Sample Category Title

USD/CAD Bouncing Higher

USD/CAD is riding higher. The technical structure suggests further strengthening towards hourly resistance at 1.2820 (07/11/2017 high). Hourly support lies at 1.2667 (10/11/2017 low). Expected to show continued upside pressures.

In the longer term, the pair has broken longterm support that can be found at 1.2461 (16/03/2015 low). Strong resistance is given at 1.4690 (22/01/2016 high). The pair is likely to head further lower.

USD/CHF Riding Short-Term Downtrend Channel

USD/CHF is heading lower. The technical structure indicates further downside risks. The pair has failed to hold consistently above the parity. If the pair heads towards 0.98, there might be even more downside pressures. The road would be wide-open for further decline.

In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015.

USD/JPY Wide-Open For Further Downside Moves

USD/JPY has broken short-term uptrend channel. Hourly support given at 113.09 (09/10/2017 low) has been broken. Stronger support is located at a distance at 111.12 (20/09/2017 low). Expected to show further decline.

We favor a long-term bearish bias. Support is now given at 99.02 (10/08/2013 low). A gradual rise towards the major resistance at 125.86 (05/06/2015 high) seems unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

GBP/USD Volatility Declines

GBP/USD is still holding below 1.32. Support is given at 1.3027 (06/10/2017 low). Resistance area is given around 1.3200. The technical structure suggests further sideways price action.

The long-term technical pattern is reversing. The Brexit vote had paved the way for further decline. Long-term support can be found at 1.1841 (07/10/2017 low). Long-term resistance given around 1.35 is at stake and indicates a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

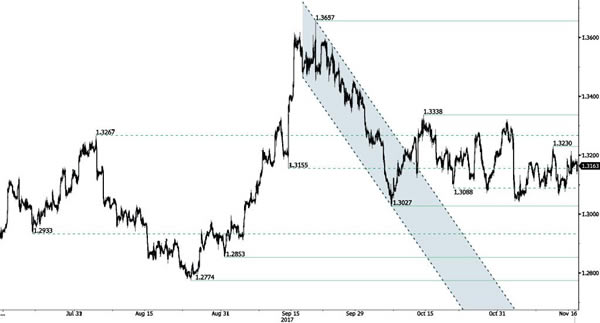

EUR/USD Bearish Consolidation After Strong Surge

EUR/USD is consolidating at the moment. Hourly resistance is located at 1.1878 (12/10/2017 high). T Hourly support is given at a distance at 1.1554 (07/11/2017 low). Expected to show continued short-term consolidation before heading higher towards resistance at 1.1878 ( 12/10/2017 high).

In the longer term, the momentum is now turning largely positive. We favour a continued bullish bias. Key resistance is holding at 1.2252 (25/12/2014 high) while strong support lies at 1.0341 (03/01/2017 low).

US Stocks Bounce Back Ahead Of Data And Fed Speakers

- Futures Higher But Pull-Back May Not Be Over;

- UK Retail Sales Beat Expectations But Worrying Trend Continues;

- US Data and Central Bank Speakers Eyed.

- Futures Higher But Pull-Back May Not Be Over

US equity markets are on course to bounce back from their blip on Thursday, with futures around a third of a percentage point higher, slightly shy of the gains seen in Europe and Asia.

Wednesday's sell-off suggested that investors had lost a little faith in the two month long rally that saw indices make new record highs almost every day. While they still look vulnerable to a small pull-back, it would appear investors are not quite ready to concede yet. Stocks have come off another strong earnings season and with Trump's tax reform plan running into difficulties in Congress, it seems investors are using the opportunity to lock in some profit.

UK Retail Sales Beat Expectations But Worrying Trend Continues

UK retail sales data gave the pound a small boost this morning, despite the numbers themselves being far from desirable. Consumer spending fell by 0.3% in October compared to a year ago – both overall and on a core basis – which was slightly better than expected but also marked the first decline in four and a half years, when the UK was fighting to stay out of recession.

While the slowdown in consumer spending comes as no surprise given the negative wage growth that has held the economy back since the start of the year, a worrying trend has formed that will likely weigh on economic output in the coming quarters. The pound may well have been given a small lift by today's numbers but the reality is that the near-term impacts of the Brexit vote are being felt and there's little to suggest the worst has passed. The FTSE is underperforming its peers this morning, weighed down by sterling's ascent, as well as general weakness that we're seeing across the commodity space.

US Data and Central Bank Speakers Eyed

There's no shortage of economic data and central bank speakers on the agenda today, with jobless claims, the Philly Fed manufacturing survey, industrial production and capacity utilisation data all being released ahead of the open. The data comes as the Fed prepares to raise interest rates again in December – which is almost entirely priced in – although when it comes to next year, markets are very much under-pricing what the Fed has proposed. While this has been a common theme over the last few years, it would suggest that markets may have some catching up to do, particularly if Donald Trump can get tax reform through, with it currently running into some stumbling blocks in Congress.

The CPI and retail sales data we got from the US on Wednesday was certainly supportive when it comes to further rate hikes, with the trend in both having improved following a rough start to the year. There are still understandable doubts about whether the Fed should still pursue tightening at the current pace due to the inconsistency in the data but as long as the data remains on a positive trajectory, I don't see it deviating from the current path, not yet anyway.

We'll get plenty of views on this today, with four Fed officials scheduled to appear including Lael Brainard – a permanent voter on the FOMC – Robert Kaplan – a voter this year – and John Williams and Loretta Mester, both of whom will be voters next year. With a number of positions still to be filled as Trump continues to shape the central bank as he wishes, the consensus view on the committee could change so it's well worth paying attention to those that will have the vote next year. These will be joined by policy makers from the ECB and Bank of England who are also scheduled to appear throughout the day.

NZDUSD Bias Tilted To The Downside

NZDUSD has a bias that is tilted to the downside during the past week, with trend indicators supporting this view. A bearish crossover of the 20 with the 50-period moving average on the 4-hour chart and an RSI below 50 are indicators of weakness in the market.

Looking at the broader picture, NZDUSD is in a downtrend and has been consolidating a decline from 0.7434 and pausing at a low of 0.6817 on October 27. The market has consequently been moving sideways and capped at the 23.6% Fibonacci level (0.6961) of the downleg from 0.7434 to 0.6817. After several tests of this level, prior upside momentum was not sustained, and prices fell back down. The target is 0.6817, which if broken would increase downside pressure and confirm a resumption of the downtrend for a move towards 0.6674.

With upside momentum non-existent in the near-term, it would be quite a challenge to rise above what is key resistance at 0.6817. But if successful, the market’s focus would shift back to the upside to target the 0.7000 handle. But only a move above 0.7200 would invalidate the short-term downtrend.

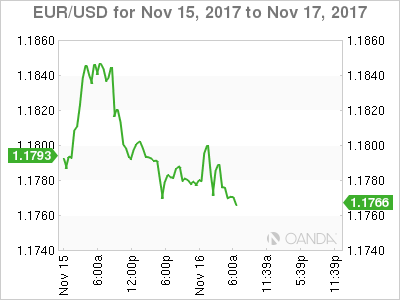

Euro Edges Lower As Eurozone CPI Matches Forecast

The euro is showing little movement in the Thursday session. Currently, EUR/USD is trading at 1.1770, down 0.18% on the day. In the eurozone, Final CPI gained 1.4% and Core Final CPI gained 0.9%, as both readings matched the forecasts. In the US, there are two key events. Unemployment claims is expected to drop to 235 thousand, and the Philly Fed Market Index is expected to drop to 24.5 points. On Friday, ECB President Mario Draghi and German Buba President Jens Weidmann speaks at Frankfurt European Banking Congress. The US will release Building Permits and Housing Starts.

There were no surprises from key consumer spending and inflation data on Wednesday. CPI and Core CPI matched the forecasts, with gains of 0.1% and 0.2%, respectively. Consumer spending reports were a mix – retail sales gained 0.1%, shy of the estimate of 0.2%. Core Retail Sales came in at 0.2%, beating the forecast of 0.0%. The Federal Reserve would certainly like to see higher inflation numbers, which remain well below the Fed inflation target of 2.0%. Still, the markets are very bullish on additional rate hikes, as the odds of upcoming rate hikes continues to move higher. Currently, the likelihood of a rate hike in December stands at 96%, and a January raise is priced in at 94%.

Central banks do their best to avoid causing market volatility, which requires clear communication with the public and the markets. However, with bank policymakers making public statements on a daily basis, differences in opinion on future monetary policy or quantitative easing are bound to come up, and this can lead to market movement. Early in the week, Fed Chair Janet Yellen and ECB Mario Draghi participated at an ECB event which focused on communication with the markets. Yellen acknowledged that the FOMC committee of 19 members posed problems, as members did not always speak with a unified voice. Yellen admitted that this problem would not be solved anytime soon, saying it was 'a work in progress'. To be fair, this is also an issue for the ECB, as the markets have on occasion reacted to comments from individual policymakers.

Eurozone Inflation Unrevised For October

Euro data this morning offered up no new surprises – Eurostat's second estimate of eurozone inflation for October was confirmed at +1.4%, down from +1.5% in September and well below the European Central Bank (ECB) target of just below +2%.

The core-inflation rate was down to +0.9%, largely due to a sharp slowdown in prices for services.

So not an encouraging release for ECB policy makers, who expect worse news to come before what they hope will be a turn for the better in mid-2018.

Details:

Eurozone: Oct CPI +0.1% m/m; +1.4% y/y

Eurozone: Oct CPI Forecast +0.1% m/m; +1.4%y/y

Eurozone: Oct Core CPI -0.1% m/m; +0.9% y/y

Eurozone Oct CPI Ex-Tobacco +0.1% m/m; +1.3% y/y

Euro under pressure

The 'single' unit is currently trading atop of its intraday euro session low at €1.1780, and remains under pressure, capped by its 50-period moving average at €1.1802.

The techies suggest that further weakness can be expected towards the horizontal support at €1.1760 at first. A clear break below this threshold would open the way towards the support at €1.1725 and €1.1700.

Only a rebound above the strong psychological resistance at €1.1805 would turn the intraday outlook to 'bullish.'

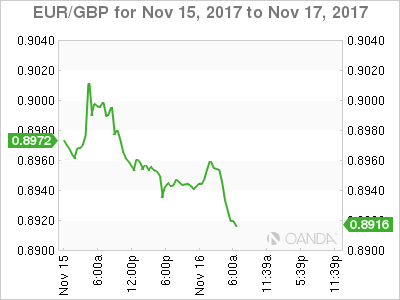

Technical Outlook: EURGBP – Shooting Star Pattern Suggests Further Easing

The cross is lower on Thursday and sees risk of further easing after Wednesday’s strong upside rejection on attempts to sustain break above 0.9013.

Shooting star patter was formed on daily chart, warning of deeper fall as today’s bearish extension returned below daily cloud and probed above 0.8928 pivot (Fibo 38.2% of 0.8791/0.9013 upleg).

South turning daily indicators support the notion for bearish extension towards next strong support at 0.8876 (Fibo 61.8% / converged 10/20SMA’s).

Upside attempts are expected to stay capped by 100SMA (0.8947) and keep alive bearish n/t scenario.

Res: 0.8947, 0.8974, 0.9013, 0.9026

Sup: 0.8910, 0.8892, 0.8876, 0.8843