Sample Category Title

Trade Idea Wrap-up: USD/CHF – Stand aside

USD/CHF - 0.9944

Most recent candlesticks pattern : N/A

Trend : Sideways

Tenkan-Sen level : 0.9945

Kijun-Sen level : 0.9959

Ichimoku cloud top : 0.9981

Ichimoku cloud bottom : 0.9981

New strategy :

Stand aside

Position : -

Target : -

Stop : -

The greenback met renewed selling interest just below resistance at 1.0020, dampening our bullishness and further choppy trading below recent high at 1.0038 would take place and weakness to 0.9920-22 (38.2% Fibonacci retracement of 0.9737-1.0038) is likely, however, reckon downside would be limited to 0.9885-90 (50% Fibonacci retracement) and support at 0.9869 should remain intact, bring another upmove later.

As near term outlook is mixed, would be prudent to stand aside in the meantime. Above 0.9980 would bring rebound to 1.0000, then 1.0020 but only break of said resistance at 1.0038 would confirm the rise from 0.9421 low has resumed and extend further gain to 1.0050-55, then towards 1.0075-80 but price should falter below 1.0100 chart resistance.

Week Ahead – Inflation, Jobs and Retail Sales in Focus; Japanese GDP also Eyed

Economic data will move to the forefront next week as the focus moves away from central bank meetings to price, employment and consumer spending indicators. Canada, the Eurozone, the UK and the US all release CPI numbers. Jobs reports are due from Australia and the UK, and retail sales figures will be published in China, the UK and the US. GDP data will also attract attention as investors get the first glimpse of third quarter economic performance in Japan.

Australian wages to remain subdued

Like in most advanced economies, a tightening labour market has not translated to higher wages in Australia, raising concerns about the negative impact of household debt rising faster than incomes. The lagging wage growth has dampened consumer spending, which, along with the weak outlook for inflation, has pushed back expectations about the timing of a rate hike by the RBA, weighing on the Australian dollar. Wage data are due on Wednesday and will be followed by employment numbers on Thursday.

Canadian inflation eyed

The Bank of Canada's governor, Stephen Poloz, reiterated this week that the Bank's next move will be data dependent. While recent Canadian data has pointed to ongoing strength in jobs growth and consumer spending, inflation isn't picking up as quickly as had been anticipated and economic growth in the second half of the year is heading for a marked slowdown compared to the first half. This has led the BoC to take a more cautious approach on further rate hikes over the coming months. October CPI readings on Friday will therefore be watched carefully for any signs that inflation is accelerating. A stronger-than-expected figure could help the Canadian dollar move further away from its recent 3½-month low versus its US counterpart.

Investment in China likely slowed further in October

Fixed asset investment in China hit a 17-year low in September and is expected to slow further in the year-to-date to October, to 7.4% on an annual basis. The data due on Tuesday will be released alongside industrial output and retail sales figures. Although recent indicators suggest the Chinese economy will see only a mild slowdown in the second half of the year, a weak batch of data next week could nevertheless dampen risk sentiment.

Japan expected to post longest growth streak since early 2000's in Q3

In the second quarter, Japan recorded its longest stretch of uninterrupted growth in 11 years. If on Tuesday, GDP data shows another quarter of positive growth for the three months that ended in September, Japan would have posted its seventh straight quarter of growth, making it its longest streak of expansion since the turn of the century. The achievement may lift the booming Nikkei 225 index to fresh 25-year highs but is unlikely to see much of a reaction in currency markets as the Bank of Japan is nowhere near in scaling back its stimulus program.

Eurozone economy shines but inflation remains elusive

The second estimate of GDP data on Tuesday is expected to confirm that the Eurozone economy grew by 0.6% quarter-on-quarter in the September quarter. The European Commission this week revised up its projection of growth in the euro area in 2017 from 1.7% to 2.2%, but revised down its forecast for inflation from 1.6% to 1.5%. The final reading of October inflation is also due next week, on Thursday. CPI is expected to have risen 1.4% on an annual basis last month, unchanged from the preliminary figure but down on the prior month's 1.5% rate. Other data to watch next week include the ZEW economic sentiment index out of Germany and Eurozone industrial output numbers, both on Tuesday. With the ECB recently signalling that it does not expect to start raising rates by late 2018 at the earliest, the euro may struggle to see much of a response from the data.

Big week for UK data

Major UK indicators next week face the risk of getting overshadowed by growing political concerns, as Brexit talks conclude their sixth round without much progress and May's government loses its second key minister in a week. However, with many analysts taking the view that the Bank of England's 25bps rate hike earlier this month was a one-and-done move, upside surprise to UK data could lift sterling. The first item on the UK calendar is inflation on Tuesday. It will be followed by unemployment and wage figures on Wednesday and retail sales numbers on Thursday. Inflation is expected to have hit 3.1% in October. A figure above 3% would oblige the BoE Governor Mark Carney to write to the government to explain why it has overshot its upper target. The focus in the employment report will be average earnings as continued weakness in pay growth would signal no end in sight to the income squeeze for consumers, while another dire month for retail sales in October would point to a poor start to the third quarter. Retail sales are forecast to post their first year-on-year decline since 2013 in October.

Busier calendar for the US

After a quiet week, the US looks set for a packed calendar in the coming seven days. However, with a December rate hike already fully priced in, the data may not cause much excitement in the markets, especially as the immediate focus is on the tax plan's passage in Congress. However, more robust numbers could provide the dollar some support should the Senate and the House fail to work out their differences over the tax reforms. The first key data out of the US next week is CPI on Wednesday. Annual inflation is forecast to ease to 2.0% in October, with the core rate holding steady, at 1.7%. Retail sales are also due on Wednesday and are expected to show sales moderating in October after a 1.6% surge in September. Other US data likely to attract attention next week are October producer prices on Tuesday, the Empire State manufacturing index on Wednesday, industrial output and the Philly Fed manufacturing index on Thursday, and building permits and housing starts on Friday.

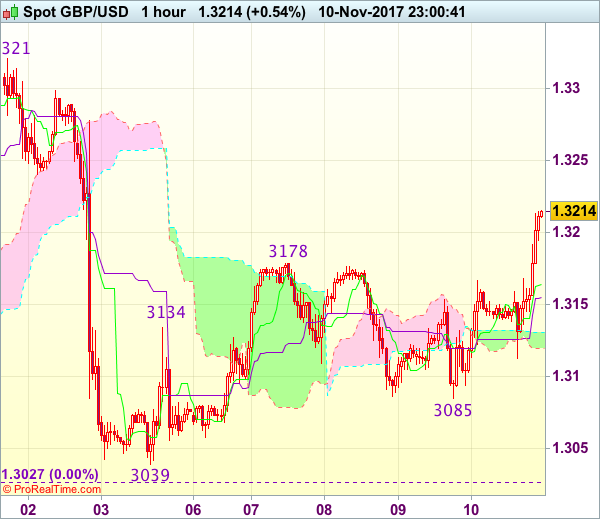

Trade Idea Wrap-up: GBP/USD – Buy at 1.3170

GBP/USD - 1.3215

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.3165

Kijun-Sen level : 1.3156

Ichimoku cloud top : 1.3131

Ichimoku cloud bottom : 1.3119

Original strategy :

Sold at 1.3140, stopped at 1.3175

Position : - Short at 1.3140

Target : -

Stop : - 1.3175

New strategy :

Buy at 1.3170, Target: 1.3270, Stop: 1.3135

Position : -

Target : -

Stop : -

Despite intra-day brief retreat to 1.3112, as cable found renewed buying interest there and has rallied above resistance at 1.3178, signaling the fall from 1.3321 has ended at 1.3039 earlier and mild upside bias is seen for the erratic rise from there to extend further gain to 1.3250, then 1.3275-80, however, near term overbought condition should limit upside and price should falter well below resistance at 1.3321, bring retreat later.

In view of this, we are looking to buy cable on pullback as 1.3165-70 should limit downside. Below 1.3135-40 would defer and risk test of said support at 1.3112 but only break of support at 1.3085 would revive bearishness and signal the rebound from 1.3039 has ended, bring weakness towards 1.3050-55 first.

Weekly Focus: Global Activity Indicators in Focus

Market Movers ahead

- We are heading for another relatively quiet week, with no major movers in the US or Europe.

- In the US, we expect inflation pressure to have remained muted in October with the headline CPI inflation rate falling to 1.9% y/y from 2.2% in September, while the core inflation rate will remain at 1.7%.

- In the euro area, focus will be on the German GDP estimate for Q3, where we expect another solid GDP figure with 0.6% q/q growth, as PMI in August and September remained at a high level.

- In the UK, we expect the CPI figures for October to show a small uptick, driven mainly by lingering effects of the weak GBP.

- In Sweden, October inflation is in focus this week, where our CPIF forecast is spot on the Riksbank's, i.e. at 1.9 % y/y.

- In Denmark and Norway, the Q3 GDP releases are likely to show q/q growth rates of 0.5% and 0.7%, respectively.

Global macro and market themes

- Emerging markets have seen a strong run this year.

- Global and domestic factors should continue to be mildly supportive for EM near term.

- However, a slowdown in China in coming months is a risk as are large unfinanced tax cuts in the US, if pushing up US yields.

- The recent surge in oil prices is being driven mostly by geopolitical concerns due to tensions in the Middle East.

- The longer-term growth outlooks in EM differ widely. India and the rest of EMs in South East Asia boast strong growth potential but LATAM countries and Russia have a more muted longer-term outlook.

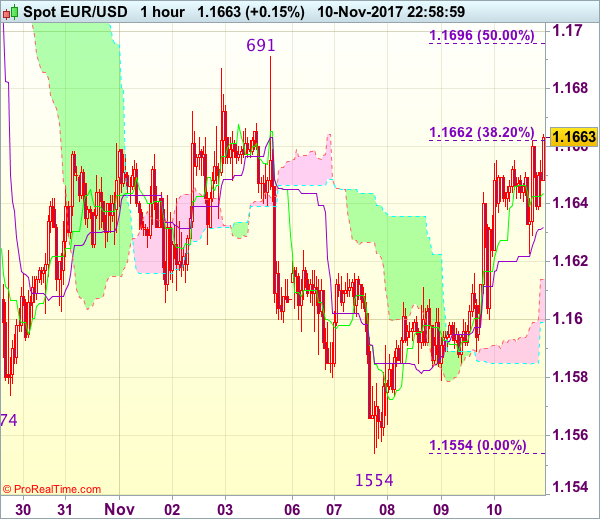

Trade Idea Wrap-up: EUR/USD – Buy at 1.1600

EUR/USD - 1.1667

Most recent candlesticks pattern : N/A

Trend : Down

Tenkan-Sen level : 1.1648

Kijun-Sen level : 1.1636

Ichimoku cloud top : 1.1614

Ichimoku cloud bottom : 1.1599

New strategy :

Buy at 1.1600, Target: 1.1700, Stop: 1.1565

Position : -

Target : -

Stop : -

Current rally signals a temporary low has been made at 1.1554 earlier this week and consolidation with upside bias is seen for retracement of recent decline, hence further gain to 1.1691-96 (previous resistance and 50% Fibonacci retracement of 1.1837-1.1554) is likely, however, reckon upside would be limited to 1.1725-29 (previous support now resistance and 61.8% Fibonacci retracement), bring retreat later.

In view of this, we are looking to buy euro on pullback as 1.1600 should limit downside and bring another rebound later. Below 1.1625-30 would bring weakness to 1.1600, however, downside should be limited and bring another rebound. Below 1.1575-80 would defer and risk a retest of this week’s low at 1.1554 first.

UK Data and Cautious Brexit Hope Block Sterling Decline

- European equities drifted cautiously lower early in the session, but trading turned much calmer after yesterday's uptick in volatility. An intraday attempt to return into positive territory failed. Most major indices show losses of about 0.25%. US equities also started the session with marginal losses.

- Donald Trump told nations of the "Indo-Pacific" region that the US would no longer tolerate "chronic trade abuses", as he urged them to enter fair and reciprocal economic relationships with America.

- Theresa May is ready to increase Britain's offer to the EU over the Brexit divorce bill, after signs that the hard Eurosceptics in her party will tolerate paying more money to break the deadlock in negotiations. Mrs May has said that Britain "will honour commitments we have made during the period of our membership" and her team are working on different scenarios that would see her considerably increase the €20bn she has already put on the table.

- EU chief negotiator Barnier raised the prospect of Brexit talks failing to reach a breakthrough by year-end, saying the UK has two weeks to come up with a better offer on the financial settlement.

- The ECB's commitment to keep interest rates low until after asset purchases end doesn't leave policy makers room to raise borrowing costs next year, Governing Council member Nowotny said in a radio interview. He added that the ECB should have signalled its intention to end asset buying.

- UK production rose a larger-than-forecast 0.7% in September, with output increasing across most manufacturing sectors, the ONS said. But construction fell the most in 18 months and a narrowing of the trade deficit was not enough to prevent the shortfall widening in the third quarter.

- Inflation in Norway came in below forecasts for a second month in a row in October, falling to its lowest level since November 2012 (1.2% Y/Y from 1.6% Y/Y vs 1.4% Y/Y forecast). Cheaper food imports continued to be the main cause of the weak price growth, despite the relatively weak krone.

Rates

Quiet trading session on core bond markets

Global core bonds lost some ground today. The move already occurred in Asian dealings (US Note future) and the European opening (Bund). In the US, it was rather strange given the growing stand-off between US House and Senate Republicans on tax reforms. After the European opening, core bond trading occurred in a narrow sideways range. Yesterday's sell-off in European stock markets and the Bund proved to be a one-off for now. The eco calendar was again uneventful. ECB Nowotny joined the German-Franco view that the ECB should have given an intent to end its QE-program rather than keeping it open-ended. A rate hike in 2018 is excluded with the current monetary policy stance, he added.

At the time of writing, the German yield curve bear steepens with yields 0.5 bps (2-yr) to 2.9 bps (10-yr) higher. The US yield curve shifts in similar fashion with yields 1.9 bps (2-yr) to 4.5 bps (30-yr) higher. On intra-EMU bond markets, 10-yr yield spreads narrow up to 3 bps.

Currencies

EUR/USD drifts marginally higher

Trading on global markets calmed down after yesterday's uptick in volatility. There were again only second tier eco data. There was also little guidance from interest rate markets or equities to guide trading in the major USD cross rates. EUR/USD held a tight range in the mid 1.16 area. USD/JPY hovered close to the 113.50 pivot. The dollar fails to regain yesterday's losses.

Overnight, Asian equities mostly showed modest losses. China outperformed. Japan underperformed again. The yen maintained yesterday's gain, but the Japanese currency again didn't profit from the additional equity losses overnight. EUR/USD held near yesterday's closing level in the 1.1650 area. So, the dollar remained slightly in the defensive.

European equity investors remained cautious after yesterday's setback, but the pace of further losses was very modest. The Bund held an extremely tight sideways range. Interest rate differentials between the US and Europe re-widened slight after yesterday's narrowing. This prevented further USD losses, but there was no sign at all of a meaningful comeback of the US currency. A downside attempt of EUR/USD early this morning had no momentum and EUR/USD settled in a tight range in the mid 1.1650 area. We look out for today's close of in EUR/USD. A close north of the 1.1690 ST range top would be slightly disappointing for USD bulls. However, we don't draw any firm conclusions yet. Next week, the US CPI and retail sales have the potential to give more meaningful guidance for USD trading. USD/JPY trades currently around 113.45. The pair failed to break beyond the 114.49/73 topside barrier. At the same time, the damage for the US currency could have been bigger given the easing in global risk sentiment.

UK data and cautious Brexit hope block sterling decline

Sterling traders saw the glass half empty earlier this week. Political uncertainty and the lack of progress in the Brexit talks were a good reason to reduce sterling long exposure. Today, the sterling glass was again half full. The UK trade deficit narrowed more than expected, supported by good export growth. At the same time, UK September production data were very strong (0.7% M/M vs 0.3% expected). Today's data don't change the overall picture on the UK economy, but they give some counterweight to other disappointing eco data of late(e.g. from the consumer sector). EU's Barnier repeated after this week's Brexit negotiations that more progress is still needed on the divorce issues. However, markets concluded that it is still possible to get the green light for negotiations on the future relationship after the December EU summit. There were 'rumours' that UK PM May would be prepared to raise the amount to UK is prepared to pay when leaving EU. EUR/GBP declined from late in the morning session and trades currently in the 0.8832 area (from around 0.8870/75 early this morning). Cable nears the 1.32 barrier. In a broader perspective, sterling stays in a ST consolidation modus, both against the euro and the dollar.

Gold Spot Shows Rounded Bottom for a Possible Continuation

Given that European, US and Japanese Equities markets have experienced some risk-off as most markets are at multi-year and all-time highs; we have seen some buying of Gold, the safe-haven precious metals recently. At this point the Gold spot shows a rounded bottom and we might see a spike from POC zone and a continuation above W H5. The POC zone ( W H4, EMA89, atr pivot) should spike the price up on a subsequent retest towards the W H5 1288.35. 4h close above the pivot should aim for M H4 - 1295.80 and possibly 1306.05 where a u-turn on rounded bottom will be complete.. Only a strong momentum above 1310.00 should follow up with 1.1316 target.

For this scenario to succeed the price must remain above the W L3 1264.52 else a break below will probably make a bearish move towards W L5 -1250.94. So at this point buying the dips looks like a possible way to go.

- H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

- W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

- D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

- D L3 - Daily Camarilla Pivot (Daily Support)

- D L4 - Daily H4 Camarilla (Very Strong Daily Support)

- PPR - Progressive Polynomial Channel

- POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

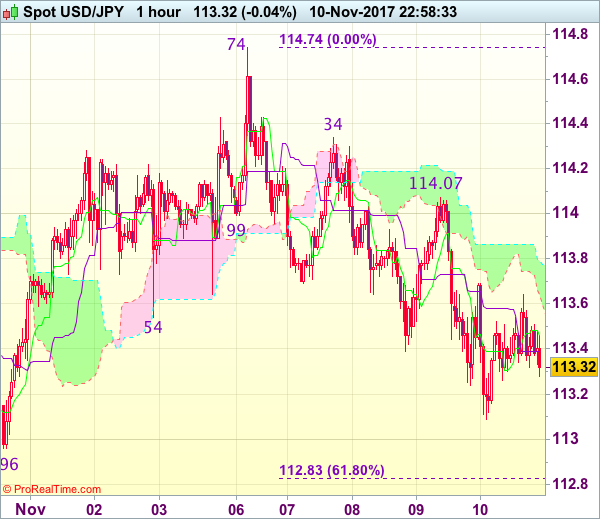

Trade Idea Wrap-up: USD/JPY – Hold short entered at 114.00

USD/JPY - 113.32

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 113.39

Kijun-Sen level : 113.46

Ichimoku cloud top : 113.79

Ichimoku cloud bottom : 113.64

Original strategy :

Sold at 114.00, Target: 113.00, Stop: 113.70

Position : - Short at 114.00

Target : - 113.00

Stop : - 113.70

New strategy :

Hold short entered at 114.00, Target: 113.00, Stop: 113.70

Position : - Short at 114.00

Target : - 113.00

Stop : - 113.70

As the greenback recovered after falling to 113.09 yesterday, suggesting consolidation would be seen, however, reckon upside would be limited to 113.65-70 and bring another decline later, below said support at 113.09 would extend the fall from 114.74 top to previous support at 112.96 but break there is needed to add credence to this view, bring further subsequent selloff to 112.60 but support at 112.30 should hold from here due to near term oversold condition.

In view of this, we are holding on to our short position entered at 114.00. Only above resistance at 114.07 would abort and signal the retreat from 114.74 has ended instead, bring a stronger rebound to 114.34, then retest of this level, above there would revive bullishness and extend recent rise from 107.32 to 115.00.

Trade Idea: EUR/GBP – Sell at 0.8890

EUR/GBP - 0.8835

Original strategy :

Sell at 0.8890, Target: 0.8770, Stop: 0.8930

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.8890, Target: 0.8770, Stop: 0.8930

Position : -

Target : -

Stop : -

Although the single currency retreated after meeting resistance at 0.8877, break of indicated support at 0.8791 is needed to signal early rebound from 0.8733 (last week’s low) has ended at 0.8939, bring further fall to 0.8750-55, then retest of 0.8733, a drop below there would extend the fall from 0.9033 to 0.8700 first.

In view of this, we are still looking to sell euro on subsequent recovery as 0.8890-00 should limit upside. Only above 0.8939 resistance would abort and extend the rise from 0.8733 to resistance at 0.8957, however, break of 0.8976 resistance is needed to signal the fall from 0.9033 has ended instead, bring further gain to 0.9000, then retest of 0.9033 later.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.

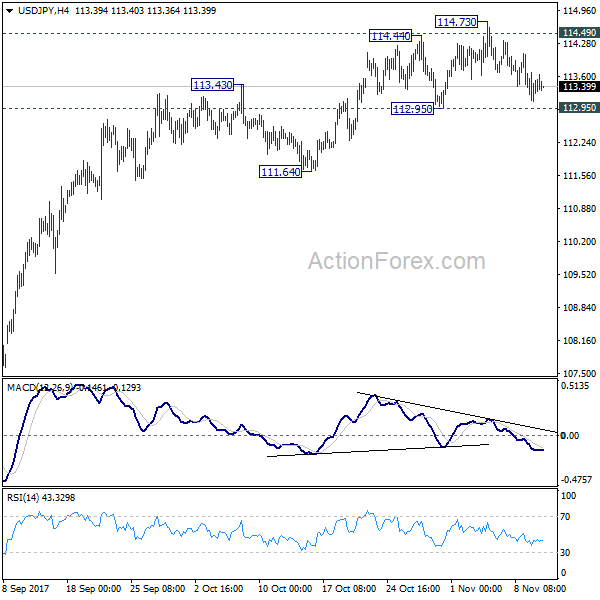

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 113.01; (P) 113.53; (R1) 113.99; More...

Intraday bias in USD/JPY remains neutral at this point. As it's still holding on to 112.95 support, near term outlook remains bullish. On the upside, sustained break of 114.49 key resistance will pave the way to retest 118.65 high. However, break of 112.95 support will now indicate rejection from 114.49 and turn bias to the downside for 111.64 support and below.

In the bigger picture, medium term rise from 98.97 (2016 low) is not completed yet. It should resume after corrective fall from 118.65 completes. Break of 114.49 resistance will likely resume the rise to 61.8% projection of 98.97 to 118.65 from 107.31 at 119.47 first. Firm break there will pave the way to 100% projection at 126.99. This will be the key level to decide whether long term up trend is resuming.