Sample Category Title

EUR/GBP Strong Downside Risk

EUR/GBP is way into a short-term bearish momentum. As long as prices are below the resistance at 0.9046 (05/09/2017 high), the shortterm technical structure is biased to the downside. Hourly support is given at a distance at 0.8733 (01/11/2017 low).

In the long-term, the pair has largely recovered from recent lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading above from its 200 DMA. Strong resistance can be found at 0.9500 (psychological level).

EUR/JPY Elliott Wave Analysis

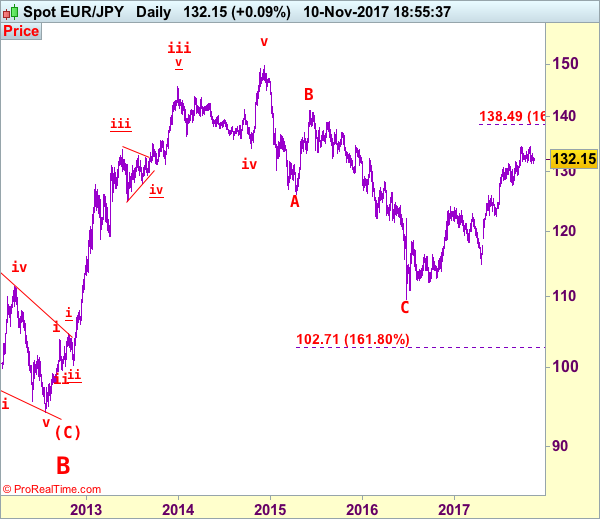

EUR/JPY - 132.12

Although the single currency fell marginally to 131.40 earlier this week, lack of follow through selling suggests consolidation would be seen and recovery to 133.00-10 cannot be ruled out, however, if our view that a temporary top formed at 134.50 is correct, upside should be limited to 133.50-60 and bring another decline, below said support at 131.40 would bring retracement of recent upmove to 131.00, then towards another previous support at 130.62, having said that, reckon 130.00 would hold from here, bring rebound later.

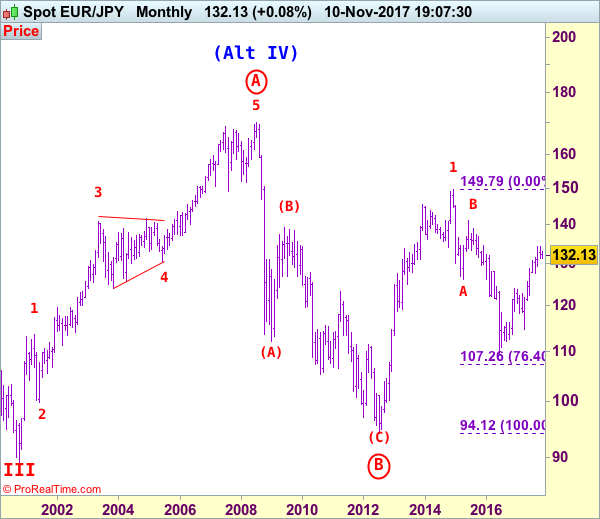

The daily chart is labeled as attached, early selloff from 169.97 (July 2008) to 112.08 is wave (A) of B instead of end of entire wave B and then the rebound from there to 139.26 is wave (B), hence, wave (C) has possibly ended at 94.12 with a diagonal triangle as labeled in the daily chart, hence upside bias is seen for further gain. Recent rally above indicated retracement level at 116.69 (50% Fibonacci retracement of the intermediate fall from 139.26-94.12) adds credence to this view and signal major reversal has commenced but first leg of this wave C has possibly ended at 149.79, hence wave 2 has commenced with wave A ended at 126.09, followed by wave B at 141.06, wave C commenced and could have ended at 109.49, indicated upside targets at 126.00 and 130.00 had been met and further gain to 135.00 would follow.

On the upside, whilst initial recovery to 133.50-60 cannot be ruled out, reckon 134.00 would hold and bring another retreat. Only break of said resistance at 134.50 would abort and signal recent upmove has resumed and extend further gain to 135.00, however, loss of upward momentum should prevent sharp move beyond 136.00-10 and reckon 136.95-00 would hold, price should falter well below 138.45-50 (1.618 times extension of 109.49-124.10 measuring from 114.85), bring correction later.

Recommendation: Sell at 133.50 for 131.50 with stop below 134.50.

To re-cap the corrective upmove from the record low of 88.93 (18 Oct 2000), the wave A from there is subdivided as: 1:88.93-113.72, 2:99.88 (1 Jun 2001), 3:140.91 (30 May 2003), 4:124.17 (10 Nov 2003) and 5 ended at record high of 169.97 (21 Jul 2008). The brief but sharp selloff to 112.08 is viewed as a-b-c x a-b-c wave (A) of B. The subsequent rebound to 139.26 is (B) of B and (C) of (B) has possibly ended at 94.12 and in any case price should stay well above previous chart support at 88.93, bring rally in larger degree wave C towards 150.00.

AUD/USD Descending Triangle

AUD/USD is ready to go even lower showing that downside pressures are still lively. Hourly resistance is given at a distance at 0.7897 (13/10/2017 high). Expected to show renewed pressures towards key support at 0.7571 (05/07/2017 low).

In the long-term, the trend is turning positive. Key supports stands at 0.6009 (31/10/2008 low) . A break of the key resistance at 0.8164 (14/05/2015 high) is needed to invalidate our long-term bearish view.

USD/CAD Selling Pressures Continues

USD/CAD continues to decline, but at a slower pace, after the set-up of a resistance at 1.2917 (27/10/2017 low). Hourly support lies at 1.2640 (25/10/2017 low). Expected to show continued short-term bearish pressures.

In the longer term, the pair has broken longterm support that can be found at 1.2461 (16/03/2015 low). Strong resistance is given at 1.4690 (22/01/2016 high). The pair is likely to head further lower.

USD/CHF Increasing Selling Pressures

USD/CHF is consolidating lower. Yet, the technical structure is still bullish. Yet, the pair has failed to hold consistently above the parity. The technical structure suggests growing selling pressures.

In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015.

USD/JPY Ready To Bounce Back

USD/JPY is riding uptrend channel below former resistance at 114.49 (11/07/2017 high). Hourly support is given at 113.09 (09/10/2017 low). Strong support is located at a distance at 111.12 (20/09/2017 low).

We favor a long-term bearish bias. Support is now given at 99.02 (10/08/2013 low). A gradual rise towards the major resistance at 125.86 (05/06/2015 high) seems unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

GBP/USD Volatility Declines

GBP/USD is still holding below 1.32. Support is given at 1.3027 (06/10/2017 low). Resistance area is given around 1.3200. Expected to show further increase.

The long-term technical pattern is reversing. The Brexit vote had paved the way for further decline. Long-term support can be found at 1.1841 (07/10/2017 low). Long-term resistance given around 1.35 is at stake and indicates a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

EUR/USD Medium-Term Momentum Remains Bearish

EUR/USD is still biased to the downside despite the current rebound. Hourly resistance is located at 1.1690 (03/11/2017 high). Hourly support is given at 1.1554 (07/11/2017 low). Expected to show some short-term consolidation.

In the longer term, the momentum is now turning largely positive. We favour a continued bullish bias. Key resistance is holding at 1.2252 (25/12/2014 high) while strong support lies at 1.0341 (03/01/2017 low).

Market Update – European Session: Awaiting To See If Progress Is Being Made In Monthly Brexit Talks

Notes/Observations

Awaiting Barnier and Davis comments following their 6th monthly round of Brexit negotiations.Earlier hints no no major progress being made

PM May was prepared to increase its offer for the financial settlement of Brexit divorce from the current £20B offer

Evolution of inflation remains key for the judgement of global risk appetite

Overnight

Asia:

Bank of Japan (BOJ) Summary of Opinions at Oct. 30-31th Meeting: should maintain easing policies until the inflation mandated is achieved. It did caution that additional easing could cause more side-effects than positive effects.

RBA Quarterly statement lowered its inflation forecasts through 2019 and now saw sub 2% core inflation until mid-2019: GDP growth forecasts little changed. Held rates steady to provide appropriate economic support and saw 3.25% GDP growth by end 2019.

China to remove foreign ownership limit in domestic banks; raises the foreign stake ceiling in brokerages to 51% v 49% prior (in-line with speculation)

Europe:

EU official: there has not been a breakthrough in talks on Brexit bill; negotiators still in talks over EU citizens' rights

UK PM May said to reiterate her commitment to securing 2-year Brexit implementation period when she meets with European business organization

SNB's Jordan: reiterated negative interest rates are still necessary and had room to maneuver on rates if necessary

Spain govt said to be pushing for the release of 8 former Catalan govt officials and expects them to be freed in time to campaign in December's elections

Americas:

House Ways & Means Committee approves its version of the tax reform bill (Vote was 24-16 along party lines). House Majority Leader McCarthy noted that the full House to vote on tax bill on House floor next week

White House: President Trump will not have formal meeting with Russia President Putin in Vietnam on sidelines of APEC Summit due to scheduling conflicts

Fed's Williams (moderate, non-voter): Rate rise in December makes sense. Penciling in 3 further hikes in 2018 and expected US interest rate to return to a normal level of about 2.5%

Economic Data

(DK) Denmark Oct CPI M/M: 0.1% v 0.1%e; Y/Y: 1.5% v 1.5%e

(DK) Denmark Oct CPI EU Harmonized M/M: 0.1% v 0.1% prior; Y/Y: 1.4% v 1.4%e

(NO) Norway Oct CPI M/M: 0.1% v 0.3%e; Y/Y: 1.2% v 1.4%e

(NO) Norway Oct CPI Underlying M/M: 0.3% v 0.2%e; Y/Y: 1.1% v 1.0%e

(RO) Romania Oct CPI M/M: 1.3% v 0.5% prior, Y/Y: 2.6% v 2.2%e

(FR) France Sept Industrial Production M/M: 0.6% v 0.5%e; Y/Y: 3.2% v 3.0%e

(FR) France Sept Manufacturing Production M/M: 0.4% v 0.8%e; Y/Y: 3.1% v 3.4%e

(FR) France Q3 Preliminary Private Sector Payrolls Q/Q: 0.2% v 0.3%e; Wages Q/Q: 0.3% v 0.3%e

(HK) Hong Kong Q3 GDP Q/Q: 0.5% v 0.6%e; Y/Y: 3.6% v 3.5%e

(UK) Sept Industrial Production M/M: 0.7% v 0.3%e; Y/Y: 2.5% v 1.4%e

(UK) Sept Manufacturing Production M/M: 0.7% v 0.3%e; Y/Y: 2.7% v 2.4%e

(UK) Sept Visible Trade Balance: -£11.3B v -£12.8Be, Overall Trade Balance: -£2.8B v -£4.3Be, Trade Balance Non EU: -£3.0B v -£5.0Be

Fixed Income Issuance:

(IN) India sold total INR150B vs. INR150B indicated in 2022, 2031, 2033 and 2046 bonds

(IT) Italy Debt Agency (Tesoro) sold €5.5B vs. €5.5B indicated in 12-month Bills; Avg yield: -0.395% v -0.344% prior; Bid-to-cover: 2.46x v 1.96x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 -0.3% at 388.8, FTSE -0.2% at 7468, DAX -0.3% at 13138, CAC-40 -0.4% at 5387, IBEX-35 -0.6% at 10083, FTSE MIB -0.3% at 22571, SMI -0.5% at 9133, S&P 500 Futures -0.5%]

Market Focal Points/Key Themes: European Indices trade weaker across the board gradually edging lower during the session, as continued profit taking and worries over the US Tax overhaul weigh. After the close yesterday Allianz reported in line results and affirmed there outlook despite the recent natural disasters, while in the materials space ArcelorMittal reported results which beat on the top and bottom line. Leonardo trading in Italy is one of the leading decliners after cutting their outlook. In the luxury space Richement reported solid results with double digit gains across China, Hong Kong and the UK, however a cautious outlook weighs on the stock. Looking ahead notable earners include retailer JC Penny.

Equities

Consumer discretionary [Richemont [CFR.CH] -4.3% (Earnings), Capita [CPI.UK] -1.8% (Capita Financial Managers to pay up to £66M as part of settlement related to Connaught), Stroeer Media [SAX.DE] +2.0% (Earnings)] - Materials: [ArcelorMittal [MT.NL] +2.8% (Earnings)]

Industrials: [ Tecnicas Reunidas [TRE.ES] -14% (Earnings) , Leonardo-Finmeccanica [LDO.IT] -19% (Earnings, cuts outlook), Vallourec [VK.FR] -3% (Earnings)]

Financials: [Allianz [ALV.DE] +0.8% (Earnings)] - Healthcare:[Getinge [GETIB.SE] -3.2% (Strategy update)]

Real Estate: [ GallifordTry [GFRD.UK] +1.4% (trading update)]

Speakers

PM May said to be prepared to increase its offer for the financial settlement of Brexit divorce from £20B

ECB's Nowotny (Austria): ECB should end QE after Sept if economy allows; ECB guidance does not allow a rate hike before 2019. Agrees with Bundesbank Gov Weidmann on necessity for QE end-date. He saw no ECB rate hike before 2019

ECB's Stournaras (Greece): Greek banks have shown progress in dealing with non-performing loans (NPLs). Unemployment, public debt and NPLs were challenges for the Greek economy

Czech Central Bank Nov Minutes: More appropriate to raise rates gradually from a financial stability point of view. Sharp one-off increase in interest rates could lead the CZK currency (Krone) to sharp appreciation (as ECB extended its QE bond buying program)

Poland EU Affairs Min Szymansk: Brexit deal will be reached at the very last minute. Could be march but it would be better in December

China President Xi: Studying the option of opening free-trade ports

President Trump: Expressed strong desire to conduct trade on a fair basis; will make bilateral trade deals with any APEC nation. Spoke openly and directly with China President Xi regarding trade deficits and would no longer tolerate chronic trade abuses. Those countries that played by the rules will be the closest economic partners

Venezuela and Russia to sign debt agreement of possible installments over 10 years on Nov 15th

Currencies

USD consolidated its soft tone from the following sessions as the US tax reform had hit hurdles. The greenback was poised for its biggest weekly drop in 4 weeks on tax concerns. US policy makers delayed the corporate tax cut by one year, set a higher "pass-through" rate for small business, and completely repealing the State and Local Tax deduction.

GBP was steady ahead of the Barnier and Davisd press conference following the 6th monthly round of Brexit negotiations. Reports circulated that PM May was prepared to increase its offer for the financial settlement of Brexit divorce from the current £20B offer

Fixed Income

Bund futures trade at 162.44 down 32 ticks, as Wednesday's mid-session reversal sees price poised to close at the lows of the week. Support lies at 162.00, followed by 161.50. Resistance stands initially at 163.51, followed by 164.25.

Gilt futures trade at 124.78 down 45 ticks following the drop by Treasuries. Continued upside eyeing 125.75 then 126.47. Downside targets include 124.24 then 123.74.

Friday's liquidity report showed Thursday's excess liquidity was little changed at €1.873T and use of the marginal lending facility climbed to €532M from €515M

Corporate issuance saw for the week ending Nov 8th Lipper fund flows reported IG fund net inflows of $4.7B and High yield funds reported net outflows of $622M.

Looking Ahead

(MX) Mexico Oct Nominal Wages: No est v 5.1% prior

05:30 (CL) Chile Central Bank Economist Survey

05:30 (ZA) South Africa to sell combined ZAR800M in I/L bonds

06:00 (BR) Brazil Oct IBGE Inflation IPCA M/M: 0.5%e v 0.2% prior; Y/Y: 2.8%e v 2.5% prior

06:00 (UK) DMO to sell combined £3.5B in 1-month, 3-month and 6-month Bills (£0.5B, £2.0B and £2.0B)

06:30 (IN) India Weekly Forex Reserves

06:30 (UK) EU/UK joint press conference following current round of monthly Brexit negotiations

06:30 (IS) Iceland to sell Bonds - 06:45 (US) Daily Libor Fixing

07:00 (IN) India Sept Industrial Production Y/Y: 3.6%e v 4.3% prior

07:30 (LX) ECB's Mersch (Luxembourg)

08:00 (RU) Russia Sept Trade Balance: $8.8Be v $6.6B prior; Exports: $30.0Be v $29.0B prior; Imports: $20.5Be v $22.4B prior

08:00 (UK) Oct NIESR GDP Estimate: No est v 0.4% prior

08:00 (ES) Spain Debt Agency (Tesoro) announces upcoming issuance

08:00 (IN) India announces upcoming Bill auction (held on Wed)

08:05 (UK) Baltic Dry Bulk Index

09:00 (MX) Mexico Sept Industrial Production M/M: -0.6%e v +0.3% prior; Y/Y: -0.8%e v -0.5% prior, Manufacturing Production Y/Y: 2.8%e v 3.3% prior

10:00 (US) Nov Preliminary University of Michigan Confidence: 100.9e v 100.7 prior

11:00 (EU) Potential sovereign ratings after EU close (Egypt and Ukraine Sovereign Debt to be rated by S&P; Greece Sovereign Debt to be rated by DBRS and Hungary Sovereign Debt to be rated by Fitch

(UR) Ukraine Sovereign Debt to be rated by S&P

13:00 (US) Weekly Baker Hughes Rig Count data

14:00 (CO) Colombia Central Bank Oct Minutes

GBPJPY Maintains Neutral Bias With Near-Term Risk Titled To The Downside

GBPJPY has been neutral since peaking at 152.85 in September, consolidating in a broad range above the mid-point of the rise from 141.34 to 152.85.

Near-term risk is tilted to the downside as the market has dropped below the 200-moving average on the 4-hour chart. Immediate support is at 148.40, which is the 38.2% Fibonacci retracement level which has been tested a few times. An extension lower would bring the 50% Fibonacci into view at a psychological level of 147.00. Below this, the 61.8% Fibonacci at 145.70 is a critical level, which if broken would shift the bias to bearish to target the 141.34 low.

To the upside, resistance levels exist at the 200-MA at 149.45, at 150.05 (23.6% Fibonacci) and then at the key 152.00 level. From here, the 152.85 peak comes into sight and rising above this would confirm the resumption of the uptrend from 141.34.

In the near term, the bias is neutral to bearish but since momentum is weak (neutral RSI), this points to more consolidation during the next few trading sessions.