the docket next week. In general, economic weakness and currency appreciation have led to a marked decline in Brazilian inflation this year. The central bank has slashed its main policy rate from 14.25 percent in October 2016 to 7.50 percent at present. Although the central bank is probably nearing the end of its easing cycle, it could cut rates a bit more if inflation falls even further.

Previous: 1.6% Consensus: 1.4% (Year-over-Year)

Eurozone PMIs • Thursday

The sharp rise in the purchasing managers' indices in the Eurozone over the past year or so is consistent with the acceleration in economic activity in the euro area that has occurred over that period. The PMI data that are on the docket for November will be helpful in gauging the strength of economic activity thus far in the fourth quarter.

Data released this week showed that real GDP in Germany grew 0.8 percent (not annualized) in Q3-2017. On a year-over-year basis, real GDP growth rose to a 6-year high of 2.8 percent. The German statistical office will provide a breakdown of the Q3 GDP data into its underlying demand-side components on Thursday. The Ifo index of German business sentiment will print on Friday. The "headline" index currently stands at an all-time high.

Prev. Manufacturing PMI: 58.5 Consensus: 58.2 Prev. Services PMI: 55.0 Consensus: 55.2

Mexican GDP • Friday

Mexico will release its second estimate of real GDP growth in Q3- 2017 on Friday. Preliminary data that printed a few weeks ago showed that real GDP growth slowed to 1.6 percent on a year-overyear, non-seasonally adjusted basis. On a seasonally adjusted basis, real GDP contracted 0.2 percent (not annualized) in Q3. The revised data that are slated for release next week will provide the first breakdown of real GDP into its underlying demand components. Therefore, analysts will get a more complete picture of the current state of the Mexican economy.

On Thursday, Mexican statistical authorities will release bi-weekly CPI inflation data. The CPI inflation rate ended last year at 3.4 percent, but it has nearly doubled this year, and the recent depreciation of the peso will put further upward pressure on inflation, at least in the near term. The Bank of Mexico may need to respond if inflation expectations were to become unmoored. Previous: 1.6% (Year-over-Year) Wells Fargo: 1.6%

Point of View

Interest Rate Watch

Inflation "Mystery" Solved?

Slower inflation this year, as the labor market has reached full employment, has in the words of Fed Chair Janet Yellen been somewhat of a "mystery." Core inflation, measured by the PCE deflator, has slowed to 1.3 percent after coming up just shy of the FOMC's 2 percent target in February.

Most Fed officials have viewed the weakening primarily as the result of a few "idiosyncratic" factors, like cheaper cell phone plans, and consequently pushed ahead with higher interest rates and balance sheet normalization. Yet without signs of an inflation rebound, the Fed's plans for three rate hikes in 2018 has looked to be in jeopardy (top graph).

CPI data this week suggest that the slowdown in inflation since the start of the year is temporary. Headline inflation in October was held down by lower energy prices, but core inflation posted a solid gain. Over the past three months, core CPI has risen at a 2.4 percent annualized rate and suggests the year-over-year rate (1.8 percent) will soon be headed higher.

While many components of the CPI feed into the estimates of the Fed's preferred measure of inflation, the PCE deflator, one noteworthy exception is healthcare. Since only about a quarter of healthcare costs are paid directly by consumers (versus employers or the government), initial monthly estimates are derived from the PPI report. An 18-month low in healthcare inflation by this measure suggests that even with the unwinding of one-offs, core PCE's rebound is likely to be slow.

Good Enough for the FOMC?

Along with the FOMC, we expect core inflation to move higher in the coming year. However, this year's stumble has led some FOMC members to become increasingly uncomfortable with inflation's persistent shortfall. Chicago Fed President Charles Evans, for example, spoke this week about the committee's symmetric target and the need for inflation to average 2 percent over time. So while there are signs that inflation is back on track, the slow recovery still poses risks to derailing the Fed's plans to raise the fed funds rate three times next year.

Credit Market Insights

Auto Loan Delinquencies on the Rise

Data from the New York Fed's quarterly report on Household Debt and Credit released earlier this week showed increases in household debt across the majority of categories in Q3. Overall household debt increased 4.9 percent on a year-ago basis, with the largest jumps year-over-year seen in credit cards and auto loans, up 8.2 percent and 6.9 percent, respectively.

Additional analysis from the New York Fed noted potential concern regarding the auto loan component of the report. Auto loan originations reached their second highest level post-recession, with the total volume now at $150.6 billion in Q3. Of specific concern are auto loans made by auto finance companies such as auto dealers and manufacturers. Delinquency rates on subprime loans from auto finance companies, namely those made to borrowers with a credit score of less than 620, are more than double the rates on subprime loans made by banks and credit unions in Q3. The newest data reinforce a broader trend. Delinquency rates on subprime loans made by banks and credit unions have generally improved postrecession, while those made by auto finance companies have continued to deteriorate.

While we have written recently about an overall positive consumer outlook, the trend in auto loans remains an area to watch. As consumers continue to dip into savings to fuel consumption amid slow wage growth, the current pace of household debt growth is likely unsustainable.

Topic of the Week

Comparing the House and Senate Tax Plans

Yesterday the House of Representatives passed its version of a tax package, while the Senate Finance Committee approved an amended version of its plan. The Senate package will now require a full vote on the Senate floor, which lawmakers hope to hold the week of November 27. The two plans contain some key differences that we summarize here and discuss in more detail in a longer report available on our website.

On the individual side, the Senate plan completely eliminates the state and local tax deduction (SALT), while the House plan repeals SALT for income and sales taxes but caps property tax deductions at $10,000. This difference will likely become an issue for lawmakers from high-tax states as the two plans are reconciled. The Senate plan preserves the estate tax, while the House bill repeals this provision after 2024. The Senate's initial markup this week also added a repeal of the Affordable Care Act's (ACA) individual mandate, setting up the potential for a tense debate seen with prior ACA repeal efforts. Notably, individual provisions in the Senate plan sunset after 2025, while corporate changes remain permanent. Sunset provisions are needed to keep budget deficits within the confines of reconciliation rules that allow passage in the Senate with only 51 votes.

On the corporate side, both plans lower the top corporate statutory rate to 20 percent from 35 percent, although the Senate delays implementation until January 2019. Both plans also include full business expensing and deemed repatriation of offshore profits. At this point in the process, the Senate must first pass it's version of the bill with a full vote. Assuming this occurs, unless the House accepts the Senate's plan as is, the two chambers must go to conference committee to reconcile the differences between the two bills. This process will likely take longer than the timeline currently envisioned by Republicans. Subsequently, we maintain our call for final passage of a tax package in Q1-2018.

The Weekly Bottom Line: Hurricanes Turn from Headwinds to Tailwinds

U.S. Highlights

- It was an eventful week across financial markets, with a plethora of economic data, Fed speeches, and political developments keeping investors busy.

- Domestic economic data was robust and beat expectations. Following on hurricane-induced weakness previously retail sales, housing starts and industrial production get a significant boost from rebuilding efforts in October. Recent data suggests that GDP growth was over 3% in Q3 and is tracking near 3% during Q4 -- helping reduce economic slack.

- Diminishing slack should provide comfort for the Fed to raise rates in December -- a view highlighted by several FOMC members this week. The hike is further supported by recent CPI and PPI data which was stronger than expected.

Canadian Highlights

- Economic indicators this week remained consistent with our view that economic activity is holding at an above trend pace in the second half of 2017.

- Headline inflation weakened in October as energy prices reversed previous gains. Underlying inflation indicators were little changed. Nevertheless, strong economic activity and rising wage growth all suggest that inflation will trend higher.

- Downwardly revised estimates of the Canadian neutral policy rate released by the Bank of Canada suggest less room for conventional policy to offset future economic shocks or increases in financial stability risks.

U.S. - Hurricanes Turn from Headwinds to Tailwinds

It was an eventful week across financial markets, with a plethora of economic data, Fed speeches, and political developments keeping investors busy. On the whole, equity markets were largely unchanged from last week's close (as of time of writing), with robust economic data and potential tax reform reinforcing the Fed's resolve to raise rates. This has lifted short-term rates somewhat higher, with the yield on the 2-year Treasury note up 7bps since last Friday.

In contrast, yields on longer-term securities have declined since last week. While a pull-back in oil prices from their recent peak was partly to blame, much of the 5bps pare-back in the 10-year Treasury bond yield was related to increased investor demand for safe assets. There was also a sell-off in the junk bond market, lwidening the spread.

Domestic economic data was in fact quite stellar, with most major releases beating expectations. Importantly, after several weeks of weakness and disruption related to Hurricane Harvey and Irma, data is now firmly showing signs of recovery. After declining during August, retail sales for October continued to rebound. They increased by 0.2% in the month, well above expectations for a flat-print, after an upwardly revised 1.9% surge in September (see Chart 1).

Housing starts too have begun to rebound. After declining during August and September, starts increased by 150 thousand, as previously-delayed projects broke ground. Even more encouraging was the fact that single family starts accounted for much of the gain, surging to match their post-recession peak achieved earlier this year. Additionally, many of the properties that were damaged or destroyed by the storms will need to rebuilt. This trend already appears in permitting data which increased by 72 thousand in October.

Industrial production, hard hit by the recent hurricanes, is is also rebounding strongly. After declining 0.5% in August, as Hurricane Harvey ravaged the Gulf Coast, shutting down refineries and chemical plants, the indicator rebounded sharply. Industrial production was up 0.5% in September and another 0.9% in October. The October surge was largely due to chemicals and petroleum & coal product manufacturing, which surged by 5.8% and 4.0%, respectively (see Chart 2).

Taken together, the recent data indicates that growth in the third quarter was well above 3%, while current tracking suggests that the economy will expand by nearly 3% in last quarter of the year. While the relationship between economic slack and inflation may not be as strong as it had been in the past, most FOMC members believe it still exists. As such, the above potential growth should provide some comfort for the Committee that inflation should over the medium-term converge to the 2% target. On that note, while headline CPI for October decelerated to 2.0% from 2.2% during the previous month as gasoline prices normalized following the hurricanes, core inflation actually accelerated to 1.8% in October (from 1.7%). With unemployment at 4.1% and wage growth seeing signs of firming, inflation should converge and the Fed should hike.

Canada - Growth Holding at an Above-Trend Pace in 17H2

The data flow this week helped reinforce our view that the Canadian economy is expanding at an above trend pace for the fifth, and likely sixth, consecutive quarter.

Manufacturing sales surprised many by rising in September (+0.7% m/m in volume terms). Labor disruptions at an Ontario assembly plant failed to offset a rise in petroleum and coal production in Quebec. As one of the final indicators of third-quarter economic activity, the report is consistent with our call of around 2.0% growth.

With Canada's housing market increasingly garnering international attention, it was encouraging to see October's resale home data confirm that activity and prices are on track for a soft landing. National existing home sales rose 0.9% (m/m) in October, marking the third consecutive advance. A rebound in Ontario dominated sales declines elsewhere, while a modest, broad pullback in new listings could act to support price growth in coming months. While national year-on-year home price growth has slowed to its weakest pace since March 2016, regional price trends remain divergent (Chart 1). Home price growth is trending higher in Vancouver and Montreal, lower in the GTA, and sideways in Calgary.

The successive string of well above-trend growth in Canada since mid-2016 has helped to absorb the economic slack that opened up following the 2014 collapse in oil prices. Nevertheless, wage and price pressures have remained subdued. This morning's data on consumer prices for October was largely uneventful, with the headline index (+1.4% y/y) giving back some of the recent energy-price driven gains. The Bank of Canada's preferred inflation measures were mixed, although CPI-common rose to its highest rate in sixteen months (Chart 2). Still, there is good reason to believe inflation will trend higher. Wage growth has accelerated alongside strong full-time job gains in recent months. Moreover, a softer Canadian dollar and stable oil prices all suggest that inflation will move toward 2% over the next year.

Rising capacity pressures are consistent with the Bank of Canada moving interest rates higher. However, the risks around the outlook mean that the Bank will remain on hold at least until early next year. But how high can interest rates possibly go? A new research article by Bank Staff this week estimates that the nominal neutral interest rate for Canada is likely within the 2.5% to 3.5% range (prev: 4.5% to 5.5%). The key implications are twofold: a lower neutral rate increases the probability of the Bank hitting its estimated effective lower bound of about -0.5%; and lower rates could exacerbate financial stability concerns by encouraging riskier borrowing behavior.

The Bank is already working to adapt to the risks posed by low rates. In a speech this week, Senior Deputy Governor Carolyn Wilkins highlighted forthcoming changes intended to strengthen the policy framework. In addition to a risk-focused research agenda, next year the Bank will improve its communication and transparency by timing its speeches to better align with fixed announcement dates between MPRs. This is a welcome move by the Bank that should help give both market participants and the average Canadian a better understanding of the policy decisions undertaken.

Canada: Upcoming Key Economic Releases

Canadian Retail Sales - September

Release Date: November 23, 2017

Previous Result: -0.3% m/m, ex-auto: -0.7% m/m

TD Forecast: 0.9% m/m, ex-auto: 1.1% m/m

Consensus: N/A

A rebound in core retail activity and surge in gasoline prices should help drive a 0.9% increase in total retail sales for September. Core retail sales (ex. auto and gasoline) saw one of the largest declines of the post-crisis period in August and such outsized moves tend to correct the following month. Gasoline station receipts will add another source of upside with prices up nearly 5% at the pump due to hurricane effects. Auto sales are likely to see a modest pickup but will be a net drag due to the sizeable increase in sales outside of the dealer's lot; motor vehicle sales are running over 10% y/y so some moderation should not be seen as overly bearish. This would leave ex-auto sales up 1.1% for their strongest gain since April. Real retail sales should underperform the nominal increase and after negative prints in July and August, are likely to come in largely unchanged for the third quarter as a whole.

Dollar Mixed Ahead of Fed Minutes

Politics drive dollar while fundamentals boost euro

The USD gained against commodity currencies but was soft against safe havens given the political situation in Washington. The Trump Administration scored a major victory with Congress passing the tax overhaul bill by a vote of 227-205. The Senate proposal will be voted after Thanksgiving and diverges from the congress version with Republicans aiming at passing both and consolidating into a single bill. The positive momentum from the legislative victory was short lived as it emerged that Special Council Mueller subpoenaed the Trump campaign regarding its ties to Russia.

Politics will play a big part during the week as the UK Prime Minister's authority has been questioned and could end in a no confidence vote with sterling traders looking for more clues on this development. Brexit negotiations are ongoing but there have been a recent string of concerns regarding how well thought out the whole divorce strategy really is.

The U.S. Federal Reserve will publish the minutes form its November meeting on Wednesday, November 22 at 2:00 pm EST. There will be more clues on where certain policy makers stand regarding inflation, but the market is still pricing in a 99 percent probability of a US rate hike in December. With the US market closed on Thursday and Friday due to the Thanksgiving holiday European PMI releases on Thursday, November 23 could boost the EUR if the string of positive data continues in Europe.

The EUR/USD gained 1.10 percent in the last five days. The single currency is trading at 1.1792 after making most of the gains this week early on strong economic data out to Europe and the ongoing political quagmire in the US. MarketPulse Analyst Kenny Fisher pointed out the strong performance of European fundamentals.

The eurozone economy continues to perform well in the third quarter. German GDP accelerated to 0.8%, while Eurozone Flash GPD remained steady at 0.6%. However, inflation remains the fly in the ointment, with levels well below the ECB target of around 2 percent. Weak inflation has kept the ECB cautious regarding its monetary stimulus program. The ECB said in October that it would chop asset-buying from EUR 60 billion to 30 billion each month, but added that it was extending the scheme until September 2018. Jens Weidmann and other senior policymakers want the ECB to act more aggressively, and have called on the ECB to announce a termination date to its stimulus program. However, Mario Draghi appears in no rush to wrap up the scheme, especially with no inflation pressures on the eurozone economy. With Draghi and Weidmann holding different views on stimulus, it will be interesting to hear both central bank heads speak at the same event on Friday.

The NAFTA fifth round of talks have entered its second day and for this round the Trade Ministers from the three nations will not be present. They held talks at the APEC Meeting in Vietnam. This could free up the negotiators to move forward in the renegotiation of the Trade agreement with less political interference. Ministers might also not be present in the sixth round held in Washington.

European Central Bank (ECB) President Mario Draghi will be speaking on Monday, November 20 at 9:00 am EST during his testimony before the European Parliament. He is not expected to wander too much from the comments he made earlier today. He has reiterated the need for patience when normalizing monetary policy. Europe has posted strong numbers, but inflation remains an area where gains have lagged.

Oil prices rebounded on Friday and almost recouped all the losses form earlier in the week. The price of West Texas Intermediate is trading at $56.31 but it did fall below the 55 price level after a surprise buildup of weekly crude inventories in the US. The arrests in Saudi Arabia and the high probability of an extension to the Organization of the Petroleum Exporting Countries (OPEC) production cut boosted oil prices.

On the other hand higher expected production out of the US and lower demand estimates from the International Energy Agency (IEA) combined with the surprise gain reported on Wednesday. Crude shorts took profit ahead of the weekend to avoid more uncertainty as more news could come out of the Middle East on the weekend, which ended up putting WTI within a small distance from the start of the week.

The battle between the rise in production in the US and the cut agreement between OPEC and other major producers will continue. The Russian Energy Minister Alexander Novak spoke yesterday to reassure that Russian producers are committed to the agreement to cut output, but he did not mention if they will go ahead with an extension of said agreement. The OPEC and major producers will meet in Vienna on November 30.

Ecuador has stopped its plans to seek an exemption from the OPEC deal after prices have reacted to the group's production agreement. The small oil producing nation had also floated the idea of leaving the cartel to be able to pump at levels that would make it easier to balance the country's budget.

Iraqi and Turkish officials are close to reassuming crude exports form the Kurdish region of Kirkuk. The independence referendum was not recognized by Iraq and backed by Turkey it threatened military action. Oil production form the region has not been able to leave for export but those issues are now being worked out between Turkey and the Iraqi government.

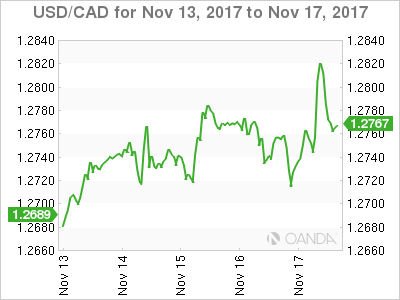

The USD/CAD gained 0.92 percent during the last five trading days. The currency is trading at 1.2801 despite the price of oil walking back most of the losses this week. A low inflation data point on Friday at 0.1 percent and Bank of Canada (BoC) Deputy Governor Wilkins speaking in NY did not leave the market a clear message that a rate hike is in the cards for the Canadian interest rate this year.

The loonie had a moment on Thursday with petroleum and coal products were behind the lift in Canadian manufacturing sales. The forecast form economists called for a 0.3 percent decline but instead showed a 0.5 gain. The energy industry was the big winner with a 10.3 percent increase in September. The move was short lived as the almost flat inflation reading on Friday after the BoC Deputy Governor already pointed out that it would take more than inflation beating the current target for the central bank to remove eve more stimulus. This is seen as a sign that the BoC could be expecting higher inflation as the loonie depreciates and oil at stable prices could drive higher wages but with the unknown fate of NAFTA and a housing market awaiting new mortgage rules it would be more prudent for the central bank to wait.

Market events to watch this week:

Monday, November 20

- 9:00 am EUR ECB President Draghi Speaks

- 7:30 pm AUD Monetary Policy Meeting Minutes

Tuesday, November 21

- 4:05 am AUD RBA Gov Lowe Speaks

- 6:00 pm USD Fed Chair Yellen Speaks

Wednesday, November 22

- 8:30 am USD Core Durable Goods Orders m/m

- 8:30 am USD Unemployment Claims

- 10:30 am USD Crude Oil Inventories

- 2:00 pm USD FOMC Meeting Minutes

- 4:45 pm NZD Retail Sales q/q

Thursday, November 23

- 4:30 am GBP Second Estimate GDP q/q

- 8:30 am CAD Core Retail Sales m/m

- 11:30 am CHF SNB Chairman Jordan Speaks

*All times EDT

Week Ahead – Flash PMIs, FOMC and ECB minutes, and UK Budget among Highlights in Muted Thanksgiving Week

With few exciting data releases on the calendar next week, attention will likely drift to central bank speeches and meeting minutes, developments on the US tax reform front and the UK Autumn budget.

RBA, ECB and Fed publish their minutes

Three central banks will release the minutes of their recent monetary policy meetings: the Reserve Bank of Australia, the European Central Bank and the Federal Reserve. The RBA is up first on Tuesday with the minutes of its November 7 policy meeting. After a series of recent data all pointing to a subdued inflation picture in Australia, the minutes are unlikely to alter that outlook even if the risks to growth are on the upside. The Australian dollar slid to 5-month lows this week and will probably struggle to find much support from the minutes, unless the Governor, Philip Lowe was to surprise with less dovish remarks in a speech the same day.

The FOMC's minutes of the October 31-November 1 policy meeting, due on Wednesday, are also not expected to cause much of a stir given that the market odds of a rate hike at the next meeting in December are running above 90%. However, the euro may be more responsive to the ECB's accounts of its October 26 meeting, which are published on Thursday. ECB President, Mario Draghi, had revealed in his press conference after the meeting that the Bank's decision to keep the asset purchase program (APP) open-ended was not unanimous. Any indication in the minutes about the degree of opposition to a further extension of APP could spur the euro even higher, following this week's impressive rally to a one-month high above $1.18.

Draghi testifies before European Parliament

Before the ECB's minutes though, traders will get the chance to hear Draghi speak when he testifies before the European Parliament's Economic and Monetary Affairs on Monday. Also important will be the November flash PMI releases from IHS Markit on Thursday, The Eurozone's composite PMI is forecast to stay unchanged at 56.0 in November. Germany's Ifo business climate gauge will follow on Friday. The index hit an all-time high in October on the back of a booming Germany economy, and is expected to hold near those levels in November.

Trade numbers from Japan and New Zealand

Japan and New Zealand will publish October trade figures on Monday and Thursday respectively. Japan will likely record its 11th consecutive month of positive export growth as the economy enjoys its longest run of uninterrupted growth since the turn of the century. The yen rarely reacts to Japanese trade data but the New Zealand dollar might see more action from the country's respective figures. Also out of New Zealand next week are retail sales numbers for the third quarter on Wednesday. With kiwi traders still fretting about the new government's economic policies and the potential monetary policy implications from reforming the Reserve Bank of New Zealand's mandate, the kiwi could be sensitive to upside surprises to the data.

UK Autumn Budget: end of austerity?

The UK finance minister, Philip Hammond, has been under pressure to ease up on austerity following the Conservative party's disastrous election result in June. In September, the government achieved its smallest budget deficit in 10 years and this may give Hammond the room to reduce the tax burden and increase spending. A pro-growth budget on Wednesday would be positive for sterling as it would raise the odds of a follow-up move by the Bank of England to this month's quarter percentage point rate hike. Also to watch out of the UK next week is Thursday's second estimate of GDP growth for the third quarter.

Quiet week for US ahead of Thanksgiving

The US economic calendar will be unusually light next week as markets will be closed on Thursday for Thanksgiving. Durable goods orders out on Wednesday will be the highlight in terms of data. Friday's flash PMI releases from IHS Markit for November will likely attract more interest than usual in the absence of any competition. A speech by outgoing Fed Chair Janet Yellen on Wednesday should also draw the attention of dollar traders. But the main topic preoccupying investors' minds will probably remain the tax plan as US Senators continue to finalize their version of the bill ahead of an expected vote the week after Thanksgiving.

The US dollar received a short-lived boost after the House of Representatives passed their version of the tax legislation this week. But the Senate's version is proving more controversial with some Senate Republicans already voicing their opposition to it. Should Senators fail to bridge their differences over the coming week, a subsequent delay of the vote could further dampen sentiment for the dollar in the near term.

Australia & New Zealand Weekly: Australian Dollar Weakens Further on Narrowing Aus/US Rates Differential

Week beginning 20 November 2017

- Australian dollar weakens further on narrowing AUS/US rates differential.

- RBA Governor Lowe speaking at ABE annual dinner, RBA Minutes.

- Australia: Westpac MI Leading index, construction work.

- NZ: retail sales and trade balance.

- Euro Area: ECB President Draghi speaks, ECB minutes.

- US: Fed Chair Yellen speaks, FOMC minutes, Thanksgiving.

- Markit flash PMIs.

- Key economic & financial forecasts.

Information contained in this report was current as at 17 November 2017.

Australian Dollar Weakens Further on Narrowing Aus/US Rates Differential

Since mid October the Australian dollar has softened from around USD 0.7825 to USD 0.76. That is in line with our targeted 2017 year end level of USD 0.76. We confirm our forecast that AUD will drift even lower in 2018 ending that year at around USD 0.70.

Readers will be aware that one core driver of this deteriorating outlook for the AUD is our expectation that the overnight yield differential between Australia and the US will narrow significantly. Our target has been that by end 2018 the RBA overnight cash rate will be 38bps below the US federal funds rate.

Further, the yield differential between Australian and US 10 year bonds will collapse to zero by end 2018.

Those dynamics are now well underway.

Back in September, markets assessed the differential between the RBA overnight cash rate and the federal funds rate by end 2018 as around 40bps, a long way from our forecast of minus 38bps.

But in recent weeks that expected margin has narrowed close to zero, still a long way from our target of minus 38bps but a very substantial move in the right direction.

Equally, the spread between the Australian 10 year bond rate and the US 10 year bond rate has contracted from 55bps on September 15 to around 23bps today.

The market's lowering of expectations for RBA hikes and relative bullish sentiment towards Australian bonds is an appropriate response to the run of recent information.

Following the below consensus Q3 CPI print of 0.6% for headline inflation and 0.35% for the core average, the ABS released the CPI reweight. Incorporating the changed weights, we struggle to see a peak in headline inflation any higher than 2.0%yr for the foreseeable future.

That belief proved to be shared by the RBA, as the November Statement on Monetary policy saw significant changes to the policy sensitive inflation outlook. Underlying inflation is now forecast at 1 ¾% for 2017; 1 ¾% for 2018; and 2% for 2019. The August forecasts had underlying inflation at 1½% - 2½% in 2017; 1½% - 2½% in 2018 and 2% - 3% in 2019.

It is our view that the decision to lower the forecasts to below the bottom of the band in 2018 and at the bottom of the band in 2019 has significant policy implications. We are now assessing a central bank which is expecting that it will undershoot its core inflation target for another year, and that, even one year out, inflation will still be at the bottom of the target zone.

We are not changing our view that rates in Australia will remain on hold in 2018 and 2019, but we have always been uncomfortable that the central bank's forecasts were implying that it was expecting it would be raising rates in 2018. These forecasts no longer portray a central bank that expects to raise rates.

In addition to the benign inflationary environment, retail sales data showed volumes up only 0.1% in Q3. This highlights downside risk to the consumption figures in the upcoming GDP release for the September quarter.

Earlier this week, the November Westpac-MI Consumer Sentiment survey fell to 99.7 from 101.4 in October. The detail cast further doubt on the consumption outlook for Q4.

Responses to our annual question on Christmas spending plans point to moderate activity. Just under a third of Australians expect to spend less on gifts this year than last, with 54% expecting to spend about the same and just 11% spending more - the lowest proportion since we began running this question in 2009. Overall the net balance of 'more minus less' is marginally more negative than last year, suggesting we're in for a repeat of last year's lacklustre Christmas spend. The state responses show consumers in Victoria and NSW are a little less inclined to restrain spending while those in SA and WA are tilting more towards cutting back.

It is no surprise that consumers are thinking about reducing spending given their very subdued income growth. This week's Q3 WPI data indicated that wages growth is tracking at 2.0%yr, remaining near historic lows. That was despite the Fair Work Commission's annual wage review decision to increase the minimum wage by an above normal 3.3%. Given last year's minimum wage rise was 2.4%, expectations were for an uplift in quarterly wages growth to 0.7%. However, the actual result came in at 0.5% reflecting softness in wages growth across the broader labour market.

Persistently low income growth is a constraint on consumer spending, particularly given the high level of household debt.

As a country that runs significant current account deficits and high associated foreign liabilities, Australia needs to offer attractive yields in order to fund these liabilities in a world where Australia's assessed risks are not reducing. As we have discussed previously, Australia's housing markets are deteriorating. In the main market, Sydney, house price momentum (6 month annualised) has slowed from 20% in January this year to -0.5% in October.

We are also seeing disturbing headwinds around regulation; taxes; and bank interest rates unnerve investors. This group still explains the dominant component of new lending for housing but in September, we saw a sharp 6.3% fall in lending to investors.

Australia's reliance on foreign investors to fund our large accumulated overseas debt is dependent on offering an attractive yield or a cheaper currency. These factors will be exacerbated if there is some waning in investor confidence. Our housing markets attract relentless scrutiny from foreign investors. Recent developments in the housing market and the near term risks are unlikely to go unnoticed.

The last time Australian rates fell below US rates was in the June 1999 - December 2000 period. The yield differential ranged from minus 25bps to minus 50bps. The AUD entered that period at around USD 0.66 and gradually fell, settling at USD 0.50.

We certainly expect that the targeted yield differential by end 2018 of minus 38bps can be sustained well into 2020 as we expect the overnight cash rate to remain on hold in 2019 as well. There is some consolation in the spread, in that the Federal Funds rate is also expected to remain steady in 2019. This sustained period of a negative interest rate differential is expected to take its toll on the AUD. By mid 2019 we are looking for the AUD to move down to USD 0.68 with the risks pitched to the downside.

Currencies are not only affected by interest rate differentials and confidence. For Australia, commodity prices and the ongoing current account deficit are also important.

Back in 1999-2000, Australia's current account deficit was averaging around 5% of GDP. We expect that over the next two years this deficit will average nearer 2.5% of GDP, thanks of course to China's industrialisation miracle. Australia's terms of trade are around 55% higher now than we saw during that last period of negative interest rate differentials.

Overall around a cumulative US10¢ fall in the AUD is expected. We are not expecting the precipitous US16¢ fall we saw in 1999 and 2000.

The Week that Was

The past week has had a focus on confidence and the labour market for Australia. Offshore, US retail and CPI inflation came in line with expectations, but German GDP caught the market off guard.

While confidence was unaffected, business conditions (as reported by the NAB business survey) surged in October to +21, a new all-time high. The gain was highly concentrated by sector (in manufacturing) and by state (in NSW); hence, the result is likely at least partly noise. It remains our belief that the NAB survey overstates current conditions, in part owing to the exiting of uncompetitive firms in some sectors, such as the auto industry. Regardless, the survey continues to provide very helpful guidance on the mix of conditions across the economy (manufacturing and construction strong; consumer-centric sectors weak) as well as the state of the labour market. For employment, the NAB survey suggests that the current strong pace of gains will persist into year end. This is consistent with the October labour force release, see below.

Given the mood of retailers, it is not surprising that after October's 'return to optimism' (a reading of 101.4), Westpac- MI Consumer Sentiment again succumbed in November, falling back to 99.7 - below the 100 optimist/pessimist divide. Whereas concerns over family finances have typically driven declines in confidence over the past year, in this instance it was renewed concern over the economic outlook. The 'economic conditions, next 12 months' index largely unwound last month's bounce, falling 6.2%; meanwhile, the five-year outlook fell 2.2%. Both of these sub-components are likely to have been affected by political uncertainty over the 'citizenship' saga.

On consumer spending, it remains the case that lingering concerns over family finances are restricting demand. Perceptions of family finances did improve in the month, but they remain at below average levels despite continued strength in employment growth and a favourable mood amongst households towards the labour market overall. Having fallen back in November, 'time to buy a major household item' is currently 7% below average. Each year, our November survey also provides colour on households' Christmas spending plans. In 2017, spending plans are downbeat, with just under a third of consumers expecting to spend less than last year, and 54% the same; only 11% plan to spend more than last year. The overall result is marginally down on last year, implying a repeat of 2016's lacklustre sales. On housing, the 'time to buy a dwelling' series did rise 3.4% in the month, but still stands 18% below average. Interestingly, in November, NSW improved as Victoria deteriorated; this follows an easing in house price growth in NSW as price gains held up in Victoria. Household's views on the housing market are clearly being affected by perceptions of affordability and competition.

One of the persistent concerns for households is weak wages growth and the Q3 wage price index indicated a continuation of subdued growth. See chart of the week below for further detail.

The enduring weakness in wages remains a stark contrast to employment growth as per the labour force survey. October only saw a net gain of 3.7k jobs. However, that came as a result of a 24.3k increase in full-time employment, and saw the annual pace of total employment growth sustained at 3.0%. At nearly twice the pace of population growth, employment growth is unquestionably strong. As we have highlighted on a number of occasions, there are two factors behind the great divide between employment growth and wages: (1) the jobs that are being created are typically lower-paid positions, an outright negative for growth in average incomes across the population; and (2) while the unemployment rate is less than half a percentage point from its full employment level, the rate of underemployment has continued to trend higher over the past three years and is presently near its historic high. Broadly, the supply of potential workers is plentiful; hence, there is no meaningful pressure on wages growth.

Switching to the global economy, little new information came to hand this week. Debate over tax reform has been continuing in both the House and Senate, and the House passed their version overnight. However, the Senate is still discussing its own version of reform, and won't vote on it until after Thanksgiving. After that, the discussions on a compromise bill will begin, which is the hard part. It will likely be some time before their similar-but-different plans on tax reform become a unified bill that can be put to a final vote.

On the data front, retail sales and the CPI were both broadly as expected and of little significance for policy. But September quarter GDP growth caught the market's attention, particularly the ongoing acceleration in the pace of growth in Germany. While this may see more disquiet amongst German authorities over the stance of Euro Area policy, the reality is that the growth and labour market outlook for the Continent as a whole are a long way from justifying higher inflation and tighter policy expectations. For further details on growth across the region and the outlook, see this week's Northern Exposure.

Chart of the week: Q3 Wage Price Index

One of the persistent concerns for households is weak wages growth. We, the market and the RBA were anticipating a reprieve in the September quarter, with the wage price index expected to gain 0.7% - supported by a known 3.3%yr rise in the minimum wage effective 1 July.

Despite this positive impetus, the wage price index disappointed materially, coming in at just 0.5% in Q3 and 2.0%yr. We estimate that, abstracting from the minimum wage effect, underlying wage growth in Q3 was likely around 0.3% - a very weak outcome. The weakness in wages remains broad based, with private wages up 1.9%yr and the public sector 2.4%yr. Within the private sector: the strongest performing industries were arts & recreation and health care & social assistance (both up 2.7%yr), while mining continued to see the slowest wage growth, circa 1.2%yr. All of these outcomes are soft versus history, and would have come as a significant surprise to the RBA.

New Zealand: Week Ahead & Data Wrap

Brave new-ish world for monetary policy

For nearly 30 years now, New Zealand monetary policy has been squarely focused on ensuring price stability. What this has meant in terms of a precise inflation target has been tweaked a little over time. In addition, successive updates to the Policy Targets Agreement (PTA) have directed the RBNZ to also consider factors such as asset prices and volatility in the exchange rate in its pursuit of price stability. But despite such changes, the core of the monetary policy framework has essentially remained intact since its inception.

However, over the coming months we're likely to see a large shake-up in the framework. The Labour-led coalition Government has signalled that it intends to expand the RBNZ's mandate to include a focus on maximising employment as well as price stability. There's also likely to be a change in the decision making structure at the RBNZ, with a shift away from the current single decision maker model to a committee structure.

With regards to the decision making structure, the proposed shift to a committee doesn't imply a big change to how the RBNZ sets policy. The RBNZ already uses a committee structure for some of its internal policy deliberations, and it includes a number of external advisers. Importantly, this change on its own doesn't imply a shift in the RBNZ's thinking with regards to the balance between activity and inflation.

In contrast, the shift to a dual mandate could have larger implications for the stance of policy. Recent media comments from the Minister of Finance indicate that the Government wants the RBNZ to place more emphasis on the state of the labour market than it has in the past. In addition, a new Governor will step into the ring in March, and the Finance Minister has signalled that he favours the appointment of someone who will follow the spirit of the coming changes to the RBNZ's mandate (the actual selection of Governors is made by the RBNZ's Board, but must be approved by the Minister).

The key question is whether adding the goal of 'maximising employment' will materially affect the RBNZ's behaviour? Not necessarily. The RBNZ has always been conscious of how its decisions will affect the real economy, including the potential impacts on the labour market and unemployment. In addition, the Government has indicated that it will not set a numerical target for 'maximum employment', or direct the RBNZ how to act when the two goals appear to conflict. Such a specification, along the lines of the dual mandates of the US Federal Reserve and the Reserve Bank of Australia, might prove to be fairly benign.

However, a key concern with a 'maximum employment' goal is that it's not symmetric. We doubt it would have prompted the RBNZ to act any differently in recent years, when both inflation and unemployment pointed in the direction of keeping interest rates low. But the acid test would come when the economy is running hot and unemployment is below its long-run sustainable rate (which the RBNZ puts somewhere around 4 to 5%). Keeping inflation on target at these sorts of times would argue for higher interest rates. That would cause a rise in unemployment, putting the two goals in conflict.

If the employment mandate caused the RBNZ to become quicker to cut interest rates and slower to raise them, the consequence would be higher inflation over time. That could actually be detrimental for growth over an extended period. It is possible for monetary policy to generate temporary increases in employment growth. However, it's not possible to run loose monetary policy indefinitely to boost employment growth or keep the unemployment rate artificially low. Attempting to do so ultimately just leads to higher inflation, but not higher employment, as the resulting increases in costs gradually erode the strength of economic activity. That's essentially what we saw around the globe over the 1960s and 1970s.

International and domestic experience has shown that the biggest contribution that monetary policy can make to the economic landscape is ensuring stability in prices. This helps to avoid large swings - up or down - in activity. And over time, this helps to support ongoing, sustainable gains in employment. This is the approach that has been in use in New Zealand for some time.

Housing conditions to remain subdued for an extended period

On the New Zealand data front, the main news over the past week was the release of the REINZ house sales figures for October. Recent weeks have seen some easing in mortgage rates, which has given the housing market a bit of a boost. We've seen this most clearly in Auckland, where house prices have been creeping higher again after moderating in the early part of the year. And we could see this continue for while a while yet.

But despite the recent pick up, New Zealand's housing market is still looking a lot softer than it did this time last year. Sales are down 15% since last October. At the same time, the double digit house price growth we saw in previous years has given way to a period of quite subdued gains. A range of factors has contributed to this slowdown. This includes the creep higher in mortgage rates in late 2016 and early 2017, as well as the tightening in lending restrictions by the RBNZ. Pre-election uncertainty also appears to have had a dampening impact.

We think the New Zealand economy is in for an extended period of weak house price inflation. The new Government is planning on rolling out a suite of regulatory changes over the coming years that will dampen housing market conditions. First off the block will be a ban on non-resident buyers of existing properties. The 'bright line' test for taxing capital gains on investment properties will also be extended from a two-year minimum holding period to five years. Such changes will be reinforced by tighter migration settings that will reduce the rate of growth in demand for housing. Longer-term, the new government has signalled that it will also remove negative gearing (the ability to use losses on rental properties to offset taxable income from elsewhere). Finally, the Government plans to review New Zealand's tax base, which could see further changes to the tax treatment of capital gains from housing.

Data Previews

Aus Oct Westpac-MI Leading Index

Nov 22, Last: -0.2%

- The Leading Index has swung sharply in recent months from well above trend to back below trend, the six month annualised growth rate holding at 0.2% below trend in Sep. The turnaround mainly reflects swings in Australia's commodity prices and to a lesser extent a shift to a rising yield curve implying tightening financial conditions.

- The Oct read will include updates on the ASX200 which surged strongly, up 4%. Other components have been mixed. On the negative side, consumer sentiment based measures deteriorated slightly and commodity prices were down 0.9% in AUD terms. On the plus side, dwelling approvals rose 1.8%; the yield spread widened slightly; and total hours worked continued to tick over. The six month growth rate may pick up given earlier weakness is starting to drop out of the picture.

Aus Q3 construction work

Nov 22, Last: 9.3%, WBC f/c: -2.7%

Mkt f/c: -2.3%, Range: -7.5% to 24.0%

- Currently, the Construction Work survey is an unreliable partial indicator for the National Accounts. Recently, LNG platforms have been imported. The survey includes the full value of the platform when it is imported, rather than actual work in the period, as in the national accounts.

- In Q2, 'construction work' reportedly spiked, +9.3%, boosted by imported platforms (which is included in private infrastructure). For Q3, with fewer platforms imported (1 rather than 2), we expect a partial reversal, -2.7%. We caution, there is a high degree of uncertainty around this forecast - the value of these platforms is unclear, due to commercial in confidence.

- Turning to private building and public works, activity in these areas grew by 1.2% in Q2 and we anticipate a further 1.5% increase in Q3, with broad based strength, across residential, commercial building and public construction.

NZ Q3 real retail sales

Nov 23, Last: +1.7%, Westpac f/c: +0.3%, Mkt f/c: 0.1%

- Retail spending powered ahead in the June quarter, boosted by some high profile sporting events - the World Masters Games and the Lions rugby tour. These events, and the associated strength in tourism inflows, saw strong spending in the hospitality sector. The June quarter also saw spending gains in areas such as building supplies and electronics.

- As we've moved into the second half of the year, the momentum in retail spending appears to have faded. A key reason for this is the slowdown in the housing market, which has dampened spending on durable items like household furnishing. We expect only a 0.3% gain in retail volumes in the September quarter. That would be the slowest growth we've seen since 2015.

Dollar on Track for Second Weekly Decline; Loonie Down on Falling Hike Expectations

Housing data out of the US and Canadian inflation numbers did manage to attract some attention during today's trading though the tone for the day was set earlier with developments on the US political front - most notably a potential connection between the Trump campaign and Russia and progress on the tax story - getting the bulk of today's focus.

At 1525 GMT, the dollar index, which gauges the greenback against a basket of currencies, was 0.2% down on the day at 93.78. On the week, it is lower by 0.7% and is on track to record its second straight weekly decline. The latest political twist after a report on the Wall Street Journal stated that Special Counsel Robert Mueller's team issued a subpoena last month demanding documents that could potentially link Trump's campaign officials with Russia, put the dollar on a negative footing during today's trading.

Dollar/yen traded 0.5% down on the day, hitting 112.32 at one point, its lowest since October 19. The pair was last traded not far above the aforementioned low. Euro/dollar was 0.2% higher, eyeing the 1.18 handle. Pound/dollar was up on the margin and within breathing distance of the 1.32 mark.

The US House of Representatives yesterday voted in favor of a tax-cut package. Attention would now shift to the Senate, where Republicans hold a slimmer 52-48 majority and thus cannot afford to lose more than two within their ranks in an upcoming vote as Democrats are unified in opposing the passage of the relevant tax legislation. Ron Johnson, one of the two Republicans senators that criticized the tax plan said he is optimistic his concerns can be dealt with. It should also be mentioned though, that according to a Time magazine report, four Republican senators have privately made talk about opposing the bill as they have concerns about the rise in the federal deficit it would cause. More developments on the tax front are expected after Thursday's Thanksgiving holiday.

US housing starts grew by 13.7% m/m in October to stand at 1.29 million units, their highest since October of last year. The increase considerably outstripped expectations for a rise by 5.6% as well as the previous month's downwardly revised decline by 3.2%. Building permits for the same month increased by 5.9%, above expectations for a rise by 2.0% and September's fall by 4.5%. It should be mentioned that disruptions by recent hurricanes negatively affected the figures in the previous month and boosted them in October as US citizens started replacing their damaged-from-flooding properties. The dollar index did manage to recover part of its earlier losses following the releases, though the US currency's gains relative to majors were limited for the most part. Also, the gains were not sustained as trading progressed.

Canadian inflation data for October showed the pace of headline inflation slowing relative to the preceding month. Month-on-month, CPI grew by 0.1% and year-on-year by 1.4%, matching expectations. These compare to September's respective figures of 0.2% and 1.6%. The Bank of Canada target for annual inflation is 2%. The deceleration was attributed to weakening energy prices and clothing costs. Core inflation though posted a slight acceleration relative to September. The BoC's measures of inflation gave a mixed picture: CPI common grew by 1.6% y/y (1.5% in September), CPI median expanded by 1.7% y/y (1.8% in September) and trimmed CPI stood at the same figure as September's (1.5%).

The Canadian dollar lost ground relative to its US counterpart as the data went public as forex market participants scaled down their expectations for another rate hike to be delivered soon by the BoC. Dollar/loonie last stood 0.5% higher on the day at 1.2811. At its highest it touched a two-week high of 1.2823. Also related to Canada, NAFTA talks will be held today in Mexico, carrying through to Tuesday.

On the Brexit bill front, UK Prime Minister Theresa May today said that Britain will honor its financial commitments to the EU. The issue is considered as one of the major impediments for progress in negotiations. However, once again no clarity was given on the exact amount. Euro/pound traded 0.1% up on the day, at 0.8926.

In emerging markets, dollar/rand was 0.6% lower at 14.0558 ahead of next week's (November 24) South African credit ratings reviews by agencies Standard & Poor's and Moody's. At its lowest, the pair fell below the 14 mark, recording a 15-day low.

Gold traded 0.5% higher at $1,285.11 per ounce, benefitting from weakness in the dollar. WTI and Brent crude were up by 1.7% and 1.2% respectively, at $56.10 and $62.07 per barrel respectively.

Weekly Focus: Market Correction But Continued Recovery

Market Movers ahead

- Minutes from the October ECB meeting could well provide clues as to what will happen after September next year when the current QE programme is set to end.

- The minutes from the most recent FOMC meeting are less likely to be interesting.

- PMIs in the euro area are likely to show further increases although the stronger EUR weighs on businesses, and Markit PMIs for the US are expected to increase as they are catching up to ISM numbers.

- The Swedish Riksbank's financial stability report is likely to draw attention, given the turnaround in the housing market.

- Survey data could point to a rebound in oil investments in Norway next year.

Global macro and market themes

- In the equity market, we have seen a correction from stretched levels but it should prove temporary.

- The likelihood of US tax cuts has increased and will remain a market theme for the rest of the year.

- Any dips in EUR/USD should be shallow and short-lived and we expect it to move higher again next year.

- We think risks to our outlook for yields over the next couple of months have now become more symmetric and that the downside potential for yields should not be neglected.

US: Homebuilding Rebounds in October, Following Previous Hurricane-Related Delays

After Harvey and Irma disrupted homebuilding activity during August and September homebuilders came back in full force in October. Housing starts rebounded (+155k) to 1,290k, surpassing consensus expectations for a tick up in activity to 1,190k. Building permits also surprised to the upside, rising by 72k to 1,297k.

The good news was amplified by positive revisions to last month's report, with single family starts rising (+44k) to 877k from an upwardly revised (+4k) September reading. The more volatile multifamily segment accounted for the bulk of the increase, rising by 111k to 413k from an upwardly revised (+4k) reading in September.

The number of building permits issued, a good forward-looking indicator of starts, also rose with single family permits up 16k to 839k and multifamily permits 56k higher at 458k.

Activity in the South rebounded strongly (+91k), as hurricane-related rebuilding begun. The Northeast (+43k) and the Midwest (+33k) also saw activity rise, while homebuilding the West subsided (-12k).

Key Implications

This was a good report overall with the pick-up in activity, particularly in the South, confirming that the previous months' lull in activity was fully related to hurricane disruptions and was thus temporary. While the rebound was skewed to the multi-family segment, single-family homebuilding also increased, matching its post-recession record high of 877k achieved in February 2017. Importantly, building permits also rose in October, with robust permitting activity likely to support homebuilding in the months ahead.

Fundamentals in the housing market remain strong, with persistent wage gains and still-low mortgage rates continuing to support demand. The single-family segment, in particular, is set to benefit as the pace of household formation rises alongside positive labor market developments. Builders echoed an optimistic sentiment in November, as hurricane-related uncertainty faded and led the NAHB's index to a level just shy of reaching a post-recession high.

Having said that, builders will continue to face challenges in the coming months, stemming from a dwindling pool of labor. An increase in demand in the South for construction workers related to hurricane-related rebuilding efforts could put a strain on builders in other regions. This will likely lead to rising costs for the homebuilders related to both labor as well as building material costs already lifted by Canadian softwood tariffs.

Builders will likely pass on some of the rise in costs to consumers in the form of higher home prices. This could hinder demand in the near- to medium-term alongside the potential for the elimination of mortgage interest deduction currently debated in Congress. Still, given the solid fundamentals, we expect homebuilding to continue to grind higher over the medium-term, with residential investment being a positive contributor to growth in the coming quarters.

USD/JPY Decline Illustrates USD’s Bleak Performance

- European equities trade near opening levels as yesterday's risk rebound already ran out of steam. US stock markets opened up to 0.3% lower.

- US housing data rebounded more than forecast in October. Housing starts rose by 13.7% M/M (vs 5.6% M/M consensus). Building permits increased by 5.9% M/M (vs 2% M/M forecast). In both cases, September data were upwardly revised.

- Germany's would-be coalition partners resumed talks on Friday after all-night negotiations failed to produce a breakthrough, with Chancellor Angela Merkel's conservatives saying they would compromise further on climate change policies to secure a deal.

- Portugal has made an early repayment of €2.78bn to the International Monetary Fund with the aim of paying back costly bailout loans ahead of schedule as the country's borrowing costs fall in debt markets.

- ECB President Draghi said in a speech in Frankfurt that with the decision to extend QE at a slower monthly pace, the signalling effect of asset purchases has "naturally increased in prominence relative to the duration effect."

- Turkish President Erdogan lashed out at the central bank, saying a lack of government intervention in monetary policy had left Turkey saddled with high inflation and facing a potential slowdown in investment.

Rates

Core bonds gain ground ahead of the weekend

Global core bonds eke out some gains today going into the weekend. Next week's volumes will probably be lower than usual because of the US Thankgiving week. US Treasuries outperformed this morning during Asian trading hours as headlines about Special Counsel Mueller's subpoena outweighed progress on US tax reforms. Trading slowed to a trickle in the European session. Stocks failed to extend yesterday's risk rebound and treaded water. Eco calendars in EMU and US couldn't lure investors into setting up directional trades with only second tier, but stronger, US housing data on the agenda. The Mueller headlines took centre stage again once US investors entered trading, pushing core bonds to intraday highs at the time of writing. ECB president Draghi said that effects of past low inflation in wage formation should not be persistent, but his comments didn't affect dealings with ECB policy tied for at least another 9 months.

At the time of writing, the US yield curve flattens with yield changes ranging between +0.5 bps (2-yr) and -2.5 bps (30-yr). The German yield curve bull flattens with yields 0.5 bps (2-yr) to 1.5 bps (30-yr) lower. On intra-EMU bond markets, 10-yr yield spread changes versus Germany range between -1 bp and +1 bp with Greece slightly underperforming (+3 bps).

Currencies

USD/JPY decline illustrates USD's bleak performance

European markets didn't know how to react to the diffuse news flow from the US. Risk sentiment remained fragile and the dollar stabilized after the overnight setback. Strong US housing data also couldn't provide a lasting support for the US currency. USD/JPY trades in the 112.50 area, within reach of the recent correction low. EUR/USD holds near the 1.18 level.

Asian markets showed a diffuse picture overnight as opening gains were partly undone later in the session. The dollar came under pressure on headlines that President Trump's election campaign received a subpoena of special Counsel Robert Mueller on the links between the campaign leaders and Russia. USD/JPY dropped from the 113+ area and set a minor new low for the week in the 112.40 area. EUR/USD returned north of 1.18.

There were no important eco data in Europe. European investors didn't know how to react to the mixed news flow from the US (tentative progress on the tax debate, deeper investigation on the Russia links of the Trump campaign team). European equities settled in wait-and see modus and so did core bonds and the dollar. EUR/USD and USD/JPY held tight ranges. Comments from ECB's Draghi in Frankfurt didn't change the market's view on the ECB's approach going forward. In the afternoon, US housing data beat consensus by a really big margin. Usually, these data have little impact on the dollar. This time, the dollar temporary gained a few ticks, but the gains couldn't be sustained. The dollar remained in the defensive going into the US equity market opening. EUR/USD trades again close to 1.18. USD/JPY hovers currently in the 1.1775 area. USD/JPY is setting minor new correction lows in the 112.35/40 area. The dollar didn't take out any important support levels today, but USD sentiment remains fragile.

GBP rebound halts as Brexit optimism looks premature

Already for quite some time, the Brexit story is a story of whether the glass is half full or half empty. Yesterday, markets saw indications that the glass is rather half full. Today, it was again half empty. On the side-lines of a meeting of EU leaders in Gothenburg, EU and UK officials had informal talks. Yesterday markets thought they had heard some positive signs. Today, markets were a bit 'unsettled' by comments from UK Brexit minister Davis as he indicated that it was now up to the EU to do some concessions. The news flow from Gothenburg also didn't suggest that big Brexit progress could be in the making. The issue on the Irish boarder also remains a potential roadblock. PM May and EU's Tusk finally came to an obvious conclusion: There is more work to be done! EUR/GBP jumped back north from the low 0.89 area to the 0.8960 area late in the morning session (currently around 0.8945). Cable dropped from the mid 1.3250/60 area and trades currently around 1.3185. Brexit-related volatility will probably continue to affect sterling trading for some time to come. That said, for now sterling stays away from important support levels.

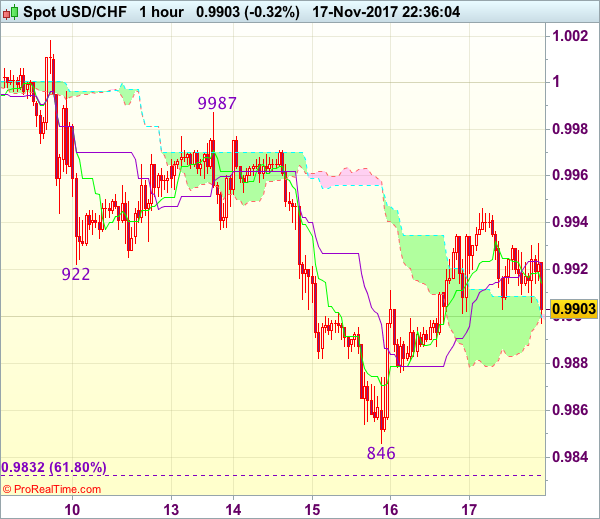

Trade Idea Wrap-up: USD/CHF – Hold short entered at 0.9935

USD/CHF - 0.9902

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9923

Kijun-Sen level : 0.9917

Ichimoku cloud top : 0.9909

Ichimoku cloud bottom : 0.9884

Original strategy :

Sold at 0.9935, Target: 0.9835, Stop: 0.9950

Position : - Short at 0.9935

Target : - 0.9835

Stop : - 0.9950

New strategy :

Hold short entered at 0.9935, Target: 0.9835, Stop: 0.9950

Position : - Short at 0.9935

Target : - 0.9835

Stop : - 0.9950