Sample Category Title

Dollar Vs Yen Reaches 8-Month High As BOJ’s Kuroda Favors Easy Policy, Oil Pierces 2-Year High

The dollar managed to hit an 8-month high against the yen on Monday in Asia after the BOJ Governor Haruhiko Kuroda signaled a continuation of the current ultra-easy monetary policy, while persistent confidence on the US economy supported the pair as well. Oil recorded a substantial increase, rising to a two-year high amid tightening markets and as anti-corruption measures took effect in Saudi Arabia.

With the economic calendar lacking important data, the dollar index which gauges the dollar's strength against a basket of major currencies was on track to break the 95-key level as investors' expectations of a third Fed-rate hike in December remained high despite a string of mixed data released on Friday.

Against the yen, the greenback touched an 8-month high of 114.72 before it pulled back to 114.37 following dovish remarks by the BOJ Governor Haruhiko Kuroda early in the session. Kuroda claimed that the current ultra-easy monetary policy is accommodative for inflation to reach the BOJ's 2% target, while he added that the central bank was considering long-term risks arising from low-interest rates. Minutes from the BOJ's September meeting showed that a majority of policymakers held the same view, believing that the current policy is sufficient to drive inflation towards the target.

The euro was trading flat around $1.16 ahead of Markit PMI readings and the Sentix index out of the Eurozone later today, with political uncertainties in Spain continuing to weigh on the currency.

The pound was moving sideways around $1.3075, with traders expecting the British Prime Minister, Theresa May, to calm business leaders' fears on cliff-edge Brexit on Monday, showing her commitment to reach a deal on the transitional period.

In other commodities, the kiwi fell 0.32% versus the dollar to $0.6885 with markets anticipating the RBNZ to maintain rates at a record low of 1.75% on Thursday and the new government to reveal its policy plans. Its Australian cousin held steady at $0.7650 ahead of the RBA policy meeting on Tuesday, where policymakers are projected to leave interest rates unchanged at a record low of 1.5%.

Looking at commodities, oil prices jumped to a two-year high on signs that markets are under tightening conditions, while arrests of royals and ministers in Saudi Arabia demanded by the Crown Prince Mohammed bin Salman in an effort to limit corruption in the country added further gains to oil prices. WTI crude was up by 0.84% at $56.11 per barrel and London-based Brent increased by 0.95% to $62.66.

Gold stood flat at $1,269.50 per ounce.

Currencies: Dollar Holds Near The Recent Highs Against The Euro And The Yen

Sunrise Market Commentary

- Rates: Technical resistance nearby, but no breaks expected

Today's eco calendar is uninspiring. We have no strong view on trading and expect sentiment-driven action. Core bonds could be lured towards nearby resistance levels, but we don't anticipate breaks higher. Italian BTP's might underperform following regional elections (Sicily) which are a first real barometer for a national vote early next year. - Currencies: Dollar holds near the recent highs against the euro and the yen

On Friday, the payrolls where not strong enough to trigger sustained USD gains, but the USD price action remained constructive. USD/EUR and USD/JPY remain near recent highs. Today, technical traded will probably prevail. The big positive interest rate differential should continue to protect the downside in the major USD cross rates.

The Sunrise Headlines

- US equities eked out modest (S&P) to moderate (NASDAQ) gains on Friday with Apple results and guidance an important driver. New all-time highs for S&P and NASDAQ. Asian equities start the week mixed.

- Saudi Arabia Crown Prince Mohammed bin Salman ordered Saturday night an anti-corruption crackdown. Security forces arrested princes, billionaires, ministers and former top officials including the well-known Alwaleed bin Talal.

- Ousted Catalan president Puigdemont and 4 former government members were released in Brussels pending a court ruling on an international arrest warrant issued by Spain. The tension between Madrid and Barcelona remains.

- US Commerce Secretary Wilbur Ross has investments in a shipping firm with ties to Putin's circle, according to the Paradise Papers reports. Also Trump's son-in-law and confident Kushner is apparently named.

- A fresh round of Brexit talks kicks off this week, which should be the focus of the UK government. However, PM May's big announcement was a new code of conduct for Conservative politicians in the wake of a sexual harassment scandal that's forced the resignation of her defence secretary.

- BOJ governor Kuroda confirmed that the BOJ will persistently continue powerful easing and that there is still a long way to getting to 2% inflation.

- Today's eco calendar is unattractive, but political issues might impact trading. US President Trump's Asian tour will be extended by one day

Currencies: Dollar Holds Near The Recent Highs Against The Euro And The Yen

Dollar holding near recent highs

On Friday, the US payrolls were a mixed bag and failed to give clear guidance for USD trading. Later in the session, a strong US non-manufacturing ISM and upbeat US equity performance supported the dollar slightly. EUR/USD finished the session at 1.1608 (from 1.1658). USD/JPY closed to session almost unchanged at (114.07).

Overnight, Asian equities are trading mixed. The PBOC warned on the risks of too high leverage. BOJ's Kuroda said that the BOJ wants inflation the overshoot the 2% target, suggesting the ultra-loose BOJ policy won't be scaled back anytime soon. USD/JPY spiked temporary north of the 114.45 resistance, but trades currently again near 114.30. Markets keep an eye on the topics that are handled during the Asian trip of US President Trump. EUR/USD is holding stable in the low 1.16 area.

Today, the final October EMU services PMI's will be released, but they are usually close to the preliminary results. The event calendar is also thin with only speeches of NY Fed Potter and NY Fed president Dudley. They speak about policy & balance sheet and lessons from the financial crisis. From ECB side, governor Praet, Visco, Hansson, Villeroy and Mersch will speak but we don't expect new info shortly after the ECB meeting. Politics will also get a lot of attention with Brexit talks and UK May's precarious position, the increased tensions between Spain & Catalonia, the Asia trip of Trump and the negotiations on the US tax plan the main features.

Last week, EUR/USD held close to the post-ECB low, but there were no followthrough losses of the euro. The nomination of Powell as next Fed-Chairman, new proposals to change the US tax code and Friday's payrolls were not able to break this stalemate. For now, the dollar fails to really profit from high interest rate differentials (especially at the short end of the curve). This is slightly disappointing for USD bulls. That said, EUR/USD currently trades more than 400 ticks below the cycle top. The wide positive interest rate differential should give the dollar downside protection unless there is high profile US negative news. However, additional rate support for the dollar will probably be modest near term. So, further EUR/USD decline might develop gradually. We maintain a cautious sell-on-upticks bias.

From a technical point of view, EUR/USD dropped below 1.1670/62 support, but no convincing follow-through dollar gains occurred. If the break is confirmed, it would confirm that the recent EUR/USD uptrend is broken. EUR/USD 1.1423 (38% retracement of 2017 rise) is the next downside target on the charts. USD/JPY's momentum was positive in past months. The pair regained 110.67/95 resistance and now tests the 114.49 correction top. A sustained break would further improved the technicals. We remain cautious to preposition for further USD/JPY gains.

EUR/USD broke below 1.1662 support, but non follow-through price action yet

EUR/GBP

Post-BoE sterling decline slows

On Friday, sterling reversed a (small) part of the losses it suffered on Thursday when the BoE indicated that the future rate hike path will be extremely gradual. The sterling rebound was reinforced by a strong UK services PMI. The (modest) intraday decline of EUR/USD also weighed slightly on EUR/GBP. EUR/GBP closed the session at 0.8877 (from 0.8927). The gain in cable was more modest as the dollar captured a better momentum later in the session. The pair finished the session at 1.3077 (from 1.3059).

Today, markets look out for a meeting of UK PM May at the Confederation of British industry. UK business are eager to hear whether the UK will be able to obtain a transition period in the Brexit negotiations with the EU. At the same time, there are still plenty of headlines on scandals that members of the UK government might be involved in. We start the week with a neutral bias on sterling. However, sterling faces plenty of political event risk. (Brexit negotiations restart this week).

In September, sterling rebounded as the BoE prepared markets for a rate hike. This rebound ran into resistance as markets anticipated that any rate hikes would be very gradual and limited. This view was confirmed at last week's BoE policy meeting. EUR/GBP currently trades in a 0.8733/0.9033 consolidation range. A downside test of this range was rejected last week. We maintain the view that the 0.8733 -0.8652 support area will be though to break in a sustainable way. A EUR/GBP buy-on-dips approach is favoured. 0.9023/33 is the first important resistance for the EUR/GBP cross rate

EUR/GBP: rebounds off 0.8733/43 support on soft BoE policy assessment

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.1607

The recent peak at 1.1690 signals a finale of the consolidation pattern above 1.1570 and the outlook is bearish, for a break through 1.1600, towards 1.1480. Minor intraday resistance lies at 1.1635.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.1635 | 1.1840 | 1.1600 | 1.1480 |

| 1.1720 | 1.1940 | 1.1480 | 1.1300 |

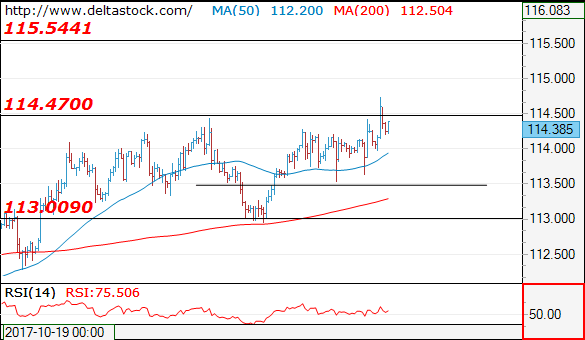

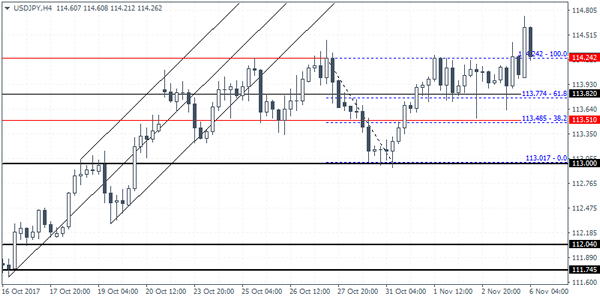

USD/JPY

Current level - 114.38

The bias is positive, for a rise towards 115.50. Crucial on the downside is 113.50.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 114.80 | 115.50 | 113.50 | 111.00 |

| 115.50 | 116.80 | 113.05 | 107.30 |

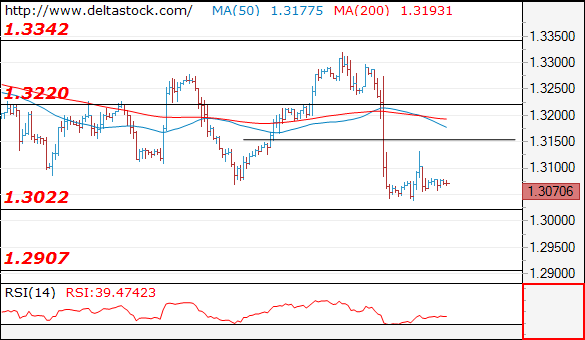

GBP/USD

Current level - 1.3070

The outlook remains bearish below 1.3150 resistance, for a violation of 1.3020 lows, towards 1.2907 zone.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3150 | 1.3220 | 1.3020 | 1.3020 |

| 1.3150 | 1.3340 | 1.2910 | 1.2760 |

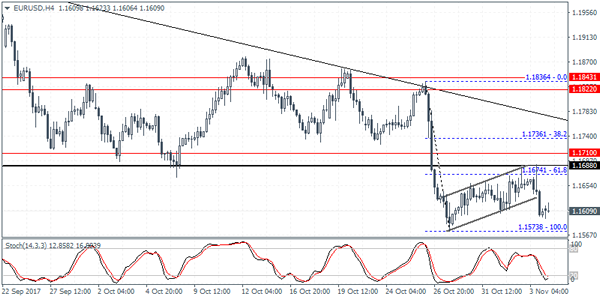

EURUSD Maintains Its Bearish Outlook, Shows Stability In Near-Term

EURUSD maintains its bearish outlook after the breakdown of the key level at 1.1660. The chart pattern on the daily time frame indicates a head and shoulders pattern with a break below the neckline giving a bearish signal.

Resistance at 1.1660 is expected to hold in the near term, as EURUSD continues to trade in a small range just below this level. A daily close below 1.1600 would increase downside pressure and open the way to 1.1470. This level is roughly the mid-point of the upleg from 1.0820 to 1.2091. A deeper decline would target 1.1300, which is the 61.8% Fibonacci retracement level.

A rise above the 50-day moving average and above the right-shoulder high of 1.1874 would confirm the short-term bearish phase has ended. This would bring a re-test of the 1.2091 peak before the resumption of the uptrend from the April lows.

Technical indicators are bearish but RSI is suggesting the near-term bias is neutral. In the bigger picture, sustained trading below the 50-day moving average will keep the bearish outlook in place.

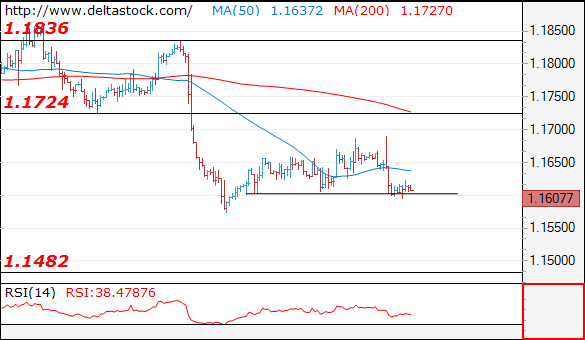

EURUSD Strongly Bearish Below 1.1640 Level

The euro continues to remain weak against the U.S dollar, following solid U.S economic data, and another bearish technical weekly price-close. The EURUSD pair is currently trading just above the key 1.1610 support level, after again being swiftly rejected from its 200-week moving average, located at 1.1670. Euro traders now await a raft of economic data coming out from the Eurozone this morning and the start of the Eurogroup meetings from Luxembourg.

The EURUSD pair remains strongly bearish while trading below the 1.1640 technical level. Further intraday selling towards 1.1573 and 1.1510 levels remains most likely, while price-action holds below the 1.1640 level.

Should price-action move above the 1.1640 level for a sustained basis, further upside towards the 1.1670 and 1.1690 remains most likely.

USDJPY Interday Bullish ABove 114.24

The U.S dollar has moved sharply higher against the Japanese yen, hitting 114.73, as Asian investors reacted to Friday's solid NFP job report from the United States. Price-action has now pulled back towards 114.35 support region, following the Bank of Japan Meeting Minutes. The Meeting Minutes showed no change in fiscal policy, however, Goushi Kataoka, a new member of the policy board, dissented and argued against the BOJ's view that current policy is sufficient to meet its target.

The USDJPY pair remains intraday bullish while trading above the 114.24 level. Further upside towards the 114.50 and 114.75 technical level should occur while price-action holds above 114.24.

Should price action decline below the 114.24 level for a sustained period, further intraday losses towards the 113.89 and 113.57 support levels remains likely.

Eurozone Data Takes The Fore

Europe will move the markets on Monday, as investors get set to digest a flurry of economic data from the currency region.

Activity begins at 07:00 GMT with a report on German factory orders. Factory output in Europe’s largest economy is forecast to drop 1.5% in September, after rising 3.6% the previous month.

The Swiss government will report on consumer inflation at 08:15 GMT. The monthly report is expected to show a 0.2% increase in October, following a similar gain the previous month. This likely translates into an annualized gain of 0.8%.

Investors can also expect multiple PMI reports courtesy of IHS Markit. The research group will report on Italian, French, German and Eurozone services activity between 08:15 GMT and 0:9:00 GMT. The monthly reports will also include the Composite PMI indicator, which gauges manufacturing and services activity. Germany’s Composite gauge is expected to show a reading of 56.9. The euro area Composite indicator is expected to come in at 54.9.

At 09:30 GMT, Sentix will release its investor confidence index. The monthly gauge is expected to show an increase to 30.8 in November from a reading of 29.7 the previous month.

Meanwhile, a report on Eurozone inflation will make headlines at 10:00 GMT. The monthly producer price index (PPI) is expected to rise 0.4% in September, translating into a 2.8% year-over-year gain.

Shifting gears to North America, US Federal Reserve Chairwoman Janet Yellen will deliver a speech at 13:00 GMT. Yellen will be replaced by Fed Governor Jerome Powell as Chair of the US central bank next February.

New York Fed President William Dudley will also deliver a speech at 17:00 GMT.

Earlier in the day, the Reserve Bank of New Zealand (RBNZ) reported a slight downtick in inflation expectations. Third quarter inflation expectations slipped to 2% annually, official data showed. That’s down from 2.1% the previous month.

EUR/USD

The euro was practically motionless on Monday, as market participants awaited key economic data. The EUR/USD exchange rate was last seen trading at 1.1612, where it was little changed compared with the previous close. The euro is vulnerable to further weakness but continues to trade in a narrow range.

GBP/USD

Cable was little changed on Monday, as a dearth of market-moving developments kept investors on the sidelines. The GBP/USD exchange rate continues to hold above 1.3000, with upside limited to 1.3111, which is the high from Friday.

NZD/USD

The New Zealand dollar fell against the greenback on Monday, as investors digested the latest inflation figures. The NZD/USD was down 0.2% at 0.6890, extending a three-week downtrend that has wiped more than 300 pips from the pair. The pair is expected to fall even further as the RBNZ remains on hold with respect to monetary policy while the Federal Reserve signals for higher rates. The NZD/USD faces immediate support at 0.6820. On the opposite side of the ledger, resistance is located at 0.6992.

EURGBP Intraday Analysis

EURGBP (0.8880): The EURGBP which posted strong gains on Thursday on the back of the BoE's rate hike was seen giving up some of the gains. EURGBP could be seen pushing lower as price action approaches the breached resistance and support level near 0.8867 - 0.8857. Establishing support at this level will suggest renewed bullish momentum to the upside. The next main target for EURGBP comes in at 0.9016. However, in the event that EURGBP slips below 0.8857, the bias could turn bearish as EURGBP risks pulling down lower towards 0.8778.

USDJPY Intraday Analysis

USDJPY (114.26): The USDJPY closed with a doji candlestick pattern on the daily chart on Friday. This comes near the resistance level of 114.31 - 114.07. Price action has been struggling to break out from this resistance level in the past few sessions but with little success. On the 4-hour chart, the inverse head and shoulders pattern was, however, validated as USDJPY broke out above 114.24. As long as this price level holds, USDJPY could be seen pushing higher. A close below 114.24 on the intraday basis could, however, signal the sideways momentum to continue.

EURUSD Intraday Analysis

EURUSD (1.1609): The EURUSD closed on a bearish note on Friday. The bearish engulfing pattern formed on the daily chart could suggest further downside momentum. On the 4-hour chart, price action has broken out from the bearish flag pattern. However, the EURUSD will be seen testing the previous lows near 1.1573. A break down below this low will indicate further declines in price. Alternately, if support is established higher, EURUSD could remain range bound and potentially invalidating the bearish outlook.