Sample Category Title

U.K Retail Sales Bounce Back In October

Data this morning showed that U.K. retail sales rebounded last month, as the strong performance of the second-hand sector offset a drop in sales of clothes and footwear.

Retail sales grew +0.3% on the month in October, beating market expectations of +0.1% growth and bouncing back from September's -0.7% declines.

Digging deeper, second-hand stores had a particularly strong month, driving the overall growth in sales. Clothing stores disappointing month can be attributed to unseasonably warm weather.

However, on an annual basis, retail sales posted its first decline in four-years, and was down by -0.3%.

Consumer price growth stood at +3% in October, the joint-fastest pace of inflation in nearly six-years.

Note: U.K's economy has slowed visibly this year as consumers come under pressure from accelerating inflation driven by the pound's steep decline in the wake of the Brexit referendum last year.

Pounds Reaction

Sterling is trading a tad higher, but the gains are limited, as today's data should not change investors' expectations that the Bank of England won't raise interest rates again any time soon, while concerns about Brexit uncertainty remains.

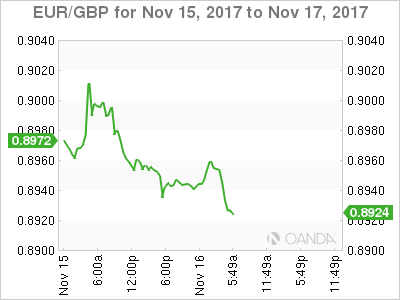

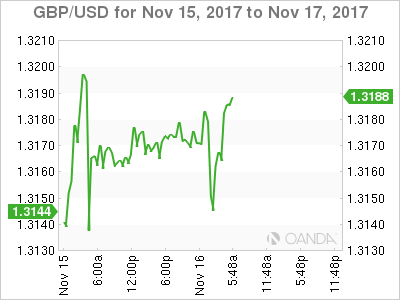

GBP/USD is last up +0.14% at £1.3189, up from £1.3159 before the release, and is expected to run into some strong offers just above the psychological £1.3200 handle. EUR/GBP trades down -0.3% at €0.8922.

Market Update – European Session: Risk Appetite Finds Some Headroom, UK Retail Sales Ahead Of Expectations

Notes/Observations

UK Oct Retail Sales registers a slight beat

UK PM May grapples with Brexit challenges at home and abroad

German Chancellor Merkel continues to face hurdles putting together her ruling coalition

Overnight

Asia:

PBoC Deputy Gov Yin Yong: Global asset prices at high level, saw possible adjustment in global asset prices; Monetary policy should also prevent systemic risks. PBoC to improve macroprudential assessment system to deal with systemic risks.

China Finance Official: Financial sector faced bubble risks, reflected in high broad money supply

PBOC Research Head: China could face “big crisis” if economic reforms are too slow; need to improve local Govt finances to help tackle local Govt debt problems

China Banking Regulator CBRC releases draft rules on banks equity management; effective in 2018. Required banks to strengthen governance systems and to establish capital restraint mechanisms based on capital adequacy ratios

Europe:

EU Brexit Negotiator Verhofstadt: Did not expect Brexit talks to fail

German Chancellor Merkel said to be wary of pushing UK PM May too hard in Brexit talks could backfire. Saw risk that excessive EU pressure over the Brexit divorce bill could weaken PM May at home. Believed If May were replaced, most of the likeliest successors were hardline Brexit backers.

UK Home Affairs Committee Report: UK faced the prospect of major border disruption after Brexit if Govt did not t prepare for all eventualities. To date had taken insufficient contingency planning to prepare the UK’s Border Force for failure to reach a deal with EU 27

Chancellor of Exchequer Hammond (Fin Min) said stick to fiscal rules and resist demands for spending surge in upcoming UK budget

Americas:

Fed's Rosengren (hawk, voter): supports a Dec rate hike; weak inflation held down by temporary factors

President Trump tweet: Big vote tomorrow (May 16th) in House, tax cuts getting close

Senator Ron Johnson (R-WI) announces he will vote Against the Senate tax bill (1stSenate Republican that would oppose the bill)

Bank of Canada (BOC) Wilkins: Reason for caution was desire to avoid policy reversal, motivated by lower than expected inflation

Economic Data:

(NL) Netherlands Oct Unemployment Rate: 4.5% v 4.7% prior

(FR) France Q3 ILO Unemployment Rate: 9.7% v 9.5%e; Mainland Unemployment Rate: 9.4% v 9.1%e

(EU) Oct EU27 New Car Registrations: +5.9% v -2.0% prior

(HK) Hong Kong Oct Unemployment Rate: 3.1% v 3.1%e (matched lowest level since Feb 1998)

(SE) Sweden Oct Unemployment Rate: 6.3% v 6.3%e; Unemployment Rate (Seasonally adj): 6.7% v 6.7%e

(UK) Oct Retail Sales (Ex Auto/Fuel) M/M: 0.1% v 0.0%e; Y/Y:-0.3 % v -0.4%e

(UK) Oct Retail Sales (Includes Auto/Fuel) M/M: 0.3% v 0.2%e; Y/Y: -0.3% v -0.5%e

(EU) Euro Zone Oct Final CPI Y/Y: 1.4% v 1.4%e; CPI Core Y/Y: 0.9% v 0.9%e; CPI M/M: 0.1% v 0.1%e

(BR) Brazil Nov FGV Inflation IGP-10 M/M: 0.2% v 0.1%e

Fixed Income Issuance:

(ES) Spain Debt Agency (Tesoro) sold total €4.65B vs. €4.0-5.0B indicated range in 2021, 2022, 2027 and 2066 Bonds

Sold €1.02B in 0.05% Jan 2021 SPGB bond; Avg yield: -0.022% v +0.043% prior, Bid-to-cover: 2.6x v 1.38x prior

Sold €973M in 0.45% Oct 2022 SPGB; Avg yield: 0.363% v 0.336% prior, Bid-to-cover: 2.34x v 1.82x prior

Sold €1.24B in 1.45% Oct 2027 SPGB; Avg yield: 1.536% v 1.457% prior; Bid-to-cover: 1.52x v 1.35x prior

Sold €1.43B in 3.45% July 2066 SPGB; Yield: 3.192% v 3.249% prior; Bid-to-cover: 1.5x v 1.3x prior

(FR) France Debt Agency (AFT) sold total €4.994B vs. €4.0-5.0B indicated range in 2020, 2023 and 2025 Oats

Sold €1.016B in 3.5% Apr 2020 Oat; Avg Yield -0.60% v -0.23% prior; Bid-to-cover: 4.48x v 2.47x prior

Sold €2.523B in 0% Mar 2023 Oat; Avg Yield: -0.13% v -0.07% prior; bid-to-cover: 2.28x v 1.10x prior

Sold €1.455B in 0.5% May 2025 Oat; Avg Yield: 0.20% v 0.29% prior; Bid-to-cover: 2.28x v 2.18x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 +0.6% at 384.1, FTSE flat at 7372, DAX +0.6% at 13054, CAC-40 +0.6% at 5333, IBEX-35 +1.2% at 10130, FTSE MIB +0.3% at 22220, SMI +0.4% at 9125, S&P 500 Futures +0.4%]

Market Focal Points/Key Themes:

European Indices trade higher across the board rebounding from the longest losing streak of the year, with outperformance in Spain, France and Germany, while the UK and Italy underperform with Banking names weighing on the FTSE MIB on liquidity concerns.

On the earnings front Sodexo trades lower after in line results, while Zumtobel trades sharply lower in Austria after a decline in profits. Elsewhere Bouygues trades higher after strong results and lifting its EBITDA margin outlook. On the M&A front Spire Healthcare trades lower after terms of a deal with Mediclinic have still not been reached, while Italian Banking names are lower after Banca Carige was unable to sign an underwriting agreement for planned €560M capital increase.

Looking ahead we continue to see major retailers report out of the US including Walmart and Bestbuy.

Equities

Consumer discretionary [Zumtobel [ZAG.AT] -20% (Earnings)]

Industrials: [GKN [GKN.UK] -7.7% (CEO steps down, take impairment charge), Sodexo [SW.FR] -2.7% (Earnings), Electrolux [ELEXB-SE] -2.1% (FY18 outlook)]

Financials: [Close Brother [CBG.UK] +4.1% (Trading update), Unicredit [UCG.IT ]-3.3% BPER Banca -2%, UBI [UBI.IT] -1.5% Unicredit [UCG.IT -0.4% (Banca Carge unable to sign underwriting agreement for planned Cap increase)]

Telecom: [Bouygues [EN.FR] +4.9% (Earnings)]

Healthcare: [Spire Healthcare [SPI.UK] -7% (No agreement reached yet with mediclinic)]

Real Estate: [ British Land [BLND.UK] +2.15 (Trading update)]

Speakers

BOE Gov Carney in a local media interview noted that BOE to support the economy no matter what the Brexit outcome. Was everyone's interest to achieve Brexit transition agreement

ECB’s Mersch (Luxembourg): Euro region still needed monetary stimulus; would not hesitate to act if necessary. Market would be wrong in expecting further QE extension (current program set to end in Sept) Securitization could increase the resilience of the banking sector

ECB's Jazbec (Slovenia): Inflation moving in-line with ECB expectations

EU's Barnier Brexit negotiation team said to flatly reject PM May's request for bespoke trade deal. EU believed only a standard free trade agreement is possible

German Chancellor Merkel: Exploratory talks on coalition had shown major differences between parties but believe an agreement could be reached. Expected coalition talks to last hours (**Note: Thursday deadline for forming Jamaica coalition)

Poland Central Bank's Kropiwnicki: No rate hike seen in 2018 (in-line with MPC majority). Could keep its interest rates unchanged at record low because monetary tightening at current phase of economic cycle could threaten investment and consumption

Czech Central Bank Gov Rusnok: Interest rates seen rising to 3.00% in two years’ time

Turkey Presidential advisor Ertem: No issue with financing the current account deficit in 2018 with inflation being tolerable and reasonable

PBoC Adviser Sheng: CNY currency (Yuan) will be 'stable' around 6.60 versus US dollar, market rates to see small fluctuations at high level; To maintain 'prudent' monetary policy in 2018. Expected to keep yuan stable; could nnot let currency fall or rise sharply

China Commerce Ministry (MOFCOM): urges EU to abide by WTO rules

Thailand Central Bank Gov Veerathai: Domestic economy in better shape at this time compared to beginning of 2017. Agricultural sector still faced challenges. THB currency (Baht) in line with regional peers; appreciation due to USD weakness

Currencies

EUR/USD found some technical resistance at its 55-day moving average and its price action was little changed in the session.

GBP/USD saw only marginal strength in the aftermath of better-than-expected retail sales data for Oct. The pair was around 1.3190 just ahead of the NY morning.

USD/JPY was slightly higher and contained within recent ranges. Pair at 113.25 ahead of the NY morning.

Fixed Income

Bund futures trade at 162.52 down 29 ticks, in the middle of this week’s trading range. Support lies at 162.00, followed by 161.50. Resistance stands initially at 163.51, followed by 164.25.

Gilt futures trade at 124.83 down 10 ticks following slight beat in UK retail sales. Continued upside eyeing 125.75 then 126.47. Downside targets include 124.24 then 123.74.

Thursday’s liquidity report showed Wednesday’s excess liquidity fell from €1.869T to €1.867T and use of the marginal lending facility dropped to €189M from €194M

Looking Ahead

(ID) Indonesia Central Bank (BI) Interest Rate Decision: Expected to leave 7-day Reverse Repo Rate unchanged at 4.25%

(EG) Egypt Central Bank Interest Rate Decision: Expected to leave key Interest Rates Unchanged

(IT) Italy Debt Agency (Tesoro) final day of sale process of BTP Italia (retail bond)

05:30 (HU) Hungary Debt Agency (AKK) to sell in 12-month Bills

05:30 (HU) Hungary Debt Agency (AKK) to sell Floating Bonds

05:30 (UK) DMO to sell £2.5B in 1.25% 2027 Gilts

05:50 (FR) France Debt Agency (AFT) to sell €1.5-2.0B in Inflation Linked 2021, 2024 and 2047 Bonds (Oatei)

06:00 (IL) Israel Q3 Advance GDP Annualized: 2.7%e v 2.4% prior

06:50 (NO) Norway Central Bank (Norges) Gov Olsen

08:00 (RU) Russia Gold and Forex Reserve w/e Nov 10th: No est v $426.3B prior

08:05 (UK) Baltic Dry Bulk Index

08:30 (US) Nov Philadelphia Fed Business Outlook: 24.6e v 27.9 prior

08:30 (US) Initial Jobless Claims: 235Ke v 239K prior; Continuing Claims: 1.90Me v 1.901M prior

08:30 (US) Oct Import Price Index M/M: 0.3%e v 0.7% prior; Y/Y: 2.5%e v 2.7% prior; Import Price Index ex Petroleum M/M: 0.2%e v 0.3% prior

08:30 (US) Oct Export Price Index M/M: 0.4%e v 0.8% prior; Y/Y: No est v 2.9% prior

08:30 (CA) Canada Sept Int'l Securities Transactions (CAD): No est v 9.9B prior

08:30 (CA) Canada Sept Manufacturing Sales M/M: -0.5%e v +1.6% prior

08:30 (CA) ADP Employment (1st ever release)

08:30 (US) Weekly USDA Net Export Sales

09:00 (UK) BOE Gov Carney with members Broadben, Cunliffe, Ramsden at BOE Future Forum, Liverpool

09:00 (BR) Brazil to sell 2023 LFT bills

09:00 (BR) Brazil to sell 2018, 2019 and 2021 LTN Bills

09:10 (US) Fed’s Meseter (hawkish, non-voter) at Cato conference

09:15 (US) Oct Industrial Production M/M: 0.5%e v 0.3% prior; Capacity Utilization: 76.3%e v 76.0% prior, Manufacturing Production: 0.5%e v 0.1% prior

09:30 (FR) ECB’s Villeroy (France) in Amsterdam

10:00 (US) Nov NAHB Housing Market Index: 67e v 68 prior

10:30 (US) Weekly EIA Natural Gas Inventories

11:00 (IT) ECB members Nowotny and Praet in Florence

12:00 (CH) SNB's Maechler speaks in Geneva

13:00 (US) (US) Treasury to sell $11B in 10-Year TIPS Reopening

13:10 (US) Fed’s Kaplan (moderate, voter) in Houston

15:00 (PT) ECB’s Constancio (Portugal) in Ottawa

15:45 (US) Fed's Brainard (voter, dove) keynote speech at OFR conference

15:45 (US) Treasury Sec Mnuchin at Financial Stability Oversight Council meeting

16:30 (NZ) New Zealand Oct Business Manufacturing PMI: No est v 57.5 prior

16:45 (NZ) New Zealand Q3 PPI Input Q/Q: No est v 1.4% prior; PPI Output Q/Q: No est v 1.3% prior

16:45 (US) Fed’s Williams (moderate, non-voter)

Technical Outlook: SPOT GOLD – N/T Focus Turns Lower After Strong Upside Rejection On Wednesday

Gold stands at the back foot today following yesterday's recovery stall ahead of key Fibo 61.8% barrier at $1290.

Subsequent quick fall left bearish daily candle with long upper shadow that signaled strong upside rejection and risk of further weakness.

Today's probe below Tenkan-sen ($1278) would result in extended bearish action on close below as daily Tenkan-sen/Kijun-sen lines are in bearish setup. Bears could travel to $1270 (Tuesday's spike low) and could extend to key support at $1263 (27 Oct low/200SMA).

Conversely, lift above $1290 pivot is required to neutralize bearish threats.

Res: 1279, 1285, 1290, 1294

Sup: 1276, 1273, 1270, 1263

Bank Of England Kills Debt With Inflation

UK inflation has come in at a strong 3% per annum, which is weighing on the pound, because an interest rate hike in 2018 looks likely. The pound is trading sideways at 1.30-1.32 USD. Why is the Bank of England so cautious about raising rates?

Because central banks, BoE included, are letting inflation run to kill the massive debt accumulated over past decades. They cannot raise interest rates quickly, as this would burst the bond bubble and disrupt the economy. BoE is playing safe and will raise rates gradually and slowly – so inflation will run higher. This will push down the pound.

Brexit has not destroyed the UK economy, but is has boosted inflation. Currency wars are not over, just because markets expect interest rates to rise. Global economies are still way into a devaluation battle, so central banks must play dovish. Too much short-term confidence may bring investors back too early, and demand for currencies would weigh on growth.

European Markets And US Futures Rebound | UK Retail & German Banking Sector In Spotlight

K Retail Sales may disappoint again

German Banking industry an interesting area

Global Stock market rout ease off

Merkel faces first post-election test

Fed wants to review inflation target

Markets

European stock market and US futures looked set to stem their losses. Today's European car sales data has shown growth reviving and this has set a positive tone for investors. Concerns about outsized gains in the stock market, overstretched valuation and the sell-off in the commodity space made investors shave some profit off the table in the last few days. However, bargain hunters have stepped back in and as a result, the oil price has moved higher. Traders are no longer paying much attention to the stockpiles or inventory story anymore.

Currencies

The UK retail sales data will deliver further information about consumer spending. Yesterday's wage and unemployment numbers were lacklustre and the wage growth number clearly showed how inflation is outpacing the wage growth. The number of people employed also dropped by 14K and this raised many eyebrows amid investors. Brexit and employment market go hand in hand and it appears that the employment market is ready to show the effects of Brexit uncertainty. The silver lining is that one particular number would not necessarily sets the trend, we need to have more a few reading before we say that the train off the track.

We expect the retail sales number to be underwhelming and the weaker trend could very well continue. The forecast is for 0.1%. The weak retail sales number could change in the coming months because we are approaching close to Black Friday and holiday period.

As for the Euro, the currency shows the ratio of aggregate puts to call options is still increasing while the recent CFTC number shows the net longs at a level not seen since 2011. The currency is simply on the rollercoaster against the dollar and Sterling. The strong German economic numbers released this week provided strong wind but it appears some stronger catalyst is needed for the currency to pick up its steam again.

Commodities

The gold price has been trading in a tight range and we need to break out of the recent consolidation zone which ranges from 1270 to 1290. The firm US data bolstered the prospects of another rate hike this year and this has made traders a little cautious in taking any major long positions. As long as the unemployment keeps falling and the US sustains its growth level, it is likely that the Fed would not only hike the interest rate this year but the process would continue into 2018 as well. This would strengthen the dollar index which could take the further shine off the metal.

Stock

The German banking industry remains the area of interest especially after the recent developments about Deutsche Bank. Althgouh consolidation in the German banking sector could be the theme for the next year, but we do think Cerberus capital management's 3% stake in Deutsche Bank is more of a value play. The fund may be looking to make money on the bank's higher share price.

Elliott Wave Analysis: EURUSD Looking Higher, While DAX Reversing Lower

We see some intraday recovery on stocks, but likely only a temporary move. We see DAX turning up with nearly 200points so it appears that wave A is here, which means that correction is underway and may stop at 13140-13228 resistance area after three waves.

German DAX, 1H

Once DAX completes a corrective rally, that’s when we may see a new strong push up on EURUSD, which is now seen in a corrective set-back. It can be wave four, or even wave two of a higher degree, but in both cases we expect market to resume the uptrend. Personally, I am hoping on a deeper and cleaner three wave drop before I may look for longs.

EURUSD, 1H

Technical Outlook: WTI OIL Trades In Extended Consolidation, Lacks Clearer N/T Direction Signal

WTI Oil holds within narrow consolidation for the second day after falling sharply on Tuesday. Consolidation above correction low at $54.80 was so far capped by falling thick hourly cloud and shows no stronger signs of basing but remains above rising 20SMA (currently at $54.80) which marks pivotal support together with $54.53 (Fibo 38.2% of $49.09/$57.90 ascend).

Overall bullish daily studies and oversold slow stochastic are supportive for possible recovery, however, weakening momentum studies are limiting.

Oil price showed limited reaction on Wednesday’s weekly crude stocks data which came below forecast but still showed a draw in inventories despite wide expectations for crude stocks build.

Sentiment in improving on expectations OPE will extend its output cut program on 30 Nov cartel meeting, which could be positive factor for oil price.

Recovery needs lift above broken 10SMA ($56.28) to generate stronger bullish signal and neutralize downside threats.

Otherwise, fresh bearish acceleration could be expected on firm break below $54.80/53 pivots.

Res: 55.54, 55.82, 56.28, 56.75

Sup: 55.15, 54.80, 54.53, 54.02

Dollar Stuck In A Tax Trap, Aussie Gains Little On Employment Data

Weakened prospects on the US tax reforms continued restricting the dollar’s gains in Asia despite Wednesday’s encouraging data cementing a third-rate hike this year, while a mixed employment report in Australia did little to support the aussie.

On Wednesday, two Senate Republicans expressed their opposition to the tax plan, claiming that they would not support a plan which favours corporations over other enterprises including small companies. Particularly the new version produced on Tuesday aims to activate permanent tax cuts for corporations and only temporary tax cuts for individuals and small businesses, while embodying a key repealing component of Obamacare in the bill. This brought a new headache to Republicans as they cannot afford to lose more than two votes given that they hold a narrow majority of 52-48 in the Senate.

Markets were also worried about a flattening yield curve, with the gap between the 2-year and 10-year US Treasury yield breaking a fresh 2017 low. This could be a sign of a future economic downturn.

The dollar index remained below the 94 key-level, trading flat at 93.84, although investors cemented their hopes on further rate hikes in the upcoming year after US retail sales in October beat forecasts and CPI matched expectations. Dollar/yen rose by 0.34% to 113.24 and dollar-denominated gold retreated by 0.20% to $1,275.80 per ounce.

In Australia, the Bureau of Statistics published new employment figures, showing that 3,700 new jobs were created in October compared to 17,500 anticipated and 26,600 tracked in September (upwardly revised from 19,800). This marked a 13-month consecutive increase and the longest row of gains since 1990. Full-time workers increased by 24,300, far above the previous mark of 9,300, driving the annual change up to 298,000, while the unemployment rate declined moderately by 0.1 percentage points to 5.4%, making a fresh four-year high.

The aussie, however, posted limited gains during the session as a disappointing report on wage growth released early on Wednesday hampered chances of a rate hike anytime soon. The aussie touched a session high of $0.7608 in the wake of the data but pulled back to 0.7589 afterwards.

The kiwi extended yesterday’s losses, falling by 0.32% to $0.6853 after the ANZ survey indicated that consumers confidence index declined by 2.6 points to 123.7 in November amid a slowing housing market and concerns on political developments.

Euro/dollar slipped by 0.11% to 1.1777 after touching a one-month high of 1.1860 on Wednesday.

Pound/dollar moved sideways around 1.3142 ahead of retail sales figures out of the UK.

Turning to energy markets, oil prices rose softly, with the WTI crude edging up by 0.14% to $55.41 per barrel and Brent climbing by 0.36% to $62.09.

Next on the day, investors will mainly keep a close eye on CPI data out of the Eurozone, initial jobless claims out of the US and focus on comments given by the BOE Governor, Mark Carney.

AUD/USD: AU Unemployment Rate

The Aussie rose against the US Dollar, following the release showing unexpected decrease in Australia's unemployment. On the report, the AUD/USD currency pair showed high volatility to eventually appreciate by 0.15% or 11 base points to the 0.7598 mark and continue consolidation at a slightly stronger area of 0.7600.

The Australian Bureau of Statistics said that the country's employment grew for a 13th month in succession, while the jobless rate dropped to the lowest rate in more than four years. Data indicated that Australian unemployment rate dipped to 5.4% in October. Despite solid jobs growth, the job market remained slack due to weak pay growth, setting inappropriate environment for talks on rate increases.

EUR/USD: US Core Consumer Price Index

The Greenback fell against the European single currency on encouraging US inflation and retail sales reports. The EUR/USD currency pair rose 20 base points or 0.17% to the 1.1858 mark, but lost the gains initially to return in the area below the 1.1800 level.

The Labour Department revealed that the US consumer inflation eased to 0.1% from 0.5% in October, while its core figure appreciated to 0.2% in the same period. Relatively strong readings pointed to the end of disinflationary trend, which worried the Fed the most. The report also showed a little slowdown in retail sales growth pace, though stronger consumers spending, including higher real wages and job gains are expected to encourage retailing in the next months.