Sample Category Title

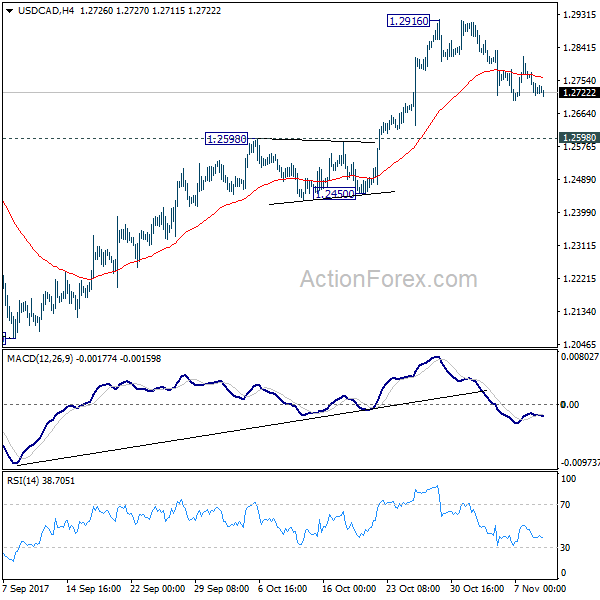

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2702; (P) 1.2739; (R1) 1.2764; More....

USD/CAD stays in consolidation from 1.2916 and outlook is unchanged. Intraday bias remains neutral at this point. As long as 1.2598 resistance turned support holds, near term outlook stays bullish. Further rise is expected in the pair. On the upside, break of 1.2916 will extend the rise from 1.2061 to 38.2% retracement of 1.4689 to 1.2061 at 1.3065. However, sustained break of 1.2598 will argue that rebound from 1.2061 has completed after hitting 55 week EMA (now at 1.2916). Near term outlook will be turned bearish in this case.

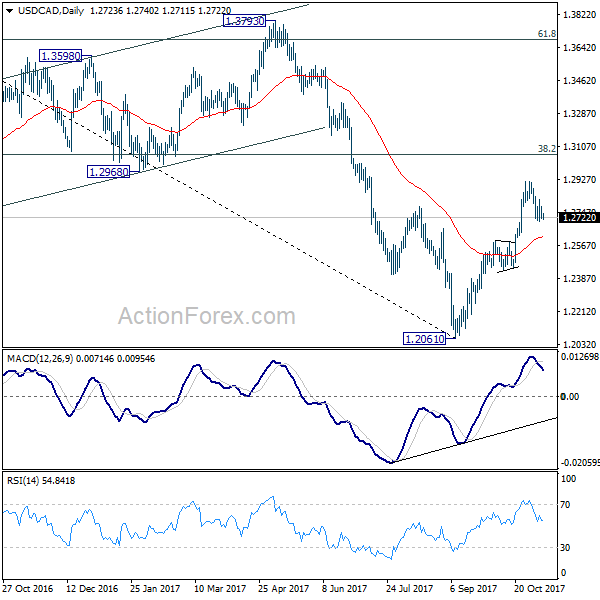

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4689 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Rise from 1.2061 medium term bottom should now target 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Firm break there will target 1.3793 key resistance next (61.8% retracement at 1.3685). We'll now hold on to this bullish view as long as 1.2450 support holds.

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

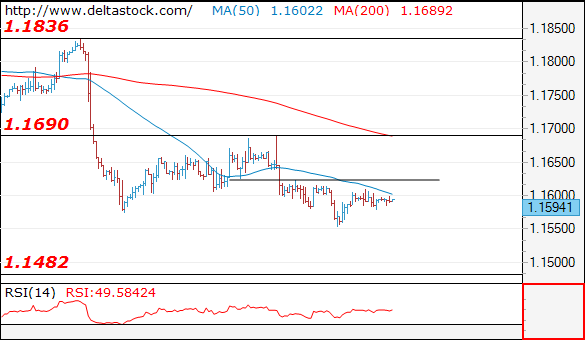

EUR/USD

Current level - 1.1594

The intraday bias is positive, for a test of 1.1625 minor resistance, but while 1.1690 remains intact, the outlook on the senior frames will be bearish, for a dip to 1.1480.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

|

1.1625 |

1.1840 |

1.1550 |

1.1480 |

|

1.1690 |

1.1940 |

1.1480 |

1.1300 |

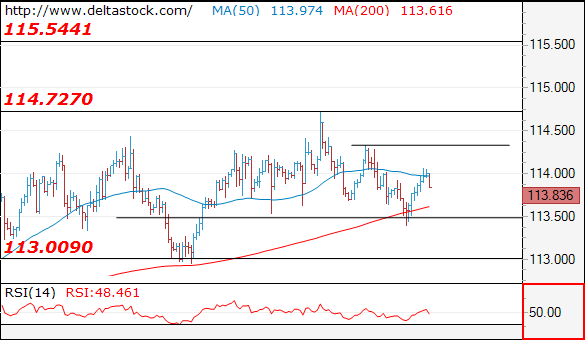

USD/JPY

Current level - 113.83

The rebound above 113.40 is corrective in nature and until 114.30 crucial high holds, the bias will be bearish, for a slide to 113.00 area. The peak at 114.30 is a trigger for a move towards 115.50.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

|

114.32 |

115.50 |

113.40 |

111.00 |

|

115.50 |

116.80 |

113.05 |

107.30 |

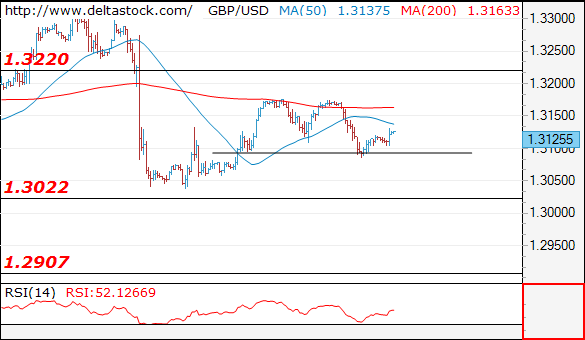

GBP/USD

Current level - 1.3125

Yesterday's precise dip to 1.3090 support area has started the third and hopefully the final leg of the whole consolidation above 1.3030 so the intraday bias is positive, for 1.3220 resistance. The latter should reinstate the slide towards 1.2910.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

|

1.3220 |

1.3220 |

1.3090 |

1.3020 |

|

1.3220 |

1.3340 |

1.3020 |

1.2760 |

Europe Seen Flat As Brexit Talks Resume

- Investors Remain in Reflection Mode as Quiet Week Continues;

- NZD Edges Higher as RBNZ Acknowledges Inflationary Impact of Weaker Currency;

- Chinese Inflation Beats Expectations But Remains Below Target;

- Brexit Talks Resume But is Anyone Optimistic at This Point?

European equity markets are poised to open relatively flat on Thursday, as we near the end of what has so far been a rather quiet week in the markets.

Broadly speaking investors have been in reflection mode this week, given the blockbuster week that preceded this and in the absence of any major economic events. While we haven’t been short of notable political stories – more woes for Theresa May, Saudi corruption crackdown and Donald Trump’s visit to Asia – as of yet none of these have had much market impact.

The two central bank decisions this week came from two of the few that are not particularly interested in shaking things up at the moment, with the Reserve Bank of New Zealand overnight leaving monetary policy unchanged with a fairly neutral statement, much in the same way that the Reserve Bank of Australia did earlier in the week.

The RBNZ decision overnight did lift the kiwi dollar a little despite an acknowledgement from the central bank that monetary policy will remain accommodative for a considerable period. This is perhaps an acknowledgement that tradable inflation has increased due to a weaker currency, with the kiwi having fallen close to 10% against the greenback from its July highs.

Chinese inflation data released overnight is having little impact on markets this morning, despite CPI accelerating more than expected to 1.9%, which is still below target. Higher fuel costs and a moderation in pork price declines was primarily responsible for the higher inflation reading, both of which can be very volatile.

Looking ahead to today, there’s isn’t much on the data front with the UK NIESR GDP estimate due out this morning and US jobless claims this afternoon. The European Commission is expected to release new economic forecasts but this isn’t typically a market moving event, although it may be of interest given the continued improvement in the region.

The UK and EU are expected to resume Brexit talks today although I doubt many are optimistic on progress given how previous meetings have gone. Time is fast running out for both sides to agree to move onto transition and trade talks before businesses begin planning for no deal worst case scenario. This would be particularly problematic for the UK so any sign that we’re headed in this direction could be bad for the pound. It will be interesting to see how vulnerable sterling is to these talks over the next couple of days.

Oil Prices Bounced

Market movers today

It's anot her quiet day on t he dat a front wit h no Tier-1 data. The main data releases are UK indust rial product ion, the NIESR UK GDP est imate and US jobless claims. The European Commission is due to publish new economic forecasts at 11:00 CET. The ECB's Villeroy is due to speak in the afternoon.

US President Donald Trump continues his visit in China today.

In Scandi, the Swedish Riksbank minutes will be released (see next page).

Selected market news

Asian stock markets continued their bull run overnight with the MSCI Asia Pacific Index rising above its past peak from 2007. Nikkei moved above the 23.000 level for the first t ime in 25 years. Asian stocks are supported by a global recovery, st rong profit growth and easy global monetary policy.

US two-year yields has continued higher hitting 1.65% overnight as more Fed hikes are priced into the short end. Two-year yields are at the highest level since 2008. The market is st ill pricing in a lit t le more than one hike throughout 2018 though, which is st ill quite dovish pricing. The rise in two-year yields is not spilling over to the long end and t he US 2-10 yield curve is now at the flat test level in ten years. We expect the flattening t rend to continue as we are close to a peak in the manufacturing cycle and wage inflat ion cont inues t o be subdued. T reasury's earlier announcement that it will not extend durat ion further in its borrowing is also support ing long bonds.

On his visit to China, US President Donald Trump repeated his views that the US companies do not face a level playing field when competing with China. However, he blamed previous US leaders rather than the Chinese leadership, saying t hat ‘who can blame another count ry for taking advantage of another count ry f or t he benefit s of it s cit izens'.

Chinese CPI inflation rose in October to 1.9% y/y (consensus: 1.8% y/y) from 1.6% y/y in September. The core measure ex food was flat though at 2.4% y/y, st ill comfortably below the 3% target . PPI inflat ion was unchanged at 6.9% y/y. It was higher than consensus at 6.6% y/y but st ill below the peak in February at 7.8%. Rising commodity prices have held up PPI inflation.

The UK RICS house price balance fell again to 1 in October from 6 in September. It adds to the evidence of a slowing UK housing market . Especially London is being hit as Brexit weighs on the market .

Oil prices bounced yesterday as the Saudi-Iran tensions as well as Venezuelan debt woes are st ill making headlines. Regarding the lat ter, Russia agreed t o rest ructure the Venezuelan debt , which eased concerns of a pot ent ial default wit h possible negat ive implicat ions for Venezuela's crude output . The EIA yesterday reported a rise in crude stocks last week, which is likely to be due to recent geopolit ical tensions, which have given incent ive to build stocks as insurance against supply risk and perhaps also some last minute stock building ahead of the winter season.

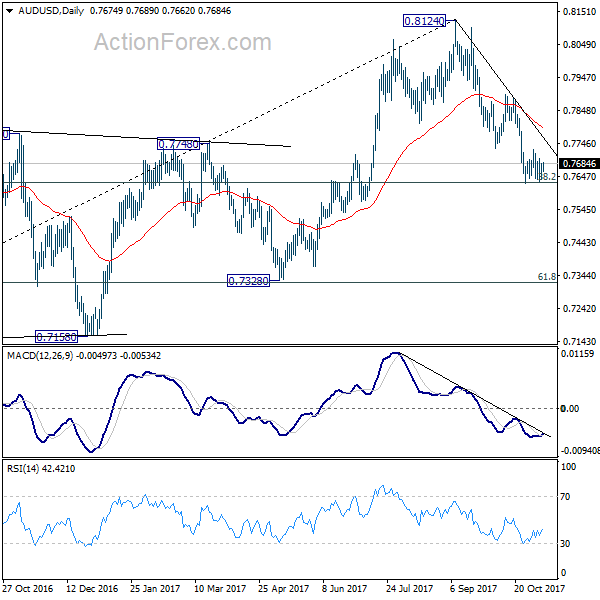

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7644; (P) 0.7664; (R1) 0.7697; More...

Outlook in AUD/USD remains unchanged as consolidation pattern from 0.7624 is extending. Intraday bias remains neutral for the moment. Near term outlook stays bearish with 0.7896 resistance intact and deeper fall is expected. Decisive break of 0.7624 will resume whole decline from 0.8124. And, AUD/USD should target next key cluster level at 0.7322/8 next.

In the bigger picture, corrective rise from 0.6826 medium term bottom is likely completed at 0.8124, after hitting 55 month EMA (now at 0.8067). Decisive break of 0.7328 key cluster support (61.8% retracement 0.6826 to 0.8124 at 0.7322) will confirm. And in that case, long term down trend from 1.1079 (2011 high) will likely be resuming. Break of 0.6826 will target 61.8% projection of 1.1079 to 0.6826 from 0.8124 at 0.5496. This will now be the favored case as long as 0.7896 near term resistance holds.

Dollar Broadly Softer on Tax Plan Worries, Markets Stuck in Consolidation Mode

Dollar continues to trade generally weak today on worries of a delay in implementing corporate tax cut. EUR/USD edged lower to 1.1553 earlier this week but is now back above 1.16 as the greenback pared gains. Both USD/CHF and USD/JPY are stuck in tight range below recent high at 1.0037 and 114.73 respectively. Yen tried to stage a breakout yesterday but there was no follow through buying. Meanwhile, AUD/USD is also holding on to 0.7624 support as sideway trading continues. New Zealand Dollar trades slightly firmer after a more hawkish than expected RBNZ statement. But recent price actions in Kiwi remains corrective in nature.

Powell's confirmation hearing scheduled on November 28

US Senate Banking Committee schedules a confirmation hearing for Jerome Powell as Fed Chair on November 28. Fed Governor has already got quick endorsement from Republicans after Trump's nomination. Senate Majority Leader Mitch McConnell met with Powell on Tuesday and said he looked forward to "supporting his nomination". Meanwhile chair of the Banking Committee, Republican Senator Mike Crapo, also hailed that Powell was "well-equipped to lead our economy and the country in a positive direction." Powell is generally seen as a safe choice by the markets and would likely continue with the policy path laid by Janet Yellen. That is, Fed will continue with rate hikes, likely three, next year, as well as the plan to shrink the USD 4.5T balance sheet.

BoJ opinions show debate on extreme steps

In the summary of opinions in the October BoJ meeting, there were debates on the call from new comer Goushi Kataoka to increase stimulus. Kataoka proposed to target 15 year bond yields to below 0.2% through the bond purchases. That is, he either wanted to expand the targeting from 10 year yields to include 15 year yields. Or, he wanted to switch to target 15 year yield. But the proposal met with oppositions as one board member described by one member as "extreme steps" that could destabilize financial markets. The member added that "the current policy is the most appropriate one to lay the grounds for companies to boost productivity, with the smallest degree of uncertainty over its effect on the economy." Nonetheless, it's consensus that there were concerns over inflation outlook and another member noted "it may take some time before inflation reaches 2 percent."

At this point, there is no confirmation on whether BoJ Governor Haruhiko Kuroda would be renewed for another term next year. The outspoken economic advisor to Prime Minister Shinzo Abe reiterated his call for changes in BoJ. Etsuro Honda said that "The leaders of the central bank must conduct a comprehensive review and then take responsibility." And, "it's impossible to end deflation without bringing in a new regime." Meanwhile, Honda also warned that BoJ has to meet the 2% inflation target before sales tax hike in 2019. Otherwise, "Japan's economy will be in critical danger."

RBNZ turned slightly more hawkish

While keeping the OCR unchanged at 1.75%, the tone of November RBNZ statement has turned slightly more hawkish than previous ones. The central bank upgraded inflation forecasts, while describing core inflation as 'subdued' and reiterating 'uncertainties' in the new government's policies. The growth outlook remained largely unchanged from August's, as weaker growth in the housing and construction sector would be offset by greater fiscal spending promised by the new government and higher terms of trade, thanks to NZD depreciation and the rise in oil prices. RBNZ slightly pushed ahead the rate hike schedule. However, given the minimal change, we believe this is rather a symbolic move. The central bank expects more material interest rate movements by 2020. We believe the monetary policy would stay unchanged for the rest of 2018. More in RBNZ Upgraded Inflation Forecasts, Ambivalent About New Government Policies

On the data front

Japan machine orders dropped -8.1% mom in September, current account surplus narrowed to JPY 1.84T. Australia home loans dropped -2.3% mom in September. China CPI accelerated to 1.9% yoy in October, PPI was unchanged at 6.9% yoy. UK RICS house price balance rose 1.0% in October. Swiss unemployment rate was unchanged at 3.1% in October. German trade surplus was largely unchanged at EUR 21.8b in September. ECB will release monthly bulletin in European session. Later in the day, Canada will release new housing price index while US will release jobless claims.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7644; (P) 0.7664; (R1) 0.7697; More...

Outlook in AUD/USD remains unchanged as consolidation pattern from 0.7624 is extending. Intraday bias remains neutral for the moment. Near term outlook stays bearish with 0.7896 resistance intact and deeper fall is expected. Decisive break of 0.7624 will resume whole decline from 0.8124. And, AUD/USD should target next key cluster level at 0.7322/8 next.

In the bigger picture, corrective rise from 0.6826 medium term bottom is likely completed at 0.8124, after hitting 55 month EMA (now at 0.8067). Decisive break of 0.7328 key cluster support (61.8% retracement 0.6826 to 0.8124 at 0.7322) will confirm. And in that case, long term down trend from 1.1079 (2011 high) will likely be resuming. Break of 0.6826 will target 61.8% projection of 1.1079 to 0.6826 from 0.8124 at 0.5496. This will now be the favored case as long as 0.7896 near term resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 20:00 | NZD | RBNZ Rate Decision | 1.75% | 1.75% | 1.75% | |

| 23:50 | JPY | BOJ Summary of Opinions Oct Meeting | ||||

| 23:50 | JPY | Machine Orders M/M Sep | -8.10% | -2.00% | 3.40% | |

| 23:50 | JPY | Current Account (JPY) Sep | 1.84T | 2.05T | 2.27T | |

| 0:01 | GBP | RICS House Price Balance Oct | 1.00% | 4.00% | 6.00% | |

| 0:30 | AUD | Home Loans M/M Sep | -2.30% | 2.00% | 1.00% | 1.50% |

| 1:30 | CNY | CPI Y/Y Oct | 1.90% | 1.70% | 1.60% | |

| 1:30 | CNY | PPI Y/Y Oct | 6.90% | 6.60% | 6.90% | |

| 5:00 | JPY | Eco Watchers Survey Current Oct | 52.2 | 50.5 | 51.3 | |

| 6:45 | CHF | Unemployment Rate Oct | 3.10% | 3.10% | ||

| 7:00 | EUR | German Trade Balance Sep | 23.1B | 21.6B | ||

| 9:00 | EUR | ECB Economic Bulletin | ||||

| 10:00 | EUR | EU Economic Forecasts | ||||

| 13:30 | CAD | New Housing Price Index M/M Sep | 0.20% | 0.10% | ||

| 13:30 | USD | Initial Jobless Claims (NOV 04) | 231K | 229K | ||

| 15:00 | USD | Wholesale Inventories M/M Sep F | 0.30% | 0.30% | ||

| 15:30 | USD | Natural Gas Storage | 65B |

ECB Policymakers Headline Thursday Session

Monetary policy is back in the spotlight on Thursday, with a parade of European Central Bank (ECB) officials expected to deliver speeches.

The ECB will launch its Economic Bulletin at 09:00 GMT. The publication is published two weeks after each Governing Council meeting. One hour later, the European Commission will release its economic growth forecasts, which will be closely watched by the financial markets.

ECB Executive Board member Benoit Coeure will kick off the speaking engagements at 10:00 GMT. Later in the day, central bank Vice President Vitor Constancio will deliver remarks. Finally, ECB Board member Sabine Lautenschlager will issue remarks at 18:20 GMT.

In terms of economic data, the Swiss government will release its monthly unemployment rate at 06:45 GMT. The jobless rate is expected to hold steady at 3.1% in October.

Fifteen minutes later, the German government will report its monthly trade balance for September. Berlin’s trade surplus is forecast to dip to €21.1 billion from €21.6 billion.

Later in the day, the Greek government will release a bevy of reports including industrial production, consumer inflation and the unemployment rate. Separately, Portugal will unveil its latest trade and unemployment figures.

In North America, the US Labor Department will release initial jobless claims for the week ended 3 November. The number of Americans filing for first time unemployment benefits is expected to rise to 231,000 from 229,000 the previous month.

Earlier in the day, the Chinese government reported a bigger than expected rise in annual inflation, with both consumer prices and producer prices extending a long run of gains.

China’s consumer price index (CPI) rose 1.9% in the 12 months through October, following a gain of 1.6% the month before. The producer price index (PPI), which measures inflation at the factory-gate level, climbed 6.9% year-over-year.

EUR/USD

The euro has had a relatively uneventful week, with technical traders keeping the currency at or around 1.1600 US. The EUR/USD exchange rate was last seen trading around 1.1592. The pair faces immediate resistance in the 1.1620 region. On the opposite side of the spectrum, support is located at the 1.1553 level.

GBP/USD

The British pound briefly fell below 1.3100 US on Wednesday, culminating an 80-pip drop on dovish sentiment surrounding the Bank of England (BOE). Cable would later regroup and was last seen trading at 1.3125. Investors should eye a break below 1.3090 as confirmation of a bearish reversal.

US OIL

After a relentless run, US oil prices have consolidated below $57.00 a barrel. However, the market remains in a firm uptrend supported by a combination of technical and fundamental indicators. The US crude contract continues to trade at a more than $6 bargain to global benchmark Brent.

GBPUSD Still Bearish Below 1.130 Level

The British pound has recovered above the key 1.3109 level against the U.S dollar, as sterling paired back losses during today's Asian trading session. The GBPUSD pair currently trades around the 1.3120 level, despite further political scandals threatening British Prime Minister Theresa May's leadership. With the economic docket remaining light for the UK and the U.S on Thursday, traders will look to any fresh news coming from the U.S Senate on the proposed tax reform bill.

The GBPUSD pair is still intraday bearish while trading beneath the 1.3130 level. Further losses towards 1.3109 and 1.3086 seem likely. Extended support is found at 1.3040 and 1.2980.

Should price action move above the 1.3130 level for a sustained period, further advancement towards the 1.3161 and 1.3200 levels remains possible.

EURO Still Intraday Bearish Below 1.1598 Level

The euro remains in a tight trading range against the U.S dollar, as the pair continues to hold below the 1.1600 level during the Asian trading session. The EURUSD is seemingly unable to find a clear directional bias, amidst a lack of macroeconomic data coming from the U.S and Europe. Financial markets are increasingly cautious ahead of the U.S tax reforms plan, which is set to be decided by U.S Senate today, sometime during early U.S trading.

The EURUSD pair remains strongly intraday bearish while trading below the 1.1598 level. Further declines towards the 1.1572 and 1.1553 level seems likely.

Should the EURUSD pair move above the 1.1598 level for a sustained period, further upside towards the 1.1610 and 1.1640 levels.

US Dollar Struggling To Settle Above 1.2800

Key Highlights

- The US Dollar recently failed to hold gains above 1.2800 versus the Canadian Dollar and started a downside move.

- There is a crucial bearish trend line forming with resistance at 1.2775 on the 4-hours chart of USD/CAD.

- Canada's Housing Starts in Oct 2017 were 222.771 better than the forecast of 210.0K.

- Today, the US Initial Jobless Claims for the week ending Nov 4, 2017 will be released, which is forecasted to increase from 229K to 231K.

USDCAD Technical Analysis

The US Dollar recovered nicely from the 1.2702 low against the Canadian Dollar. However, the USD/CAD pair failed at 1.2818 and started a sharp downside move.

It seems like a crucial bearish trend line with resistance at 1.2775 on the 4-hours chart protected gains above 1.2810-20. The pair is now well below 1.2800, the 100 (red) and 200 (green) simple moving averages (hourly).

It recently broke the 50% Fib retracement level of the last wave from the 1.2702 low to 1.2818 high. Therefore, there are chances of further declines and the pair might even retest 1.2700. On the upside, the most important resistance is at 1.2775, followed by the 1.2800 handle.

Canada's Housing Starts

Recently in Canada, the Housing Starts report for Oct 2017 was released by the Canadian Mortgage and Housing Corporation. The market was looking for the Housing Starts to be 210.0K in Oct 2017 compared with the same month a year ago.

The actual result was better than the forecast, as Housing Starts in Oct 2017 were 222.771. It was also above the last revised reading of 219.3K.

Commenting on the report, CMHC's chief economist, Bob Dugan, stated:

The trend in housing starts essentially held steady in October following a decrease in September. Nevertheless, new home construction remains very strong in 2017, as the seasonally adjusted number of starts has been above 200,000 units in nine of ten months so far this year.

Overall, it seems like the USD/CAD might continue to move down towards the 1.2700 handle, and it could even break it for a new weekly low.

Economic Releases to Watch Today

Germany's Trade Balance for Sep 2017 2017 – Forecast €21.1B, versus €21.6B previous.

Germany's Imports of goods and services Sep 2017 – Forecast +0.3%, versus +1.2% previous.

Germany's Exports of goods and services Sep 2017 – Forecast -1.1%, versus +3.1% previous.

US Initial Jobless Claims – Forecast 231K, versus 229K previous.

Canada's New Housing Price Index (NHPI) for Sep 2017 (MoM) – Forecast +0.2%, versus +0.1% previous.