Sample Category Title

EUR/USD Mid-Day Outlook

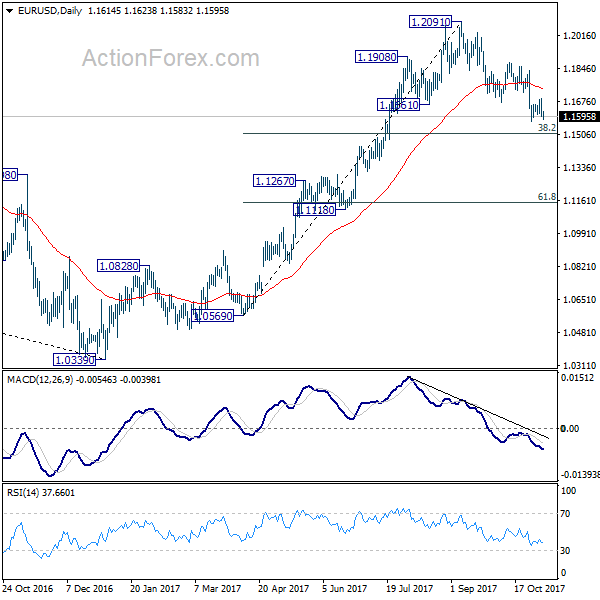

Daily Pivots: (S1) 1.1574; (P) 1.1632 (R1) 1.1666; More...

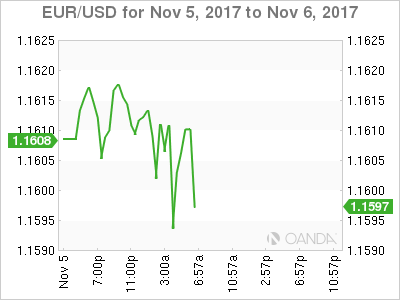

EUR/USD dips mildly today but it's staying above 1.1574 support. Intraday bias remains neutral and more consolidation could be seen. But after all, break of 1.1879 resistance is needed to confirm completion of the decline from 1.2091. Otherwise, near term outlook will stay bearish. Below 1.1574 will target 38.2% retracement of 1.0569 to 1.2091 at 1.1510.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be cautious on 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

Euro Softer in Directionless Markets, Dollar Mixed

The direction in the Forex markets is no too clearly today. Yen was initially sold off earlier but there was no follow through selling so far. Instead, Euro is back under some selling pressure despite solid economic data. On the other hand, Dollar is mixed as US President Donald Trump's trip to Asia is no providing any inspiration to the markets. Instead, eyes will stay on the progress of the tax plan in Congress. But for now, in a rather light week, attention will be on RBA rate decision in the upcoming Asian session.

Trump gives no inspiration as a salesman in Asia

The way US President Donald Trump fed fish in the koi pond in Japan could have caught some headlines. But underneath, Trump is doing his salesman job there in his trip. He claimed that Japan Prime Minister Shinzo Abe will "shoot" North Korean missiles "out of the sky" when Abe completes the "purchase of lots of additional military equipment from the United States". But earlier he accused Japan for the trade surplus with US. He said that "the United States has suffered massive trade deficits at the hands of Japan for many, many years." He went further and said that "right now our trade with Japan is not free and it's not reciprocal" and pledged that "it will be done in a quick and very friendly manner."

Meanwhile the markets are keeping an eye on those who are doing real business at home in the US. House Speaker Paul Ryan said his chamber could pass a Republicans backed tax reform plan by Thanksgiving. And Ryan expects Senate to follow about a week later. Ryan also defended against criticisms that the tax plan would add US 1.5T to deficit. He emphasized that "Paul Ryan Deficit Hawk is also a growth advocate. Paul Ryan Deficit Hawk also knows that you have to have a faster growing economy, more jobs, bigger take home pay, that means higher tax revenues."

ECB Peter explains ECB's decision on APP

ECB chief economist Peter Praet explained ECB's decisions to half monthly asset purchase to EUR 30b and extend the program by nine months. He noted that "when considering the appropriate calibration of the asset-purchase program there were three important dimensions to consider: pace, horizon and optionally." He reiterated the view that "the brighter economic prospects have increased our confidence in the gradual convergence of inflation toward our aim. This called for a lower pace of purchases."

Also, "we have always emphasized that monetary policy needs to be persistent and patient for underlying inflation pressures to gradually build up." Therefore, "the longer horizon also anchors short-term interest-rate expectations for a longer period, thereby reinforcing the Governing Council's forward guidance on policy rates."

Eurozone Sentix confidence hit highest since 2007

Eurozone Sentix Investor Confidence rose to 34.0 in November, up from 29.7 and beat expectation of 31.0. That's also the highest reading since July 2007. Meanwhile, current situation gauge rose to 45.8, up from 41.8. Expectation gauge rose to 22.8, up from 18.3. Sentix noted that "both situation and expectations contribute to this positive development. Things are even better in Germany, where we can report all-time highs."

Also from Eurozone, PPI rose 0.6% mom in September. Services PMI was revised up to 55.0 in October. Italy services PMI dropped to 52.1 in October. German factory orders rose 1.0% mom in September.

Swiss CPI was unchanged at 0.70% mom yoy in October.

RBA widely expected to stand pat

RBA rate decision will be a main focus in the upcoming Asian session. The central bank is widely expected to keep the Cash Rate unchanged at 1.50%. That will be the 15 straight months RBA stands pat. The last time there was a move, RBA cut interest rate by -25bps back in August 2016. Governor Philip Lowe has repeatedly stated his stance that RBA won't follow some other global central banks in stimulus exit. And there are speculations that RBA could lower near term GDP forecasts as recent data disappointed. More importantly, if there would be a downgrade in inflation forecast, we could see another round of selloff in Aussie.

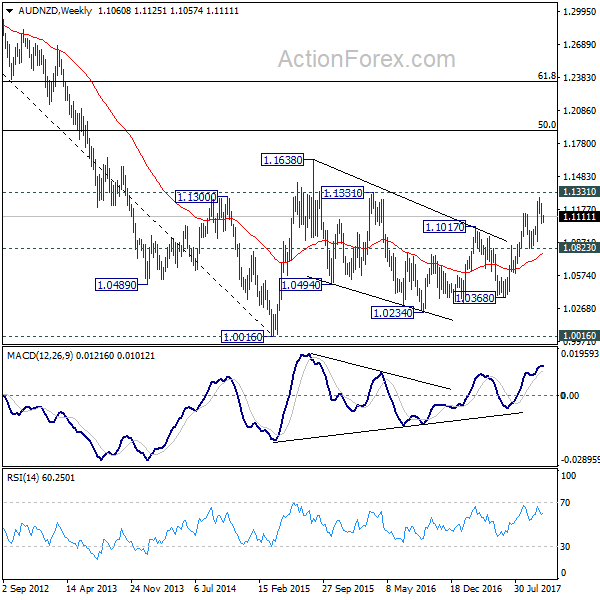

AUD/NZD was shot higher briefly after New Zealand Election, but there was no follow through buying since then. Even though the markets are unhappy with the new labor-led coalition in New Zealand, Aussie has indeed under-performed in the past two weeks. It's early to call for a trend reversal in the cross with 1.0832 support intact. But for now, 1.1331 resistance looks solid and AUD/NZD will feel heavy as it approaches this level.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1574; (P) 1.1632 (R1) 1.1666; More...

EUR/USD dips mildly today but it's staying above 1.1574 support. Intraday bias remains neutral and more consolidation could be seen. But after all, break of 1.1879 resistance is needed to confirm completion of the decline from 1.2091. Otherwise, near term outlook will stay bearish. Below 1.1574 will target 38.2% retracement of 1.0569 to 1.2091 at 1.1510.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be cautious on 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BOJ Minutes Sep Meeting | ||||

| 0:00 | AUD | TD Securities Inflation M/M Oct | 0.30% | 0.30% | ||

| 2:00 | NZD | RBNZ 2-Year Inflation Expectation Q4 | 2.00% | 2.10% | ||

| 7:00 | EUR | German Factory Orders M/M Sep | 1.00% | -1.10% | 3.60% | 4.10% |

| 8:15 | CHF | CPI M/M Oct | 0.10% | 0.10% | 0.20% | |

| 8:15 | CHF | CPI Y/Y Oct | 0.70% | 0.70% | 0.70% | |

| 8:45 | EUR | Italy Services PMI Oct | 52.1 | 53 | 53.2 | |

| 8:50 | EUR | France Services PMI Oct F | 57.3 | 57.4 | 57.4 | |

| 8:55 | EUR | Germany Services PMI Oct F | 54.7 | 55.2 | 55.2 | |

| 9:00 | EUR | Eurozone Services PMI Oct F | 55 | 54.9 | 54.9 | |

| 9:30 | EUR | Eurozone Sentix Investor Confidence Nov | 34 | 31 | 29.7 | |

| 10:00 | EUR | Eurozone PPI M/M Sep | 0.60% | 0.40% | 0.30% | |

| 15:00 | CAD | Ivey PMI Oct | 59.6 |

Canadian Dollar Flat at Start of Week

The Canadian dollar is almost unchanged in the Monday session. Currently, USD/CAD is trading at 1.2754, down 0.07% on the day. On the release front, Canada will release Ivey PMI, which is expected to improve to 60.2 points. In the US, FOMC member William Dudley will speak, and could announce his retirement from the Federal Reserve. On Tuesday, Fed Chair Janet Yellen and Bank of Canada Governor Stephen Poloz will speak at public engagements.

Canadian employment data was sharp on Friday, as the economy produced 35.3 thousand jobs, well above the estimate of 15.3 thousand. This marked the highest gain since June. South of the border, job numbers were a disappointment. After a decline in September, a result of the hurricanes which battered the US, nonfarm payrolls rebounded sharply with a reading of 261 thousand. This was a respectable number, but still fell short of the forecast of 312 thousand. Wage growth also disappointed, slowing to 0.0%, short of the estimate of 0.2%. This marked the first time in 2017 that wage growth did not increase, underlining persistent weak inflation. Although Fed Chair Yellen and other Fed policymakers have expressed confidence that inflation levels will rise, this is still yet to occur, despite strong growth and a labor market at capacity.

On Thursday, US President Trump nominated Federal Reserve Governor Jerome Powell to head the Federal Reserve. Powell will take over in February 2018 when Yellen's term expires. Powell is expected to hold the course with monetary policy, which has been marked by incremental and small rate hikes since December 2015. It's all but a given that the Fed will raise interest rates in December, but the forecast for 2018 is less clear. If the US economy continues to grow at current levels, we could see up to three rate hikes next year. Powell will also be tasked with continuing to trim the Fed's huge balance sheet of $4.2 billion. Last month, the Fed has started trimming the balance sheet by $10 billion/mth, but these cuts are expected to increase in size next year.

EURUSD Selling Likely to Increase Below 1.1610

The euro continues to decline against the U.S dollar on Monday, despite a series of stronger than expected economic data releases from the Eurozone. The EURUSD currently trades around the 1.1590 level, as U.S dollar index strength continues to force the pair lower. Earlier, the Eurozones Sentix Investors Confidence Survey rose sharply for the month of November, with the German reading hitting an all-time High. October PPI inflation figures also continued to improve in the Eurozone, with a 0.6 percent monthly gain.

The EURUSD pair remains strongly technically bearish while trading below the 1.1610 level. Intraday euro selling is likely to increase below 1.1610, with further declines towards the 1.1573 and 1.1510 levels expected.

Should price action move back above the 1.1610 technical level, euro buyers will likely push price-action back towards the key 1.1640 resistance level.

GBPUSD Still Bearish Below 1.3130

The British pound has recovered the 1.3100 handle against the U.S dollar, hitting 1.3126, as the new trading week gets underway. The British pound is attracting early buying interest, ahead of speech from UK Prime Minister Theresa May, who is scheduled to address the conference of the Confederation of British Industries later today. The GBPUSD pair currently trades around the 1.3110 level, as traders await May's speech and the next directional move in the U.S dollar index.

The GBPUSD pair remains bearish while trading beneath the 1.3130 technical level. Further declines should be expected towards the 1.3070 and 1.3048 levels.

Should price action move above the 1.3130 level for a sustained period, further upside towards 1.3160 and 1.3259 remains possible.

RBA Meets as Aussie Retreats; New Forecasts Eyed

The Reserve Bank of Australia is due to announce its latest policy decision on Tuesday amid a mixed outlook for the economy. Australia's central bank is almost certain to hold rates unchanged at 1.5% following disappointing inflation and retail sales numbers for the third quarter.

Rising household debt has been holding back consumer spending, with anaemic wage growth further restraining households' spending power. Like in most other advanced economies, a tightening labour market in Australia has done little in lifting wages, despite impressive increases in full-time jobs in recent months. Inflation meanwhile fell further below the RBA's 2-3% target band in the third quarter after briefly hitting the target during the first three months of the year.

The subdued inflation outlook has kept rate cut hopes alive, though the majority view is that the RBA will stay on hold until late 2018, when the first rate hike is expected to come. Given the improving global growth outlook and steady Chinese demand for raw materials, the RBA is unlikely to make an impulse response to any weak data releases, especially as construction activity and exports performance remain strong.

The RBA's latest quarterly outlook report - the November Statement on Monetary Policy - might prove more insightful about future policy than Tuesday's policy announcement. The report, due on Friday, will likely show broadly unchanged forecasts for growth and inflation. But the Australian dollar could be susceptible to any notable changes to the inflation picture, especially if it points to a possible delay to the timing of the first rate hike.

The aussie has turned bearish in the medium term after retreating sharply (about 6%) from its September two-year high of $0.8124, and falling below its moving averages. The downtrend stalled after finding support around the $0.7630 area. If the aussie manages to avoid a breach of this key support after next week's events, the currency might start to see a shift in sentiment to a more neutral one.

Fed’s Dudley Speech Eyed After Retirement Reports

US futures are trading relatively flat ahead of the open on Monday, struggling to gather any real momentum after having recorded all-time high closes again on Friday on the back of decent jobs data.

The jobs data wrapped up a very busy week for financial markets that included a Federal Reserve meeting, new Fed Chair announcement, tax reform and a large batch of earnings reports. With the week ahead looking much quieter, investors will be left to reflect on the events of the last week and determine what it means for markets over the coming months, with a rate hike in December still the base case scenario in most people’s view.

The third quarter earnings season has given investors plenty of reason for optimism and with the global economy as a whole looking more healthy than it has in years, there’s little reason to be pessimistic right now. Of course there is still plenty of risks bubbling away underneath the surface which is likely to leave markets vulnerable at times, but investors seem more than willing to shrug this off for now.

The highlight of the European session so far has been the services and composite PMI surveys, which were broadly mixed compared to expectations but continue to show progress being made. The recovery has been very slow compared to elsewhere but we’re finally seeing it gather momentum which is allowing the ECB to take its foot off the gas.

We did see a significant improvement in euro area investor sentiment in November, more so than was expected, with confidence rising to its highest since July 2007. Overall, the market reaction to the data has been rather muted this morning, with equity markets still trading in the red and the euro pretty much unchanged against the dollar, albeit with a small bump higher around the Sentix release.

From a US perspective, the week is looking rather quiet both in terms of economic data and earnings, with the reporting season now drawing to a close. The most notable events this week will likely be Donald Trumps Asia visit and appearances from a number of Federal Reserve officials. The first of these today will be William Dudley who is believed to be preparing to announce his retirement, if speculation is to be believed. This will create another spot on the board of Governors, enabling Trump to further put his mark on the central bank.

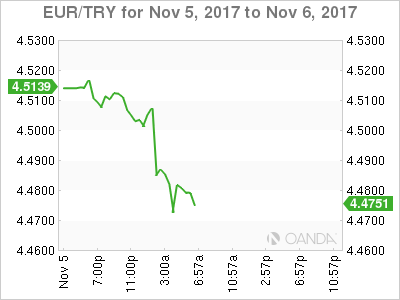

Turkey’s Central Bank Supports Lira

Monday November 6: Five things the markets are talking about

Ahead of a light week for economic data releases, investor focus has turned to Asia and the U.S. president's visit to the region.

Trump has already brought up trade grievances about both China and Japan and has warned the region nations against challenging the U.S. After Japan, Trump flies to South Korea and China later in the week.

Two more central banks are meeting this coming week – the Reserve Bank of Australia (Nov. 6 10:30 pm EDT) and Reserve Bank of New Zealand (Nov. 8 3 pm EDT). Neither is expected to change policy.

In Europe, composite PMI's will be posted in Europe, beginning with today's German September manufacturing orders and industrial production. Industrial production for France, Italy and the U.K are also expected this week.

In Asia, China begins to release its latest monthly data for merchandise trade and consumer and producer price indexes for October.

Elsewhere, Brexit talks will resume amid a lack of progress in talks over the U.K.'s exit from the E.U.

1. Equities mixed results

In Japan, the Nikkei share average ended flat overnight as weakness in financials was offset by gains in retailing. The index ended almost unchanged after printing its highest intraday level in 21-years. Last week, the Nikkei rallied +2.4%, its eighth consecutive weekly gain. That was its longest winning streak since PM Abe's Abenomics reforms started five years ago. The broader Topix edged down -0.1%.

Down-under, Australia's S&P/ASX 200 Index dipped -0.2% and South Korea's Kospi index lost -0.9%.

In Hong Kong, stocks pared sharp losses overnight, as mainland investors sought bargains in blue chip stocks. The benchmark Hang Seng index tumbled as much as -1.6%, but recouped most of its losses by market close, ending down -0.6%. The China Enterprises Index lost -0.7%.

Note: The weakness was the result of profit taking triggered by negative news flows over the weekend – including a corruption crackdown in Saudi Arabia and a call for tougher regulation in China.

In China, stocks ended higher, supported by gains in consumer and healthcare firms. The blue-chip CSI300 index rose +0.7%, while the Shanghai Composite Index closed up +0.5%.

In Europe, regional bourses trade slightly lower across the board consolidating recent gains, as the Spanish Ibex once again under performs.

U.S stocks are set to open in the black (+0.2%).

Indices: Stoxx600 flat at 395.9 FTSE -0.1% at 7549, DAX -0.2 at 13453, CAC-40 -0.2 at 5507, IBEX-35 -0.3% at 10324, FTSE MIB -0.2% at 22963, SMI +0.1% at 9291, S&P 500 Futures +0.1%

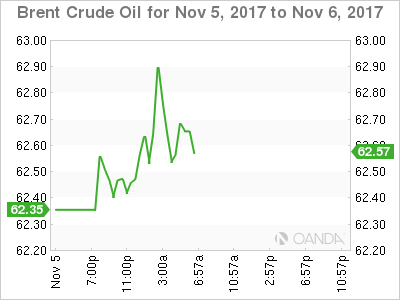

2. Oil hits highest levels in two-years, amid tightening markets, gold lower

Oil prices hit their highest levels since July 2015 overnight as markets tightened, while Saudi Arabia's crown prince tightened his power over the weekend through an anti-corruption crackdown that included high-profile arrests.

This morning, Brent futures traded as high as +$62.90 per barrel, that is over +40% higher from last June's 2017 lows. U.S West Texas Intermediate (WTI) crude has rallied above +$56 per barrel. It's one-third higher than its 2017 lows.

Saudi Crown Prince Mohammed bin Salman has tightened his grip on power through an anti-corruption purge by arresting royals, ministers and investors. In the short term, no immediate change is expected in the oil policy of Saudi Arabia, which is the world's biggest exporter of crude oil. The Prince seems strongly committed to anchoring the OPEC agreement deep into 2018.

Elsewhere, there are ongoing signs of tightening market conditions. In the U.S, energy companies cut eight oilrigs last week, to 729, in the biggest reduction since May 2016. While there seems to be growing consensus amongst OPEC members to extend their pledge to hold back about -1.8m bpd beyond next March's deadline.

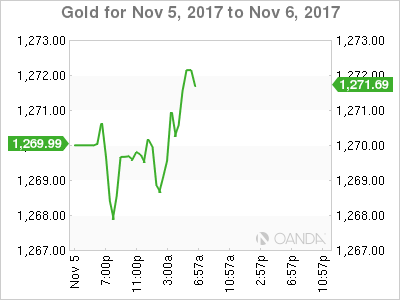

Ahead of the U.S open, gold prices trade atop of their one-week low hit in last Friday's session, as the dollar firmed after largely upbeat U.S economic data reinforced the prospects of another rate hike by the Fed in December. Spot gold is down -0.1% at +$1,268.61 per ounce.

3. Sovereign yields fall

It's rumoured that Federal Reserve Bank of New York President William Dudley is close to announcing his retirement. If so, his early departure would mean the top three positions at the Fed changing over within a relatively short period.

President Trump announced last week that Fed Governor Jerome Powell would be nominated to replace Janet Yellen when her term expires in February.

Note: Vice-Chairman Stanley Fischer retired in mid-October.

Spreads for Saudi Arabia's international bonds widened slightly in early trade in response to the government's anti-corruption crackdown, which has detained dozens of people from the kingdom's political and business elites.

The yield on U.S 10-years has fallen-1 bps to +2.32%, the lowest in more than two weeks. In Germany, the 10-year Bund yield fell -2 bps to +0.34%, the lowest in eight weeks, while in the U.K, the 10-year Gilt yield declined – 2bps to +1.245%, the lowest in more than seven weeks.

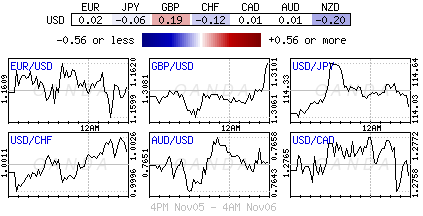

4. Tight FX ranges on rate differentials

The USD is holding onto its recent gains against the major pairs as the markets believe, that despite the softer-than-expected jobs data on Friday, there is little change in market expectations for the Fed to raise interest rates next month for a third time this year.

The EUR (€1.1607) is trading flat after having dropped to a one-week low at €1.1596, and against the pound at €0.8875. USD/JPY (¥114.02) managed to print an eight-month high just under ¥114.75 on news of Saudi Arabia anti-corruption crackdown.

Elsewhere this morning, Turkey's central bank (CBRT) took steps to support price and financial stability, after TRY's ($3.8561 -0.53%) recent slump. In a statement on its website, the CBRT, said it has tweaked its reserve option mechanism, lowering the upper limit for the FX maintenance facility to +55% from +60% – their aim is to draw liquidity from the market and support the currency.

5. German Manufacturing Orders Rose in September

German data this morning points to a resilient growth pace in their economy. Manufacturing new orders increased by +1.0% on the month in September, beating market expectations of a -1.3% decline.

Digging deeper, orders in August were also revised upward to show growth of +4.1% after an originally reported +3.6% rise. Foreign orders rose +1.7%, while domestic orders slid +0.1%. Foreign orders from within the eurozone grew by +6.3%.

Other Euro data showed that PMI services data mostly came in below expectations – miss: Italy, France, Germany and the beat were the Eurozone.

Technical Outlook: SPOT GOLD – Limited Correction Before Bears Resume

Spot Gold price bounced on Monday after downside attempts stalled ahead of last Friday's low at $1265.

Strong supports lay at $1260/$1263 zone (06 Oct low/200SMA/27 Oct n/t congestion low) which keep the downside protected for now, however, overall bearish structure keeps the downside at risk.

The notion is supported by bearish sentiment as recent strong economic data from the US maintain expectations for Fed's rate hike in December, which keeps the yellow metal price under pressure.

Recovery rally faces solid barriers from daily Tenkan-sen ($1273) and Kijun-sen ($1283) which should ideally limit upside attempts.

However, daily cloud is twisting this week and may attract for further recovery.

Extended corrective rallies are expected to stay under psychological $1300 barrier to keep bears in play, for renewed attempt at $1260 pivot, loss of which would trigger fresh bearish extension towards $1240 (50% of $1122/$1357 rally).

Res: 1273, 1280, 1283, 1289

Sup: 1265, 1263, 1260, 1251

Equities Sold Off

Market movers today

We have no global tier-1 data set for release today. The euro area is due to release Sentix confidence, where we look for a small rise from an already high level.

Some central bank speakers will be out though. Tonight, the Fed's Vice Chairman Bill Dudley (voter, neut ral) is due to speak. There has been speculation he might announce his own retirement , which would add to the turnover of FOMC officials coming up and make the future Fed policy stance more uncertain. Also, the ECB's Peter Praet is due to speak today.

Overnight Japanese wage data and the rate decision from the Reserve Bank of Austral ia are due, but it will generally be a quiet week with no market movers in the euro area or the US. China is due to publish CPI/PPI and FX reserves and Brexit negotiations resume on Thursday.

In the Scandi region today, Swedish data for industrial production and orders will be released. For the rest of the week in Scandi, focus turns to the Riksbank minutes and Norwegian inflation. See more on Scandie markets on page 2.

Selected market news

Equities sold off and Asia-Pacific currencies generally weakened vis-à-vis USD after decent US data on Friday and as US President Trump on the first stop of his Asia trip in Tokyo complained regarding the US-Japanese trade relation, calling not least for greater Japanese investment in the US. Asian stock markets were also weighed upon by the Chinese central bank issuing concerns over excessive financial leverage in the country. USD/JPY rose to March highs following comments by the Bank of Japan's Haruhiko Kuroda, stressing the need to overshoot the inflation target. Trump's 11-day trip of Asia, visiting five nations, will take him to South Korea on Tuesday-Wednesday, which is most likely going to put tense relations with North-Korea at the top of the agenda.

Friday's US data releases on th e wh ole came out on the strong side. The US job report showed some payback in October after the (at least partly) hurricane-related drop in job growth in September with non-farm payrolls rising by some 260,000. Average hourly earnings were weak at 0.0% m/m, but a key reason for this was that low-paid Americans, deterred from working due to hurricanes, returned to their jobs last month. Separately, the US ISM nonmanufacturing came in at 60.1, the highest level since 2005. The US e conomic data surprise index has notably seen a turn for the better recently and we expect this to continue into 2018, as our quantitative business -cycle framework continues to point to a US cyclical rebound over the next 3-6M. Overall, this supports the Fed's case for a rate hike in December, and market pricing for a 25bp hike at that meeting was little changed, running just above 90%.

A further drop in the US rigcount and a consolidation of the powers of the Saudi Crown Prince Mohammed bin Salman over the weekend – and hence his call for OPEC output curbs to be extended at the upcoming meeting of the cartel – sent Brent crude to levels not seen since mid-2015, now trading above USD62/bbl.