Sample Category Title

Dollar Lacks Momentum for Recovery as Senate Tax Plan Awaited

Dollar tries to recover today but momentum is weak. The greenback is still trading as the weakest major currency for the week, as weighed down by concerns over the tax plan. But the picture could be cleared up as Senate is set to unveil their version of the bill. Released from US, initial jobless claims rose 10k to 239k in the week ended November 4, higher than expectation of 231K. Nonetheless, the four week moving average dropped -1.25k to 231.25k, lowest since March 1973. Continuing claims rose 17k to 1.9m in the week ended October 28. From Canada, new housing price index rose 0.2% mom in September.

Elsewhere, German trade surplus was largely unchanged at EUR 21.8b in September. UK RICS house price balance rose 1.0% in October. Swiss unemployment rate was unchanged at 3.1% in October. Japan machine orders dropped -8.1% mom in September, current account surplus narrowed to JPY 1.84T. Australia home loans dropped -2.3% mom in September. China CPI accelerated to 1.9% yoy in October, PPI was unchanged at 6.9% yoy.

Republicans to unveil their tax plan

In the US, House Ways and Means Committee are spending the last efforts in hammering out the tax bill for a vote today. Meanwhile, Senator Republicans are set to brief and publish their own version of the bill today too. A key point of focus for the financial markets is the corporate tax cut from 35% to 20%. There are talks that Senators would opt for delaying the cut to comply with the budget rule. But Senator Orrin Hatch, chairman of the tax-writing finance committee, said he would prefer not to delay. Other than that, economists will scrutinize the plans to see how far the versions are apart. Thus, there would be a more realistic sense on whether the final version could be. Dollar could have a strong reaction once the Senate tax bill is released.

Cleveland Fed Mester: Gradual rate path is best strategy

Cleveland Fed President Loretta Mester said in a television interview that "a gradual path is the best strategy we have for prolonging the expansion." She added that "obviously we want to be responsible to changes in the economic outlook and as data comes in we are always revising the outlook." WTI oil price surged to 2 year high at 57.96 yesterday on Middle East political uncertainty. But that doesn't worry Mester and she said "the key thing will be, does it upset inflation expectations? Will they arise? Will they respond to those oil price increases?"

Powell's confirmation hearing scheduled on November 28

US Senate Banking Committee schedules a confirmation hearing for Jerome Powell as Fed Chair on November 28. Fed Governor has already got quick endorsement from Republicans after Trump's nomination. Senate Majority Leader Mitch McConnell met with Powell on Tuesday and said he looked forward to "supporting his nomination". Meanwhile chair of the Banking Committee, Republican Senator Mike Crapo, also hailed that Powell was "well-equipped to lead our economy and the country in a positive direction." Powell is generally seen as a safe choice by the markets and would likely continue with the policy path laid by Janet Yellen. That is, Fed will continue with rate hikes, likely three, next year, as well as the plan to shrink the USD 4.5T balance sheet.

ECB could delay and improve bad loan rules

ECB's plan to implement tougher rules on bad loans is a hot topic this week. Chair of the Supervisory Board at the European Central Bank Danièle Nouy told EU Parliament in Brussels that the "the drafting can be improved, for sure, and it will be improved." And, she proposed to "give us a bit more time". Originally, the rules would be consulted until December 8. Daniele said that could be pushed back to January 1. The plan drew heavy criticism from EU Parliament and Italy. In particular, Italian Economy Minister Pier Carlo Padoan said the plan "goes beyond the supervisory limits" of the bloc's SSM mechanism.

Brexit negotiation restarts

Brexit negotiations restart in Brussels today. A sticky point of the deadlock is the amount of the divorce bill. It's believed that EU would require UK to pay as much as EUR 60b in financial obligations But so far, UK has refused to clearly state how much it's willing to pay. Ahead of the negotiations, European Commissions released new economic forecasts. EC projects UK economy to grow 1.5% in 2017, 1.3% in 2018 and slows further to 1.1% in 2019, the year Brexit happens. The figures would be second lowest among EU nations.

BoJ opinions show debate on extreme steps

In the summary of opinions in the October BoJ meeting, there were debates on the call from new comer Goushi Kataoka to increase stimulus. Kataoka proposed to target 15 year bond yields to below 0.2% through the bond purchases. That is, he either wanted to expand the targeting from 10 year yields to include 15 year yields. Or, he wanted to switch to target 15 year yield. But the proposal met with oppositions as one board member described by one member as "extreme steps" that could destabilize financial markets. The member added that "the current policy is the most appropriate one to lay the grounds for companies to boost productivity, with the smallest degree of uncertainty over its effect on the economy." Nonetheless, it's consensus that there were concerns over inflation outlook and another member noted "it may take some time before inflation reaches 2 percent."

At this point, there is no confirmation on whether BoJ Governor Haruhiko Kuroda would be renewed for another term next year. The outspoken economic advisor to Prime Minister Shinzo Abe reiterated his call for changes in BoJ. Etsuro Honda said that "The leaders of the central bank must conduct a comprehensive review and then take responsibility." And, "it's impossible to end deflation without bringing in a new regime." Meanwhile, Honda also warned that BoJ has to meet the 2% inflation target before sales tax hike in 2019. Otherwise, "Japan's economy will be in critical danger."

RBNZ turned slightly more hawkish

While keeping the OCR unchanged at 1.75%, the tone of November RBNZ statement has turned slightly more hawkish than previous ones. The central bank upgraded inflation forecasts, while describing core inflation as 'subdued' and reiterating 'uncertainties' in the new government's policies. The growth outlook remained largely unchanged from August's, as weaker growth in the housing and construction sector would be offset by greater fiscal spending promised by the new government and higher terms of trade, thanks to NZD depreciation and the rise in oil prices. RBNZ slightly pushed ahead the rate hike schedule. However, given the minimal change, we believe this is rather a symbolic move. The central bank expects more material interest rate movements by 2020. We believe the monetary policy would stay unchanged for the rest of 2018. More in RBNZ Upgraded Inflation Forecasts, Ambivalent About New Government Policies

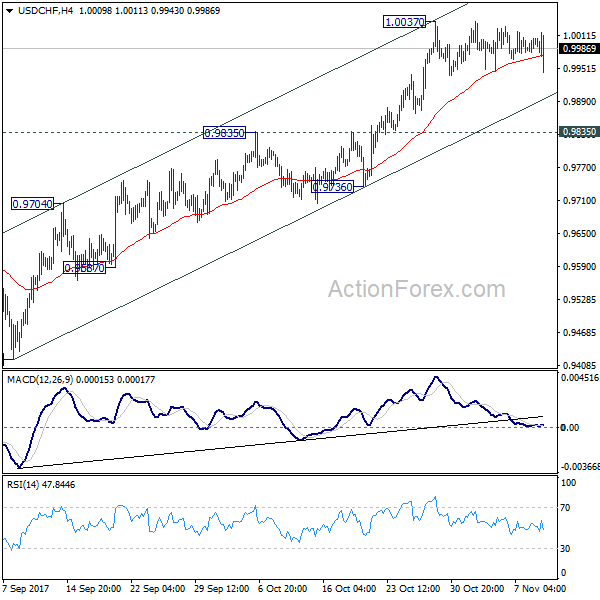

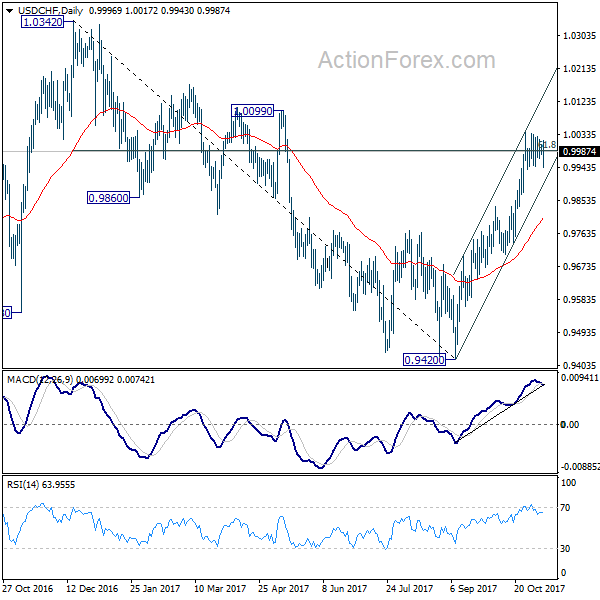

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9986; (P) 0.9996; (R1) 1.0012; More....

USD/CHF spikes lower today but quickly recovers. The pair is staying in consolidation from 1.0037 and intraday bias remains neutral. We'd continue to expect downside of retreat to be contained above 0.9835 resistance turned support and bring rally resumption. On the upside break of 1.0037 will resume whole rally from 0.9420. And with sustained trading above 61.8% retracement of 1.0342 to 0.9420 at 0.9990, USD/CHF should then target a test on 1.0342 key resistance.

In the bigger picture, current development suggests that USD/CHF has defended 0.9443 (2016 low) key support level again. Rise from 0.9420 could is a medium term up move and should target a test on 1.0342 high. This represents the upper end of a long term range that started back in 2015. On the downside, break of 0.9736 support is now needed to indicate completion of the rise from 0.9420. Otherwise, further rally will remain in favor in medium term.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 20:00 | NZD | RBNZ Rate Decision | 1.75% | 1.75% | 1.75% | |

| 23:50 | JPY | BOJ Summary of Opinions Oct Meeting | ||||

| 23:50 | JPY | Machine Orders M/M Sep | -8.10% | -2.00% | 3.40% | |

| 23:50 | JPY | Current Account (JPY) Sep | 1.84T | 2.05T | 2.27T | |

| 00:01 | GBP | RICS House Price Balance Oct | 1.00% | 4.00% | 6.00% | |

| 00:30 | AUD | Home Loans M/M Sep | -2.30% | 2.00% | 1.00% | 1.50% |

| 01:30 | CNY | CPI Y/Y Oct | 1.90% | 1.70% | 1.60% | |

| 01:30 | CNY | PPI Y/Y Oct | 6.90% | 6.60% | 6.90% | |

| 05:00 | JPY | Eco Watchers Survey Current Oct | 52.2 | 50.5 | 51.3 | |

| 06:45 | CHF | Unemployment Rate Oct | 3.10% | 3.10% | 3.10% | |

| 07:00 | EUR | German Trade Balance Sep | 21.8B | 23.1B | 21.6B | |

| 09:00 | EUR | ECB Economic Bulletin | ||||

| 10:00 | EUR | EU Economic Forecasts | ||||

| 13:30 | CAD | New Housing Price Index M/M Sep | 0.20% | 0.20% | 0.10% | |

| 13:30 | USD | Initial Jobless Claims (NOV 04) | 239K | 231K | 229K | |

| 15:00 | USD | Wholesale Inventories M/M Sep F | 0.30% | 0.30% | ||

| 15:30 | USD | Natural Gas Storage | 15B | 65B |

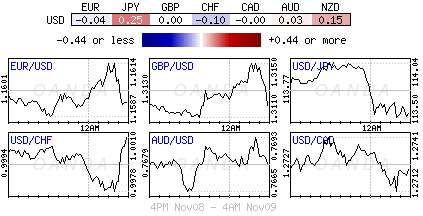

USDCAD Cracks Key Support at 1.2700 Zone

The pair remains in red on Thursday and hit two-week low at 1.2687 after probing below 1.2698 base and 20SMA at 1.2695. Loonie is supported by recent strength in oil prices and could extend advance against the US dollar. Firm break below 1.2700 support zone is expected to trigger stops parked below and spark fresh weakness towards 1.2628 (Fibo 61.8% of 1.2450/1.2916 upleg) and 1.2600 (Fibo 38.2% of 1.2061/1.2916 ascend. Mixed signals from daily chart studies could result in extended consolidation while 20SMA limits downside attempts. Extended upticks should be capped south-turning 10SMA (1.2788) to keep near-term bears off 1.2916 high in play.

Res: 1.2740; 1.2788; 1.2819; 1.2835

Sup: 1.2687; 1.2628; 1.2600; 1.2560

Canadian Dollar Edges Lower, Canadian Inflation Report Next

The Canadian dollar has posted losses in the Thursday session. Currently, USD/CAD is trading at 1.2700, down 0.22% on the day. On the release front, Canada releases the New Housing Price Index, while the US will publish unemployment claims.

Canadian housing numbers jumped on Wednesday, helping the Canadian dollar hold its own against the greenback. Housing Starts improved to 223 thousand, well above the forecast of 211 thousand. This matched the highest reading since March. There was more good news from Building Permits, which soared 3.8%, crushing the estimate of 0.7%. This follows two sharp declines.

On Tuesday, Bank of Governor Stephen Poloz on Tuesday, after Poloz maintained a neutral stance towards interest rates. Poloz said that the Bank continued to monitor how the economy was doing after rate hikes in July and September. The markets were caught off guard by the September move, and the Canadian dollar responded with strong gains. Poloz did not offer any insight as to future rate hikes, leaving the markets guessing regarding a December rate hike. Poloz added that he was not concerned that inflation remains below the BoC's target of 2 percent. The BoC will have to keep a close eye on the US, as the Federal Reserve is almost certain to raise rates in December. If the BoC does not match the hike, the Canadian dollar will likely weaken against the greenback.

GBPUSD Still Bearish Below 1.3130

The British pound continues to trade on the back-foot against the U.S dollar, with price-action caught in a narrow range between the 1.3109 and 1.3130 levels. The GBPUSD pair failed to participate in the broad-based sell-off in the U.S dollar index, during today's European session. Trading sentiment in the British pound remains weak, as delays in Brexit negotiations and UK political wrangling threaten the United Kingdom's economic outlook. Sterling traders now await the decision from the U.S Senate on the proposed Trump administration tax reforms.

The GBPUSD pair remains strongly bearish while trading below the 1.3130 level. Further declines towards the 1.3086 and 1.3036 levels appear the most likely scenario.

Should the U.S Senate disappoint later today, further upside towards the 1.3200 and 1.3268 levels remains likely.

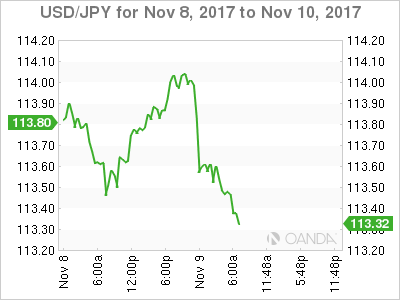

USDJPY Strongly Bearish Below 113.68 Level

The U.S dollar has fallen sharply against the Japanese Yen, hitting 113.23, as the U.S dollar index succumbs to heavy selling pressure. Foreign exchange traders are becoming nervous ahead of today's decision on the proposed tax reform plan, by the Trump administration. The USDJPY pair currently trades against the price-lows of the day, after breaching a number of key downside technical levels. Traders now await the latest news from the U.S Senate, which is expected to come shortly after the U.S opening bell.

The USDJPY pair remains strongly intraday bearish while trading below the 113.68 level, further downside towards the 112.90 and 112.30 levels is likely, if the Trump administrations tax plan falters.

Should the USDJPY pair regain the 113.68 level, further upside towards 113.89 and 114.24 seems possible if risk-on sentiment returns.

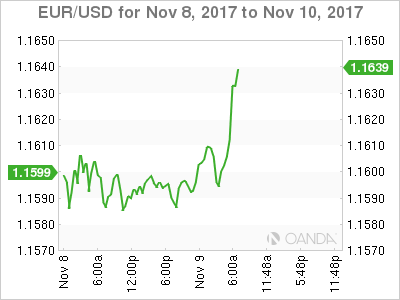

EURUSD – Pressure Builds Up On Corrective Recovery Higher

EURUSD - With the pair still holding on its recovery threats, further push higher is expected. Resistance comes in at 1.1650 level with a cut through here opening the door for more upside towards the 1.1700 level. Further up, resistance lies at the 1.1700 level where a break will expose the 1.1750 level. Its daily RSI is bullish and pointing higher suggesting further strength. Conversely, support lies at the 1.1550 level where a violation will aim at the 1.1500 level. A break of here will aim at the 1.1450 level. Below here will open the door for more weakness towards the 1.1400. All in all, EURUSD faces further corrective recovery threats.

Dollar’s Mixed Fortunes And Equities Wild Swings

Thursday November 9: Five things the markets are talking about

With little data on the docket this week investor's attention has focused on Asia, where Trump has embarked on an 11-day tour.

Overnight, it was no surprise that Trump said China is taking advantage of U.S workers and companies with unfair trade practices, but he managed to blame his predecessor rather than China for allowing the massive U.S. trade deficit to grow.

Elsewhere, Brexit talks resume this morning in Brussels with no indication that a breakthrough is anywhere close, while stateside, tax reform discussions remain ongoing and the broad uncertainty around the bill has the ‘mighty' dollar again under pressure.

Note: E.U officials are said to be planning for a ‘no deal' on Brexit or reversal of the decision before 2018 amid U.K PM May's more ‘fragile' leadership position.

1. Stocks wild swings

In Japan, equities ended down overnight after intraday swings took the Nikkei and Topix indexes to multi-decade highs only to plummet in afternoon trading. The Nikkei ended down -0.2%, while the broader Topix lost -0.3%.

In Hong Kong, stocks hit another decade-peak Thursday, with investor sentiment underpinned by China's strong inflation data that pointed to economic resilience. The Hang Seng index rallied +0.8%, while the China Enterprises Index jumped +1.5%.

In China, regional stocks rose on Thursday, led by the blue-chip index scaling a fresh two-year high, as investors were encouraged by strong inflation data that showed economic momentum remains robust. The blue-chip CSI300 index rose +0.7%, while the Shanghai Composite Index closed up +0.4%.

In Europe, indices are trading mixed with notable out performance in Italy as Banks outperform on comments from ECB's Nouy being open to delaying new rules on non-performing loans. Elsewhere, corporate earnings continue to be the focal point.

U.S socks are set to open in the ‘red' (-0.1%).

Indices: Stoxx600 -0.1% at 394.2, FTSE flat at 7528, DAX +0.1% at 13389, CAC-40 +0.1% at 5474, IBEX-35 +0.1% at 10236, FTSE MIB +0.5% at 22950, SMI flat at 9259, S&P 500 Futures -0.1%

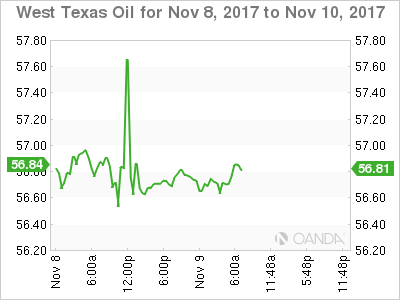

2. Oil prices stabilize, gold higher

Oil prices have steadied just below their two-year highs on Thursday, supported by supply cuts by OPEC and other major exporters including Russia.

Benchmark Brent crude is unchanged at +$63.49 a barrel. On Tuesday, Brent reached an intra-day high of $64.65; it's highest since June 2015. U.S light crude is also steady at +$56.81, not too far off this week's more than two-year high of +$57.69 a barrel.

Crude ‘bears' that this week's push higher – Brent is up by more than +40% since July – may have run its course due to increases in U.S supplies and some indicators of a demand slowdown.

Prices are still supported by efforts led by OPEC and Russia to withhold supplies in order to tighten the market and prop up prices.

Note: OPEC will discuss output during a meeting on Nov. 30, and is expected to extend the limits beyond their expiry in March 2018.

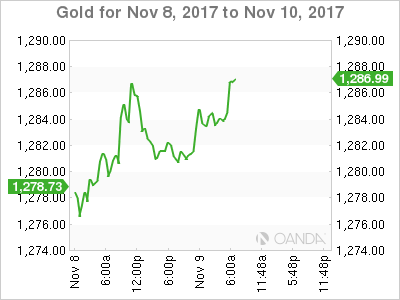

Ahead of the U.S open, gold prices have edged a tad higher overnight, one day after marking an intraday three-week high, as the dollar eased. Spot gold has rallied +0.2% at +$1,283.91 per ounce. Yesterday, it rose +0.4% and touched it's highest since Oct. 20 at +$1,287.13 an ounce.

3. Sovereign yield curves remain tight

Sovereign and U.S Treasury prices have barely moved, with curves consolidating at their flattest levels in nearly a decade.

The yield on U.S 10's have sank -2 bps to +2.31%, the lowest in more than three-weeks. In Germany, 10-year Bund yields are unchanged at +0.33%, the lowest in two-months, while in the U.K, the 10-year Gilt yield has declined less than -1 bps to +1.223%, the lowest in two-months.

Note: Yesterday's U.S Treasury +$24B 10-year note auction came down at +2.314% with a bid-to-cover of 2.48 vs. 2.23 prior and 2.27 over the las ten auctions.

The Reserve Bank of New Zealand kept policy unchanged in its Thursday decision but indicated an interest rate hike could come sooner thanks to a pick-up in inflation. The kiwi surged. The RBNZ left Cash Rate (OCR) unchanged at +1.75% and noted that Kiwi employment growth had been strong.

4. The Dollar's mixed fortunes

On the whole, the FX market remains relatively subdued, but the USD is beginning to face some headwinds as the US-lead Republican tax-reform plan is coming under some heavy scrutiny.

GBP/USD (£1.3096) is a tad lower outright, as market focus now shifts back to the sixth round of monthly Brexit talks between the U.K and E.U officials. There are some doubts beginning to fester on whether the E.U would feel comfortable in moving to the second phase of talks when E.U leaders meet again next month. Again, U.K political and economic uncertainty leaves the pound vulnerable.

Note: PM May has suffered the second resignation in a week from her cabinet Wednesday as Priti Patel resigned as international development secretary.

USD/JPY (¥113.46) is also lower as the Yen firmed following the Nikkei Stock Average reversal of its wild intraday +2% gain overnight. The index ended the session -0.2% lower, after breaching 23,000 for the first time in 25-years.

5. China inflation data suggest economy strong

Data overnight showed that China's producer prices were surprisingly strong in October, while consumer inflation picked up pace, suggesting the world's second largest economy remains robust, easing market concerns of a slowdown.

Chinas price pressures remain strong on the back of still rapid economic growth, a tight labour market, capacity cuts and temporary disruptions to industrial production

China OCT CPI m/m: +0.1% vs. +0.2%e; y/y: +1.9% (highest since Jan reading of +2.5%) vs. +1.8%e. PPI y/y: +6.9% vs. +6.6%e.

DAX Edges Lower Despite Sharp German Trade Surplus

The DAX has lost ground in the Thursday session. Currently, the DAX is at 13,346.50, down 0.27% on the day. On the release front, Germany’s trade surplus improved to EUR 21.8 billion, easily beating the forecast of EUR 21.6 billion. The EU will release its economic forecast, which provides analysis and economic activity of the 28 EU members.

Stock markets are sensitive to corporate earnings, and disappointing numbers on Tuesday pushed the DAX down 1.0 percent. Financial stocks were in red territory – Deutsche Bank dropped 0.59% and Commerzbank slid 1.53 percent. The DAX remains under pressure on Thursday.

The eurozone economy continues to impress in 2017, and retail sales, the primary gauge of consumer spending, rebounded sharply in September. The reading of 0.7% came after two straight declines, and marked the strongest gain since February. Consumer confidence is high, and the markets are hoping for stronger consumer spending in the fourth quarter.

German coalition talks are gaining steam, as President Angela Merkel has convinced potential partners to drop key demands. Merkel’s conservative bloc saw its support erode in the election, and needs the support of two smaller parties – the Greens and the liberal FDU. After intense negotiations, the Greens have dropped a demand on the phase-out of fossil fuels. The FDU wanted to lower taxes by 30-40 billion euros, but has agreed to more moderate tax cuts. Merkel has been under pressure from her own bloc to tighten immigration policy, but the Greens are opposed to such a move. If the talks continue to progress, Merkel could have a government in place in December.

Japan 225 Index Remains Bullish Despite Reversal From Multi-Decade High, Looks Overstretched In Short-Term

The Japanese 225 index hit a multi-decade high of 23,414 earlier in the day before reversing to last stand 0.9% lower relative to yesterday’s close.

Despite the decline, the index remains bullish in the short-term as indicated by technical indicators. The Tenkan-sen line being above the Kijun-sen line is a positive alignment pointing to bullish momentum in the short-term. The RSI supports this view as it has been advancing in recent days. Notice though that the indicator is currently at 75, exceeding the 70-overbought level.

The stochastics are painting a negative intra-day picture though: the %K line has crossed below the slow %D line with both lines currently heading lower.

On the upside, the area around the 23,000 mark, which was breached earlier in the day, could provide some resistance. Further above, the range around today’s multi-decade high of 23,414 might constitute an additional barrier in case of stronger bullish movement.

Should the index decline, the area around the current level of the Tenkan-sen at 22,624 might act as support. Further below, the range around the Kijun-sen at 22,004 could be significance, providing support as well.

The index has gained considerably over the last two months after in large part moving sideways in the preceding few months. It currently trades above the 50- and 100-day moving averages (MAs), as well as above the Ichimoku cloud. Both MAs are positively-sloped, while a bullish (golden) cross was recorded around mid-October when the 50-day MA moved above the 100-day one. All these are supporting a bullish medium-term picture.

Overall, the index is bullish in both the short- and medium-term though that are signs that it might be overstretched

Banxico To Stay On Hold, Bitcoin Reverses Gains Amid Fork Cancellation

Bitcoin tumbles after SeWit2x fork cancellation

The price of Bitcoin flash crashed yesterday at around GMT 18:00 after Mike Belshe, CEO of BitGo, published a note explaining the reasons why they will not support the Segwit2x fork. The note was also signed by Wences Casares (CEO Xapo), Jihan Wu (Bitmain), Jeff Garzik (Bloq), Peter Smith (CEO Blockchain) and Erik Voorhees (CEO Shapeshift). The note explains that the initial purpose of SegWit2X was to improve Bitcoin scalability but also to reduce fess, which are quite elevated. However, this should be done by keeping the community together, Belshe explains, which cannot be done will only 30% support among miners. He regrets that they “have not built sufficient consensus for a clean blocksize upgrade at this time'.

Following the publication of the note, the price of Bitcoin exploded to $7,900 before falling as low as $6,978 at certain exchanges (13% move in less than 2 hours). The price finally stabilized at around $7,300 yesterday evening. Nevertheless, Bitcoin came under renewed selling pressing on Thursday morning as investors continues to price out the fork.

It is also worth mentioning that there were rumours that a small group miners (that represents only 30% of hash power) will carry out the fork. However, it seems that investors are not buying it as the price of BTC resumed its debasement. On the bright side, alt-coins have rallied strongly as investors sell BTC and reallocate their portfolio.

Mexico: Overnight rate should remain on hold

Banxico will likely keep its interest rates steady tonight at 7%. There are many reasons for that. First of all, inflation expectations are now getting lower as the central bank certainly raised too strongly the overnight rate by anticipating a stronger Fed tightening rate path. Indeed, at least 4 rate hikes were expected by markets from the Fed. Now that the Fed is on hold until December meeting, there is no rush for Banxico to act.

We recall that the Mexican central bank is monitoring the interest rate differential between the US in order to avoid any potential capital outflow. A narrow rate differential is clearly not at the advantage of Mexico but now the spread is so large that investors have a preference for the Mexican Peso which offers strong return.

However, the Fed will certainly raise rates one more time in December but we don’t believe this is going to go any higher at least in the medium-term or it will likely trigger the burst of the bond bubble.

Currency-wise, the MXN has strengthened from 22 to 16 MXN for one single dollar note which is why we have seen Mexican’s inflations expectations suffering. Right now, Fed monetary policy have driven the USD higher against the MXN and we believe that it is likely that we see Banxico reducing their overnight rate next year which would send the MXN lower. The MXN is overvalued at the moment.