Sample Category Title

USD/JPY Ready To Bounce Back

USD/JPY is riding uptrend channel below former resistance at 114.49 (11/07/2017 high). Strong support is located at a distance at 111.12 (20/09/2017 low).

We favor a long-term bearish bias. Support is now given at 99.02 (10/08/2013 low). A gradual rise towards the major resistance at 125.86 (05/06/2015 high) seems unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

GBP/USD Ready For A Triple Top Below 1.32

GBP/USD is monitoring 1.32. Support is given at 1.3027 (06/10/2017 low). Resistance area is given around 1.3200. Expected to show further increase,.

The long-term technical pattern is reversing. The Brexit vote had paved the way for further decline. Long-term support can be found at 1.1841 (07/10/2017 low). Long-term resistance given around 1.35 is at stake and indicates a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

EUR/USD Consolidating Around 1.16

EUR/USD is still biased to the downside after breaking hourly support at 1.1575 (27/10/2017 low). Hourly resistance is located at 1.1658 (30/10/2017 high). Expected to show some shortterm consolidation.

In the longer term, the momentum is now turning largely positive. We favour a continued bullish bias. Key resistance is holding at 1.2252 (25/12/2014 high) while strong support lies at 1.0341 (03/01/2017 low).

NZDUSD Tracking Higher After Bouncing Off Multi-Month Low

NZDUSD made a recovery off the 0.6817 area, which is a level at the bottom of a multi-month range. On the 4-hour chart, the pair is slowly tracking higher in a slow sideways range. But the short-term outlook is looking bullish after a bullish signal was given by the crossing of the 20 and 50-period moving averages.

Immediate support is at 0.6944. A drop below this would see prices target the 20-period MA at 0.6923 and then from here the 50-period MA is at 0.6903. Further support lies at the November 6 low at 0.6874 before reaching the range-low at 0.6817.

Rising above the 0.6976 high would see prices push higher towards the key psychological 0.7000 level. A continuation in a rally would target another psychological level at 0.7200 ahead of the September 20 high of 0.7434.

Market Update – European Session: Focus On Monthly Round Of UK/EU Brexit Talks

Notes/Observations

Brexit negotiations are set to resume Thursday; question whether the Dec Summit would approve the stage for phase 2 of talks

ECB SSM chief Nouy seemed open to delaying controversial new rules on non-performing loans that are due to go into effect at the beginning of next year.

Sweden Central Bank Minutes hints that members are appearing more split on its 2018 policy strategy

RBNZ welcomed the recent fall in the currency as it boosts tradables inflation

US Republican tax-reform plan in the remained under scrutiny; details expected later today

Overnight

Asia:

New Zealand Central Bank (RBNZ) left Cash Rate (OCR) unchanged at 1.75%. Noted that NZD currency (Kiwi) had eased and if sustained would increase inflation. Employment growth had been strong;

Bank of Japan (BOJ) Summary of Opinions at Oct. 30-31th Meeting note that its current policy was most appropriate. Should persistently continue with current easing but monitor effects. BoJ was taking extreme steps to achieve its price target

China Oct CPI registers its highest annual pace since Jan (Y/Y: 1.9% v 1.8%e)

China Commerce Ministry (MOFCOM) Official Zhong Shan: Deals between the US and China reached $253.4B (in-line with recent speculation)

Europe:

EU officials said to be planning for a ‘no deal’ on Brexit or reversal of the decision before 2018 amid UK PM May’s more ‘fragile’ leadership position. EU said to be giving Britain 2-3 weeks to set out how much it’s prepared to pay in Brexit settlement, warning that otherwise they would struggle to prepare this year for a transition deal the UK was requesting

BOE’s McCafferty (dissenter) stated that could not say when more rate hikes would occur. Inflation forecast based on 2 more rate increases over 3 year horizon period (in-line with MPC majority). No big differences among MPC members about the trajectory for rates. If inflation picked up, would have to look at range of factors when considering rates

German Bundesbank's Dombret (ECB SSM member): some banks aren't sufficient prepared for Brexit

Americas:

Banking Committee sets Nov 28th for proposed Fed chair Powell hearing

Treasury Sec Mnuchin: there are short term concerns about the impact of FX on trade; dollar strength is partly a reflection of the US economy. Hope for debt ceiling increase in December; govt could fund itself at least through January. Starting to look at filling the other empty Fed board seats; there was no specific criteria for Vice Chair; Yellen had not decided whether to stay at Fed when term ends in 2024

Economic Data

(CH) Swiss Oct Unemployment Rate: 3.0% v 3.0%e, Unemployment Rate (Seasonally Adj): 3.1% v 3.1%e

(DE) Germany Sept Current Account: €25.4B v €23.5Be; Trade Balance: €24.1B v €22.3Be, Exports M/M: -0.4% v -1.3%e; Imports M/M: -1.0% v +0.3%e

(MY) Malaysia Central Bank (BNM) left its Overnight Policy Rate unchanged at 3.00% (as expected)

(FR) Bank of France Oct Business Sentiment: 106 v 105e

(CZ) Czech Oct CPI M/M: 0.5% v 0.3%e; Y/Y: 2.9% v 2.7%e

(HU) Hungary Oct CPI M/M: 0.3% v 0.4%e; Y/Y: 2.2% v 2.3%e

(PH) Philippines Central Bank (BSP) left its Overnight Borrowing Rate unchanged at 3.00% (as expected)

Fixed Income Issuance:

(SE) Sweden sold SEK500M in I/L 2027 Bonds; Avg Yield: -1.1505% v -1.277% prior; Bid-to-cover: 2.09x v 1.95x prior

(IE) Ireland Debt Agency (NTMA) sold total €1.25B vs. €1.0-1.25B indicated range in 2026 and 2045 IGB Bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 -0.1% at 394.2, FTSE flat at 7528, DAX +0.1% at 13389, CAC-40 +0.1% at 5474, IBEX-35 +0.1% at 10236, FTSE MIB +0.5% at 22950, SMI flat at 9259, S&P 500 Futures -0.1%]

Market Focal Points/Key Themes:

European Indices trade mixed this morning with notable out performance in Italy as Banks outperform on comments from ECB SSM chief Nouy being open to delaying new rules on Non performing loans.

Elsewhere earnings continued to be the focal point with a raft of big cap names reporting. Dax components Siemens, Adidas, Merck and Munich Re reported mixed results, whilst in the UK Sainsbury's trades lower after lower H1 profits, Burberry is having its worst day in 5 years after medium term guidance implying flat growthm while Vestas Wind is another notable faller after missing on the top and bottom line.

Looking ahead notable earners include retailers Macy's, Office Depot and Kohls.

Equities

Consumer discretionary [Sainsburys [SBRY.UK] -3.0% (Earnings), Adidas [ADS.DE] -1.7% (Earnings), Burberry [BRBY.UK] -10% (Earnings)]

Industrials: [Siemens [SIE.DE] -2.0% (Earnings)]

Financials: [Munich Re [MUV2.DE] +1.3% (Earnings), Unicredit [UCG.iT] +3.3% (Earnings), Commerzbank [CBK.DE] +3.5% (Earnings),

Aegon [AGN.NL] +5.3% (Earnings)]

Telecom: [ City Fibre [CUTY.UK] +25% (Agreement with Vodafone)]

Healthcare: [Astrazeneca [AZN.UK] +1.6% (Earnings)]

Energy: [ VestasWind [VWS.DK] -20% (Earnings)]

Speakers

ECB Economic Bulletin was in-line with Draghi’s post rate decision press conference. Risks surrounding growth remain broadly balanced. SPF survey pointed to unabated growth momentum in H2 of 0217. Headline inflation likely to temporarily decline towards end of 2017

ECB’s Coeure (France): Nothing justifies the end of ECB support to growth (in-line with Council view). Private debt was more worrying than public debt. Public debt was a concern but not a financial risk

ECB’s Nouy (SSM chief): ECB sees a need to step up Brexit preparations and will continue to ask banks to do so as well. Now is the right time for additional steps on NPLs; ECB to carefully consider all comments before finalizing the draft addendum

ECB lowered emergency liquidity assistance (ELA) cap for Greece banks from €28.6B to €26.9B

Sweden Central Bank (Riksbank) Oct Minutes: Several members discussed housing market developments

Riksbank Gov Ingves: Fulfillment of inflation target was currently good while global inflationary pressures were subdued. If Riksbank made policy less expansionary and deviate from other central banks then the SEK currency (Krona) would risk appreciating too quickly

Riksbank Dep Gov Ohlsson: Believed that Riksbank should signal hike in early 2018

Riksbank Member Skingsley: No need to change current policy balance but not ruling out supporting further stimulus

Riksbank member Member Floden: Economic and inflation outlook unchanged; did not expect to advocate for an extension to the QE bond buying program. Appropriate to leave rates unchanged until mid-2018

China and US said to agreed to boost coordination on monetary and forex policies

Malaysia Central Bank policy statement noted that its monetary policy stance remained accommodative but might consider reviewing stance given the strength of global and domestic macroeconomic conditions. Headline inflation seen moderating in 2018 while domestic demand is expected to remain key source of growth in 2018

Philippines Central Bank policy statement noted that its current policy setting remained appropriate as the CPI outlook remained manageable. Inflation to settle within target in both 2017 and 2018 and near the mid-point over the policy horizon

Currencies

FX markets were subdued with the USD facing some headwinds as the US-lead Republican tax-reform plan in the remained under scrutiny

GBP/USD was slightly lower and hovering just under the 1.31 area. Focus was on the 6th round of monthly Brexit talks between UK and EU officials. Some doubts are bubbling whether the EU would feel comfortable in moving to the 2nd phase of talks when EU Leaders meet in Dec. GBP holding up despite some self-destruction within the UK cabinet (Priti Patel resigned as international development sec).

USD/JPY was lower and currently below 113.50 level. The Yen firmed following the Nikkei Stock Average reversal of its earlier 2% gain. The Index ended the session 0.2% lower, after breaching 23000 for the first time since January 1992.

Fixed Income

Bund futures trade at 163.37 up 13 ticks, as Wednesday’s mid-session reversal ultimately saw the rally faded. Support lies at 162.00, followed by 161.50. Resistance stands initially at 163.51, followed by 164.25.

Gilt futures trade at 125.56 up 11 ticks and still near the November high. Continued upside eyeing 125.75 then 126.47. Downside targets include 124.90 then 124.24.

Thursday’s liquidity report showed Wednesday’s excess liquidity rose to €1.873T from €1.872T and use of the marginal lending facility climbed to €515M from €238M

Looking Ahead

(EG) Egypt Oct Urban CPI Y/Y: No est v 31.6% prior; CPI Core Y/Y: No est v 33.3% prior

(UK) EU/UK Begin 2-day round of monthly Brexit negotiations

05:30 (HU) Hungary Debt Agency (AKK) to sell Bonds

05:30 (PL) Poland to sell Bonds

05:30 (UK) DMO to sell £2.75B in 0.75% 2023 Gilts

06:00 (BR) Brazil CONAB Crop Report

06:00 (PT) Portugal Sept Trade Balance: No est v -€1.3B prior

06:00 (IE) Ireland Oct CPI M/M: No est v -0.6% prior; Y/Y: No est v 0.2% prior

06:00 (IE) Ireland Oct CPI EU Harmonized M/M: No est v -0.6% prior; Y/Y: No est v 0.2% prior

06:00 (ZA) South Africa Sept Manufacturing Production M/M: 0.0%e v 0.3% prior; Y/Y: 0.6%e v 1.5% prior

07:00 (CZ) Czech Central Bank comments on Oct CPI

07:50 (EU) ECB's Villeroy (France) speaks in Brussels

08:00 (RU) Russia Gold and Forex Reserve w/e Nov 3rd: No est v $424.5B prior

08:00 (RU) Russia Oct Official Reserve Assets: No est v $425.5B prior

08:00 (UK) Oct NIESR GDP Estimate: No est v 0.4% prior

08:05 (UK) Baltic Dry Bulk Index

08:15 (LX) ECB’s Mersch (Luxembourg) in Vienna

08:30 (US) Initial Jobless Claims: 232Ke v 229K prior; Continuing Claims: 1.89Me v 1.884 M prior

08:30 (US) Weekly USDA Net Export Sales

08:30 (CA) Canada Sept New Housing Price Index M/M: 0.2%e v 0.1% prior; Y/Y: 3.8%e v 3.8% prior

08:45 (PT) ECB’s Constancio (Portugal) in Rome

09:00 (MX) Mexico Oct CPI M/M: 0.6%e v 0.3% prior; Y/Y: 6.4%e v 6.4% prior; CPI Core M/M: 0.2%e v 0.3% prior

09:00 (BR) Brazil to sell Fixed Rate 2023 and 2027 Bonds

09:00 (BR) Brazil to sell 2018, 2019 and 2021 LTN Bills LTN

10:00 (US) Sept Final Wholesale Inventories M/M: 0.3%e v 0.3% prelim; Wholesale Trade Sales M/M: 0.9%e v 1.7% prior

10:00 (FR) ECB’s Villeroy (France) in Brussels

10:30 (US) Weekly EIA Natural Gas Inventories

11:00 (US) Treasury announcement for 10-year TIPS auction for Nov 16th

11:30 (CH) SNB chief Jordan in Frankfurt

12:00 (US) USDA World Agricultural Supply and Demand Estimate (WASDE) Crop Report

12:00 (US) GOP Senate to release details of tax bill

13:00 (DE) ECB’s Weidmann (Gernmany)

13:00 (US) Treasury to sell $15B in 30-Year Bonds

13:20 (DE) ECB’s Lautenschlaeger at conference in Washington DC

14:00 (MX) Mexico Central Bank (Banxico) Interest Rate Decision: Expected to leave Overnight Rate unchanged at 7.00%

16:45 (NZ) New Zealand Oct Card Spending Retail M/M: No est v 0.1% prior; Total M/M: No est v -0.1% prior

18:00 (PE) Peru Central Bank (BCRP) Interest Rate Decision: Expected to leave Reference Rate unchanged at 3.50%

Technical Outlook: US Crude At The Back Foot After Disappointing US Oil Inventories Data

WTI oil stands at the back foot on Thursday after previous day’s action closed in red. Oil price fell on Wednesday on disappointing US data which showed a build in oil inventories by 2.2 million barrels, against forecasted draw of 2.8 million barrels.

Oil price pulled back after hitting new multi-month high at $57.90, closing in red for the second day.

Wednesday’s daily candle with long upper shadow also signals heavy upside and risks deeper pullback.

Overextended daily studies support the notion as RSI is overbought and slow stochastic is reversing from overbought territory.

Stronger bearish signal could be expected on violation of rising 10SMA ($55.54), while extended consolidation is seen while the latter holds.

Break below 10SMA would risk extension towards $54.53 (Fibo 38.2% of $49.09/$57.90 ascend).

Res: 57.00, 57.67, 57.90, 59.04

Sup: 56.67, 56.40, 55.82, 55.54

Euro Hugging 1.16, US Jobless Claims Next

The euro continues to have a quiet week, as it stays close to the 1.16 line. In the Thursday session, EUR/USD is trading at 1.1607, up 0.11% on the day. On the release front, Germany’s trade surplus improved to EUR 21.8 billion, easily beating the forecast of EUR 21.6 billion. The EU will release its economic forecast, which provides analysis and economic activity of the 28 EU members. In the US, today’s key highlight is unemployment claims, which is expected to edge higher to 232 thousand.

German coalition talks are gaining steam, as President Angela Merkel has convinced potential partners to drop key demands. Merkel’s conservative bloc saw its support erode in the election, and needs the support of two smaller parties – the Greens and the liberal FDU. After intense negotiations, the Greens have dropped a demand on the phase-out of fossil fuels. The FDU wanted to lower taxes by 30-40 billion euros, but has agreed to more moderate tax cuts. Merkel has been under pressure from her own bloc to tighten immigration policy, but the Greens are opposed to such a move. If the talks continue to progress, Merkel could have a government in place in December.

After failing to pass a new healthcare act, President Trump has his sights set on tax reform, a key item in his domestic platform. Trump wants Congress to pass legislation overhauling the tax code before the end of the year, but that could prove to be too tight of a deadline. Most Democrats have come out against the proposal, and not all Republicans are on board. The bill would cut corporate taxes from 35% to 20%, but predictably, Democrat and Republican lawmakers are at odds as to whether the bill will lower taxes for the middle class. The bill is presently being debated in a congressional committee and is expected to move to the House floor next week. The Senate will present its version of the bill on Thursday, so we can expect plenty of activity in Congress in the next few weeks. Tax reform faces an uphill battle, which has weighed on investor risk appetite and pushed gold prices higher.

The US labor market remains very strong, and this was reflected in another sharp employment report on Tuesday. JOLT Jobs Openings was almost unchanged at 6.09 million, easily beating the forecast of 5.98 million. Unemployment claims are also expected to show little movement on Thursday, with a forecast of 232 thousand. The unemployment rate is at a sizzling 4.1%, but wage growth remains a concern, reflective of weak inflation. In October, Average Hourly Earnings posted a flat 0.0%, the first time wages have not increased since November 2016.

Daily Technical Analysis: EURUSD, GBPUSD, USDJPY, USDCHF

EURUSD

The EURUSD didn't make significant movement yesterday. The bias remains neutral in nearest term. Overall I remain bearish as a part of the “head and shoulders” formation with nearest target seen at 1.1450 but need a clear break below 1.1580/50 to continue the bearish run. Immediate resistance remains around 1.1650/70 region. A clear break above that area could trigger further bullish pressure testing 1.1725 but as long as stay below 1.1900 I remain bearish and any upside pullback should be seen as a good opportunity to sell.

GBPUSD

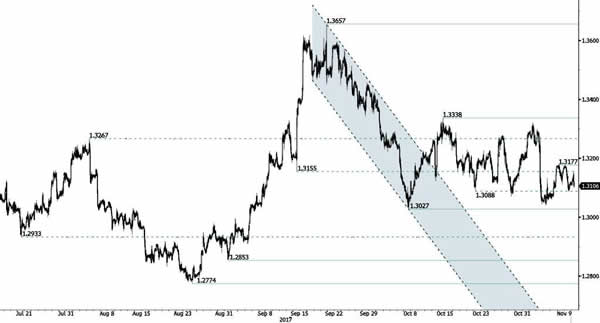

The GBPUSD had a bearish momentum yesterday bottomed at 1.3086, touched the trend line support as you can see on my daily chart below. The bias is bearish in nearest term testing 1.3000 key support which remains a good place to buy with a tight stop loss. Immediate resistance is seen around 1.3130. A clear break above that area could lead price to neutral zone in nearest term testing 1.3200 region but key resistance remains at 1.3330 area. On the downside, a clear break below 1.3000 would stop the major bullish trend with a potential bearish reversal scenario.

USDJPY

The USDJPY was indecisive yesterday. Price attempted to push lower bottomed at 113.39 but closed higher at 113.86 and hit 114.06 earlier today in Asian session. The bias is neutral in nearest term. The bearish pin bar scenario remains valid but need a clear break below 113.20 to confirm further bearish scenario testing 112.25 – 111.65 region. Immediate resistance is seen around 114.50 which remains a good place to sell with a tight stop loss. Overall I remain neutral.

USDCHF

The USDCHF had another insignificant movement yesterday. Price is still trapped between 1.0037 – 0.9940 range area. We need a clear break from that range area to see clearer direction. Overall I remain bullish but need a clear break above 1.0037 to resume the bullish trend targeting 1.0100 or higher. On the downside, a clear break and daily close below 0.9940 would expose 0.9835 support area.

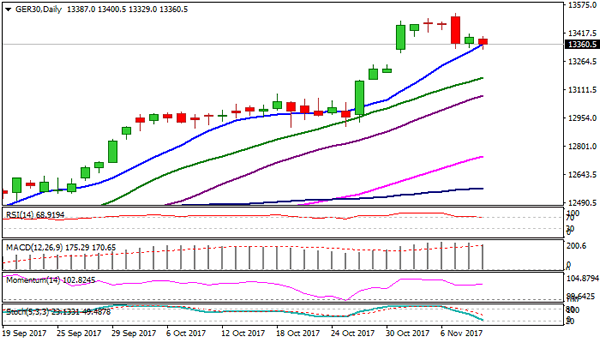

Technical Outlook: DAX – Consolidation Under New All-Time High Remains Supported By Rising 10SMA

DAX remains at the back foot on Thursday and consolidating within narrow range after pulling back strongly from fresh all-time high at 13530. Dips were so far contained by rising 10SMA (13359) which marks initial support and trigger for deeper pullback on firm break below it. Daily RSI is attempting to reverse from overbought territory and has formed bearish divergence, could trigger stronger bearish signal on break lower. Also, MACD bearish divergence adds to existing pressure, however, sustained break below 10SMA is needed to signal further easing, which could stretch towards rising 20SMA (currently at 13174).

Res: 13417, 13501, 13555, 13618

Sup: 13359, 13244, 13174, 13144

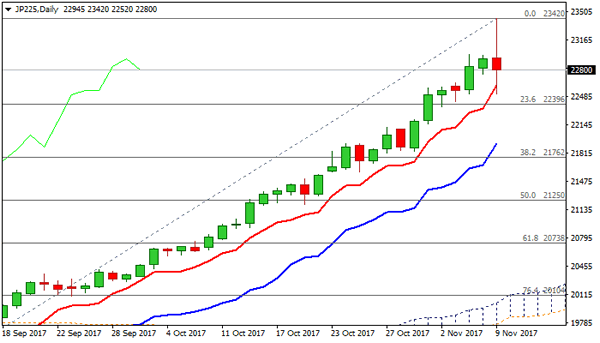

Technical Outlook: Nikkei 225 Is Consolidating After Sharp Fall, Further Downside Favored

Nikkei 225 index for December delivery collapsed in Asia on Thursday after initially rallying to fresh multi-year high at 23420.

Sharp fall spiked to 22520 low, denting initial support at 22618 (daily Tenkan-sen) but subsequent bounce made probes below 22618 short-lived for now.

The index remains in steep uptrend in past two months which requires correction. Overextended daily studies generated initial signal, with slow stochastic already reversed from overbought zone while daily RSI is turning south, deep in the overbought territory.

Close below pivotal supports at 22618 (Tenkan-sen) and 22413 (10SMA) is needed to generate stronger bearish signal for extension towards 22396 (Fibo 23.6% of 19080/23420 ascend), with further easing to challenge rising 4-hr cloud (spanned between 223025 and 22088).

Initial resistance lies at 22858 (broken hourly cloud top), followed by converged hourly Tenkan-sen / Kijun-sen (22970) and 23000 zone where extended upticks should be capped to keep in play freshly established near-term bears.

Res: 22858, 22970, 23000, 23076

Sup: 22708, 22680, 22618, 22520