Sample Category Title

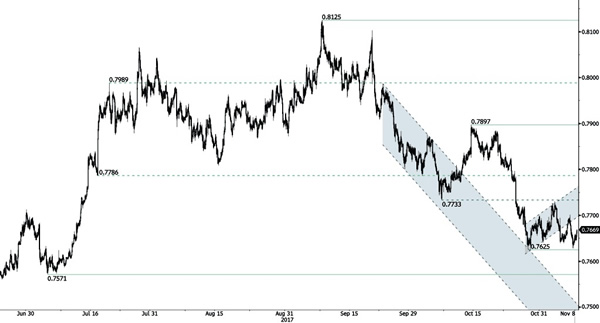

AUD/USD Room For Further Downside

AUD/USD is ready to bounce back but downside pressures are still lively. Hourly resistance is given at a distance at 0.7897 (13/10/2017 high). Expected to show renewed pressures towards key support at 0.7571 (05/07/2017 low).

In the long-term, the trend is turning positive. Key supports stands at 0.6009 (31/10/2008 low) . A break of the key resistance at 0.8164 (14/05/2015 high) is needed to invalidate our long-term bearish view.

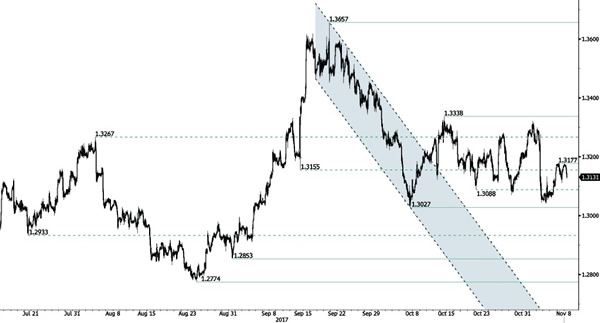

USD/CAD The Bearish Consolidation Is Not Over

USD/CAD continues to weaken after the set-up of a resistance at 1.2917 (27/10/2017 low). This suggests a further extension of bullish momentum. Hourly support lies at 1.2703 (06/11/2017 low). Expected to show continued short-term bearish pressures.

In the longer term, the pair has broken longterm support that can be found at 1.2461 (16/03/2015 low). Strong resistance is given at 1.4690 (22/01/2016 high). The pair is likely to head further lower.

USD/CHF Holding Around Parity

USD/CHF is consolidating. Yet, the technical structure is still bullish. The technical structure suggests an improving short-term buying interest. Expected to show continued bullish momentum. Hourly support stands at 0.9951 (01/11/2017 low).

In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015.

USD/JPY Ready To Bounce Back

USD/JPY is riding uptrend channel below former resistance at 114.49 (11/07/2017 high). Strong support is located at a distance at 111.12 (20/09/2017 low).

We favor a long-term bearish bias. Support is now given at 99.02 (10/08/2013 low). A gradual rise towards the major resistance at 125.86 (05/06/2015 high) seems unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

GBP/USD Double Top Below 1.32

GBP/USD is monitoring 1.32. Support is given at 1.3027 (06/10/2017 low). Resistance area is given around 1.3200. Expected to show further increase,.

The long-term technical pattern is reversing. The Brexit vote had paved the way for further decline. Long-term support can be found at 1.1841 (07/10/2017 low). Long-term resistance given around 1.35 is at stake and indicates a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

EUR/USD Stronger Selling Pressures

EUR/USD is biased to the downside after breaking hourly support at 1.1575 (27/10/2017 low). Hourly resistance is located at 1.1658 (30/10/2017 high). Expected to show some shortterm consolidation.

In the longer term, the momentum is now turning largely positive. We favour a continued bullish bias. Key resistance is holding at 1.2252 (25/12/2014 high) while strong support lies at 1.0341 (03/01/2017 low).

Market Update – European Session: US Tax Reform Momentum Seemed To Have Slowed For The Time Being

Notes/Observations

President Trump arrives in China; greeted by another Chinese trade surplus

US tax reform momentum seemed to have slowed as GOP talk about holding corporate tax cuts back by a year

Overnight

Asia:

(CN) China Oct Trade Balance (USD-denominated): $38.2B v $39.1Be, Exports Y/Y: 6.9% v 7.1%e, Imports Y/Y: 17.2% v 17.0%e

BOJ member Funo: reiterated that important to continue current powerful easing as still some distance from inflation target. Noted that would not necessarily keep policy unchanged until 2% inflation was reached

US President Trump speech to Korea National Assembly: World cannot tolerate rogue regime that threatens it with nuclear devastation; all responsible nations must join forces to isolate North Korea and deny it any form of support

Europe:

EU official said to discuss Brexit transition stance at a meeting on Wed, Nov 8th

Americas:

Senate GOP reportedly considering a 1-year delay on corporate tax in reform bill (**Note: Delay would save $100B in the bill). Could face resistance from Trump who has sought immediate implementation

Fed's Harker (hawk, voter): Reiterates Fed on pace to hike rates in Dec 2017; 2018 hinges on inflation

Bank of Canada (BOC) Gov Poloz: economy was likely to need less monetary stimulus over time; BOC would be cautious in adjusting policy rate in the future. inflation was behaving well within the normal zone of tolerance

Energy:

Weekly API Oil Inventories: Crude: -1.6M v -5.1M prior

Economic Data

(TH) Thailand Central Bank (BOT) left its Benchmark Interest Rate unchanged at 1.50% (as expected)

(FR) France Sept Trade Balance: -€4.7B v -€4.7Be

(ES) Spain Sept Industrial Output NSA Y/Y: 0.2 v 2.3% prior; Industrial Output SA Y/Y: 3.4% v 3.1%e

(CZ) Czech Oct Unemployment Rate: 3.6% v 3.6%e

(ZA) South Africa Oct Sacci Business Confidence: 92.9 v 93.0 prior

Fixed Income Issuance:

(IN) India sold total INR110B vs. INR110B indicated in 3-month, 6-month and 12-month Bills

(SE) Sweden sold SEK 10Bvs. SEK10B indicated in 3-month bills; Avg Yield:-0.8304% v -0.7460% prior; Bid-to-cover: x v 2.43x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 -0.1% at 394.3, FTSE flat at 7515, DAX flat at 13385, CAC-40 -0.1% at 5475, IBEX-35 -0.3% at 10197, FTSE MIB -0.6% at 22836, SMI +0.2% at 9234, S&P 500 Futures flat]

Market Focal Points/Key Themes:

European Indices trade mixed this morning, trading little changed as Macro data remained light. The deluge of earnings continued this morning, notably in Germany E.ON which reported slightly better then expected results, Hannover Re cuts its outlook amidst the recent natural disasters, while Wirecard is under pressure after being linked to the recently release paradise papers. In the UK M&S reversed earlier gains after reporting H1 results, in France Credit Agricole weighs after lower Q3 profits and in the Netherlands Supermarket giant Ahold Delhaize trades sharply higher after strong results.

Looking ahead, notable earners in the US include Humana, Wendy's and MGM resorts.

Equities

Consumer discretionary [Marks & Spencer [MKS.UK] -1.5% (Earnings), JD Weatherspoons [JDW.UK] +0.3% (Earnings), Ahold Delhaize [AD.NL] +5% (Earnings), Wizz Air [WIZZ.UK] -8% (Earnings)]

Financials: [Credit Agricole [ACA.FR] -4.3% (earnings)]

Technology: [Wirecard [WDI.DE] -2.7% (Link to paradise papers)]

Healthcare: [Lundbeck [LUN.DK] -4% (Earnings)]

Utilities: [SSE [SSE.UK] +0.3% (Earnings, agreement with Innogy)]

Energy: [ E.ON [EOAN.DE] +1.1% (Earnings), Tullow Oil [TLW.UK] +2.9% (Trading update)]

Speakers

BOE Agents Summary: Pay growth has edged up and expected to be higher in 2018 as recruitment difficulties had intensified. Forecasted pay settlements between 2.5-3.5% next year. Saw modest growth in investment in the coming year

France Fin Min Le Maire: France and Germany should harmonized their corporate tax rates by end of 2018. To form working groups to discuss next steps of Euro Zone reforms

Greece PM Tsipras reiterated working intensively to conclude third bailout review

German Leading Economic Institutes (Advisors) noted that ECB should urgently communicate a strategy for the normalization of policy and should quickly reduce asset purchases and end the program earlier. Believed that QE undermined the effectiveness and credibility of the ESM crisis mechanism. Raised 2017 GDP growth forecast from 1.4% to 2.0% and 2018 GDP growth forecast from 1.% to 2.2%

Russia Fin Min Siluanov: Venezuela ready to restructure debt owed to Russia

Russia govt spokesperson: Probability of a Trump/Putin meeting on sidelines of upcoming APEC Summit in Vietnam was high

White House official: President Trump to decide whether North Korea would be labeled a state sponsor of terrorism by the end of his current Asia trip. Reiterated that China is not doing enough under UN sanctions

Thailand Central Bank policy statement noted that the decision was unanimous to keep policy steady and reiterated that its accommodative policy was still needed. Monetary policy still supported the country's economic recovery at a time of high household debt. Domestic economy was expected to grow at a faster pace than its previous assessment, driven by growth in exports and improvement in domestic demand. THB currency (Baht) price movement within regional peers.

Currencies

USD was softer against most major pairs after reports circulated that that Senate Republicans could postpone the $845 million corporate tax cut until 2019. Dealers noted that the prospect of delays could hurt the greenback’s luster for now.

Overall price action has seen quiet session with narrow ranges. EUR/USD hovering around the 1,16 area while USD/JPY at 113.70.

Fixed Income

Bund futures trade at 163.47 up 16 ticks, underpinned with core bond. Support lies at 162.00, followed by 161.50. Resistance stands initially at 163.51, followed by 164.25.

Gilt futures trade at 125.65 up 18 ticks with the focus on BOE Financial Policy Committee Kohn's speech. Continued upside eyeing 125.75 then 126.47. Downside targets include 124.90 then 124.24.

Wednesday's liquidity report showed Tuesday’s excess liquidity rose to €1.8720T from €1.8645T and use of the marginal lending facility climbed to €238M from €197M

Corporate issuance saw $13.3B come to the primary market via 6 issuers, headlined by Oracle's five-part bond offering.

Looking Ahead

(UR) Ukraine Oct CPI M/M: No est v 2.0% prior; Y/Y: 14.1%e v 16.4% prior

(NL) Netherlands Debt Agency (DSTA) announces upcoming DSL bond auction for Tues, Nov 14th

05:30 (CL) Chile Central Bank's Traders Survey

05:30 (DE) Germany to sell €3.0B in 0% Oct 2022 BOBL

05:30 (PT) Portugal Debt Agency (IGCP) to sell 4.125% Apr 2027 OT

06:00 (CL) Chile Oct CPI M/M: +0.3%e v -0.2% prior; Y/Y: 1.6%e v 1.5% prior

06:00 (PT) Portugal Q3 Unemployment Rate: No est v 8.8% prior

06:00 (IE) Ireland Sept Property Prices M/M: No est v 2.0% prior; Y.y: No est v 12.2% prior

06:00 (PL) Poland Central Bank (NBP) Interest Rate Decision: Expected to leave Base Rate unchanged at 1.50%

06:00 (RU) Russia to sell combined RUB25B in OFZ bonds

06:45 (US) Daily Libor Fixing

06:50 (UK) BOE Financial Policy Committee (FPC) Kohn at conference in London

07:00 (US) MBA Mortgage Applications w/e Nov 3rd: No est v -2.6% prior

08:00 (HU) Hungary Central Bank (NBH) Oct Minutes

08:00 (RU) Russia Oct Official reserve Assets: $426.5Be v $424.8B prior

08:05 (UK) Baltic Dry Bulk Index

08:15 (CA) Canada Oct Annualized Housing Starts: 211.0Ke v 217.3K prior (revised 217.1K)

08:30 (CA) Canada Sept Building Permits M/M: +1.0%e v -5.5% prior

10:00 Poland Central Bank Gov Glapinski to hold post rate decision press conference

10:30 (US) Weekly DOE Crude Oil Inventories

11:00 (IT) Italy Debt Agency (Tesoro) announces upcoming BTP bond auction for Monday, Nov 13th

12:00 (CA) Canada to sell 5-Year Bonds

13:00 (US) Treasury to sell $23B in 10-Year Notes

13:00 (DE) German Chancellor Merkel at church event

15:00 (NZ) New Zealand Central Bank (RBNZ) Interest Rate Decision: Expected to leave Cash Rate (OCR) unchanged at 1.75%

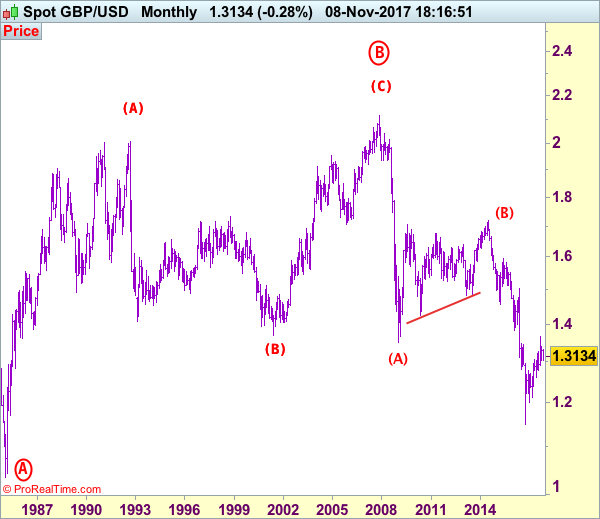

GBP/USD Elliott Wave Analysis

GBP/USD – 1.3132

Despite rebounding to 1.3321 last week, as sterling retreated again after faltering below indicated previous resistance at 1.3338, retaining our bearishness, however, the subsequent bounce from 1.3039 suggests further choppy trading would take place and recovery to 1.3200 cannot be ruled out but upside should be limited to 1.3240 and bring another decline later. Below 1.3039 support would bring a retest of 1.3027, break there would confirm the fall from 1.3658 top has resumed for weakness to 1.3000, then towards 1.2950 but support at 1.2909 should limit downside and another previous support at 1.2852 would remain intact.

Our preferred count on the daily chart is that cable's rebound from 1.3500 (wave (A) trough) is unfolding as a wave (B) with A ended at 1.7043, followed by triangle wave B and wave C as well as wave (B) has possibly ended at 1.7192, below support at 1.4232 would add credence to this count, then further fall to 1.4000 level would follow but reckon downside would be limited to 1.3655 support and price should stay above previous support at 1.3500.

On the upside, although initial recovery to 1.3170 cannot be ruled out, reckon upside would be limited to 1.3220-25 and bring another decline. Above 1.3240-50 would risk a stronger rebound to 1.3300 but only break of indicated resistance at 1.3338 would shift risk to upside and signal another leg of rebound from 1.3027 is underway for further subsequent gain to 1.3400 and possibly towards resistance at 1.3455. Having said that, if our view that top has been formed at 1.3658 is correct, upside would be limited to 1.3500-10 and bring another decline later.

Recommendation: Stand aside for this week.

Longer term - Cable's rise from 1.0520 (Feb 1985) to 2.0100 (September 1992) is seen as [A], the decline to 1.3682 is labeled as (B) and (C) wave rally has ended at 2.1162 (9 Nov, 2007) which is also the top of larger degree wave B with circle. The selloff from there is a 5-waver with wave (A) ended at 1.3500 (23 Jan 2009), wave (B) itself is labeled as A: 1.6733, triangle wave B: 1.4813 and wave C as well as top of wave (B) ended at 1.7192 (2014), hence the selloff from there is an impulsive wave (C) with wave I : 1.4566, wave II 1.5930, an extended wave III is unfolding and already exceeded our downside target at 1.3500 and 1.3000, hence weakness to 1.2500 and possibly 1.2000 cannot be ruled out, however, price should stay well above psychological level at 1.0000.

The Greenback Extends Gains Amid Tax Plan Hopes And European Political Jitters

RBA maintains its wait-and-see approach

The US dollar extended gains against all of G10 currencies on Tuesday. The gains were quite limited as investors awaited several key speeches today. Draghi will speak at GMT 9 am, while across the Atlantic Poloz (BoC) will give a press conference this evening. In Australia, the central bank (RBA) held the Cash Rate Target unchanged at record low 1.5%. Governor Lowe made few changes to the statement and maintained its growth forecast of around 3% over the few next year. The RBA also expressed its concerns about the weakness in inflation (CPI eased to 1.8%y/y in the third quarter, down from 1.9% in the previous one) and reiterated its warning that further strength of the Aussie could only worsen the situation.

The Reserve Bank of Australia finds itself in a tricky place, as the economy kept improving and reducing its dependence to the mining sector, while on the other hand a few indicators such as inflation and retail sales are sending mixed signals. The RBA will wait patiently on the sidelines for a long-time. The market is not pricing any rate hike before at least the end of the summer 2018. Against such a backdrop, the risk is significantly skewed to the downside in AUD/USD. However, upside risk is not zero as an positive surprise in inflation together with another disappointment regarding Trump tax plan could trigger an AUD rally.

AUD/USD is currently testing the key 0.76-0.77 area and has been unable to validate a break of the $0.77 resistance (200dma). The USD rally is losing steam amid a lack of positive news in the US. Therefore, a return towards $0.78 appears likely in the short-term. In the longer-term, we maintain our bearish view.

Political risk rise in Europe

Political risk have again picked up in Europe prompting a stark sell of in Euro. In Italy the center-right coalition led by former Italian Prime Minister Berlusconi solidly won regionals elections in Sicily. With over 90% of the ballot counted, Nello Musumeci took 40% of the vote over 5-Star candidate Giancarlo Cancelleri impressive 35%. The elections was viewed by many as a litmus test for next year’s Italian national elections. The turnout for both antiestablishment parties’ indicates the reactionary vote remain influential. EURUSD bearish momentum continues hitting 1.1566 low.

Clearly the concern is fragmentation of the EU as Italians in poll have shown the highest dislike and preference to leave the EU of any member nation. However, a portion of the move should be attributed to broader FX risk aversion (migrating into USD), while equities continue to power ahead. Yet our midterm view this that European Union convergence has move past the “event horizon”. This unified union will be able to keep Italy in folds and therefore we would fade short-term risk volatility. This view, will be reinforced by further strengthening in the European economy. German Industrial production fell 1.6% in September greater then markets expectations of 0.9%. The slowdown can be attributed to broader weakness in European leading indicators after significant acceleration. We suspect the weak read will be short lived an ECB loose monetary policy and solid outlook for global economy will support output growth.

Switzerland FX Reserves hit record high

This morning has been released the Swiss FX reserves for October. The data increased strongly to $741.5 billion from $724.4billion. The reserves hit a clear record high.

The SNB balance sheet continues to expands, meaning that the SNB still believes the CHF is overvalued, or at least that upside risks on the CHF are strong. The FX reserves are coming from money creation in other words the central bank’s debt. It is clear that as long as global monetary policy remains loose, the Swiss FX reserves will continue climbing and increase the SNB exposure to global economic conditions.

The EURCHF is below 1.16 and the EUR remains the main driver. The strong Quantitative easing from the European Central Bank continues at least until September 2018 and this is still posing threat to the Swiss stability. The inflation, that seems to be back in the US, has slowed unexpectedly in Europe in October preventing a bigger change of the ECB monetary policy. A stronger European inflation would definitely help to clear some pressures off the CHF.

EURJPY Holds Neutral Trend, Near-Term Bias Tilted To Downside

EURJPY holds a neutral trend in the medium term as it has been trading within a range during the past 7-weeks. The market is currently trading at the lower end of this range with an intra-day bias that is tilted to the downside.

A break below 131.50 would turn the focus to the downside to target the September 15 low of 130.60. The next support is expected at 129.36 and 127.55.

Only a move above 132.40 would ease immediate downside pressure. Resistance is expected at 131.12. Clearing this level would add further gains towards 133.90, with scope to re-test the October 26 peak at 134.50 at the top of the 7-week range. At this stage, an extension higher would confirm a resumption of the longer-term trend from April.

Risk is tilted to the downside in the near term and technicals are bearish. Ichimoku cloud analysis on the 4-hour chart shows Tenkan-sen and Kijun-sen lines are negatively aligned while EURJPY is trading below the cloud. RSI is in bearish territory below 50. The medium-term neutral trend will likely remain in play as long as support at 131.50 holds firm.