Sample Category Title

EUR/USD: US JOLTS Job Openings

The EUR/USD exchange rate continued to increase on the US JOLTS report on Monday. The release caused 20% volatility in the pair, where the Euro lost 3 base points against the US Dollar, but kept recovering in an attempt to enter the 1.1600 area again. The bullish sentiment was fuelled additionally by the Fed's Yellen speech in the evening.

The JOLTS report showed that demand for workers in the US remained solid, with 6.1M job openings registered in September. The job opening rate, as well as pace of hiring were unchanged at 4% and 3.6%, respectively. Despite the recent hurricanes' fallout, levels were steady, indicating the resilient labour market. However, nearly 1.7M people were laid off or fired in September, compared with 1.5M a year ago

Technical Outlook: GBPUSD – Fresh Weakness Faces Strong Supports At 1.3100 Zone

Cable moved lower on Wednesday after advance in past two days was capped by 10SMA at 1.3175. Hanging Man candlestick was left on Tuesday, signaling that bulls from 1.3038 (03 Nov low) might be running out of steam.

Plethora of barriers (MA's / daily cloud base) lies above and weighs on near-term action, along with bearishly aligned daily studies. Near-term bias is expected to remain at the downside while these resistances cap.

Today's fresh weakness penetrated into thick hourly cloud but break below strong 1.3100 support zone (cloud base / 100SMA) is required to confirm reversal and re-expose key near-term supports at 1.3038/26, break of which will be bearish.

Alternative scenario requires sustained break above 1.3200 resistance zone to shift near-term focus higher.

Res: 1.3175, 1.3187, 1.3214, 1.3278

Sup: 1.3125, 1.3108, 1.3096, 1.3057

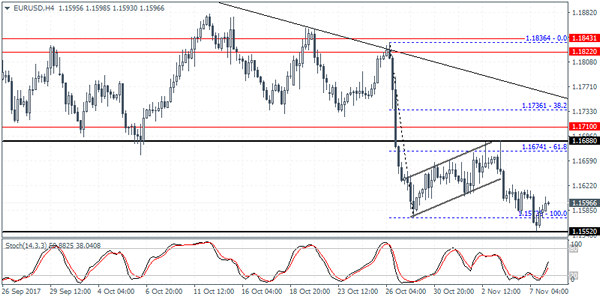

Technical Outlook: EURUSD – Weaker Dollar Boost The Euro But Upside Action Was So Far Limited, Keeping 1.1500 Target...

The Euro returned to 1.1600 zone in early Wednesday's trading but upside attempts off Tuesday's fresh low at 1.1553 (the lowest since 20 July) were so far limited.

The single currency was boosted by rumors about delay of US tax reforms plan, however, stronger upside action could be expected on sustained break above pivotal barrier at 1.1622 (falling 10SMA/Tenkan-sen).

Extended correction above 1.1622 would face barriers at 1.1644 (broken bearish flag's lower boundary), 1.1674 (broken neckline of daily H&S pattern) and pivotal 1.1700 zone, break of which would signal stronger recovery.

Bearish daily studies see extension towards 1.1500 support zone as more likely scenario then rally towards 1.1700.

Res: 1.1622, 1.1644, 1.1674, 1.1690

Sup: 1.1583, 1.1553, 1.1510, 1.1445

Forex: Data & Polls Pressure Sterling

Sterling suffered downward pressure on Tuesday as the latest monthly report from the British Retail Consortium showed non-food sales slumping in October to the lowest levels in 5 years. Total sales crept up 0.2% from a year earlier, like-for-like sales slipped 1%, a reversal from the 1.9% rise in September. British consumers continue to experience a squeeze on their incomes as wage growth is behind inflation, driven by the continued weakness in GBP following the Brexit vote in 2016

More pressure was added on GBP following the release of a poll, conducted by ORB International for The Telegraph, that showed public confidence in Prime Minister May’s ability to deliver a strong Brexit had fallen to a record low. 66% of those polled disapprove of the way the Government is handling negotiations with the EU. Prior to the snap election in June, the percentage of disapprovers stood at 45%. The poll also suggested that public confidence in Prime Minister May has fallen sharply with only 26% believing she will “get the right deal for Britain in the Brexit negotiations” – in June this stood at 44%. With several key members of the Conservative Party suffering suspensions, due to sexual harassment allegations, and Foreign Secretary Boris Johnson damaging international relations following his recent remarks concerning the imprisonment of a British dual national in Iran, many are wondering if Theresa May’s tenure as Prime Minister may be near its end.

In the US, reports are circulating that Senate Republican leaders are considering a 1-year delay in the implementation of a major corporate tax cut to comply with Senate rules. USD had seen a recent improvement against its peers on expectations that President Trump’s Administration would deliver on their pledge to reduce taxes, which would help economic growth and lift interest rates. With the prospect of delays, USD will lose much of its appeal and could give back its recent gains.

EURUSD is 0.12% lower in early Wednesday trading at around 1.1600.

USDJPY is 0.2% lower in early session trading at around 113.75.

GBPUSD is little unchanged in early trading at around 1.3172.

Gold is 0.25% higher, trading around $1,278.50.

WTI is little changed overnight, currently trading around $57.15.

Major data releases for today:

At 08:00 GMT, the European Central Bank is scheduled to hold a non-monetary policy meeting in Frankfurt, Germany.

At 13:15 GMT, the Canadian Mortgage and Housing Corporation will release Housing Starts (YoY) for October. The forecast is calling for 210K new homes constructed against the previous release of 217.1K. We can expect to see CAD volatility if the release is significantly different from expectations.

At 15:30, The US Energy Information Administration will release Crude Oil Stocks change for the week ended November 3rd. The forecast is for another draw of -2.8M compared to the previous draw of -2.435M. The EIA report never fails to cause volatility in both WTI and Brent, especially if the release is wildly different from expectations.

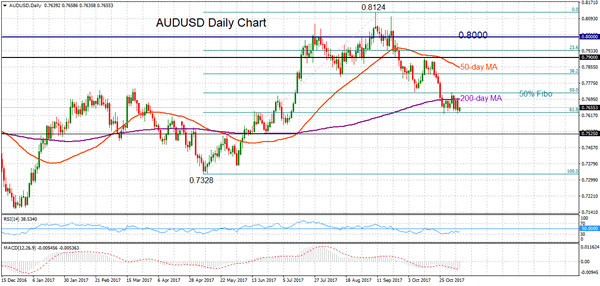

AUDUSD Shifts From Bearish To Neutral In The Short-Term

AUDUSD has shifted from bearish to neutral in the short-term as it continues to trade in a range since October 26 after breaking below the 200-day moving average.

Risk is tilted to the downside as AUDUSD has retraced more than half of the upleg from 0.7328 to 0.8124. The pair is now trapped between the 50% and 61.8% Fibonacci levels, with resistance at 0.7723 and support at 0.7631.

MACD remains in bearish territory and is sloping down, suggesting there is scope for further downside. RSI is also in bearish territory below 50 but is currently neutral, indicating momentum has weakened and the market has entered a consolidation phase.

A daily closing below the key 0.7600 level would see AUDUSD re-enter a bearish phase and another leg lower towards 0.7525 and 0.7328 cannot be ruled out.

Only a move above 0.7900 would shift the focus back to the upside to open the way towards the 0.8124 peak. A rise above this point would confirm a resumption of the uptrend from 0.7328.

In the near-term, the neutral phase is expected to continue, while the medium-term outlook remains bearish.

Dollar Weaker On Possible Tax Cut Delay, Kiwi Steady Ahead Of RBNZ Meeting

The dollar opened weaker in Asia as traders were concerned about a potential delay in the implementation of a corporate tax cut, while they also turned cautious on US-North Korea political developments after Trump delivered a warning message to North Korea. The kiwi stood flat ahead of the RBNZ policy meeting starting later today.

A report by the Washington Post on Tuesday raised questions about the progress of the US tax legislation and hence pressured the dollar. The relevant article stated that Senate Republicans were considering a one-year delay in putting a major corporate tax-cut into effect as the tax code could find difficulties to comply with Senate rules. The sources cited in the report were unidentified.

In the meantime, in South Korea, Trump used a tougher language against the North Korean leader, Kim Jong Un, a day after he called North Korea to 'come to the table' and make a deal. He said that the regime's efforts to develop a nuclear program was putting the country 'into grave danger', advising Kim to 'not underestimate' the US. Next, Trump will fly to China to meet President Xi Jinping, with trade and North Korea expected to be on the agenda.

The dollar index which gauges the strength of the greenback against a basket of major currencies notched 0.07% down to 94.80, while safe-haven assets gained some ground against the dollar as investors turned somewhat risk-averse following Trump's warnings. Dollar/yen declined by 0.24% to 113.75, dollar/swissie fell by 0.14% to 0.9986 and gold moved up by 0.22% to $1,278.40 per ounce.

The euro was mainly flat around $1.1590, and the pound reversed some of yesterday's gains on news that the UK Prime Minister, Theresa May, was considering firing a member of her cabinet ahead of the resumption of Brexit negotiations on Thursday. According to BBC reports and the Sun newspaper, May is likely to dismiss the International Development Secretary Priti Patel after the latter held unauthorized meetings with Israeli officials without May being aware. This comes a week after the Defence Minister Michel Fallon resigned on allegations of sexual misbehavior.

Trade data out of China, showed that growth in exports eased to 6.9% y/y in October compared to 7.2% expected and 8.1% in September, whereas imports increased by 17.2% y/y, above the 16.0% anticipated and below the 18.6% in September.

The aussie retreated slightly after the release of the Chinese trade data, but resumed its uptrend afterwards, rising to $0.7659 (+0.20%).

The kiwi was moving sideways around $0.6908 after a sharp fall amid falling dairy prices ahead of the RBNZ policy meeting expected to start later today. The RBNZ policymakers are projected to hold rates steady at the record low level of 1.75% and adjust their outlook for inflation.

Dollar/loonie changed hands at 1.2752, affected little by remarks made by the BOC Governor Stephen Poloz yesterday. Poloz held a neutral stance on upcoming rate moves, highlighting the fact that the central bank was monitoring wage growth and inflation as well as the economic capacity to see how the economy was responding to July's and September's rate hikes.

Turning to energy prices, WTI crude oil retreated by 0.30% to $57.03 per barrel and Brent decreased by 0.08% to $63.64 following the weekly API report released yesterday which showed that US crude oil stocks declined by 1.562 million barrels in the week ending November 3. Analysts expected a bigger fall of 2.700 million barrels.

XAUUSD Intraday Analysis

XAUUSD (1277.89): Gold prices have remained range bound with price action seen trading sideways within the 1285 resistance level and 1262 support level. The newly plotted falling trend line is also seen being breached with price action briefly testing the trend line on a dip. This suggests some upside momentum. Resistance is seen at 1285 level, and a breakout above this level is essential for gold prices to post further gains. Above 1285 resistance, we can expect gold prices to eventually post a correction towards 1320 - 1324 resistance level.

USDJPY Intraday Analysis

USDJPY (113.76): The USDJPY recovered the losses from Monday, but price action remains muted near the 114.07 - 114.31 resistance level. Failure to break past this resistance level continues to increase the downside risks in price. Currently, the sideways range is expected to continue although, on the 4-hour chart, the break of the rising trendline could suggest some downside momentum. Support is seen at 113.00 which could be tested and would mark a correction to the downside. The inverse head and shoulders continuation pattern looks to be weakening in this scenario, and we expect that USDJPY could be posting further correction to the downside.

EURUSD Intraday Analysis

EURUSD (1.1596): The EURUSD fell to the previously established low near 1.1573 on Tuesday, but price action was seen rebounding off this level. We expect the near-term upside to continue but following which we could see another attempt to break past the lows of 1.1573. To the upside, the gains will be likely limited to the short-term resistance level formed at 1.1610 with a breakout above this level pushing EURUSD towards the main resistance area of 1.1710 - 1.1688. Failure to break past the 1.1573 low could potentially invalidate the bearish flag pattern

Euro Continues To Extend Losses. RBNZ Meeting Coming Up

The markets were seen trading subdued yesterday as the US dollar briefly maintained the gains. The euro was seen weakening as economic data showed that German industrial output fell 1.6% on the month in September. This was stronger than the 0.8% decline that was forecast. As a result, the EURUSD fell to mid-July lows briefly at 1.1585 and extended strong losses against the British pound as well.

Oil prices were seen stabilizing following the recent rally. Crude oil futures closed 0.3% lower on the day. As a result, the Canadian dollar was also trading soft. The BoC Governor Poloz said yesterday that inflation was seen within the normal tolerance level for the central bank.

Looking ahead, the RBNZ's monetary policy meeting is expected to be announced today. The RBNZ's Overnight cash rate is widely expected to remain unchanged at 1.75%.