Sample Category Title

Market Update – European Session: Euro Zone PMI Services Mainly Revised Lower, Sentix Confidence At Fresh 10-Year High

Notes/Observations

PMI Services data mostly comes in below expectations (Miss: Italy, France, Germany; Beat: Euro Zone)

Euro Zone Sentix Confidence Index at fresh decade high

Overnight

Asia:

Bank of Japan (BOJ) Gov Kuroda reiterated BOJ to continue with powerful easing; Price moves weak compared with improvement in the economy. Corporate price setting stance was key to BOJ outlook. Expected companies' stance on prices and wages to become more bullish

Bank of Japan (BOJ) Sept 20-21st Policy Meeting Minutes (2 meetings ago) noted that momentum towards price goal was being maintained. Discussed market participants concerns about YCC; most members shared view that BoJ should stick with current policy

During President Trump's visit to the country, Japan to tell US it will strengthen sanctions against North Korea

Europe:

ECB's Coeure (France) reiterated General Council view that exchange rate is not an ECB policy targe

Eurogroup Chief Dijsselbloem (outgoing): Will select the next head at the Dec meeting

ECB’s Smets (Belgium): To take some time until accelerating growth leads to wage pressure and inflation (in-line with general Council view)

BOE Gov Carney reiterated view that recent BoE rate hike is a modest adjustment. Possible that in the event of a bad Brexit deal, the BOE would not be able to cut interest rates in future because of that inflationary pressures

Italy President Mattarella could dissolve Parliament before end of 2017 in order to prepare for possible elections next March

Former Catalan President Puigdemont said to be released from custody with conditions. Puigdemont and four of his ministers were released by a judge in Belgium and the individuals are said to have been ordered to remain in Belgium at their given addresses. extradition is expected in 15 days

Americas:

NY Fed President Dudley (FOMC voter) to retire before term expires in Jan 2019; could leave as soon as the Spring of 2018

Treasury Sec Mnuchin reiterated goal to get tax bill to President Trump in 2017

Energy:

Saudi Arabia’s Crown Prince ordered the arrest of individuals including members of the royal family, ministers and investors. Eleven princes and four ministers were said to have been among those who were detained, along with businessman Alwaleed bin Talal.

Economic Data

(DE) Germany Sept Factory Orders M/M: +1.0% v -1.1%e; Y/Y: 9.5% v 7.1%e

(BR) Brazil Oct FIPE CPI (Sao Paulo) M/M: 0.3% v 0.3%e

(ES) Spain Oct Services PMI: 54.6 v 55.6e (48th month of expansion), Composite PMI: 55.1 v 54.6e

(CH) Swiss Oct CPI M/M: 0.1% v 0.1%e; Y/Y: 0.7% v 0.7%e

(CH) Swiss Oct CPI EU Harmonized M/M: 0.1% v 0.2% prior; Y/Y: 0.8% v 0.8% prior

(SE) Sweden Sept Industrial Production M/M: 2.2% v 2.0%e; Y/Y:4.5 % v 4.0%e

(IT) Italy Oct Services PMI: 52.1 v 52.9e (17th month of expansion but lowest since Oct 2016), Composite PMI:52.9 v 54.3e

(FR) France Oct Final Services PMI: 57.3 v 57.4e (confirmed 16th month of expansion and highest since March), Composite PMI: 57,4 v 57.5e

(DE) Germany Oct Final Services PMI: 54.7 v 55.2e (confirmed 52nd month of expansion and highest since Feb), Composite PMI: 56.6 v 56.9e

(EU) Euro Zone Oct Final Services PMI: 55.0 v 54.9e (confirmed 52nd month of expansion), Composite PMI: 56.0 v 55.9e

(EU) Euro Zone Sept PPI M/M: 0.6% v 0.4%e; Y/Y: 2.9% v 2.7%e

Fixed Income Issuance:

(NO) Norway sold NOK3.0B vs. NOK3.0B in 3-month Bills; Avg Yield: 0.43% v 0.38% prior; Bid-to-cover: 2.43x v 3.13x prior

Equities

Indices [Stoxx600 flat at 395.9 FTSE -0.1% at 7549, DAX -0.2 at 13453, CAC-40 -0.2 at 5507, IBEX-35 -0.3% at 10324, FTSE MIB -0.2% at 22963, SMI +0.1% at 9291, S&P 500 Futures +0.1%]

Market Focal Points/Key Themes:

European Indices trade slightly lower across the board consolidating recent gains, as the Spanish Ibex once again under performs.

Deutsche Telekom trades over 3% lower after majority owned T-Mobile ended merger talks with Sprint, while on the earnings front Vopak in the Netherlands reported weak results, while Post NL shares trade higher after Q3 results and affirmed outlook. Elsewhere Aldermore trades higher after the board approved the takeover approach from FirstRand, while in the healthcare space UCB trades higher after the FDA approves label extension for brivaracetam.

Looking ahead notable earners include Cardinal Health and Sysco.

Consumer discretionary [WIZZ.UK] +1.3% (Oct metric)]

Industrials: [Post NL [PNL.NL] +4.6% (Earnings)]

Financials: [Aldermore [ALD.DE] +2.4% (Board approves takeover by FirstRand for 313p/shr), Carillion [CLLN.UK] +2.2% (Contract win)]

Telecom: [Deutsche Telekom [DTE.DE] -3.1% (T-Mobile and Sprint end merger talks)]

Healthcare: [UCB [UCB.BE] +1.8% (FDA approves label extension for UCB's brivaracetam for the treatment of partial onset seizures in pediatric epileptic patients)]

Real Estate: [Vopak [VPK.NL] -5.1% (Earnings)]

Speakers

ECB's Praet (Belgium, chief economist) reiterated that substantial amount of accommodation is needed (in-line with General Council). Extension of QE program was justified by the continuing need for substantial monetary policy support

PM May: Pleased there has been progress on post-Brexit citizens right

Portugal Econ Min Cabral: Growth at 3.0% was sustainable

Japan Dep Chief Cabinet Sec Nishimura: Trump and Abe did not discuss any bilateral Free tared Agreement (FTA)

Currencies

USD was holding onto recent gains against the major pairs as markets believed that despite the softer-0than-expoecte jobs data on Friday there was little change in market expectations for the Fed to raise interest rates in December for a third time this year

USD/JPY pair hit 8-month highs just under 114.75

Fixed Income

Bund futures trade at 163.11 up 32 ticks, as the ECB expected to continue to front-load purchases, with focus on the latest monthly PSPP release which will include redemption data. Support lies at 162.00, followed by 161.50. Resistance stands initially at 163.51, followed by 164.25.

Gilt futures trade at 125.25 up 18 ticks and still near the October high. Continued upside eyeing 125.75 then 126.47. Downside targets include 124.90 then 124.24.

Monday’s liquidity report showed Friday’s excess liquidity rose to €1.860T from €1.849T and use of the marginal lending facility fell to €168M from €188M

Corporate issuance saw $26.8B sold last week in the primary market

Looking Ahead

05:25 (BR) Brazil Central Bank Weekly Economists Survey

05:30 (NL) Netherlands Debt Agency (DSTA) to sell €1.0-2.0B in 3-month bills

06:00 (IE) Ireland Sept Industrial Production M/M: No est v 1.4% prior; Y/Y: No est v 1.5% prior

06:00 (IN) India announces details of upcoming bond sale (held on Fridays)

06:30 (CL) Chile Sept Economic Activity M/M: -0.1%e v +0.3% prior; Y/Y: 1.6%e v 2.4% prior

06:30 (TR) Turkey Oct Effective Exchange Rate(REER): No est v 90.3 prior

06:45 (US) Daily Libor Fixing

07:00 (BR) Brazil Oct PMI Services: No est v 50.7 prior; PMI Composite: No est v 51.1 prior

08:05 (UK) Baltic Dry Bulk Index

08:50 (FR) France Debt Agency (AFT) to sell combined €4.2-5.4B in 3-month, 6-month and 12-month Bills

09:00 (MX) Mexico Oct Consumer Confidence: 88.6e v 89.2 prior

09:30 (EU) ECB announces Covered-Bond Purchases

09:35 (EU) ECB calls for bids in 7-Day Main Refinancing Tender

10:00 (CA) Canada Oct Ivey Purchasing Managers Index (Seasonally Adj): No est v 59.6 prior

11:30 (US) Treasuries to sell 3-Month and 6-Month Bills

12:00 (US) Fed's Dudley (dove, FOMC voter) speaks to The Economic Club of New York

16:00 (US) Weekly Crop Progress Report

CRUDE OIL Strong Buying Demand

Crude oil has surged and set up a new resistance at 56.28 (06/11/2017 high). The commodity is trading at 1-year high. Expected to show further shot-term bearish consolidation. Indeed the technical structure has a history of decent consolidation phase.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. For the time being the pair lies in an upside momentum. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).

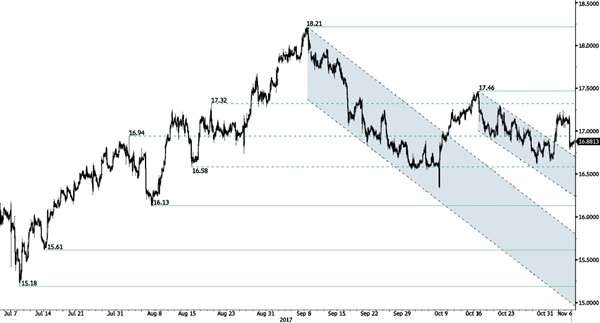

SILVER Selling Pressures Are Back

Silver is back below 17. Hourly support can be found at 16.60 (27/10/2017 low). Hourly resistance is given at 17.46 (13/10/2017 high). Additional support can be found at 16.13 (06/10/2017 low).

In the long-term, the trend is rater negative. Further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

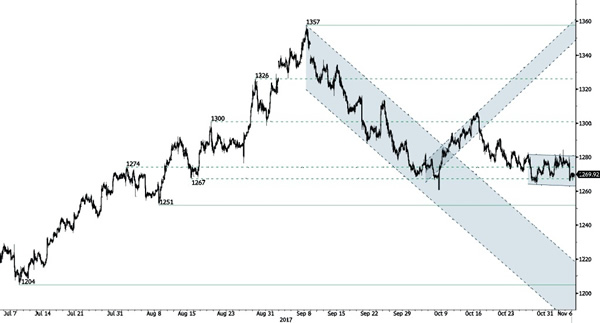

GOLD Range-Trading

Gold remains weak. The technical structure confirms a longer consolidation phase. Support lies at a distance at 1251 (08/08/2017 high). Resistance is now located at 1288 (20/10/2017).

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

BITCOIN Short-Term Consolidation

Bitcoin is now consolidating after setting-up a new all-time high for 4 consecutive days. The technical structure shows a tremendous positive short-term momentum. Hourly support can be located at 6027 (30/10/2017 low). Strong support stands very far at 2975 (22/08/2017 low). In the short-term, the digital currency should continue rising.

In the long-term, the digital currency has had an exponential growth. There are decent likelihood that the asset will reach $10'000.

EUR/CHF Pushing Higher Within Former Uptrend Channel

EUR/CHF is back within former uptrend channel. Support is given at 1.1610 (27/10/2017 low). Rising channel suggests further bullish momentum.

In the longer term, the technical structure has reversed. Strong resistance is given at 1.20 (level before the unpeg). Yet, the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).

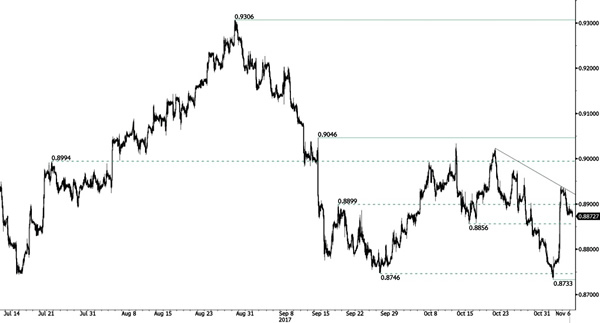

EUR/GBP Bouncing Lower

EUR/GBP is consolidating after the sharp increase. As long as prices are below the resistance at 0.9046 (05/09/2017 high), the shortterm technical structure is biased to the downside. Hourly support is given at a distance at 0.8733 (01/11/2017 low).

In the long-term, the pair has largely recovered from recent lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading above from its 200 DMA. Strong resistance can be found at 0.9500 (psychological level).

AUD/USD Edging Lower

AUD/USD is ready to bounce back but downside pressures are still lively. Hourly resistance is given at a distance at 0.7897 (13/10/2017 high). Expected to show renewed pressures towards key support at 0.7571 (05/07/2017 low).

In the long-term, the trend is turning positive. Key supports stands at 0.6009 (31/10/2008 low) . A break of the key resistance at 0.8164 (14/05/2015 high) is needed to invalidate our long-term bearish view.

USD/CAD Wide-Open For Further Downside

USD/CAD is weakening after set-up a resistance at 1.2917 (27/10/2017 low). This suggests an extension of bullish momentum. Hourly support lies at 1.2331 (26/09/2017 high). Expected to show continued short-term bullish pressures.

In the longer term, the pair has broken longterm support that can be found at 1.2461 (16/03/2015 low). Strong resistance is given at 1.4690 (22/01/2016 high). The pair is likely to head further lower.

USD/CHF Holding Around Parity

.

USD/CHF is consolidating. Yet, the technical structure is still bullish. The technical structure suggests an improving short-term buying interest. Expected to show continued bullish momentum. Hourly support stands at 0.9951 (01/11/2017 low).

In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015.