Sample Category Title

Tax Twists

Markets were pushed and pulled on leaks and reports from tax plans Thursday in a clear sign of what's at stake. The Swiss franc was the top performer while the New Zealand dollar lagged. New RBA forecasts are due up later.

Markets soured on signs the Senate would ask for a one-year delay in cutting corporate taxes to 20% on Thursday but the mood had improved by late in the day on signs the legislation could pass.

There is a balance between how favourable the plan is for business and the economy versus the likelihood of success. The initial reports of a one-year delay in the corporate rate sent the S&P 500 down as much as 26 points and USD/JPY as low as 113.10 – the worst in a week.

Signs of support from influential Senators late helped to boost USD/JPY back to 113.50 and the S&P 500 closed down 10 points.

At the same time, other markets were pulled in different directions. There was a sizeable slump in Eurozone sovereign bonds and that pushed 10-year yields up roughly 5 bps throughout the continent and narrow spreads with Treasuries. That gave the euro a half-cent boost.

In Japan, we will be watching the Nikkei very closely in the day ahead. It surged to the highest since 1992 on Thursday before reversing to close slightly lower. The selling continued in the futures market in a nearly 4% drop from the peak.

Aside from that, Australian dollar risks will be high at 0030 GMT when the RBA will update its forecasts on growth and inflation in the Statement on Monetary Policy.

Pound Inches Higher, Markets Eye British Mfg. Production

The British has ticked higher in the Thursday session. In North American trade, GBP/USD is trading at 1.3131, up 0.11% on the day. On the release front, there are no British indicators. In the US, unemployment claims climbed to 239 thousand, missing the estimate of 232 thousand. On Friday, the UK releases Manufacturing Production and the US publishes Preliminary UoM Consumer Sentiment.

The Brexit talks are moving slowly, and one major sticking point is the size of Britain's divorce bill. The European Union is demanding EUR 60 billion, while Britain has countered with an offer for EUR 20 billion. Britain wants to move on to discussing a trade deal with the continent, but the Europeans are insisting on more progress on the divorce bill as well as on other non-trade issues. If the sides still remain deadlocked in December without no deal in sight, hardliners on both sides could derail the talks completely, which would send shivers up the spines of investors and hurt the British pound. The Europeans are also wary about the ability of Theresa May to deliver the goods, given her continuing struggles at home. Two ministers have been forced to resign from May's cabinet in recent weeks, and she hasn't been able to present a coherent Brexit policy to the Europeans or to the voters at home.

BoE Governor Mark Carney hasn't shied away from public statements on Brexit, much to the angst of many lawmakers. Carney weighed in again on Brexit in a television interview on the weekend. Carney expressed concern at the lack of uncertainty over a final deal with the European Union, saying that the economy "should really be booming, but it's just growing." According to Carney, the BoE wants a scenario with a smooth transition out of the EU, with a trade deal that was somewhere in between full membership in a single market and a 'no deal' outcome. The BoE cut rates in August 2016, just after the Brexit vote. This reflected the Bank's fear of a sharp downturn in the British economy, which did not occur. The BoE raised rates last week (for the first time since 2007), in what was widely viewed as a corrective measure to the August 2016 rate cut.

Dollar Index Trades in Extended Consolidation; US Tax Reforms Plan Seen as Catalyst for Fresh S/T Direction

The dollar index stands at the back foot on Thursday and probes below 10SMA (currently at $94.63) which turned into sideways mode after tracking the ascend of past two weeks.

Firm break below 10SMA pivot would trigger further easing and expose key supports in $94.10 zone, which previously acted as key resistances (former tops of 16 Aug / 06 Oct / Fibo 38.2% of $92.57/$95.05 upleg.

The index is in short-term consolidative phase between $94.10 and $95.05, as broader bulls are taking a breather before resuming.

However, the dollar requires a catalyst to continue two-month uptrend from $90.97 which was so far capped by falling weekly Kijun-sen and Fibo 61.8% of $94.50/$90.97 downleg.

Focus is on US tax reforms plan, implementation of which has been delayed, with firmer signs of progress expected to boost the greenback.

Alternatively, further delay in implementation of the plan would risk deeper correction which could be sparked on firm break below $94.10 pivot.

Res: 94.85; 95.05; 95.27; 95.94

Sup: 94.41; 94.10; 93.81; 93.63

Tax Reform Uncertainty Continues Weighing on the Dollar; Brexit Talks Resume

In another mostly quiet day in terms of data releases, forex market participants' attention remained firmly on the US tax reform front. Jobless claims and wholesale inventory data out of the US did generate some interest, though market reaction following the releases was subdued. Meanwhile, Brexit negotiations are resuming today.

At 1526 GMT the dollar index traded 0.25% down on the day at 94.63. Once again, the prospect of a delay in the delivery of tax cuts or reforms offering less of a benefit to US corporations than initially expected, has been weighing on the greenback. A Senate tax-cut bill that differs from the one in the House of Representatives is expected to be unveiled today, further perplexing the situation in case the two versions stand far apart. According to the Senate Finance Committee, today's release would constitute a "conceptual mark" rather than the delivery of a detailed legislative text.

Dollar/yen was 0.2% down on the day, further distancing itself from Monday's eight-month high of 114.72. At its lowest today, the pair recorded a nine-day low of 113.22. Euro/dollar last traded up by 0.3% at 1.1630. The pair started the day below the 1.16 handle and rose as high as 1.1644, a six-day peak.

Trump's Asian tour continues. While in Beijing, he made reference to unfair trade practices on behalf of China, blaming his predecessors at the White House for the situation.

On the data front, US jobless claimants for the week ending November 4 rose to 239k from 229k during the preceding week (this constituting a near 44-½-year low), exceeding expectations of 231k. The rise was seen as evidence that claims processing disrupted by the hurricanes hitting US soil has started to improve. Despite the increase, claims remain comfortably below the 300,000 mark. This feat, which holds true for the 139th consecutive week (the longest since 1970), is seen as denoting a robust jobs market. The four-week average of first-time claimants, which is less susceptible to weekly volatility, fell by 1.25k to stand at 231.25k, its lowest since 1973. Continuing claims, which include individuals receiving benefits after an initial week of state aid, increased by 17k relative to the previous week to reach 1.90 million. Expectations were for a reading of 1.89m. The US currency did not react much relative to majors within the first minutes of data release.

September wholesale inventory data out of the US released later in the session showed inventories rising by 0.3% m/m, as expected. August's figure saw a downward revision to 0.8% m/m growth from the previously reported 0.9%. Market reaction was limited as the data went public.

As Brexit talks are resuming today, euro/pound traded 0.3% higher on the day at 0.8869. Pound/dollar was little changed relative to yesterday's close, trading at 1.3107. PM May's government is seen as weakening following two cabinet resignations over the last week.

The European Commission today raised its growth forecasts for 2017 eurozone growth to 2.2% – it's strongest in a decade – from the previous 1.7%. At the same time, it cut its forecast for 2017 UK growth to 1.5%, while it projects a slowdown for the nation in 2018-19 as well.

Kiwi/dollar was down by 0.2% after rising to a more than two-week high of 0.6979 earlier in the day. Despite the pullback, the pair retained most of its gains following the RBNZ delivering what was perceived as a "hawkish hold" of rates at record low levels – the central bank's official cash rate stands at 1.75%. October electronic card retail sales out of New Zealand are due at 2145 GMT.

In commodities, gold continued gaining on the back of dollar weakness, posting a three-week high of $1,288.13 an ounce during today's trading. It last stood 0.2% higher on the day, trading at $1,283.50 an ounce. WTI was 0.9% higher at $57.32 a barrel and Brent was 0.6% up at $63.87 per barrel. Earlier in the week they both rose to their highest since July 2015, touching $57.92 and $64.65 a barrel respectively.

ECB Board member Sabine Lautenschlager will be giving a speech at the "Monetary, Financial, and Prudential Policy Interactions in the Post-Crisis World" conference in Washington DC at 1820 GMT.

Greenback’s Decline Leads to Growth for Other Currencies

The EUR/USD price broke the local descending trend line and is growing thanks to improving forecasts from the European Commission. Economic growth in the Eurozone will accelerate to 2.2% in 2017 which is 0.5% better than compared to the previous figure. At the same time, the European Commission noted the risks that can hurt economic growth in the region including Brexit, protectionism and geopolitical tensions. The bulls were encouraged by an increase in the German trade surplus to 21.8 billion euro in September against the 21.0 billion forecasted.

The main driver on the market today has been the weakening of the US dollar due to a lack of confidence in tax reforms being passed in. Proposed tax reform was one of the main stimulants for the greenback since the election of President Trump. Additional pressure on the USD came today from the initial jobless claims growing to 239,000 against the expected 232,000.

Uncertainty on the stock and forex markets resulted in an increased interest in safe haven assets like the Japanese yen. Tomorrow's release of the tertiary industry activity index in Japan may influence traders' mood, but the main focus will be on the discussions concerning tax reforms in the US.

British investors are waiting for the release of statistics on industrial production and goods trade balance tomorrow. The possible upside is likely to be limited by uncertainty about the outcome of Brexit talks.

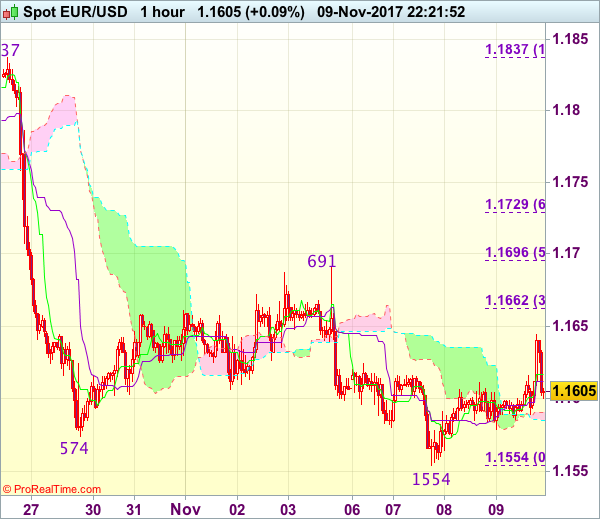

EUR/USD

The EUR/USD has left the limits of the local descending channel and is trying to fix above 1.1620. In case of success, the next targets will be at 1.1730 and 1.1825. The RSI on the 15-minute chart is close to the overbought zone and that may be a signal for a price rollback soon. In case of growth resuming, the closest targets will be 1.1550 and 1.1500.

GBP/USD

The GBP/USD keeps moving within the 1.3050-1.3050 range. Gaining a foothold above 1.3150 may become the basis for further price increases with the closest targets at 1.3250 and 1.3400. On the other hand, in order to continue the bearish trend, quotations need to break through the support at 1.3050. Volatility is likely to remain elevated tomorrow due to a publication of important macro data.

USD/JPY

The USD/JPY keeps moving along the inclined descending line. The closest target is located at 113.00 and breaking through it is likely to lead to 111.00 and 110.30. For the local descending trend to change to positive, the price will need to fix above 114.00. After the sharp decline, we may see the price rebound in the background of profit taking.

Yen Gains Ground as US Jobless Claims Disappoints

USD/JPY has posted losses in the Thursday session. In North American trade, USD/JPY is trading at 113.68 down 0.17% on the day. On the release front, Japanese Economy Watchers Sentiment improved to 53.2, beating the estimate of 50.7 points. In the US, unemployment claims climbed to 239 thousand, missing the estimate of 232 thousand. On Friday, the US publishes Preliminary UoM Consumer Sentiment.

The Bank of Japan has faced criticism over its ultra-accommodative stimulus program, but received support from the IMF on Thursday. The IMF stated that the BoJ should maintain the program in order to boost inflation, which remains at low levels, despite a stronger Japanese economy. Critics have argued that the massive stimulus has distorted markets, such as a 26-year high for the Tokyo stock market. However, the BoJ has consistently said that it will not taper the program until inflation moves closer to the Bank's 2 percent target. This stance puts the BoJ at odds with the Federal Reserve and the ECB, which are looking to reduce stimulus. However, the IMF noted that this divergence had not caused any significant capital outflows out of Asia, since the Fed and ECB had clearly communicated to the markets their shift in policy.

While US President Trump makes headlines with his visit to China, there is plenty of activity in Congress. After failing to pass a new healthcare act, President Trump has his sights set on tax reform, a key item in his domestic platform. Trump wants Congress to pass legislation overhauling the tax code before the end of the year, but that could prove to be too tight of a deadline. Most Democrats have come out against the proposal, and not all Republicans are on board. The bill would cut corporate taxes from 35% to 20%, but predictably, Democrat and Republican lawmakers are at odds as to whether the bill will lower taxes for the middle class. The bill is presently being debated in a congressional committee and is expected to move to the House floor next week. The Senate will present its version of the bill on Thursday, so we can expect plenty of activity in Congress in the next few weeks. Expectations that Trump will cut taxes has been the catalyst for a stock market rally over the past year, and if the bill does become law, the US dollar will likely gain ground.

Yen Hardly Profits from Volatility Up-tick

- European equities initially fend off heightened volatility stemming from Asian trading, but eventually fell prey to profit taking as well. Main indices trade up to 1% lower. US stock markets opened around 0.5% lower.

- The EU said that it is poised to beat 2017 economic growth expectations, with strong private consumption and the global recovery propelling the fastest pace of eurozone expansion in a decade (2.2% forecast from 1.7%). The UK is set to have the lowest growth of almost any EU country when it leaves the bloc in 2019 (1.1%).

- Even with an increase last week (from 229k to 239k), the level of US filings for unemployment benefits indicates steady demand for workers, Labor Department figures showed. The average number of applications filed over the past month was the lowest in 44 years.

- European financial markets are not deep enough to allow ECB quantitative easing to run on indefinitely, ECB Executive Board member Coeure said.

- ECB head of supervision, Nouy, signaled that she's willing to compromise on controversial plans to toughen rules on bad loans after criticism from the European Parliament. She told lawmakers that the guidance could be changed in response to comments received during a consultation period, and the Jan. 1 start date could be pushed back.

- The rate of growth of bad debt in Italy, excluding securitisations, has declined to the lowest level since the end of the eurozone debt crisis, marking the latest sign of the country's turnround. The annual growth rate of bad debt flows net of securitisations was 8.5% in September.

- Germany's imports and exports both fell in September as its trade surplus widened, highlighting the importance of domestic consumption as a driver of growth in Europe's largest economy. Seasonally adjusted exports fell by 0.4% on the month while imports were down by 1.0%, Federal Statistics Officedata showed.

Rates

Bund sell-off at odds with moves on other markets

Global core bonds lost ground today with German Bunds significantly underperforming US Treasuries. The weak performance of the Bund is at odds with risk aversion on stock markets, peripheral bond markets and, to a lesser extent, FX markets. European equity indices initially fend off the increased volatility from Asian trading, but eventually fell prey to profit taking as well (strengthening Tuesday's bearish engulfing pattern), losing up to 1%. Peripheral spreads widened a second straight session. The yen's gains on FX markets remain modest. The eco calendar, central bank speeches and events provide less of an explanation either. US weekly jobless claims stabilized near multiyear lows, but this was in line with forecasts. ECB Coeuré warned that ECB QE won't last indefinitely, but it wasn't the first time that he raised this concern. Other ECB speakers didn't really touch on monetary policy. The EC upgraded its growth forecasts, but the timing didn't coincide with the start of the Bund sell-off. Technical factors offer an explanation, but it goes a long way to exclusively pinpoint today's move to failed tests of support levels in the German 5-yr yield (-0.4%) and 10-yr yield (+0.3%).

At the time of writing, the German yield curve bear steepens with yields 1.3 bps (2-yr) to 5 bps (10-yr) higher. Changes on the US yield curve range between +0.4 bps (2-yr) and +1.6 bps (30-yr). On intra-EMU bond markets, 10-yr yield spreads widen up to 3 bps (Italy).

The Irish treasury successfully tapped two on the run IGB's today: €0.8 bn 1% May2026 and €0.45 bn 2% Feb2045. The combined amount sold was the maximum of the targeted €1-1.25 bn with an auction bid cover of 1.81. Year-to-date, the NTMA has issued €15.75 bn benchmark bonds this year, compared with its upwardly revised €16 bn target. The US Treasury completes its refinancing operation later today with a $15 bn 30-yr Bond auction. The WI trades currently around 2.8%.

Currencies

Yen hardly profits from volatility up-tick

Global markets were spooked by an unexpected uptick of volatility on equity markets. At the same time, Bunds and Treasuries came under pressure.The dollar and the euro both received interest rate support, despite the equity correction. This prevented a meaningful gain of the usual safe havens (Japanese yen, Swiss franc). EUR/USD trades little changed in the low 1.16 area. USD/JPY trades at around 113.55.

Trading on Asian markets turned much more volatile than what we've got used to recently. Japanese markets took the lead in this turnaround. The Nikkei set a 25-yr top, but fell off a cliff later in the session. There was no specific news or event to explain the move. Other regional equity markets developed a similar, but more modest pattern. EUR/USD was hardly affected and traded stable in the 1.16 area. USD/JPY dropped from the 114 area to around 113.50.

European equities opened little changed. Initially it looked that European markets could avoid the volatility uptick in Asia. However, the Asian swing had planted seeds of uncertainty in European investors' minds. The topside in European equities was blocked and indices finally dropped below first intraday support levels. Remarkably, safe haven bunds couldn't profit. On the contrary, the Bund also fell prey to an aggressive selling move. Moves in the T-Note future were much more modest. The combination of higher core/EMU yields and substantial equity losses still pushed USD/JPY a few ticks lower. However, the (LT) interest rate differential narrowed substantially in favour of the euro. This prevented the 'usual' sell-off in the likes of EUR/JPY. EUR/USD even temporary rebounded to the 1.1640/45 area.

In the US trading session, Treasuries gradually joined the rise in European yields, supporting the dollar. USD/JPY settled in the mid 113 area. EUR/USD returned to the 1.16 pivot. US jobless claims were higher/worse than expected but no issue for (currency) markets. In the end, save haven currencies like the yen and the Swiss franc profited only slightly from the uptick in equity volatility as it was counterbalanced by higher interest rate support for the euro and the dollar.

Brexit and global risk-off weigh on sterling

Sterling came again under pressure yesterday due to a flaring up of political uncertainty in the UK. This correction continued today. There were no important eco data in the UK. Investors kept a close eye on the next round of official Brexit negotiations that started in Brussels today. EU negotiators were said to maintain a very cautious approach as they tried to ponder the consequences of the political turmoil in the UK. The overall risk-off context is usually a negative for sterling, too. EUR/GBP trades in the 0.8865/70 area. Cable is changing hands around 1.31.

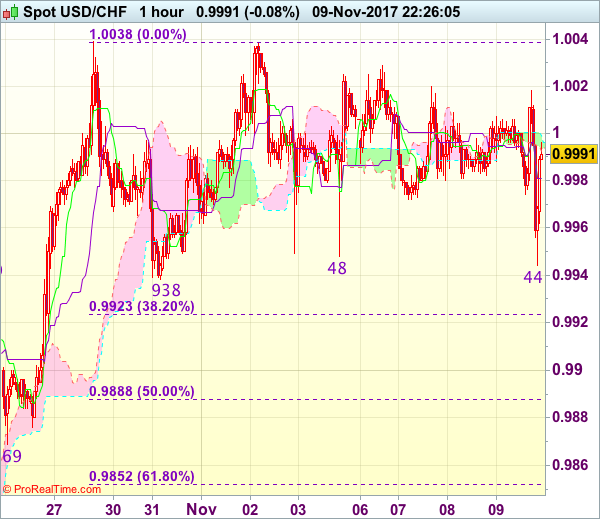

Trade Idea Wrap-up: USD/CHF – Stopped profit and stand aside

USD/CHF - 0.9965

Most recent candlesticks pattern : N/A

Trend : Up

Tenkan-Sen level : 0.9981

Kijun-Sen level : 0.9981

Ichimoku cloud top : 0.9999

Ichimoku cloud bottom : 0.9992

Original strategy :

Bought at 0.9950, stopped profit at 0.9970

Position : - Long at 0.9950

Target : -

Stop : - 0.9970

New strategy :

Stand aside

Position : -

Target : -

Stop : -

The greenback has retreated again after faltering below resistance at 1.0020, dampening our bullishness and near term choppy trading is likely to continue, hence downside risk is seen for test of 0.9938 support, break there would signal top has been formed at 1.0038 earlier, bring retracement of recent rise to 0.9920-23 (38.2% Fibonacci retracement of 0.9737-1.0038) but 0.9885-90 (50% Fibonacci retracement) should limit downside, bring another upmove later.

As near term outlook is mixed, would be prudent to stand aside in the meantime. Above 1.0020 would bring test of 1.0038 but break there is needed to confirm the rise from 0.9421 low has resumed and extend further gain to 1.0050-55, then towards 1.0075-80 but price should falter below 1.0100 chart resistance.

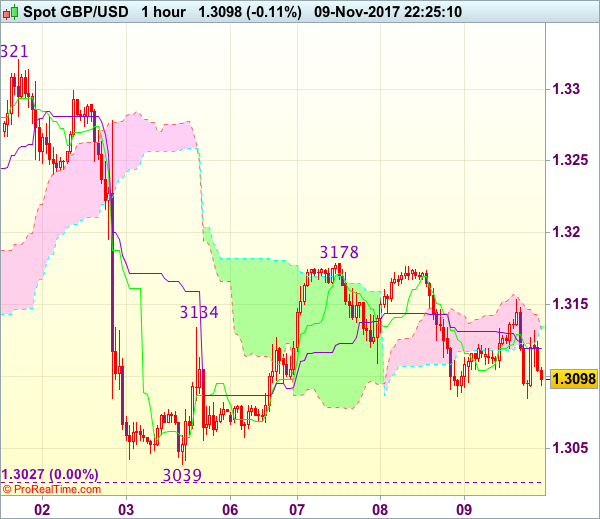

Trade Idea Wrap-up: GBP/USD – Hold short entered at 1.3175

GBP/USD - 1.3106

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.3119

Kijun-Sen level : 1.3119

Ichimoku cloud top : 1.3135

Ichimoku cloud bottom : 1.3133

Original strategy :

Sold at 1.3175, Target: 1.3045, Stop: 1.3175

Position : - Short at 1.3175

Target : - 1.3045

Stop : - 1.3175

New strategy :

Hold short entered at 1.3175, Target: 1.3065, Stop: 1.3155

Position : - Short at 1.3175

Target : - 1.3065

Stop : - 1.3155

Although the British pound has recovered after falling to 1.3085 and consolidation would be seen, reckon resistance at 1.3153 would cap upside and bring another decline later, below said support would add credence to our bearish view that the rebound from 1.3039 has ended at 1.3178, bring further fall to 1.3055-60, then retest of this support. Looking ahead, only a drop below 1.3027 low would confirm early downtrend has resumed for weakness to psychological support at 1.3000, then towards 1.2970-75.

In view of this, we are holding on to our short position entered at 1.3175. Only above 1.3175-80 would risk gain to 1.3200, break there would defer and prolong choppy trading, risk a stronger rebound to 1.3235-40 first.

Trade Idea Wrap-up: EUR/USD – Stand aside

EUR/USD - 1.1615

Most recent candlesticks pattern : N/A

Trend : Down

Tenkan-Sen level : 1.1617

Kijun-Sen level : 1.1612

Ichimoku cloud top : 1.1591

Ichimoku cloud bottom : 1.1585

Original strategy :

Sold at 1.1620, stopped at break-even

Position : - Short at 1.1620

Target : -

Stop : - 1.1620

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Intra-day rebound to 1.1644 dampened our near term bearishness and suggests temporary low has been formed at 1.1554 earlier this week, hence upside risk is seen for retracement of recent decline and gain to 1.1645-50, then 1.1662-65 (38.2% Fibonacci retracement of 1.1837-1.1554) is likely, however, reckon upside would be limited to resistance at 1.691-96 (50% Fibonacci retracement) and bring retreat later.

On the downside, below 1.1575-80 would suggest an intraday top is formed and revive bearishness for retest of 1.1554, break there would extend recent decline to 1.1520-25, then 1.1500 but oversold condition should prevent sharp fall below latter level and reckon 1.1470-75 would hold. As near term outlook is mixed, would be prudent to stand aside for now.