Sample Category Title

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3124; (P) 1.3150; (R1) 1.3193; More....

Intraday bias in GBP/USD remains neutral at this point. Consolidation from 1.3026 is still in progress. In case of stronger rise, upside should be limited below 1.3337 resistance to bring fall resumption. Break of 1.3038 will now resume decline from 1.3651 to 1.2773 key support level. However, decisive break of 1.3337 will indicate that pull back from 1.3651 is completed and medium term rise from 1.1946 is resuming.

In the bigger picture, as noted before, GBP/USD hit strong resistance from the long term falling trend line. Current development is starting to favor that corrective rebound from 1.1946 low has completed at 1.3651. Decisive break of 1.2773 will confirm this bearish case and target a test on 1.1946 low next, with prospect of resuming the low term down trend. Nonetheless, break of 1.3320 resistance will restore the rise from 1.1946 for 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

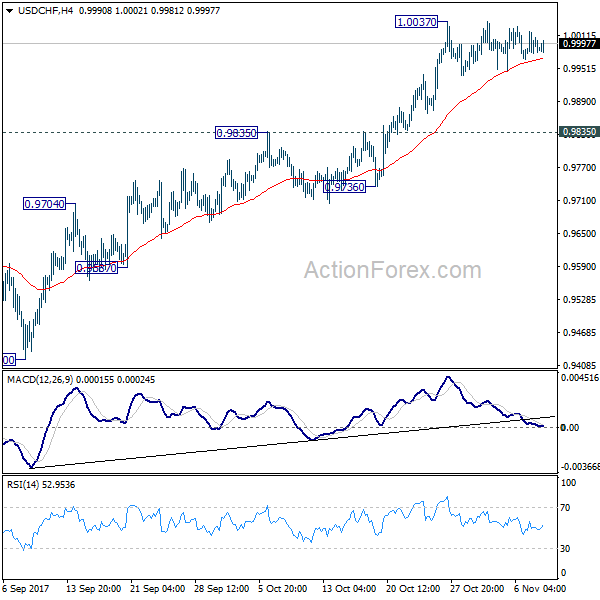

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9972; (P) 0.9995; (R1) 1.0026; More....

Intraday bias in USD/CHF stays neutral at this point as consolidation from 1.0037 is extending. In case of deeper retreat, downside should be contained above 0.9835 resistance turned support and bring rally resumption. On the upside break of 1.0037 will resume whole rally from 0.9420. And with sustained trading above 61.8% retracement of 1.0342 to 0.9420 at 0.9990, USD/CHF should then target a test on 1.0342 key resistance.

In the bigger picture, current development suggests that USD/CHF has defended 0.9443 (2016 low) key support level again. Rise from 0.9420 could is a medium term up move and should target a test on 1.0342 high. This represents the upper end of a long term range that started back in 2015. On the downside, break of 0.9736 support is now needed to indicate completion of the rise from 0.9420. Otherwise, further rally will remain in favor in medium term.

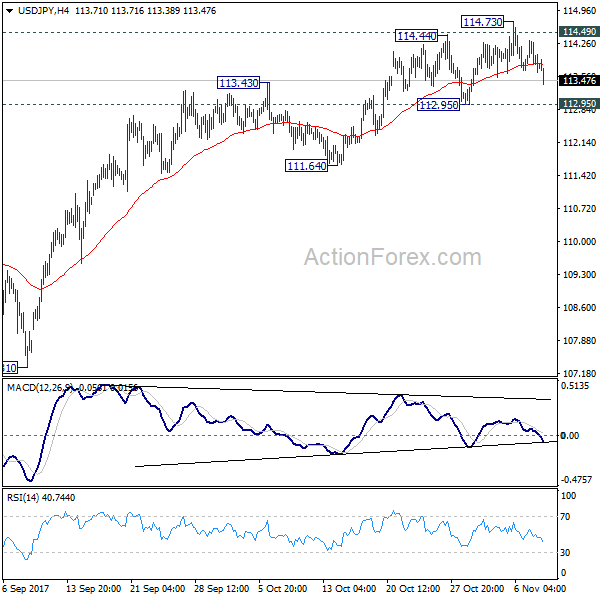

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 113.67; (P) 114.00; (R1) 114.31; More...

USD/JPY dips notably today as pull back from 114.73 extends lower. But still, with 112.95 support intact near term outlook stays bullish and further rally is in favor. Sustained trading above 114.49 key resistance will pave the way to retest 118.65 high. However, break of 112.95 support will now indicate rejection from 114.49 and turn bias to the downside for 111.64 support and below.

In the bigger picture, medium term rise from 98.97 (2016 low) is not completed yet. It should resume after corrective fall from 118.65 completes. Break of 114.49 resistance will likely resume the rise to 61.8% projection of 98.97 to 118.65 from 107.31 at 119.47 first. Firm break there will pave the way to 100% projection at 126.99. This will be the key level to decide whether long term up trend is resuming.

Yen Surges on Global Flattening Yield Curve

Yen trades broadly higher today following a so called flattening yield curve phenomenon globally. 10 year German bund yields extends recent decline and hits a two month low at 0.32 today. 2 year yield was flat at -0.76% and that makings the 108 basis points spread the lowest in two months. Similar situation is seen in US with spread between 2- and 10-year yield at 67 basis points, lowest in nearly a decade. Economists see that as a sign of worry over inflation path. That is, inflation might not be heading up while global central banks begin tightening policies. Meanwhile, sentiments were also weighed down by uncertainty over the US tax plan as there were reports that Senate Republican could delay corporate tax cuts by a year to comply with Senate rules.

Technically, USD/JPY is so far holding well above 12.95 near term support despite today's dip. Hence, outlook in USD/JPY stays bullish. However, EUR/JPY as taken out 131.65 key near term support again. GBP/JPY also breaches 148.65 minor support. Both developments suggests more downside should be seen in EUR/JPY and GBP/JPY in near term.

Sterling lower as PM May could fire another minister

Sterling tumbles broadly today on news that Prime Minister May could lose a second member of her cabinet within a week. International Development Secretary Priti Patel could follow Defense Secretary Michael Fallon to be shown the door by May. The political turmoil and scandals add to undermining May's authority, with no tangible progress shown on Brexit negotiation so far.

Accord to a BoE report, regional agents found that hiring difficulties were "above normal" a some sectors. And, pay growth had already begun to head up. More upside pressure in wages would be seen in 2018. Meanwhile, overall growth in activity was "broadly stable" comparing to a year ago. Strongest growth was found in manufacturing. Services growth was moderate. Economic uncertainties were weighing on constructions. In particular, the uncertainty around Brexit negotiations was "dragging on spending".

German Merkel making progress in coalition talks

German Chancellor Angela Merkel seems to be making progress in her coalition talks. The Green party has agreed to compromise on key environmental issues with the pro-business Free Democratic Party. Greens admitted that the target to ban on internal combustion engines by 2030 wouldn't be enforceable. The request for shutting down 20 most polluting coal-fired power plants by 2020 will also be modified. Now it's the time for AfD to respond. Merkel targets to end the exploratory talks and start serious negotiation on coalition by November 16. .

Staying in Germany, a five-member Council of Economic Experts urged ECB to "quickly reduce the purchases and end them earlier". The group said that interest rate developments "suggest the ECB should significantly tighten its monetary policy to adapt to macro economic developments". The German economy is believed by the group to be heading for a "boom phase" with growth hitting 2.2% next year, an upward revision of prior expectation of 2.0%. Meanwhile, the group also warned that "hard Brexit" could create upheaval in EU. And, the "one-off extension that largely preserves the status quo would be sensible".

IMF Lagarde hails BoJ Kuroda

IMF Managing Director Christine Lagarde hailed that BoJ was doing the correct thing to maintain the pledge on the massive stimulus. She noted that "one of the strengths of central bankers is to be very clear in their communication and determined in their resolve, which clearly Governor Kuroda has demonstrated."

BoJ board member Yukitoshi Funo also defended the central bank's massive asset purchase program. And even with the JPY 6T ETF purchases, "stock prices aren't overheating". But he also sounded open to tweaking of the program and said "we're not assuming we won't make any changes to all of our various policy tools until 2 percent inflation is achieved."

RBNZ to stand pat as overhaul starts

RBNZ rate decision will be the main focus in upcoming Asian session. The central bank is widely expected to keep OCR unchanged at 1.75%. Acting Governor Grant Spencer will stay in change until next March. New Zealand Finance Minister Grant Robertson has launched a review on RBNZ mandate earlier this week. Additional mandate could include employment as monetary policy goals, but exchange rate won't be. But after all, it's perceived that the revision will raise the bar for a rate hike by RBNZ, and make monetary policies friendly to the labor-led government's expansionary fiscal policy.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 113.67; (P) 114.00; (R1) 114.31; More...

USD/JPY dips notably today as pull back from 114.73 extends lower. But still, with 112.95 support intact near term outlook stays bullish and further rally is in favor. Sustained trading above 114.49 key resistance will pave the way to retest 118.65 high. However, break of 112.95 support will now indicate rejection from 114.49 and turn bias to the downside for 111.64 support and below.

In the bigger picture, medium term rise from 98.97 (2016 low) is not completed yet. It should resume after corrective fall from 118.65 completes. Break of 114.49 resistance will likely resume the rise to 61.8% projection of 98.97 to 118.65 from 107.31 at 119.47 first. Firm break there will pave the way to 100% projection at 126.99. This will be the key level to decide whether long term up trend is resuming.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 03:45 | CNY | Trade Balance (CNY) Oct | 254B | 275B | 193B | |

| 03:50 | CNY | Trade Balance (USD) Oct | 38.2B | 39.5B | 28.5B | |

| 05:00 | JPY | Leading Index Sep P | 106.6 | 106.6 | 107.2 | |

| 13:15 | CAD | Housing Starts Oct | 223K | 220K | 217K | 219K |

| 13:30 | CAD | Building Permits M/M Sep | 3.80% | 0.70% | -5.50% | -5.10% |

| 15:30 | USD | Crude Oil Inventories | -2.5M | -2.4M | ||

| 20:00 | NZD | RBNZ Rate Decision | 1.75% | 1.75% |

Canadian Dollar Improves on Poloz Talks Hawkish

The Canadian dollar has gained grounds in the Wednesday session, recovering most of the losses from Tuesday. Currently, USD/CAD is trading at 1.2731, down 0.36% on the day. On the release front, the focus is on Canadian housing data. Housing Starts is expected to slip to 211 thousand, while the markets are forecasting a strong rebound for Building Permits, with an estimate of 0.7%. On Thursday, Canada releases the New Housing Price Index, while the US will publish unemployment claims.

The Canadian dollar received a boost from BoC Governor Stephen Poloz on Tuesday, after Poloz maintained a neutral stance towards interest rates. Poloz said that the Bank continued to monitor how the economy was doing after rate hikes in July and September. The markets were caught off guard by the September move, and the Canadian dollar responded with strong gains. Poloz did not offer any insight as to future rate hikes, leaving the markets guessing regarding a December rate hike. Poloz added that he was not concerned that inflation remains below the BoC's target of 2 percent. The BoC will have to keep a close eye on the US, as the Federal Reserve is almost certain to raise rates in December. If the BoC does not match the hike, the Canadian dollar will likely weaken against the greenback.

US President Trump is off in Asia, but there is plenty of activity in Congress. After failing to pass a new healthcare act, President Trump has his sights set on tax reform, a key item in his domestic platform. Trump wants Congress to pass legislation overhauling the tax code before the end of the year, but that could prove to be too tight of a deadline. Most Democrats have come out against the proposal, and not all Republicans are on board. The bill would cut corporate taxes from 35% to 20%, but predictably, Democrat and Republican lawmakers are at odds as to whether the bill will lower taxes for the middle class. The bill is presently being debated in a congressional committee and is expected to move to the House floor next week. The Senate will present its version of the bill on Thursday, so we can expect plenty of activity in Congress in the next few weeks. Expectations that Trump will cut taxes has been the catalyst for a stock market rally over the past year, and if the bill does become law, the US dollar will likely gain ground.

USDJPY Remains Vulnerable On Correction

USDJPY - The pair remains weak and vulnerable to the downside. On the downside, support comes in at the 113.50 level where a break if seen will aim at the 113.00 level. A cut through here will turn focus to the 112.50 level and possibly lower towards the 112.00 level. On the upside, resistance resides at the 114.50 level. Further out, we envisage a possible move towards the 115.00 level. Further out, resistance resides at the 115.50 level with a turn above here aiming at the 116.00 level. On the whole, USDJPY faces pullback threats on correction

Trump Rally Alive and Well

- One Year on and the Trump Rally is Very Much Alive and Well;

- USD Consolidating But Further Gains May Lie Ahead;

- GBP Under Pressure as May's Problems Mount;

- Oil Inventories Eyed as Oil Rally Continues.

One Year on and the Trump Rally is Very Much Alive and Well

One year on from Donald Trump's election victory and US equity markets are on course to open near record highs once again, having made stunning gains over the last 12 months - more than 30% in the case of the Dow and Nasdaq.

While many may claim that Trump's achievements to date equate to very little given his difficulties repealing and replacing Obamacare, slower than expected progress on tax reform and minimal detail on fiscal stimulus, investors have clearly not been deterred as is evident by staggering gains in US stocks. Of course, much of this may still be conditional on the President delivering on the latter two in particular and some is also attributable to the rally in global equity markets over the same period, but the Trump trade is clearly still alive and well.

This is despite the fact that the Fed has raised interest rates three times since the election and is likely to do so again next month, which many will have believed could have threatened the economic recovery and with that, the stock market rally. That is clearly not the case and with the economy having now come off two quarters of around 3% annualised growth, one may wonder whether there is any need for the spending element of the President's plan to revive the economy. There certainly doesn't appear to be the desire for it that we've seen for tax reform over the course of the year.

While political and geopolitical events have caused minor problems along the way, the rally has been very gradual and consistent with few hiccups along the way. In the absence of any major US economic events this week, Trump's tour of Asia will continue to attract the bulk of the attention, although I imagine the rhetoric coming from the meetings and press conferences will be broadly in line with what we've heard already. Assuming no slip ups along the way and no unexpected back and forth with North Korea - which is possible given the country is one of the main topics of conversation - there's little reason to believe we won't see more of the same in the markets.

USD Consolidating But Further Gains May Lie Ahead

The US dollar has consolidated over the last couple of weeks since rebounding off its lows on the prospect of more rate hikes and tax reform progressing more smoothly than thought - albeit not as quickly as one would hope. The greenback is still looking bullish into the end of the year though and the appointment of Jerome Powell as Janet Yellen's replacement as Chair should support this, particularly if he is accompanied by other hawkish appointments on the board.

GBP Under Pressure as May's Problems Mount

It's been a relatively slow week for the markets so far, despite there being a number of concerning political stories than have the potential to cause further disruption down the line. The UK as ever is right at the top of this list, with Prime Minister Theresa May in the uncomfortable position of potentially being forced to sack another member of her cabinet at a time when her position is already seen by many as untenable in the aftermath of her disastrous election campaign.

Still, the softness we're seeing in the pound today is likely more a reflection of the Bank of England's decision to raise interest rates last week while adopting a dovish stance on future hikes. While much of the move was priced in on Thursday, we have seen a minor pullback since and I think today's drop is simply a continuation of Thursday's initial decline. The pound will face a big test around 1.30-1.3050 against the dollar should we reach those levels and a break of this could trigger a move back towards 1.28.

Oil Inventories Eyed as Oil Rally Continues

The one notable release today will be crude inventory numbers from EIA which come after API reported another small drawdown on Tuesday and as the political situation in Saudi Arabia - OPEC's largest producer - becomes a growing concern. I don't think this has been a big factor in oil's recent rise given the talk of an output cut extension next year, growing demand forecasts and the stabilisation in US output. With momentum not slowing though there does appear to be more upside potential and the situation in Saudi Arabia may be supportive of this the longer is goes on.

USDJPY Strongly Bearish Below 113.68 Level

The U.S dollar has slipped below key support against the Japanese yen during the European trading session, hitting 113.55, as the U.S tax reduction plan faces a possible set back later today. The U.S Dollar index is also sliding lower and stocks are turning down, as the specter of a delay to the proposed corporate tax reduction by the Republican Senate, weighs on overall risk-on trading sentiment. The USDJPY pair currently trades around the price-lows of the day, after earlier breaching the key 113.68 technical level.

Should price action remain below the 113.68 level for a sustained period, further declines towards the 113.33 and 112.90 levels appear most likely. Extended intraday USDJPY support is located at 112.29 and 111.79.

If price-action closes back above the 113.68 level, further upside towards the 113.89 and 114.24 levels remains possible.

GBPUSD Still Intraday Bullish Above 1.3109

The British pound has given back Tuesday's trading gains against the U.S dollar, as UK political woes continue to hamper sterling upside. The GBPUSD pair has declined during the European trading session, as the UK Conservative party faces another scandal, weakening Theresa May's position as British Prime Ministers. Price-action currently trades just below the 1.3130 technical level, after earlier hitting 1.3175, ahead of the start of the U.S trading session.

The GBPUSD pair still retains an intraday bullish bias while trading above the key 1.3109 technical level, further upside attempts towards the 1.3138 and 1.3161 levels remains likely.

Should price-action close below the 1.3109 level for a sustained basis, intraday selling towards the 1.3078 and 1.3030 levels remain likely.

DAX Under Pressure After Weak Corporate Returns

The DAX has ticked lower in the Wednesday session. Currently, the DAX is at 13,358.50, down 0.16% on the day. There are no major events in the eurozone on the schedule. France posted a trade deficit of EUR 4.7 billion, which matched the estimate. On Thursday, Germany releases Trade Balance and the US publishes unemployment claims.

European stock markets dipped on Tuesday, as investors were not impressed with European corporate earnings. The DAX dropped 1.0 percent, and financial stocks were in red territory – Deutsche Bank dropped 0.59% and Commerzbank (DE:CBKG) slid 1.53 percent. The DAX continues to head lower on Wednesday.

Eurozone rebounded sharply in September, pointing to an improvement in consumer spending. The gain of 0.7% came after two straight declines, and marked the strongest gain since February. The markets are hoping for strong eurozone consumer spending in the fourth quarter, given the robust German economy and stronger economic conditions in the eurozone.

After failing to pass a new healthcare act, President Trump has his sights set on tax reform, a key item in his domestic platform. Trump wants Congress to pass legislation overhauling the tax code before the end of the year, but that could prove to be too tight of a deadline. Most Democrats have come out against the proposal, and not all Republicans are on board. The bill would cut corporate taxes from 35% to 20%, but predictably, Democrat and Republican lawmakers are at odds as to whether the bill will lower taxes for the middle class. The bill is presently being debated in a congressional committee and is expected to move to the House floor next week. The Senate will present its version of the bill on Thursday, so we can expect plenty of activity in Congress in the next few weeks. Expectations that Trump will cut taxes has been the catalyst for a stock market rally over the past year, and if the bill does become law, the US dollar will likely gain ground.