Sample Category Title

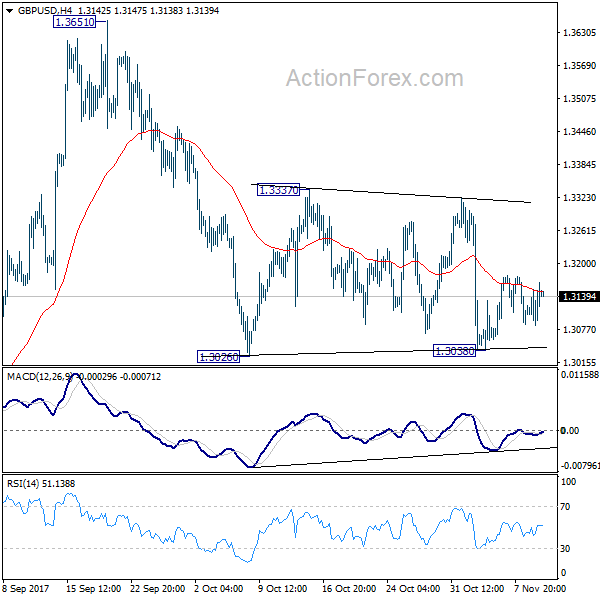

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3097; (P) 1.3131; (R1) 1.3178; More....

Intraday bias in GBP/USD remains neutral as consolidation from 1.3026 continues. Upside of recovery should be limited below 1.3337 resistance to bring fall resumption. Break of 1.3038 will now resume decline from 1.3651 to 1.2773 key support level. However, decisive break of 1.3337 will indicate that pull back from 1.3651 is completed and medium term rise from 1.1946 is resuming.

In the bigger picture, as noted before, GBP/USD hit strong resistance from the long term falling trend line. Current development is starting to favor that corrective rebound from 1.1946 low has completed at 1.3651. Decisive break of 1.2773 will confirm this bearish case and target a test on 1.1946 low next, with prospect of resuming the low term down trend. Nonetheless, break of 1.3320 resistance will restore the rise from 1.1946 for 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

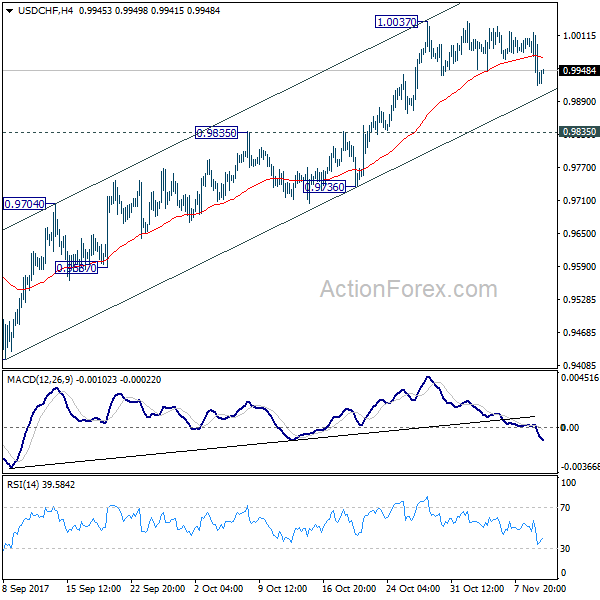

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9901; (P) 0.9959; (R1) 0.9997; More....

USD/CHF's consolidation from 1.0037 is still in progress and drips lower. Intraday bias remains neutral at this point. As noted before, downside should be contained above 0.9835 resistance turned support and bring rally resumption. On the upside break of 1.0037 will resume whole rally from 0.9420. And with sustained trading above 61.8% retracement of 1.0342 to 0.9420 at 0.9990, USD/CHF should then target a test on 1.0342 key resistance.

In the bigger picture, current development suggests that USD/CHF has defended 0.9443 (2016 low) key support level again. Rise from 0.9420 could is a medium term up move and should target a test on 1.0342 high. This represents the upper end of a long term range that started back in 2015. On the downside, break of 0.9736 support is now needed to indicate completion of the rise from 0.9420. Otherwise, further rally will remain in favor in medium term.

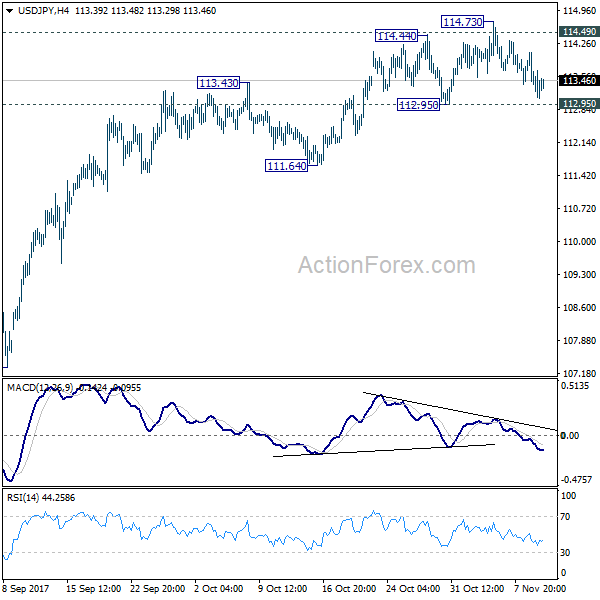

USD/JPY Daily Outlook

Daily Pivots: (S1) 113.01; (P) 113.53; (R1) 113.99; More...

Intraday bias in USD/JPY remains neutral at this point. As it's still holding on to 112.95 support, near term outlook remains bullish. On the upside, sustained break of 114.49 key resistance will pave the way to retest 118.65 high. However, break of 112.95 support will now indicate rejection from 114.49 and turn bias to the downside for 111.64 support and below.

In the bigger picture, medium term rise from 98.97 (2016 low) is not completed yet. It should resume after corrective fall from 118.65 completes. Break of 114.49 resistance will likely resume the rise to 61.8% projection of 98.97 to 118.65 from 107.31 at 119.47 first. Firm break there will pave the way to 100% projection at 126.99. This will be the key level to decide whether long term up trend is resuming.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7654; (P) 0.7674; (R1) 0.7698; More...

AUD/USD's consolidation from 0.7624 is still in progress and intraday bias remains neutral. Overall, near term outlook stays bearish with 0.7896 resistance intact and deeper fall is expected. Decisive break of 0.7624 will resume whole decline from 0.8124. And, AUD/USD should target next key cluster level at 0.7322/8 next.

In the bigger picture, corrective rise from 0.6826 medium term bottom is likely completed at 0.8124, after hitting 55 month EMA (now at 0.8067). Decisive break of 0.7328 key cluster support (61.8% retracement 0.6826 to 0.8124 at 0.7322) will confirm. And in that case, long term down trend from 1.1079 (2011 high) will likely be resuming. Break of 0.6826 will target 61.8% projection of 1.1079 to 0.6826 from 0.8124 at 0.5496. This will now be the favored case as long as 0.7896 near term resistance holds.

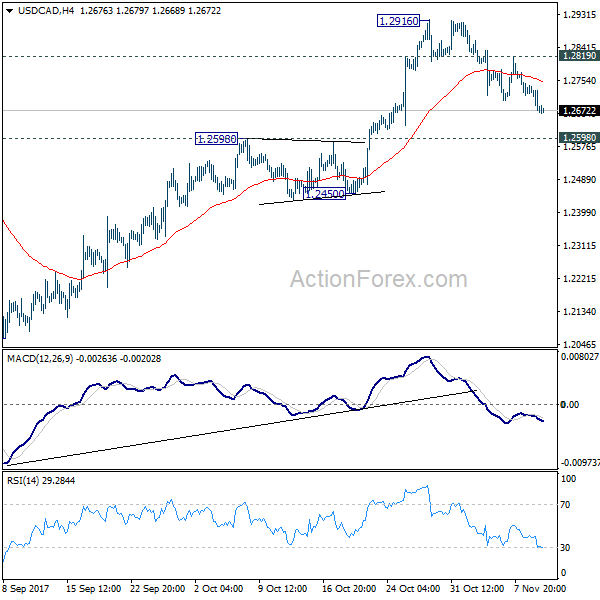

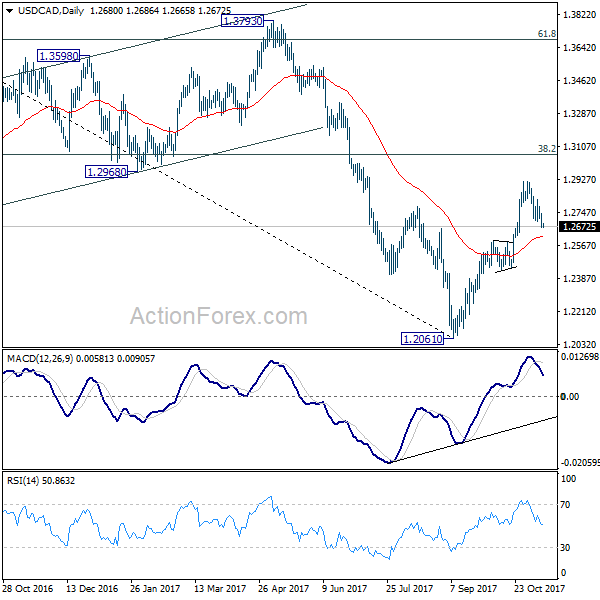

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2652; (P) 1.2696; (R1) 1.2725; More....

USD/CAD's corrective pull back from 1.2916 is still in progress and could extend lower. But still, as long as 1.2598 resistance turned support holds, near term outlook stays bullish. Further rise is expected in the pair. Above 1.2819 minor resistance will turn bias back to the upside for 1.2916 high first. Break there will extend the rise from 1.2061 to 38.2% retracement of 1.4689 to 1.2061 at 1.3065. However, sustained break of 1.2598 will argue that rebound from 1.2061 has completed after hitting 55 week EMA (now at 1.2916). Near term outlook will be turned bearish in this case.

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4689 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Rise from 1.2061 medium term bottom should now target 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Firm break there will target 1.3793 key resistance next (61.8% retracement at 1.3685). We'll now hold on to this bullish view as long as 1.2450 support holds.

Dollar Soft as Senate Released Tax Plan, Stocks Down But Not Out

The US markets responded negatively overnight as Senate's version of tax plan confirmed they wanted to delay corporate tax cut by a year. But considering intraday price actions, the reactions were not disastrous. DOW dropped initially to 23310.02 before paring much losses to close at 23461.91, down -101.42 pts or -0.43%. That's close to open at 23492.09. S&P 500 dropped as low as 2566.33 before closing at 2584.62, down -9.76 pts or -0.38%. That's even slightly higher than open at 2584.00. NASDAQ dropped to as low as 6687.28 then closed at 6750.05, down -39.07 pts or -0.58%. That's notably higher than open at 6737.45. After all, US equities has now entered into a consolidation phase after recent record runs. 10 year yield tried to recovery and ended up 0.006 at 2.331. Dollar, on the other hand, stays pressured and is set to end as the weakest one for the week.

Senate tax plan confirms corporate cut delay

The Senate's version of tax plan was finally released yesterday. And it's confirmed that Senators proposed to delay the corporate tax cut from 35% to 20% in 2019. That's a year later than what the House proposed, that is 2018. There are also differences in some key aspect. To name a few, Senate prefers to set up a top individual rate of 38.2%, instead of House's 39.6% which is unchanged. This carries symbolic meaning of lowering taxes for the richer. Senate's version also repeals the deductions for state and local taxes. Some see the differences as significant and could set up a long process of reconciliation.

The House Ways and Means committee passed its tax bill yesterday, setting it up for a full House vote as soon as next week. Senate will hold hearings on the bill next week. And the Senators are targeting to pass it a week after Thanksgiving. After passing the bill in Senate, the two chambers will try to close the gaps in a process known as a conference committee.

ECB officials optimistic on economic outlook

ECB Executive Board member Benoit Coeure acknowledged that the expansion in Eurozone economy is becoming more balanced and robust. But he noted that "this recovery is carried in no small part by monetary policy and the exchange rate and equally by low commodity prices." And, he emphasized that "these factors won't last forever" and "if we accept this, the states of the euro zone will find themselves unarmed when the next crisis arrives." He urged to "build up new firepower and for that we need reforms."

Separately, Governing Council member Francois Villeroy de Galhau said that "Euro-area growth will be sustained in the next two years thanks to strong investment and thanks to increased convergence among countries." And, "this forecast, including a positive but still subdued inflation, confirms the adequacy of the gradual normalization of our monetary policy we are engaged in." He referred to the European Commission forecast that growth is accelerating to 2.2% this year.

Another Governing Council member Philip Lane said that "if we have enough signals, we can get active and move on" with monetary policy. And he emphasized that "our monetary policy does not always have to follow such a gradual and incremental approach as it is currently the case." And, "inflation doesn't have to reach our goal before we discuss changing our policy." Nonetheless, he also acknowledged that "inflation must be clearly on the way towards this goal. At the moment this is not the case."

Brexit to take place at 11 p.m. GMT, on March 29, 2019

In UK, Brexit Secretary David Davis is going to propose an amendment to the EU Withdrawal Bill in the Parliament next week. He suggests to making "crystal clear" that the departure will take place at 11 p.m. GMT, on March 29, 2019. Davis said that "we've listened to members of the public and Parliament and have made this change to remove any confusion or concern about what 'exit day' means". And, "this important step demonstrates our pragmatic approach to this vital piece of legislation -- where MPs can improve the Bill, whatever their party, we will work with them."

RBA sees accelerating growth, sluggish inflation ahead

RBA's Statement of Monetary Policy showed that the central bank is expecting accelerating growth but sluggish inflation ahead. Thus, it's likely to maintain a neutral stance to keep the cash rate unchanged at record low at 1.5%. Here is a summary of changes in projections:

- GDP growth at 2.5% in Dec 2017, 3.25% in Dec 2018, 3.25% in Dec 2019. Prior forecast at 2-3%, 2.75-3.75%, 3-4% respectively

- CP inflation at 2% in Dec 2017, 2.25% in Dec 2018, 2.25% in Dec 2019. Prior forecast at 1.5-2.5%, 1.75-2.75%, 2-3% respectively.

- Underlying inflation at 1.75% in Dec 2017, 1.75% in Dec 2018, 2% at Dec 2019. Prior forecast at 1.5-2.5%, 1.5-2.5%, 2-3% respectively.

On the data front

Japan M2 rose 4.1% yoy in October. UK productions will be the main focus in European session. Trade balance and construction output will also be released. US will release U of Michigan sentiment.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2652; (P) 1.2696; (R1) 1.2725; More....

USD/CAD's corrective pull back from 1.2916 is still in progress and could extend lower. But still, as long as 1.2598 resistance turned support holds, near term outlook stays bullish. Further rise is expected in the pair. Above 1.2819 minor resistance will turn bias back to the upside for 1.2916 high first. Break there will extend the rise from 1.2061 to 38.2% retracement of 1.4689 to 1.2061 at 1.3065. However, sustained break of 1.2598 will argue that rebound from 1.2061 has completed after hitting 55 week EMA (now at 1.2916). Near term outlook will be turned bearish in this case.

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4689 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Rise from 1.2061 medium term bottom should now target 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Firm break there will target 1.3793 key resistance next (61.8% retracement at 1.3685). We'll now hold on to this bullish view as long as 1.2450 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Japan Money Stock M2+CD Y/Y Oct | 4.10% | 4.10% | 4.10% | 4.00% |

| 0:30 | AUD | RBA Monetary Policy Statement | ||||

| 4:30 | JPY | Tertiary Industry Index M/M Sep | -0.2% | -0.10% | -0.20% | |

| 9:30 | GBP | Industrial Production M/M Sep | 0.30% | 0.20% | ||

| 9:30 | GBP | Industrial Production Y/Y Sep | 1.90% | 1.60% | ||

| 9:30 | GBP | Manufacturing Production M/M Sep | 0.30% | 0.40% | ||

| 9:30 | GBP | Manufacturing Production Y/Y Sep | 2.40% | 2.80% | ||

| 9:30 | GBP | Construction Output M/M Sep | -0.90% | 0.60% | ||

| 9:30 | GBP | Visible Trade Balance (GBP) Sep | -12.9B | -14.2B | ||

| 15:00 | USD | U. of Mich. Sentiment Nov P | 100.6 | 100.7 |

Market Morning Briefing: The Pound Trades Near A Crucial Support

STOCKS

Almost all major equity indices seems to have initiated a corrective dip except Shanghai and could continue to fall next week, bringing a pause to the recent rally.

Dow (23461.94, -0.43%) has immediate support near 23400 and lower upport on the weekly charts at 23000. While that holds, there could be a decent dip in the index today before again trying to rise higher in the medium term.

Dax (13182.56, -1.49%) has come off from resistance visible on the 3-day candle chart. While the resistance holds, the index could come off towards 13000-12800 in the near term. Immediate view is bearish for the next week.

Nikkei (22547.42, -1.40%) finally seems to have formed a top below 23500 and while that holds, the index could see either a sharp correction possibly heading towards 22000 or consolidate sideways near current levels. The fall in Dollar Yen if continues can pull down Nikkei in the coming sessions.

Shanghai (3419.76, -0.23%) has some room on the upside towards 3460-3500 for the near term. Note that 3500 is an important resistance on the upside and the index could be ranged in the 3500-3380 region for at least the remaining sessions for this month.

Nifty (10308.95, +0.06%) is likely to come off towards 10100 in the coming sessions before again trying to attempt arise towards 10500 again in the longer term. Immediate view is bearish.

COMMODITIES

Gold (1285.34) is slowly trying to rise towards 1300. But an interim rejection from 1290 is possible just now which could push the price to levels near 1280-1270 again. An eventual rise towards 1300 is possible in the coming week.

Brent (63.78) could possible trade in the 65-63 range for a few sessions before trying to attempt higher levels. While 65 holds, we may also look at a possibility of a fall towards 62-61 in the medium term.

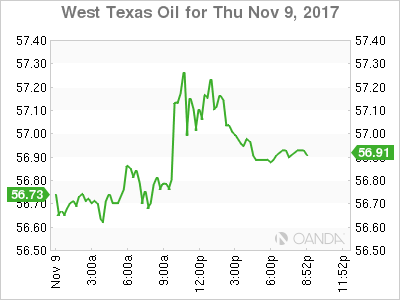

WTI (57.03) could find an interim support near 56.50 which if holds could keep the price range bound within 56-58 region. A break above 58 could open up chances of testing 59 in the longer term.

Copper (3.0820) is trading near immediate support on the daily candle chart. If that holds, the price could bounce back towards 3.20-3.25 again in the coming week. Near term looks bullish.

FOREX

The Euro (1.1640) as the ECB has upped it's European growth forecast from 1.7% to 2.2% (for 2017) and from 1.8% to 2.1% in 2018, leading to a hardening of German yields (see Interest Rates below). The change in direction now targets 1.17 in the near term. 7nclear whether we will get to see a rise past that.

Dollar-Yen (113.30) has come off substantially from the 114.50, the Resistance that was holding it down for the last several days. Crucial Support seen near 113 now. A confirmed break below that could be very bearish.

Basically, the market has to decide whether it has had enough of Dollar strength or it still believes in the rise of the Dollar Index (94.53) from the September low of 91.The uptrend looks intact while Support at 94.25 holds.

The Pound (1.3145) trades near a crucial Support, with deeper Support near 1.3025. It could be a candidate for a bounce if these Supports hold over the next few days.

The Aussie (0.7683) has been ranged roughly between 0.7625-7725 over the last two weeks. Still, it seems a final dip to 0.7600 would be appropriate. Note that Copper could stage a bounce from near current levels. To that extent the downside might be limited for the Aussie as well.

Dollar-Yuan (6.6390) could be on the threshold of a strong rise, but needs a break above 6.65-66 for confirmation. This will be interesting to watch. Similarly, Dollar-Rupee (63.95) needs a break above 65.10-15 to confirm a strong rise.

INTEREST RATES

The German 10Yr (0.37%) and the 30Yr (1.26%) have both moved up from 0.33% and 1.21% respectively, on the back of the increase in European GDP forecasts by the ECB. But we need to see the 10Yr move up past 0.40% in order to be able to think of a sustained rise.

Meanwhile, the US Yields have also risen, albeit a little less. The 10yr (2.34%) is up from 2.33% while the 30Yr (2.82%) is up a goodish bit from 2.78%. The 30Yr has potential to test 3.00% in the coming weeks while the 10Yr can rise to 2.50% while above 2.25%.

It is possible that the German-US 10Yr Spread (-1.97%) may find Resistance near current levels.

Significantly, in India, leading bankers (Uday Kotak of Kotak Mahindra Bank and Rajnish Kumar of SBI) have started talking about limited room for a rate cut. The 10Yr GOI (6.9314) has been trading above 6.85% this week and has moved up steadily in the last few sessions. 7% is an important resistance just now, which if breaks could initiate sharp rise for the medium term.

Frantic Friday?

Frantic Friday?

Senate Republican tax cut proposals unnerved markets

It was a tumultuous Thursday as Washington smoke screens and fades have traders running every which way but up. But the overriding concern is that GOP dissent is running high creating a high level of angst that this vital piece of legislation will even pass a vote.

The Republican plan was to implement a 20% corporate tax cut after a one-year delay. Investors had a massive anxiety attack sending the Dow down 130 points, as currency traders relentlessly hammered USDJPY near the key 113 tipping point

There's a definite risk-off tone in currency markets but trying to decipher if investors hate the plan or are merely booking profits will be the crucial determinant. All eyes are on equity index futures this morning, after USDJPY coming within a stone through of 113.00 overnight, it's going to be one of those “edges of the seat” days as dealers continue to digest Washington headlines. Downside USDJPY risk could accelerate hugely on a break of critical 113 support line as this will likely trigger a wave of JPY cross-selling

The Australian Dollar

The RBA lowered their inflation forecast through 2019 all but serving the Aussie dollar up on a platter.Although this was the likely outcome due to the change in CPI measurement methodology, we could see a decent sell-off on the Aussie eventually materialize more so against the NZD given the divergent monetary policy rhetoric of late between the RBNZ and RBA. Keep in mind AUDUSD trade remains exceptionally sticky these days so best to express any negative bias through the crosses.

The US Dollar

We knew this was going to be a challenging week for the greenback given the sparse economic diary and we should expect the dollar to struggle in the weekend as US political crowing will hang like an anvil around the dollar neck near term.

The Japanese Yen

We're holding the bottom end of the near term 113 -114.50 range but USDJPY will be at the complete mercy of tax reform rhetoric. Ultimately I expect cooler heads to prevail onUS tax reform and view the current market sell-off as a correction.Over the long haul, the overtly dovish BoJ will continue to weaken JPY.

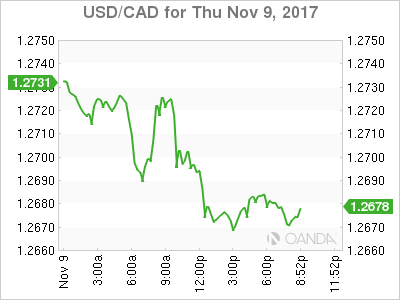

USD/CAD Canadian Dollar Higher US Tax Worries Hurt USD

The Canadian dollar rose on Thursday as the US senators are paring back some of the corporate tax cuts in an effort to keep the impact of the proposed bill under $1.5 trillion. Republican senators are pushing back the timelines on reducing the corporate tax rate until 2019 and will water down the original plan introduced by the Trump Administration. Treasury Secretary Steven Mnuchin has already said that a delay is better than a longer phase in. The amount of differences between the Senate proposal and the one working its way through the House of representatives are considerable and increase the chances of the tax overhaul not being a reality in 2017.

The political tide could also be changing in the United States ahead of next year primaries. Regional elections have racked important wins for Democrats with a more divided congress forecasted in the future. If the Administration has not been able to pass legislation with majorities it would be almost impossible having to seek bipartisan support.

Trade talks are going into the midnight hour in Vietnam with comments from the Japanese and Mexican teams that a deal is close. Japan claims that there has been a ministerial agreement, but the Canadian Trade Minister has said on twitter that an agreement has not been reached. It seems that details still need to be ironed out, but there seems to have been progress made to bring the TPP into fruition. The United States left the Trans Pacific Partnership as one of the first executive orders of President Trump.

The USD/CAD lost 0.42 percent in the last 24 hours. The currency pair is trading at 1.2674 after concerns with the US tax reform plans have taken the wind out of the US dollar sails. Oil continues to support the rise of the loonie with has seen the Canadian currency appreciate 0.60 percent this week.

Canadian new home prices rose in September. Vancouver was the big winner, while Toronto remains unchanged in a report Statistics Canada published Thursday. Mortgage rule changes and regulation to reduce real estate speculation by foreign buyers has cooled one of the hottest markets in the globe. The weakness of the Canadian dollar after the drop in oil prices and the overall stability of the economy made urban destinations rise as investment opportunities. Price rose and with it levels of household debt amongst Canadians, sending warning signs to Financial institutions and rating agencies. The Bank of Canada (BoC) has hiked rates twice in 2017 and continues to monitor debt levels with a possible rate lift in the first quarter of 2018 if inflation continues to rise.

Energy prices rose above the $57 price level only to return to $56.95 on the back of increasing rumours of a possible coronation of crown prince Mohammed bin Salman if his 81-year-old father abdicates. The uncertainty of what the corruption arrests real impact will have on the world’s second largest producer of crude and de facto leader of the Organization of the Petroleum Exporting Countries (OPEC) has the price of crude rising. With the November 30 meeting between oil producers who agreed to cut production fast approaching the existence of the OPEC is also at stake as Saudi Arabia has raised the levels of animosity towards Iran and its perceived allies.

The pact to reduce supply has been the main driver adding stability to the energy market in the past two years. The architects of the agreement has been Saudi Arabia, but also bears remembering that their plan to drive US shale producers out of business by over-drilling is what led to the spectacular crash in oil prices in the first place.

At the moment oil rig counts in the US have not been rising as fast as oil prices. Temporary weather factors have keep US supply down, although last week’s surprise crude inventory numbers could be the beginning of a US led rise in supply.

Market events to watch this week:

Friday, November 10

5:30am GBP Manufacturing Production m/m

Gold Rally Continues As Jobless Claims Jump

Gold has posted gains for a second straight day. In Thursday’s North American trade, the spot price for an ounce of gold is $1286.73, up 0.42% on the day. On the release front, unemployment claims climbed to 239 thousand, missing the estimate of 232 thousand. On Friday, the US publishes Preliminary UoM Consumer Sentiment.

Unemployment Claims were a disappointment at 239 thousand, climbing to a 4-week high. Investor sentiment will not fall after one soft employment report, but there are some concerns with the US labor market. Nonfarm payrolls rebounded in October with a gain of 261 thousand, after a rare decline a month earlier. Still, this reading was well off the forecast of 312 thousand. Wage growth remains a problem, reflective of chronically low inflation. In October, Average Hourly Earnings posted a flat 0.0%, the first time wages have not increased since November 2016.

After failing to pass a new healthcare act, President Trump has his sights set on tax reform, a key item in his domestic platform. Trump wants Congress to pass legislation overhauling the tax code before the end of the year, but that could prove to be too tight of a deadline. Most Democrats have come out against the proposal, and not all Republicans are on board. The bill would cut corporate taxes from 35% to 20%, but predictably, Democrat and Republican lawmakers are at odds as to whether the bill will lower taxes for the middle class. The bill is presently being debated in a congressional committee and is expected to move to the House floor next week. The Senate will present its version of the bill on Thursday, so we can expect plenty of activity in Congress in the next few weeks. Expectations that Trump will cut taxes has been the catalyst for a stock market rally over the past year, and if Trump succeeds in overhauling the tax code, investor risk appetite could soar and weigh on gold prices.