Sample Category Title

Japan’s Adjusted Merchandise Trade Surplus Unexpectedly Widened In October

.

For the 24 hours to 23:00 GMT, the USD declined 0.88% against the JPY and closed at 112.11 on Friday.

In the Asian session, at GMT0400, the pair is trading at 112.03, with the USD trading 0.07% lower against the JPY from Friday's close.

Overnight data showed that Japan's adjusted merchandise trade surplus unexpectedly widened to ¥322.9 billion in October, against market consensus for a decline to ¥206.7 billion. In the prior month, the nation posted an adjusted merchandise trade surplus of ¥240.3 billion.

The pair is expected to find support at 111.72, and a fall through could take it to the next support level of 111.40. The pair is expected to find its first resistance at 112.52, and a rise through could take it to the next resistance level of 113.00.

Going ahead, investors would look forward to Japan's all industry activity index for September, slated to release tomorrow.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Swiss Franc Trading A Tad Lower In The Morning Session

For the 24 hours to 23:00 GMT, the USD declined 0.56% against the CHF and closed at 0.9884 on Friday.

In the Asian session, at GMT0400, the pair is trading at 0.9886, with the USD trading marginally higher against the CHF from Friday’s close.

The pair is expected to find support at 0.9864, and a fall through could take it to the next support level of 0.9843. The pair is expected to find its first resistance at 0.9919, and a rise through could take it to the next resistance level of 0.9953.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

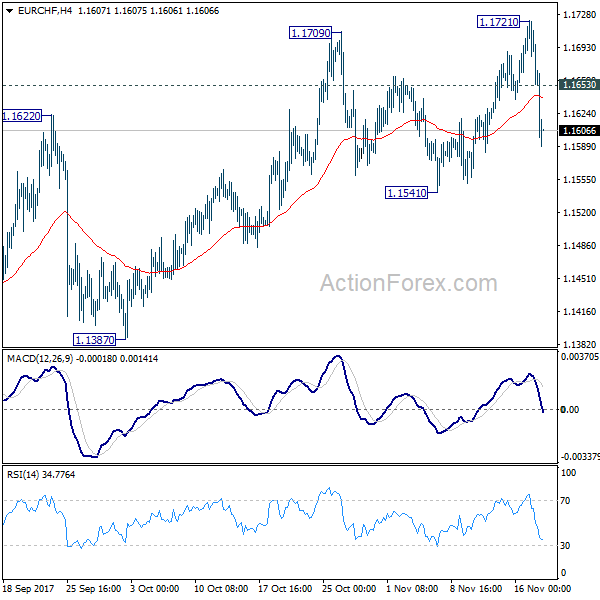

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1629; (P) 1.1676; (R1) 1.1699; More...

The sharp decline of EUR/CHF and strong break of 1.1638 support is raising the chance of trend reversal. Intraday bias in turned back to the downside 1.1541. Considering bearish divergence condition in 4 hour MACD and daily MACD, decisive break of 1.1541 will confirm topping and turn near term outlook bearish for 1.1355 key support. On the upside, above 1.1653 minor resistance will turn bias back to the upside for 1.1721 high instead.

In the bigger picture, long term rise from SNB spike low back in 2015 is still in progress. EUR/CHF should now be heading back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.1355 support holds. However, break of 1.1355 will indicate medium term topping. In that case, EUR/CHF should head back to 55 week EMA (now at 1.1158) and possibly below.

Canada’s Annual Inflation Slowed For The First Time In 4 Months In October

For the 24 hours to 23:00 GMT, the USD slightly rose against the CAD and closed at 1.2755 on Friday.

The Canadian Dollar fell against the USD, after downbeat inflation data in Canada diminished the prospects for a near term interest rate hike.

Data revealed that Canada's consumer price index (CPI) slowed to 1.4% YoY in October, meeting market expectations and easing for the first time in four months. The CPI had recorded a rise of 1.6% in the previous month.

In the Asian session, at GMT0400, the pair is trading at 1.2789, with the USD trading 0.27% higher against the CAD from Friday's close.

The pair is expected to find support at 1.2728, and a fall through could take it to the next support level of 1.2667. The pair is expected to find its first resistance at 1.2837, and a rise through could take it to the next resistance level of 1.2885.

With no major macroeconomic releases in Canada today, investors would focus on global macroeconomic events for further direction.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

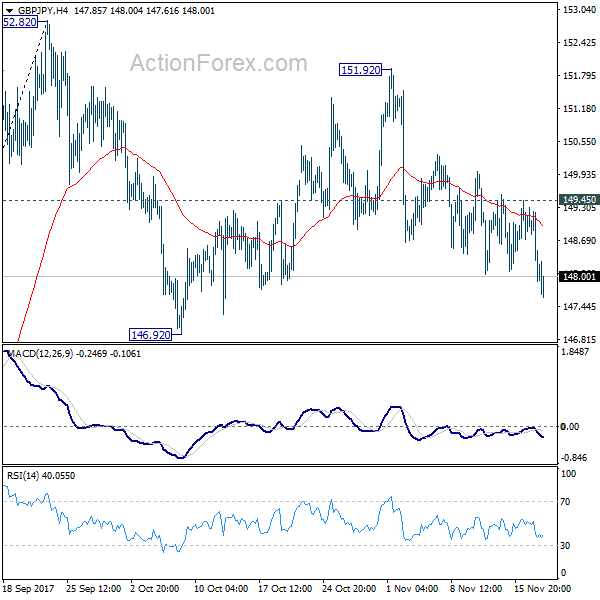

GBP/JPY Daily Outlook

Daily Pivots: (S1) 147.54; (P) 148.42; (R1) 148.92; More...

Intraday bias in GBP/JPY remains on the downside for 146.92 support and below. Price actions from 152.82 are viewed as a corrective pattern. We'd expect strong support from 61.8% retracement of 139.29 to 152.82 at 144.45 to contain downside and bring rebound. On the upside, break of 149.45 minor resistance will turn bias back to the upside for 151.92/152.82 resistance zone.

In the bigger picture, medium term rebound from 122.36 is still expected to resume after corrective pull back from 152.82 completes. Firm break of 38.2% retracement of 196.85 to 122.36 at 150.43 will carry long term bullish implications. In that case, GBP/JPY could target 61.8% retracement at 167.78. However, break of 139.29 will indicate rejection from 150.43 key fibonacci level. And the three wave corrective structure of rebound from 122.36 will argue that larger down trend is resuming for a new low below 122.26.

Market Update – Asian Session: Germany Govt Weakness And Continued Uncertainty On US Tax Reform

Headlines/Economic Data

Japan

Weakness in the financial sector: Mega banks decline; Topix Securities brokers index -1%

(JP) Japan's government may seek to cut corporate tax rate to ~25% vs ~30% currently for companies that increase wages by 3% and make capital expenditures – Japanese Press

(JP) Japan PM Abe: Reiterates desirable for BoJ to continue 'super easy' policy, Japan no longer in deflation and excessive Yen strength has been corrected

Drug companies, Shionogi and Chugai, decline: Japan's Health Ministry released its reform plan which seeks to gradually lower prices for off-patent drugs.

Steel makers trade generally higher: Tokyo Steel to raise steel prices amid strong demand and higher raw materials costs.

Japan exports rise for 11th straight month in Oct: JAPAN OCT TRADE BALANCE: ¥285.4B V ¥330.0BE; ADJ ¥322.9B V ¥206.7BE; Exports y/y: 14.0% v 15.7%e; Exports to China +26% y/y, EU +15.8% y/y, US +7.1%; Asia +18.9%

Korea

Kospi opened +0.1%; Market has since reversed gains

Weakness in Chip Sector: Samsung -0.6%, Hynix -0.6%

Korean Won declines by over 0.4% (first drop in 4 sessions)

South Korea Q3 average daily FX transaction volume $51.6B (highest since Q1 2016) v $50.8B q/q – Bank of Korea

South Korea sold 20-yr bonds at 2.56%

SOUTH KOREA OCT PPI M/M: 0.0% V 0.5% PRIOR; Y/Y: 3.5% V 3.8% PRIOR

Politics: South Korea and China foreign ministers to hold meeting this week - Korean press

South Korea President Moon approval rating rises after Southeast Asia trip

(KR) Bank of Korea (BOK) sells KRW400B in 6-month monetary stabilization bonds at 1.68%

China/Hong Kong

Equity markets are currently lower as of the time of writing. Volatility seen in small cap Chinext index.

Hang Seng Materials Index -0.8%; Hang Seng Energy Index -0.8%, Hang Seng Utilities Index -0.7%, Hang Seng Information Technology Index % (Tencent +1%)

Hypermart company Sun Art Retail Group declines by over 8% after reChinext indexceived HK$62.0B bid from Alibaba unit's which valued company at discount to prior close

On Friday, the PBoC said that it would ban financial companies from the capital pool business. As part of the rules, ‘highly indebted' companies will not be allowed to invest in asset management products.

China will more quickly establish a regulatory framework for financial holding companies, according to the PBoC's Quarterly Monetary Policy Report.

(CN) CHINA OCT PROPERTY PRICES M/M: RISES IN 50 OUT OF 70 CITIES V 44 PRIOR; Y/Y RISE IN 60 CITIES OUT OF 70 CITIES V 67 PRIOR

(CN) China PBOC Q3 monetary policy implementation report: Will maintain a prudent and neutral monetary policy and keep liquidity conditions stable, to fend off systemic risks

6808.HK Alibaba forms strategic alliance with Auchan Retail and Ruentex Group to acquire 36.16% stake in Sun Art for HK$22.4B

(CN) PBoC OMO: Injects CNY100B v CNY30B injected in 7,14 and 63-day reverse repos prior; Net injects CNY20B v CNY10B drain prior

USD/CNY (CN) PBoC sets yuan reference rate at 6.6271 v 6.6277 prior

Australia/New Zealand

ASX Consumer Discretionary Index -0.5% Financials Index -0.4%; Energy Index +0.5%

(AU) Australia Liberal National Party Senator Barry O'Sullivan drafting a bill for a parliamentary commission of inquiry into the nation's banking sector, covering superannuation, insurance, banks, financial services, protections for small business and the rural sector

(AU) Reserve Bank of Australia (RBA) head of financial stability Kearns: Australia banks have tightened lending conditions for commercial property in recent years

(AU) IMF Article IV Mission Statement: Low wage growth to weigh on Australia household incomes; economic growth pickup likely to be modest; RBA may keep rates on hold for another year

NetWealth Group (investment management firm) rises over 35% in share debut

(NZ) New Zealand Oct food prices m/m: -1.1% v -0.2% prior

(AU) Australia buys back A$400M in March 2019 and Oct 2019 Bonds, bid-to-cover 2.71x

(AU) Australia sells A$400M v A$400M indicated in 3.25% April 2029 Bonds, avg yield 2.6437%, bid to cover 4.98x

MRM.AU Placement raises $22.4M, institutional component of rights offer raises further A$15.7M at A$0.20/shr; +22%

PMP.AU CEO Peter George to retire and Kevin Slaven to be interim CEO; Cuts FY18 adj EBITDA A$50-55M (prior 70-75M); -31%

RBA in focus for Tuesday's session: Reserve Bank of Australia to release Nov Meeting Minutes and Gov Lowe to comment on ‘Evolving Themes' in annual year-end speech before economists

Other Asia

(TH) Thailand Q3 GDP q/q: 1.0% v 0.6%e; y/y: 4.3% v 3.9%e (fastest pace since 2013); Thai Baht (THB) -0.1%

(TH) Thailand Central Bank Porametee comments following release of Q3 GDP data: No need to rush into hike in key interest rate; reiterates monetary and fiscal policies to stay accommodative

Malaysia Central Bank (Bank Negara): Intervention is not to manage MYR level; Offshore ringgit trading is illegal; Short selling framework being extended to Islamic govt bonds; To introduce interbank bills in MYR and foreign currency.

North America

(US) According to Committee for a Responsible Federal Budget tax bill will cost $2.2T instead of the $1.41T indicated if all temp changes in the bill were made permanent - US financial press

M&A: Semiconductor processor company Cavium said to receive ~$6.0B or at least $80/share offer from Marvell Technology (at least ~5.5% premium)

Politics: US Special Prosecutor Mueller said to send request for documents to DoJ related to Russia probe , according to US media report: The directive was issued within the past month and the action is the first request for records that Mueller has made of the DoJ, says the report.

Tax Reform: US Senator Susan Collins (ME-R) said does not believe the repeal of Obamacare's individual mandate should be part of the tax bill.

OMB Director Mulvaney said President Trump would agreement to removing the repeal of Obamacare mandate from the Senate tax bill if it becomes an impediment to passage

The health care mandate is not a ‘bargaining chip' in the Senate tax bill, said US Treasury Sec Mnuchin.

Mexican Peso and Canadian dollar open the week lower: Mexico is thought to see US idea on NAFTA auto agreement as ‘unworkable'

Europe

(DE) Germany Free Democrats Party said to be breaking off coalition talks with Merkel; Merkel could avoid a snap election if she convinces reluctant Social Dems to enter coalition - German Press; EUR/USD fell 0.6% to 1.1722 on the report

(DE) German Chancellor Merkel: no stone left unturned to form 4-party coalition; regrets no common solution for parties - speaking to reporters

(UK) UK Fin Min Hammond: we are on the brink of serious progress in Brexit talks; UK to make proposals to EU in time for the December council meeting - BBC interview

Dutch telcom Altice SA says not preparing equity raise

Levels as of 00:00ET

Nikkei -0.5%, Hang Seng -0.3%; Shanghai Composite -0.8%; ASX200 -0.2%, Kospi -0.1%

Equity Futures: S&P500 -0.2%; Nasdaq100 -0.2%, Dax -0.4%; FTSE100 -0.1%

EUR 1.1797-1.1723; JPY 112.20-111.89; AUD 0.7571-0.7550;NZD 0.6819-0.6794

Dec Gold -0.3% at $1,292/oz; Dec Crude Oil -0.2% at $56.62/brl; Dec Copper -0.4% at $3.06/lb

EURUSD – Closes Higher But With Caution Of Pullback

EURUSD - The pair may be biased to the upside but could face pullback risk in the new week. Resistance comes in at 1.1800 level with a cut through here opening the door for more upside towards the 1.1850 level. Further up, resistance lies at the 1.1900 level where a break will expose the 1.1950 level. Conversely, support lies at the 1.1700 level where a violation will aim at the 1.1650 level. A break of here will aim at the 1.1600 level. Below here will open the door for more weakness towards the 1.1550. All in all, EURUSD faces further corrective recovery threats.

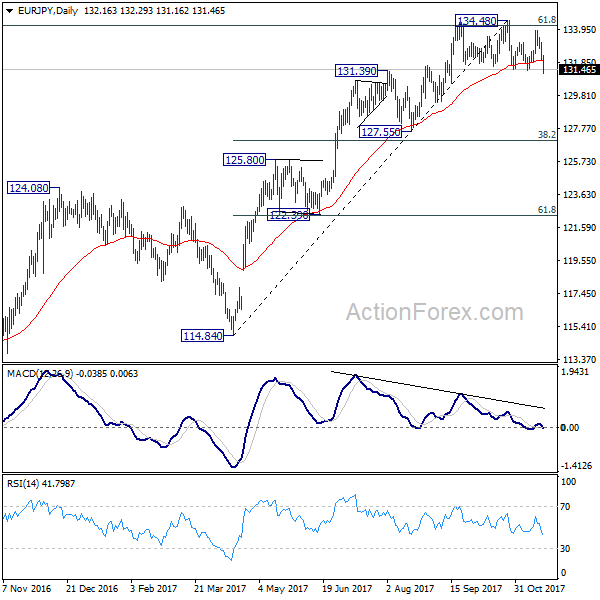

EUR/JPY Daily Outlook

Daily Pivots: (S1) 131.74; (P) 132.45; (R1) 132.85; More....

EUR/JPY fall's sharply today and breaches 131.38 support. The development argues that a head and should top pattern is completed (ls: 134.39; h: 134.48; rs: 133.85). That indicates near term reversal after rejection from 134.20 long term fibonacci level. Intraday bias is now on the downside for 38.2% retracement of 114.84 to 134.48 at 126.97, which is close to 127.55 support. We'll look for support from there to bring rebound on first attempt. On the upside, above 132.30 will dampen this bearish case and turn bias back to the upside for 133.85 instead.

In the bigger picture, medium term rise from 109.03 (2016 low) is seen as at the same degree as the down trend from 149.76 (2014 high) to 109.03 (2016 low). 61.8% retracement of 149.76 to 109.03 at 134.20 is already met. Sustained break there will pave the way to key long term resistance zone at 141.04/149.76. However, break of 127.55 support will argue that the medium term trend has reversed and will turn outlook bearish for deeper fall back to 114.84/124.08 support zone at least.

Euro Dives as German Merkel Failed to Form Coalition

Euro dives broadly after Germany Chancellor Angel Merkel declared failure in forming a coalition government. After over time exploratory talks, Merkel's Christian Democratic-led bloc couldn't reach an agreement with pro-business Free Democratic Party and center-left Greens. Merkel will now meet with President Frank-Walter Steinmeier next. The meeting with Steinmeier suggests that Merkel will not opt for forming a minority government with the Greens. And the reincarnation of the grand coalition with SPD is unlikely too. Instead, Merkel may ask Steinmeier to order another election. In the meantime, she will stay as the "caretaker" chancellor. And for the time being, Germany will hold of any work with France on Euro reforms until the domestic political picture comes clear.

Chancellor Hammond: UK ready to offer Brexit bill before Dec summit

Chancellor of Exchequer Philip Hammond indicated that UK could be ready to break the negotiation "logjam" with EU and make a divorce bill offer before December summit. Hammond said on BBC that UK is "on the brink of making some serious movement forward". And, "we will make our proposals to the European Union in time for the council. I am sure about that." Meanwhile he also insisted that "It's not about demands, it's about what is properly due from the U.K. to the European Union under international law in accordance with European treaties." He added that "we've always been clear it won't be easy to work out that number. But whatever is due, we will pay."

Goldman Sachs predicts four Fed hikes in 2018

It's widely expected that Fed will raise interest rate in December by 25bps to 1.25-1.50%. And according to Fed's own projections and comments from some hawks, Fed would hike three more times in 2018. But accord to a note by Goldman Sachs economist, Fed would indeed hike four times. The note said that "the US economy heads into 2018 with strong growth momentum and an unemployment rate already below levels that Fed officials view as sustainable.: And, "the strength is becoming 'too much of a good thing' and containing further overheating will become a more urgent priority in 2018 and beyond."

White House softens stance on Obamacare individual mandate repeal

It's clear that with 52-58 advantages over the Democrats in Senate, the Republicans can only afford two "no" votes for the tax bill. Ron Johnson has already declared opposition last week. And Susan Collins is a great uncertainty as she said "I haven't reached that conclusion yet" during the weekend. There are many areas that Collins, as a centrist, is not satisfied with the Senate Republican tax bill. But a key stick point is the inclusion of the provision to remove the individual mandate of the Obamacare. She criticized that "The fact is that if you do pull this piece of the Affordable Care Act out, for some middle-income families, the increased premium is going to cancel out the tax cut that they would get."

But the White House has also softened their stance on this issue. Office of Management and Budget Director Mick Mulvaney said that "If it becomes an impediment to getting the best tax bill we can, then we are okay with taking it out." And, it's ultimately up to House and Senate Republicans to figure out what to do. The Senate will take their bill to floor after lawmakers return from Thanksgiving.

In the calendar

On the data front, Japan trade surplus widened to JPY 0.32T in October. German PPI and US leading indicator will be featured later in the day. Looking ahead, the calendar is relatively light with US on Thanksgiving holiday. FOMC minutes and ECB accounts will be the main feature. meanwhile, focuses will also be on Eurozone PMIs ad German Ifo. Here are some highlights for the week:

- Monday: Japan trade balance; German PPI; US leading indicator

- Tuesday: RBA minutes; Japan all industry index; Swiss trade balance; UK public sector net borrowing; Canada wholesale sales; US existing home sales

- Wednesday: US jobless claims, durable goods orders; FOMC minutes; Eurozone consumer confidence

- Thursday: New Zealand retail sales; German GDP final; Eurozone PMIs, ECB monetary policy accounts; UK GDP revision ; Canada retail sales

- Friday: Japan PMI manufacturing; German IFO; US PMIs

EUR/JPY Daily Outlook

Daily Pivots: (S1) 131.74; (P) 132.45; (R1) 132.85; More....

EUR/JPY fall's sharply today and breaches 131.38 support. The development argues that a head and should top pattern is completed (ls: 134.39; h: 134.48; rs: 133.85). That indicates near term reversal after rejection from 134.20 long term fibonacci level. Intraday bias is now on the downside for 38.2% retracement of 114.84 to 134.48 at 126.97, which is close to 127.55 support. We'll look for support from there to bring rebound on first attempt. On the upside, above 132.30 will dampen this bearish case and turn bias back to the upside for 133.85 instead.

In the bigger picture, medium term rise from 109.03 (2016 low) is seen as at the same degree as the down trend from 149.76 (2014 high) to 109.03 (2016 low). 61.8% retracement of 149.76 to 109.03 at 134.20 is already met. Sustained break there will pave the way to key long term resistance zone at 141.04/149.76. However, break of 127.55 support will argue that the medium term trend has reversed and will turn outlook bearish for deeper fall back to 114.84/124.08 support zone at least.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Trade Balance (JPY) Oct | 0.32T | 0.21T | 0.24T | 0.27T |

| 7:00 | EUR | German PPI M/M Oct | 0.30% | 0.30% | ||

| 7:00 | EUR | German PPI Y/Y Oct | 2.70% | 3.10% | ||

| 15:00 | USD | Leading Index Oct | 0.60% | -0.20% |

Market Morning Briefing: The Aussie Has Immediate Support Near 0.75

STOCKS

Almost all the major equity indices are trading weak along with the Asia Pac indices except Nifty.

Dow (23358.24, -0.43%) still has scope of testing 23600 on the upside while above 23200 levels. But in case the index breaks below 23200, a test of 23000 is possible before again resuming the uptrend.

Dax (12993.73, -0.41%) was unable to move above 13100 in spite of seeing a sharp rise from levels near 12800. A re-test of 12900-12800 looks possible before again resuming to bounce back towards 13100 and higher in the medium term.

The strength in Nikkei (22271.35, -0.56%) seems to have slowed down a bit now and we could see a fall towards 22000 again in the next couple of sessions. Near term looks weak.

Shanghai (3357.11, -0.76%) could bounce back from support near 3370-3360 and move back towards 3400-3420 this week.

Nifty (10283.60, +0.67%) is trading in the middle of the broad 10100-10400 region and could move towards either side this week. A test of 10400 first followed by a sharp fall towards 10100 is preferred but in case the index starts falling from current levels, it could initially come off towards 10200-10100 before again bouncing back.

COMMODITIES

Gold (1291.37) is trading higher but could be stuck in the 1270-1300 region for a few more days before moving above 1300 to test higher levels of 132/25. Immediate daily resistance is seen near 1300-1305 which is likely to hold just now.

Brent (62.56) may move up towards 64-65 while above 61 (decent support). WTI (56.76) has also bounced well as expected and could target higher levels of 58-59 which is a longer term resistance. Near term looks bullish.

Copper (3.0505) may face some rejection near 3.10 and could come off towards 3.00-2.95 as we have been mentioning since the past few editions. Near term looks bearish.

FOREX

Dollar Index (93.99) has immediate support near 93.40 and while that holds, a rise back to 94.50 is expected.

EURO (1.1736) almost tested levels near 1.19 as expected last week before facing rejection near 1.1860. The price could come off to 1.1700-1.1650 levels in the near term.

Dollar-Yen (112.006) looks weak just now. Although immediate support is visible near 111.60/50, in case the bears turn out to be stronger, we may expect a test of 111 on the downside.

The Pound (1.3198) has decent chances of moving towards 1.33 in the near term. View is bullish.

The Aussie (0.7555) has immediate support near 0.75 on the weekly candles and that could produce a medium term bounce leading it to a rise towards 0.76-0.77 in the coming sessions. Near term looks bullish while above 0.75.

Dollar-Rupee (65.03) is likely to move up towards 65.10/20 with a possible test of 64.90 on the downside.

INTEREST RATES

The US-Japan 10Yr (2.28%) is likely to come down towards 2.25/20% in the near term and if that happens it could well pull down Nikkei and dollar Yen along with itself. Near term looks bearish for all the three.

The US yields are all heading towards near term channel supports which if holds, could produce a decent bounce in the near term. The 5Yr (2.04%), 10YR (2.33%) and the 30YR (2.76%) are trading just above support levels and look bullish for the coming sessions.

The Japan 5YR (-0.12%) and the 10YR (0.04%) are looking weak and could come off towards -0.14% and 0.024% respectively in the near term.