Sample Category Title

Currencies: EUR Declines On Political Uncertainty In Germany

Sunrise Market Commentary

- Rates: German politics and risk sentiment in focus

The failed German coalition talks are a short term positive for Bunds. Risk sentiment on stock markets will probably remain key for core bond trading. The German Dax is still in the “danger zone” between 12 900 and 13 000. Losing this technical area would suggest a more pronounced downward correction. The eco calendar is uneventful today. - Currencies: EUR declines on political uncertainty in Germany

Last week, the euro was more resilient than the dollar to global uncertainty. This morning, the euro suffered a setback as the German government negotiations collapsed. The jury is still out whether this will have a lasting impact on FX trading. Short-term, we assume that the topside in the euro has become better protected

The Sunrise Headlines

- US stock markets ended the week on a weaker note, closing up to 0.4% lower. Asian bourses cede ground overnight as well with China underperforming (-1%) as the PBOC tightened asset management rules.

- The protracted struggle to form a new German government under the leadership of Angela Merkel collapsed, plunging Europe's biggest economy into political uncertainty and raising the prospect of new elections.

- UK PM May is expected to get the green light from ministers today to increase her Brexit “divorce bill” offer, narrowing the gap with the EU's €60bn estimate in a bid to break the deadlock in talks with Brussels.

- China's central bank issued sweeping guidelines to tighten rules on asset management business, the latest step by Beijing to fend off systemic risks in the country's rampantly growing shadow banking sector.

- Special Counsel Mueller's team investigating whether President Trump sought to obstruct a federal inquiry into connections between his presidential campaign and Russian operatives has now directed the Justice Department to turn over a broad array of documents, ABC News has learned.

- Republican hopes to pass a tax bill may hinge on whether to repeal the Obamacare rule that requires people to buy health insurance. Senator Collins said that would be "a problem," a sign that changes will be needed.

- Today's eco calendar is extremely thin with only central bank speeches from ECB Nowotny, Lautenschlaeger, Draghi and Constancio

Currencies: EUR Declines On Political Uncertainty In Germany

German political crisis to weigh on the euro?

On Friday, sentiment on risk remained fragile and the dollar struggled to prevent further losses. Diffuse news from the progress on the US tax bill and from the investigation into the Russia links of the Trump campaign kept investors in a waitand- see modus. Strong US housing data couldn't provide a lasting support for the US currency either. EUR/USD held near the 1.18 level for most of the session and closed the day at 1.1790. USD/JPY experienced stronger headwinds and tested the 112 area. (close at 112.10).

Overnight, risk sentiment in Asia remains negative. Most regional indices are trading down. China underperforms as the Chinese regulator proposed new measure to curb risk in some parts of the financial sector. Japanese trade data were strong, but close to expectations and had no big impact. The collapse of the German coalition talks filters through into market sentiment. EUR/USD dropped from the 1.18 area and trades currently in the 1.1740 area. For now, USD/JPY suffers no further losses. The pair holds in the 112 area.

Today, the eco calendar is thin, except for the US leading indicators, no market mover. Several ECB members including Nowotny, Lautenschlaeger (hawks), Draghi and vice-president Constancio (doves), will speak at different occasions. The views of all speakers are well-known. Further out this week, the eco calendar remains thin and dominated by the US Thanksgiving holiday on Thursday and Black Friday. The US durables and the Minutes of the last FOMC meeting on Wednesday are the sole releases of interest. In EMU, the calendar is somewhat more interesting with the preliminary PMI's for November and the ECB Minutes of the last policy meeting on Thursday and the German IFO on Friday.

Asian markets opened with a risk-off bias this morning. European investors will ponder the potential impact from the collapse of the German government negotiations. Last week, the dollar was more sensitive to global risk aversion than the euro. Given the developments in Germany, the balance between the euro and dollar might turn more neutral or even tilt to the disadvantage of the euro. In this respect, we keep a close eye on the price action in the EUR/JPY cross rate. The pair is currently testing the key 131.40 support. A sustained break of this support area, combined with a more protracted risk-off sentiment might weigh on EUR/USD and, to a lesser extent on USD/JPY. We start the week with cautiously negative bias on the euro.

From a technical point of view, EUR/USD set a new post-ECB low two weeks ago, but the move petered out. EUR/USD last week regained intermediate resistance at 1.1690/1.1837, but the 1.1880 MT correction top was left intact. A break above the latter would suggest a full retracement to the 1.2092 correction top. We don't preposition for such a scenario unless real negative news from the US pops up. On the downside, the 1.1554 reaction low remains the first important reference, but it is still far away. A further downside correction within the 1.1554/1.1880 range is favoured. The USD/JPY's momentum was positive in October, but deteriorated this month. The pair tested the 114.49 MT range top, but the attempt failed. Recent price action was unconvincing despite a solid US interest rate support. Last week's drop below the 112.96 support reinforces the downside pressure. 111.65 is the next key support. A break would turn the picture outright USD negative.

EUR/USD: Will uncertainty on Germany break the euro positive momentum ?

EUR/GBP

EUR/GBP: topside test again rejected

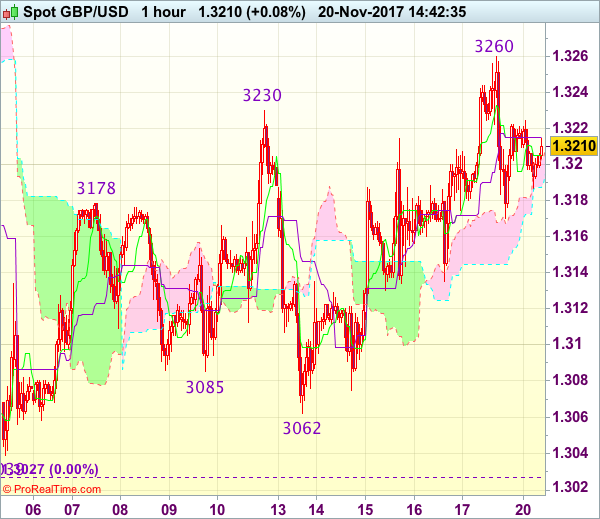

Earlier last week, markets saw rising chances of a potential positive development in the Brexit negotiations. On Friday, sentiment was less constructive as UK Brexit Minister Davis indicated that it was now up to the EU to do concessions. The news flow from the Gothenburg EU meeting /summit also didn't suggest that big Brexit progress could be in the making. PM May and EU's Tusk finally came to an obvious conclusion: There is more work to be done! EUR/GBP jumped back north from the low 0.89 area to the 0.8960 area late in the morning session. The pair closed the session at 0.8923. Cable dropped from the 1.3250/60 area to the 1.3170 are, but rebound later in the session. The pair closed the session at 1.3215 and holds the established sideways consolidation pattern.

There are no important eco data in the UK today. BoE deputy governor Dave Ramsden speaks at King's College in London. However, we don't expect BoE talk to change the outlook for the sterling going forward. EUR/GBP declined on the negative headlines from Germany overnight. At the same time, there are press rumours that the UK is considering to raise the amount it is prepared to pay for the Brexit divorce. ST, these developments might be positive for sterling and negative for the euro. In a longer term perspective , a political stalemate in Germany probably also won't make the Brexit process easier. However, in a day-to-day perspective, euro softness due to the uncertainty on Germany will probably prevail as a driver for EUR/GBP trading.

MT technical: Recently, the BoE driven sterling rebound ran into resistance and sterling declined again as markets anticipated that any rate cycle would be very gradual and limited. EUR/GBP trades in a 0.8733/0.9033 consolidation range. Last week, the EUR/GBP rebound ran into resistance just ahead of the 0.9033 range top. We changed our ST bias on EUR/GBP from positive to neutral last week. The 0.9015/33 area might be tough to break short-term.

EUR/GBP: topside test rejected. Room for a further technical rebound of sterling?

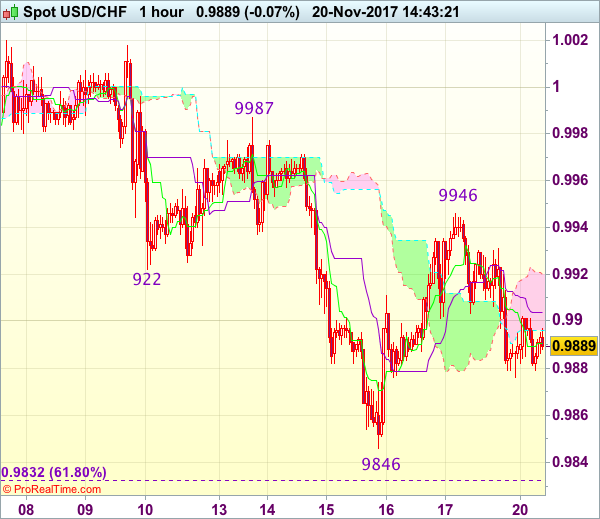

Trade Idea : USD/CHF – Hold short entered at 0.9935

USD/CHF - 0.9893

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9890

Kijun-Sen level : 0.9904

Ichimoku cloud top : 0.9920

Ichimoku cloud bottom : 0.9896

Original strategy :

Sold at 0.9935, Target: 0.9835, Stop: 0.9950

Position : - Short at 0.9935

Target : - 0.9835

Stop : - 0.9950

New strategy :

Hold short entered at 0.9935, Target: 0.9835, Stop: 0.9950

Position : - Short at 0.9935

Target : - 0.9835

Stop : - 0.9950

Although the greenback rebounded after falling to 0.9846 last week, as 0.9946 has capped dollar’s upside and the pair has retreated, retaining our bearishness, hence consolidation with downside bias remains for weakness to 0.9860-70 but break there is needed do signal the rebound from 0.9846 has ended, bring retest of this level first. Once this level is penetrated, this would signal the erratic decline from 1.0038 top has resumed for at least a retracement of early upmove to previous resistance at 0.9837, break below there would encourage for subsequent decline towards 0.9795-00.

In view of this, we are holding on to our short position entered at 0.9935. Above said resistance at 0.9946) would defer and risk test of 0.9970-75 but price should alter below resistance at 0.9987, bring another decline later.

Forex: Draghi: ‘Eurozone Economy Is Robust But…’

Speaking at the Frankfurt European Banking Congress, ECB President Mario Draghi, commented that 'although the eurozone economy was robust' recovery was still heavily reliant on stimulus from the European Central Bank. He stated that positive economic growth alone was not enough to allow the ECB to increase the pace of monetary policy normalization. The current lackluster inflation growth is causing withdrawal of stimulus to be slow. He commented that 'Despite this progress on the real side of the economy, from a monetary policy perspective our task is not complete, as we have not yet seen a sustained adjustment in the path of inflation'.

On Friday, data from the US Census Bureau showed that the rate of new home construction in the US rose sharply in October. New Housing Starts rose a healthy 13.7% in October (from September), as the negative impacts of the summer hurricanes appear to have been overcome. The annualized rate climbed to 1.29 million, beating forecasts of 1.19 million. The increase ended 3 consecutive monthly declines. The more forward-looking dataset of New Home Permits rose 5.9% to a rate of 1.3 million, indicating that the housing industry is growing at a healthy pace as the US economy is strengthening.

Statistics Canada released data on Friday showing the consumer price index was up 1.4% in October compared with a year ago, following a 1.6% increase in September. The Bank of Canada, which uses a 2% inflation target in setting monetary policy, raised its key interest rate target twice this year following strong economic growth to start the year. The markets expect growth for H2 to come in at a slower pace and the BoC has suggested that while further rate hikes are likely, they will be cautious and pay close attention to the incoming economic data. The markets do not expect a rate hike until the end of Q1 next year at the earliest.

Officials from the US, Canada and Mexico have been meeting in Mexico City for the 5th of 7 planned rounds to update the North American Free Trade Agreement (NAFTA), from which President Donald Trump has threatened to withdraw. The US Administration has, apparently, made demands that other members have deemed unacceptable. With negotiations ongoing, it appears that all sides are far from agreement, which is likely to cause, in particular, volatility in MXN as Mexico appears to be the largest economic loser if the US does indeed withdraw.

EURUSD is 0.5% lower in early Monday trading at around 1.1730.

USDJPY is little changed from Friday's close, currently trading around 112.05.

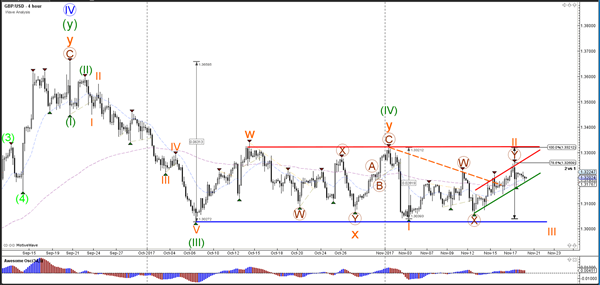

GBPUSD is 0.1% lower in early session trading at around 1.3200.

USDMXN is 0.14% higher, currently trading around 18.9350.

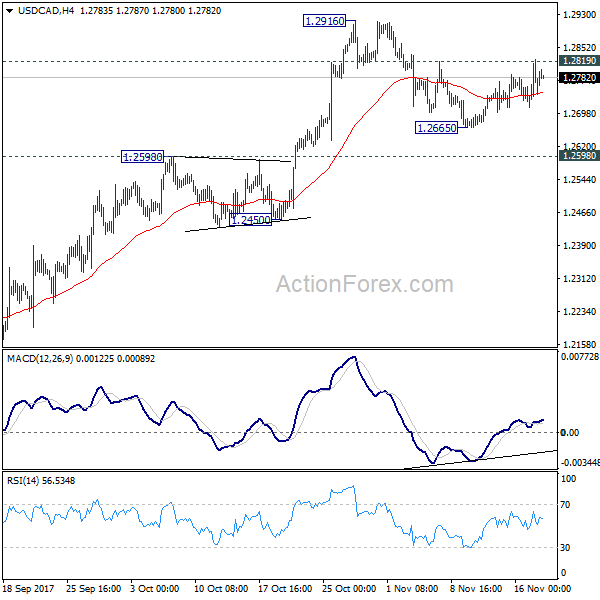

USDCAD is 0.2% higher in early Monday trading at around 1.2790.

Gold is 0.16% lower, currently trading around $1,291.75.

WTI is little changed in early trading at around $56.77.

Major data releases for today:

At 18:00 GMT, ECB President, Mario Draghi, is scheduled to provide an introductory statement at the ECON Hearing of the European Parliament in Brussels, Belgium.

Trade Idea : GBP/USD – Hold long entered at 1.3180

GBP/USD - 1.3225

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.3216

Kijun-Sen level : 1.3215

Ichimoku cloud top : 1.3203

Ichimoku cloud bottom : 1.3189

Original strategy :

Bought at 1.3180, Target: 1.3280, Stop: 1.3145

Position : - Long at 1.3180

Target : - 1.3280

Stop : - 1.3145

New strategy :

Hold long entered at 1.3180, Target: 1.3280, Stop: 1.3170

Position : - Long at 1.3180

Target : - 1.3280

Stop : - 1.3170

Although the British pound retreated after rising to 1.3260 late last week, as 1.3170 has contained downside, retaining our bullishness for recent erratic rise from 1.3039 to bring retest of said resistance, break there would extend headway to 1.3280-90, however, as broad outlook remains consolidative, reckon upside would be limited and another previous resistance at 1.3321 should remain intact, bring retreat later.

In view of this, we are holding on to our long position entered at 1.3180. Below said support at 1.3170 would abort and risk correction to 1.3150 but only break of said support at 1.3134 would signal top has been formed instead, bring weakness to 1.3100, then towards support at 1.3062.

Trade Idea : EUR/USD – Buy at 1.1700

EUR/USD - 1.1749

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.1746

Kijun-Sen level : 1.1768

Ichimoku cloud top : 1.1809

Ichimoku cloud bottom : 1.1792

Original strategy :

Bought at 1.1790, stopped at 1.1755

Position : - Long at 1.1790

Target : -

Stop : - 1.1755

New strategy :

Buy at 1.1700, Target: 1.1800, Stop: 1.1665

Position : -

Target : -

Stop : -

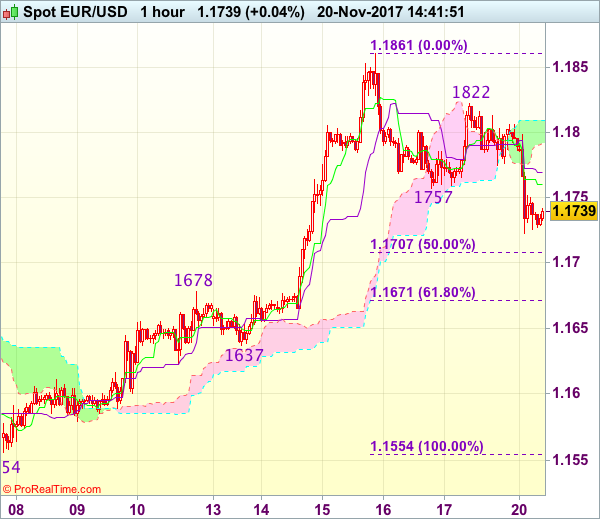

Although the single currency has dropped again after meeting renewed selling interest at 1.1822 and near term downside risk remains for the fall from 1.1861 (last week’s high) to bring retracement of recent upmove to 1.1700-10 (50% Fibonacci retracement of 1.1554-1.1861), however, still reckon 1.1671-78 (61.8% Fibonacci retracement and previous resistance) would contain downside and bring another rise later, above 1.1770-75 would bring rebound to 1.1800 but only break of said resistance at 1.1822 would retain bullishness and signal the fall from 1.1861 top has ended, bring retest of this level later.

In view of this, we are looking to buy euro on next decline. Only below 1.1671-78 would defer and signal top has been formed instead, bring a stronger retracement of recent rise to 1.1650, then test of previous support at 1.1637 which is likely to hold from here.

US Travel Note Tax Cuts Are Coming But Will Be Watered Down

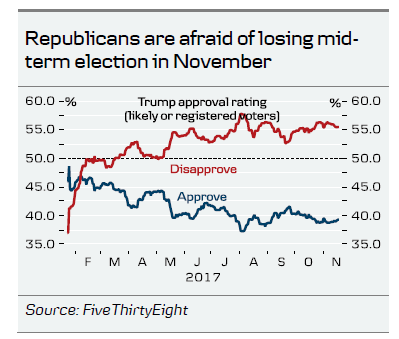

- Most economists think the US expansion is going to continue in coming years with growth above potential and see few risks near term.

- Most expect the Republicans to deliver a deficit-financed tax cut (most realistically in Q1 18), as they are afraid of the mid-term election in November next year. However, the final version is likely to be watered down (in terms of how big cuts they can make), as there is opposition to the tax revenue raises (like removing tax deductions). Growth impact is expected to be small both in the short and long run so it should not mean a lot in terms of Fed policy. This also limits how much it should push up US yields.

- Economists – including at the rating agencies – do not seem to be concerned about increasing public debt despite US public finances being unsustainable to begin with already under current law. One reason is that interest payments in percent of GDP are low due to low rates.

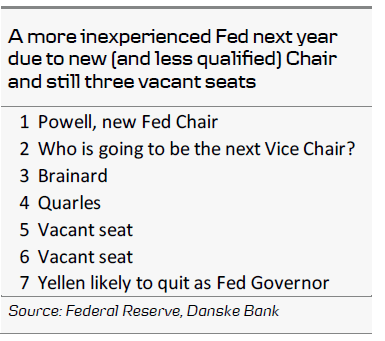

- Jerome Powell was the safe choice for the next Fed Chair and will continue the current monetary policy strategy but will rely more heavily on staff compared to Yellen or Bernanke. Do not expect any controversial nominations for the vacant Fed seats.

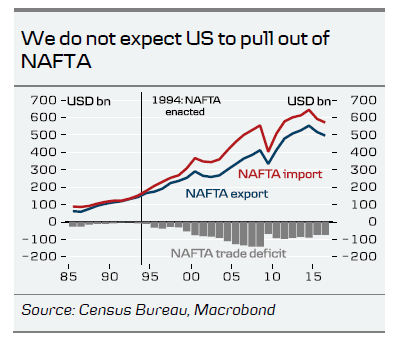

- Low probability of a trade war with China. NAFTA is a ‘joker' (not least with elections in Mexico next year), which may disrupt US supply chains but analysts expect the US to remain in NAFTA.

Expansion set to continue in coming years

The consensus view is that the US expansion is set to continue in coming years with growth above 2% (potential growth is 1.75-2.00%, according to consensus). Confidence is high among consumers and businesses, suggesting growth will be driven more balanced between private consumption and business investment, as the oil sector has rebounded after the downturn due to sharp oil price drop. The oil sector has become more important for the rest of the economy, as shale oil production requires more input from the rest of the industrial sector than traditional oil production. Economists in general do not think there are many risk factors out there at the moment but mentioned the Chinese debt situation, increasing US rates and NAFTA (North American Free Trade Agreement) as three potential risks. US economists are also still worried about the political situation in Europe, with both the Catalonian crisis and Italy mentioned.

In terms of the Fed, most expect two to three hikes next year (in line with our view), as inflation rebounds and Powell is not expected to change the current monetary policy strategy. That said, we met a few suggesting the Fed could hike four to five times, as they expect higher-than-consensus wage growth and inflation. Others were sceptical to this view, as they think markets are not prepared for so many hikes and it could lead to a stronger USD, which would slow growth and inflation.

Tax cuts are on their way

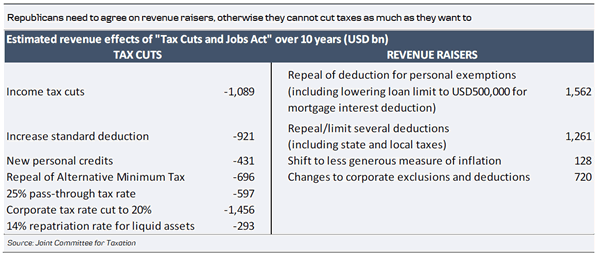

Most people we spoke with expect the Republicans to deliver tax cuts. The main reason is that the Republicans are afraid of the mid-term election in November next year. The Republican hypothesis is that they will lose badly if they are unable to deliver at least one major legislative result. This has only become more important for the Republicans after they suffered big losses in the recent elections in New Jersey and Virginia. This also helps to explain why Republican fiscal hawks have accepted a budget resolution making room for deficit-financed tax cuts of USD1,500bn over 10 years (equivalent to 0.9% of nominal GDP per year). That said, it is not a given that tax cuts will actually increase support for the Republicans, as corporate tax cuts are not especially popular among the Americans.

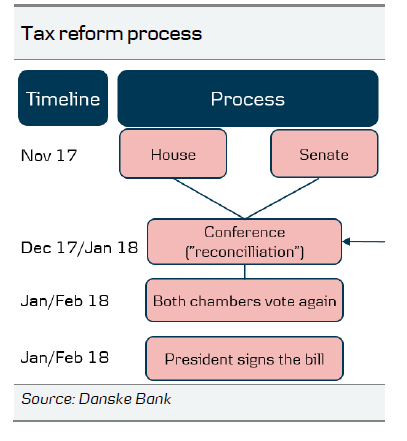

Tax reform has become more likely but is definitely not certain and there is still a risk that the whole thing could backfire, as was the case with Obamacare. I think this is also the reason why analysts have different views on where we might end up. The consensus view is that it will be a watered down version of what is currently on the table, not least given that there is some heavy lobbying against some of the revenue raisers such as a deduction for state and local taxes, a deduction for property taxes and so on. Without tax revenue raisers, Republicans cannot make big corporate tax cuts as they are very expensive (by itself a corporate tax rate cut to 20% costs USD1,500bn over ten years). Remember that the Republican can only afford to lose two votes in the Senate and 22 in the House. Given that the rules to avoid filibusters in the Senate are stricter than in the House and given that the Republicans can only afford to lose two votes in the Senate, the final deal likely looks to be more like the Senate tax bill than the House tax bill (remember, the House also had to give in on the budget). The most important people to follow in the Senate are McCain, Flake, Corker and Collins (Trump has had conflicts with most of them).

Based on our discussions with political analysts, we expect the Republicans to deliver tax cuts in the beginning of next year, as we believe the negotiations between the House and the Senate are going to be very complicated. We expect the final version to be a watered down versions, as they cannot agree on financing all the elements they want to include (but still using the whole USD1,500bn tax cut window). Comparing the House and Senate tax bills, it seems like the Republicans are prioritising corporate tax cuts over income tax cuts.

Do not expect a big boost to growth from tax reforms

Most economists do not expect a big economic boost from tax reform although it is slightly positive. The reason is two-fold: (1) income tax cuts target mainly high income earners (also as low income earners already pay little or no tax), who generally have a low, marginal propensity to consume and (2) investments may not increase significantly despite the possibility of deducting investment costs, as credit has been cheap in recent years. Overall, tax reform is more likely to boost investment than consumption. This also means that the Fed is unlikely to hike much faster next year on the back of this. The Republicans’ hope that tax reform will increase potential growth from 2% to 3% was described as ‘fantasy’. We agree that it would not have a big impact on potential growth (which is pulled down by demographics and low productivity growth) and hence it should not increase the natural rate of interest significantly, thus limiting the impact of tax reform in the longer end of the US yield curve.

Besides corporate tax cuts, tax reform will most likely include a one-off tax rate for companies bring money held offshore back to the US, i.e. another round of ‘Homeland Investment Act’. In the House plan, the tax rate is 14%, so higher than promised earlier. Most economists do not expect it to have a significant growth impact, in line with what research proved to be the case last time. The money will more likely be spent on share buybacks and dividends. In addition, the companies may pay down their debt.

Increasing public debt but downgrade unlikely at the moment

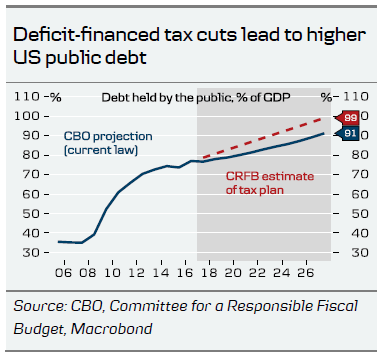

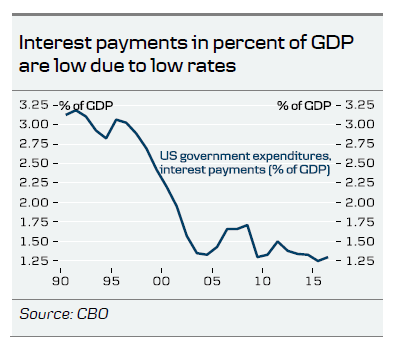

Economists agree that it is not the right time to spend more money, as we are already close to full employment and fiscal policy works with a lag on the real economy. Also, it means there is less ammunition to boost growth through fiscal policy when the next crisis hits. According to estimations made by Committee for a Responsible Fiscal Budget (CRFB), US public debt will increase from around 77% currently to 99% (versus 91% under currently law) based on the House tax bill. Here, it is important to remember that the Republicans have included some ‘gimmicks’ in the proposal to make it look cheaper than it actually is. For instance, new policy appears to be temporary in the bills but in reality it is going to be extended (politicians have talked openly about this). Also note that most models show that the dynamic effect on government deficit is limited, see CFRB: Dynamic Scoring Confirms: House or Senate Tax Bills Would Still Add to Debt, 16 November. Despite higher public debt (remember that public debt is already unsustainable in the long run under current law), economists do not seem worried about a potential downgrade. Interest payments in percent of GDP have declined due to lower rates and the US economy is in good shape. There does not seem to be a clear tipping point but history shows that politicians do not usually act until a problem becomes urgent, which could be when the US falls into recession next time and public finances deteriorate. One economist made the point that Japan did not lose its triple ‘AAA’ rating before debt reached 120% of GDP. Others argued that it may not be a major event if the US credit rating is lowered.

Powell was the safe choice as next Fed Chair

As President Trump was unlikely all along to reappoint Janet Yellen as Fed Chair, Powell was the safe choice, as he is likely to pursue the current monetary policy strategy with gradual hikes and a continuation of ‘quantitative tightening’ (shrinking the balance sheet) but is likely to be a bit easier on regulation. Also, his nomination means that the Fed’s independence is not under pressure (at least for now), as some have feared that people like Kevin Warsh or Gary Cohn, who might have been under Trump’s control, could take over.

That said, Powell’s record and background is definitely not as strong as Janet Yellen’s or Ben Bernanke’s and he is going to rely more on Fed staff than previous Fed Chairs. A more inexperienced Fed may be problematic when the next crisis hits or when the Fed is going to decide the future monetary policy framework.

No-one expects any trouble when the Senate is set to approve Powell, most likely before New Year (but perhaps not until after the December Fed meeting). Economists do not expect further nominations for the vacant seats before Powell is approved. There is not much speculation about who could be nominated for the seats but names like Marvin Goodfriend, Kristin Forbes and Jeremy Stein were mentioned. Analysts do not expect any controversial nominations as the Senate Banking Committee usually works by consensus (which is good for Fed’s independence). We may see a package of nominations including one Democrat-leaned person in order to get Democratic support for the nominations in the Senate.

It seems unlikely that John B. Taylor will become the Fed Vice Chair, as he may be too proud to accept something less than the Chair. The analysts we spoke with expect Yellen to step down as Fed Governor when her term as Chair expires although she could stay on the board as a regular Fed governor for a little while until some of the vacant seats are filled.

While a Powell-led Fed may be more hawkish on the margin (depending on future nominations), analysts do not expect the Fed to become more rule based. Also, any attempts to end/audit the Fed (or other controversial changes to the Fed) seem unlikely to pass Congress at this point.

Low probability of trade war with China

While President Trump has advocated for big shifts in US foreign and trade policy for a long time, he has tweeted more than he has actually acted. The foreign policy experts we talked with think the risk of a trade war with China is low, especially as China has made some concessions to the US on trade and is working with the US on North Korea. In general, analysts are more worried about NAFTA, as the negotiations are also spilling over to the Mexican election next year. A likely scenario, especially if Trump gets a victory on taxes, is that the US will get some concession on, for example, the rules of origin but will not pull out of the deal (all businesses are lobbying against this). If the US does pull out, it would be bad for companies, as many US companies have supply chains in Mexico. One risk factor is that if Trump were to become a ‘lame duck’ after the mid-term election (assuming the Democrats win either the House or the Senate), he may become more active on foreign and trade policy, where the President in general has more power to act alone

Daily Wave Analysis: USD/JPY Falling Wedge Approaches 38.2% Fibonacci Level

Currency pair USD/JPY

The USD/JPY is approaching a 38.2% Fibonacci support level and potential bounce spot. A failure for price to break above resistance could still indicate an extension of the bearish correction towards lower Fibonacci levels like the 50% Fib.

The USD/JPY is testing the support trend line (green) which could cause price to bounce back to the top of the channel resistance (red). Price seems to be building a falling wedge chart pattern as well, which is another factor that could create a bullish response.

Currency pair EUR/USD

EUR/USD is retesting the support trend line (blue). A break below the support could indicate a failure to continue the uptrend and makes an ABC more likely than a 123 (pink) pattern, which in turn could mean that the wave 4 (light purple) is still active.

The EUR/USD potential breakout aboveresistance (red) could indicate a continuation of the uptrend within a wave 5 (purple) of wave 3 (pink). A push below the 61.8% Fib makes a wave 4 less likely.

Currency pair GBP/USD

The GBP/USD is building a bullish channel (red/green) within the sideways range (red/blue). A breakout above the top (100% Fib) or below the support (blue) is needed before a new trend can be expected.

The GBP/USD is either expanding itsWXY complex correction (green) via a new ABC (blue) or price will break below the channel support (green) and build a bearish zigzag (red).

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7530; (P) 0.7569; (R1) 0.7602; More...

Intraday bias remains on the downside for the moment. Current decline from 0.8124 should target next key cluster level at 0.7322/8. On the upside, above 0.7607 minor resistance will turn intraday bias neutral. But outlook will stay bearish as long as 0.7729 resistance holds.

In the bigger picture, corrective rise from 0.6826 medium term bottom is likely completed at 0.8124, after hitting 55 month EMA (now at 0.8049). Decisive break of 0.7328 key cluster support (61.8% retracement 0.6826 to 0.8124 at 0.7322) will confirm. And in that case, long term down trend from 1.1079 (2011 high) will likely be resuming. Break of 0.6826 will target 61.8% projection of 1.1079 to 0.6826 from 0.8124 at 0.5496. This will now be the favored case as long as 0.7729 near term resistance holds.

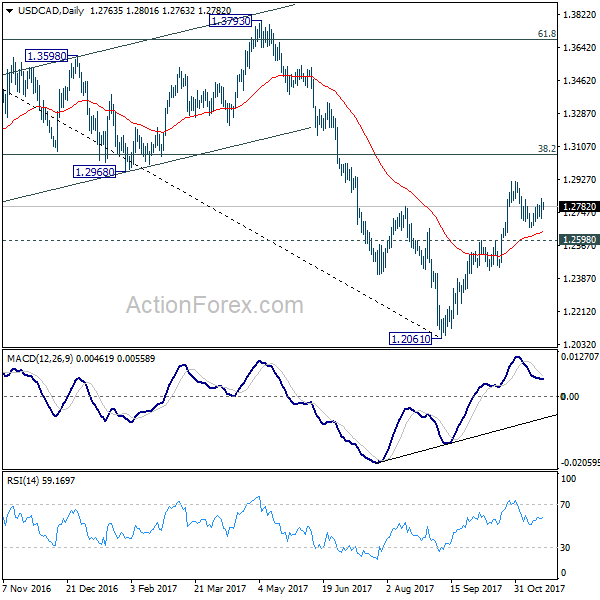

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2710; (P) 1.2767; (R1) 1.2820; More....

Intraday bias in USD/CAD remains neutral at this point. Price actions from 1.2916 are seen as a corrective pattern. In case of another fall, we'd expect downside to be contained by 1.2598 resistance turned support and bring rebound. Above 1.2819 will turn bias to the upside for 1.2916 first. Break there will resume whole rally from 1.2061 to 38.2% retracement of 1.4689 to 1.2061 at 1.3065. However, sustained break of 1.2598 will argue that rebound from 1.2061 has completed after hitting 55 week EMA (now at 1.2916). Near term outlook will be turned bearish in this case.

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4689 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Rise from 1.2061 medium term bottom should now target 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Firm break there will target 1.3793 key resistance next (61.8% retracement at 1.3685). We'll now hold on to this bullish view as long as 1.2450 support holds.

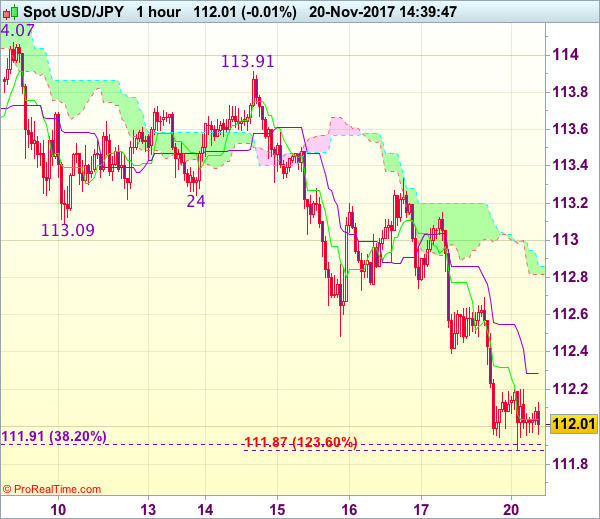

Trade Idea : USD/JPY – Sell at 112.60

USD/JPY - 112.02

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 112.04

Kijun-Sen level : 112.29

Ichimoku cloud top : 112.86

Ichimoku cloud bottom : 112.82

New strategy :

Sell at 112.60, Target: 111.60, Stop: 111.60

Position : -

Target : -

Stop : -

As the greenback has remained under pressure after last week’s selloff from 113.91, suggesting recent decline from 114.74 top is still in progress, hence bearishness is seen for further weakness to previous support at 111.65, break there would extend fall to 111.45-50, however, near term oversold condition should limit downside and reckon 111.00-05 would hold from here, bring rebound later.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as 112.60-65 should limit upside. bring another decline later. Above 112.85-90 would risk test of previous support at 113.09 but only break there would abort and signal low is formed instead, bring a stronger rebound to 113.33 resistance first.