Sample Category Title

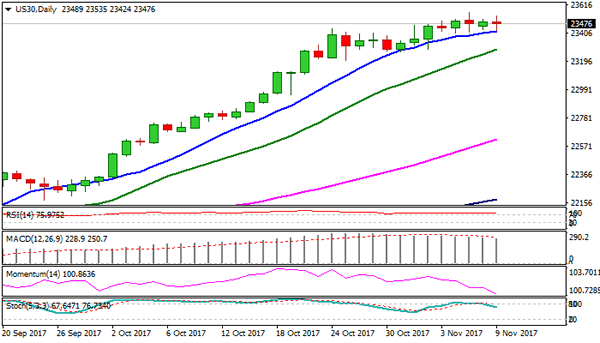

Technical Outlook: Dow Jones – 10SMA Holds Consolidation For Now But Deeper Pullback Could Be Anticipated

Dow Jones is consolidating under fresh all-time high at 23555 posted earlier this week, with firm bullish structure remaining in play, despite strongly overbought daily studies. The price is holding above rising 10SMA (23419) which tracks ascend in past two months and marks initial support. Slow stochastic has already reversed on daily chart with overbought RSI and bearish divergence formed on RSI/MACD, suggesting that corrective action should be anticipated. Initial trigger will be close below 10SMA which would open way towards next solid supports at 23283 (rising 20SMA) and 23270 (30/31 Oct higher base). Break here would signal deeper correction. Meanwhile, extended consolidation is seen as likely near-term scenario while 10SMA contains (10SMA is still heading north and showing no signs of fatigue) with fresh upticks not ruled out.

Res: 23535, 23555, 23777, 23936

Sup: 23419, 23283, 23200, 23160

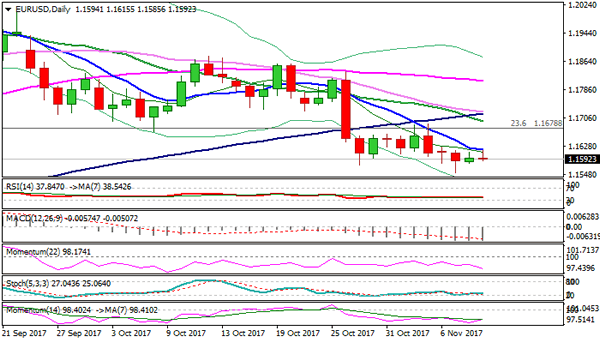

Technical Outlook: EURUSD – 10 SMA Continues To Cap Recovery Attempts

The Euro is slightly bid in early Thursday's trading and holding around 1.1600 handle, but so far without significant upside action.

Key barriers at 1.1618/22 (10SMA / Tenkan-sen) are still capping, with break here needed to generate bullish signal for further advance.

Broken bearish flag support line at 1.1648 and broken H&S pattern neckline at 1.1674 are next barriers which guard pivotal 1.1700 resistance zone.

Break here is needed to signal reversal.

On the downside, Fibo support at 1.1510 remains as near-term target, with bearish daily studies keeping focus shifted lower.

No important releases from the Eurozone scheduled today and the single currency is expected to mainly driven by techs.

Res: 1.1622, 1.1648, 1.1674, 1.1690

Sup: 1.1580, 1.1553, 1.1510, 1.1445

Forex: Kiwi Gets A Boost

Earlier today the Reserve Bank of New Zealand (RBNZ) left their Official Cash Rate (OCR) unchanged at a record low of 1.75% – as the markets had forecast. More importantly was the RBNZ revising inflation forecasts upwards, which is likely to signal an increase in interest rates earlier than previously predicted. RBNZ acting Governor Spencer stated after the announcement “Monetary policy will remain accommodative for a considerable period,” & “the exchange rate has eased since the August statement and, if sustained, will increase tradables inflation and promote more balanced growth.” The RBNZ had set an inflation target of between 1% and 3% and now expects inflation to reach 2% in Q2 of 2018, a full 3 quarters earlier than previously expected. Because of inflationary pressure, the markets are forecasting a rate hike by the end of next year. Following the announcement, NZDUSD rose from around 0.6922 to just above 0.6970. NZDUSD has suffered in the second half of this year, after reaching a high in July of around 0.7550 the Kiwi slumped to lows around 0.6830 earlier this month. Today’s announcement gives a much needed “boost” to the Kiwi.

Wednesday’s EIA report surprised the markets with an unexpected increase of oil inventories. The markets had been expecting another drawdown around -2.8M that continues a trend seen over the past few releases. For the week ending November 3rd US Crude Oil inventories rose 2.2M as supplies increased, while production jumped to a record all-time high. The major focus is the fact that US production increased 67,000 bpd to 9.62 Million bpd – the highest since data was readily available in 1983. The increase in US production can only undermine OPEC’s supply cuts to boost the price of crude.

EURUSD is unchanged in early Thursday trading at around 1.1600.

USDJPY is -0.25% lower, currently trading around 113.55.

GBPUSD is 0.15% higher in early trading at around 1.3135.

NZDUSD is currently trading around 0.6960.

Gold is 0.30% higher, currently trading around $1,285.

WTI is currently trading -0.20% lower at around $56.95.

Major data releases for today:

At 09:00 GMT, the European Central Bank launches a new publication, the Economic Bulletin, to replace the ECB Monthly Bulletin. It will be published two weeks after each Governing Council meeting.

At 10:00 GMT, the European Commission will release Economic Growth forecasts as compiled by the Directorate General for Economic and Financial Affairs (DG ECFIN).

At 13:30 GMT, the US Department of Labour will release Initial Jobless Claims for the week ended November 3rd and Continuing Claims for the period ended October 27th. The previous release of Initial Claims of 229K is expected to be bettered, with forecasts calling for a release of 232K. Continuing Claims are expected to come in at 1885K, a minor increase on the previous release of 1884K. Any significant deviation from forecast will see USD volatility.

At 15:00 GMT, the UK National Institute of Economic and Social Research will release an estimate of UK GDP. This release occurs 1 month before the official GDP release and could result in GBP volatility.

At 16:30 GMT, Swiss National Bank Chairman Thomas Jordan is scheduled to speak at the CFS Presidential Lectures in Frankfurt, Germany on the subject: “Independence of Central Banks after the Financial Crisis: The Swiss Perspective”.

USDJPY Neutral In Short-Term After Bullish Phase Stalls At Top Of Broader Range

USDJPY has been range-bound during the past 2 weeks, trading at the top of a broader 7-month range. The short-term bullish phase has lost momentum as indicated by the RSI.

The pair has been trading within a range of 112.95 and 114.73 since October 23 following a steady rise off the 108.00 area. Ichimoku cloud analysis is showing that the Tenkan-sen and Kijun-sen lines are positively aligned but are shifting to neutral.

USDJPY is starting to come under pressure but immediate support is expected at 113.17. Failure to hold at this level would shift the market’s focus to the downside. A sustained break of the key 113.00 level could lead to an extension lower towards the 200-day moving average (111.72). From here the near-term outlook starts to look bearish with scope to fall towards the bottom of the range in the 108.00 area.

To the upside, immediate resistance lies at 114.00, which if broken, would see a re-test of Monday’s high at 114.73. Rising above this top would take prices to the next peak at 115.50 hit in March. From here there is little resistance until the 118.00 handle.

In the bigger picture, the trend is neutral but the short-term bullish phase has stalled and is at risk of reversing if there is continued rejection at the 114.00 area.

Kiwi Rallies As RBNZ Signals Faster Inflation, Aussie Climbs On Chinese Inflation

The kiwi recorded a strong rebound on late Wednesday, flying to a two-week high after the RBNZ left rates unchanged but raised expectations that future hikes might emerge earlier than anticipated. The aussie posted some gains early on Thursday as China, Australia’s main export partner, released stronger than projected annual CPI figures.

As it was mainly expected, the RBNZ policymakers decided to keep rates steady at a record low level of 1.75%. However, what pushed the kiwi higher was a statement highlighting that policymakers are anticipating inflation to reach the 1-3% RBNZ target a year earlier than expected, with the central bank’s governor, Grant Spencer, saying that “GDP growth will be fast for longer, inflation will be higher, the unemployment rate will be lower and interest rates may have to rise a bit earlier in 2019.” Moreover, the RBNZ claimed that fiscal stimulus from the new government would also support prices to run faster. The kiwi jumped to a two-week high of $0.6972 in the wake of the announcement and fluctuated near that level during the Asian session on Thursday.

Consumer prices in China increased by 1.9% y/y in October, recording the highest rise since February and beating the forecasts of 1.8%. In September the figure stood at 1.6%. Month-on-month prices slowed down by 0.4 percentage points to 0.1%, below the expectations of 0.2%. Annual growth in producer prices remained flat at 6.9%. Following the data, the aussie gained 0.28%, jumping to a session high of $0.7688 and being 0.14% up on the day.

In China, US President, Donald Trump, asked the Chinese President, Xi Jinping to further toughen his stance on North Korea, while regarding US-China trade relations, he said that the relationship “has not been a very fair one”. Back in the US, uncertainties around the progress of the tax legislation have not been resolved yet as the markets anticipate a Senate tax-cut bill to differ from the version agreed in the House of Representatives. Note that tax proposals from both the upper and lower chamber will be unveiled later today.

The dollar index retreated by 0.13% on the day to 94.74 as a decline in the US 10-year treasury yield acted as a drag on the dollar as well. Dollar/yen retreated by 0.32% to 113.50 as geopolitical risks turned investors’ focus to safer investments. Dollar/swissie fell by 0.23% to 0.9976. Gold moved up by 0.31% to $1,284.80 per ounce.

Japanese data on machinery orders were also in focus during the session, with the core measure surprisingly contracting by 3.5% y/y in September instead of rising by 1.9% as analysts forecasted. In August core machinery orders grew by 4.4%. The monthly gauge reached the biggest decline since June 2016, falling by 8.1% versus -1.8% expected and 3.4% seen in the previous month.

The euro climbed by 0.10% to $1.1605 after the release of encouraging German trade data, while the pound was in an uptrend on the back of a weaker dollar despite the forced resignation of the International Development Secretary, Priti Patel on Wednesday over her secret meetings with Israeli officials. Pound/dollar advanced by 0.24% to $1.3144.

Turning to energy markets, oil prices were mainly flat supported by ongoing supply cuts by OPEC and non-OPEC producers, although the EIA report showed that US crude oil inventories increased unexpectedly by 2.237 million barrels last week after falling by 2.434 million in the week ending November 3. WTI crude and Brent were trading around $56.85 and $63.54 per barrel respectively.

EURUSD Analysis: Tries To Bypass 1.1603

Despite that American and Chinese companies signed deals worth $253.4B over the last two days, the currency exchange rate stayed neutral. Most probably such hesitations, which result in relentless attempts of the pair to break through resistance area near the 1.6003 level, are related to concerns that Trump's tax reform could be delayed. On the one hand, it looks like the surge should be neutralized, as that zone is additionally secured by the 100-hour SMA. On the other hand, yesterday's movement points out formation of a new minor ascending channel, which already consists of three reaction lows. From this perspective, the exchange rate is likely to climb to the next resistance level located between the 200-hour SMA at 1.1621 and the weekly PP at 1.1631.

GBPUSD Analysis: Sinks Amid Priti Patel Scandal

During the previous trading session the cable was in perfect situation to make a rebound from combined support level formed by the 55-hour SMA, the weekly PP as well as the 38.2% retracement level and make a breakout from the ascending triangle pattern. However, another political scandal in the British government led to rapid sell-off of the Pound. As a result, the exchange rate got in a tricky situation. On the one hand, further road to the south is blocked by the 100-day SMA and the lower line of a large symmetrical triangle. This disposition supports intention of bulls to return the pair back to the pre-fall 1.3175 level. However, in order to achieve this goal, the rate needs to pass through combined resistance set up by the above retracement level, the weekly PP and the 55-hour SMA.

USDJPY Analysis: Plunges Amid BoJ Summary Of Opinions Release

A release of the Bank of Japan Summary of Opinions as well as ongoing concerns over delay of the Trump's tax reform implementation continued to push the exchange rate in southern direction. In technical terms, this downward movement is expressed in one-week long descending channel, which consist of three reaction highs and lows. As in early morning the pair made a rebound from an upper trend-line of the pattern, the rest of the day it is expected to spend either in a red zone or in consolidation. This assumption is supported by the fact that the northern side accumulated all active barriers, such as the 55-, 100- and 200-hour SMAs plus the weekly PP. Moreover, the closest support area is supposedly located only near the 113.40 mark.

XAUUSD Analysis: Heads To Upper Edge Of Ascending Channel

Pressure of the 55-, 100- and 200-hour SMAs prevailed over the combined resistance formed by the 61.8% retracement level and the monthly PP. As a result, the exchange rate approached and tested the upper trend-line of a large ascending channel. Although the first attempt was not successful, the pair is expected to continue climbing to the top, using support provided by the above moving averages plus the weekly R1 located at the 1,281.00 level. There is a need to notice that on daily chart the pair faces no barriers on its way up until the weekly R2 at 1,291.92. This fact as well as the aggregate market sentiment, which is 63% bullish, suggests that the rate has a high probability to breakout from the channel up, instead of making a rebound near the 1,288.00 mark.

EUR/NOK 1H Chart: Pair Tests Triangle

The common European currency is trading against the Norwegian Krone in a channel up valid since mid-July. The latest test of its upper line occurred on October 31. Along the way, the rate entered another patter—a descending triangle. The general characteristics of this pair suggest that the rate should break out to the upside. The rate hindering near the upper triangle boundary might serve as an early indication of such a move. This scenario would set the Euro towards the upper boundary of a junior channel circa 9.54. However, the rate has been stranded between the 55– and 200-hour SMAs for two sessions. A breach of one of these lines is likely to set the tone for the subsequent movement. In case the 200-hour SMA is breached, the aforementioned scenario should occur. Conversely, a breach of the former should guide the pair towards the 9.43 mark in the short-term and possibly even lower.