Sample Category Title

USD/JPY Daily Outlook

Daily Pivots: (S1) 113.35; (P) 114.04; (R1) 114.39; More...

USD/JPY failed to sustain above 114.49 key resistance and retreated. Intraday bias is turned neutral again. As long as 112.95 support holds, near term outlook remains bullish and further rally is in favor. Sustained trading above 114.49 will pave the way to retest 118.65 high. However, break of 112.95 support will now indicate rejection from 114.49 and turn bias to the downside for 111.64 support and below.

In the bigger picture, medium term rise from 98.97 (2016 low) is not completed yet. It should resume after corrective fall from 118.65 completes. Break of 114.49 resistance will likely resume the rise to 61.8% projection of 98.97 to 118.65 from 107.31 at 119.47 first. Firm break there will pave the way to 100% projection at 126.99. This will be the key level to decide whether long term up trend is resuming.

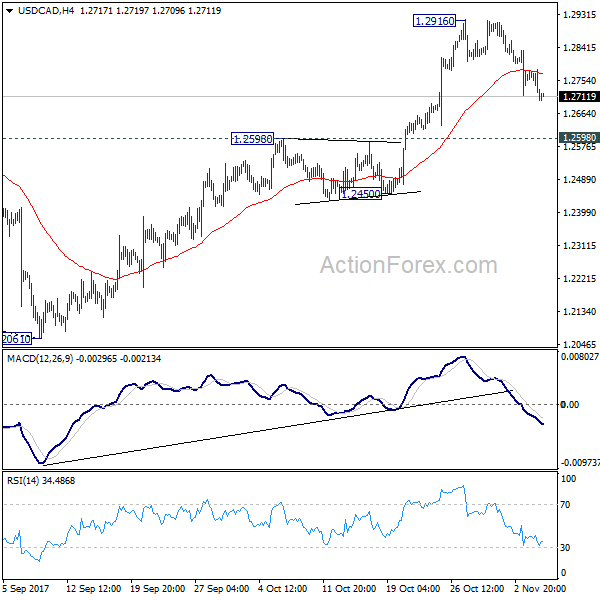

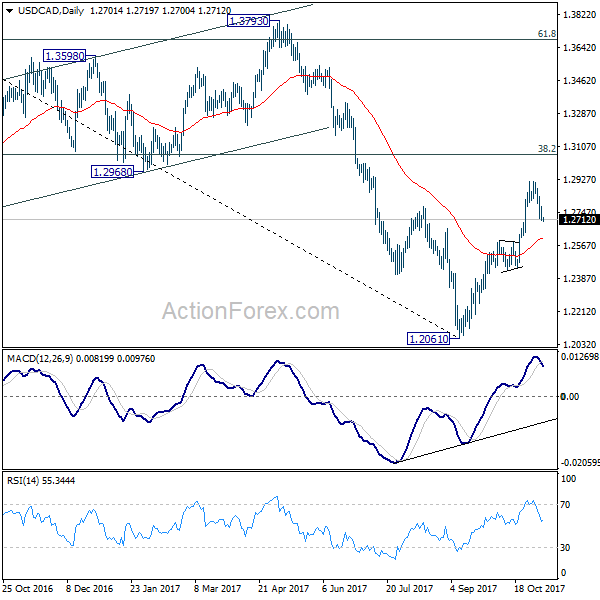

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2677; (P) 1.2729; (R1) 1.2756; More....

USD/CAD's pull back from 1.2916 extended lower but it's still kept well above 1.2598 8 resistance turned support. Near term outlook stays bullish and another rise is expected. On the upside, break of 1.2916 will extend the rise from 1.2061 to 38.2% retracement of 1.4689 to 1.2061 at 1.3065. However, sustained break of 1.2598 will argue that rebound from 1.2061 has completed after hitting 55 week EMA (now at 1.2916). Near term outlook will be turned bearish in this case.

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4689 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Rise from 1.2061 medium term bottom should now target 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Firm break there will target 1.3793 key resistance next (61.8% retracement at 1.3685). We'll now hold on to this bullish view as long as 1.2450 support holds.

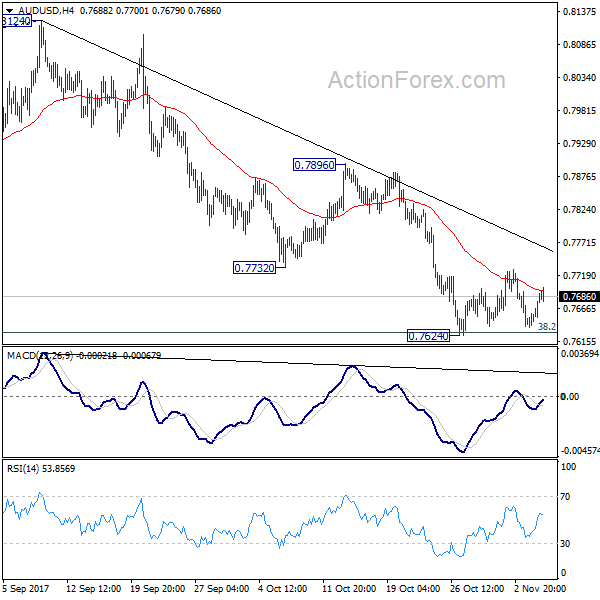

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7655; (P) 0.7673; (R1) 0.7708; More...

AUD/USD recovers ahead of 0.7624 support as consolidation continues. Intraday bias remains neutral first. Near term outlook remains bearish with 0.7896 resistance intact and deeper fall is expected. Decisive break of 0.7624 will resume whole decline from 0.8124. And, AUD/USD should target next key cluster level at 0.7322/8 next.

In the bigger picture, corrective rise from 0.6826 medium term bottom is likely completed at 0.8124, after hitting 55 month EMA (now at 0.8067). Decisive break of 0.7328 key cluster support (61.8% retracement 0.6826 to 0.8124 at 0.7322) will confirm. And in that case, long term down trend from 1.1079 (2011 high) will likely be resuming. Break of 0.6826 will target 61.8% projection of 1.1079 to 0.6826 from 0.8124 at 0.5496. This will now be the favored case as long as 0.7896 near term resistance holds.

Risk Appetite Stays in Financial Markets, Aussie Steady after RBA

The financial markets continued to trade with risk appetite this week. DOW managed to make another record high despite a mere 9.23 pts rise. S&P 500 and NASDAQ performed slightly better and gained 0.13% and 0.33% respectively, both at new records. FTSE was also firm yesterday and gained 0.03% to new record close at 7562.28. While that was below intraday record at 7598.99, that was enough to help lift Sterling for a rebound. GBP/USD is temporary safe after failing to break through 1.3026 key support following post BoE selloff. Meanwhile, Aussie trades steadily after RBA left cash rate unchanged at 1.50% as widely expected, with a carbon copy statement.

NAO warned of Brexit risks to public finances

In a report by National Audit Office, Head Amyas Morse warned that "public and private borrowing are high, kept affordable by record low interest rates, and quantitative easing continues 10 years after the crisis it responded to". The report pointed out that since 2009, UK government borrowing had increased by 61%. Interest payments have already cost the government GBP 222b. And with the use of index-linked gilts, a rise of 1% in inflation could add GBP 26b in interest between 2016-18 and 2020-21.

Morse added that "there are significant risks to the public finances and any unexpected developments, potentially including consequences of leaving the EU could exacerbate them. In these circumstances, the Treasury needs to constantly monitor these risks and be ready to react quickly and flexibly. It has taken steps to increase its capacity to respond."

More reports on Brexit assessments will be published this week. John Bercow, the Speaker of the House of Commons, has set the government a deadline of Tuesday evening to publish the Brexit assessments demanded by parliament. That came after the parliament voted unanimously last week to call on Brexit Secretary David Davis to release all the details.

Eurogroup agree to ECB approach on bad loans

Eurogroup head Jeroen Dijsselbloem said in a press conference after the meeting of Eurozone finance ministers yesterday. He noted that there was "a general agreement" on ECB's approach to tackle bad loans of banks in the region. And, it's believed that it's the right time to proceed with tougher measures to avoid the build up of so called non-performing loans by Eurozone financial institutions. EUR 1T of bad loans were accumulated after the financial crisis. And that has only be reduced to EUR 0.8T decently.

German Merkel to complete exploratory coalition talks in 10 days

In Germany, Chancellor Angela Merkel named out the clearly differences between her potential coalition partners. But she wants to end the exploratory talks to complete by November 16 and launch serious negotiations then.. Merkel noted that immigration and climate policy are the most contentious issues between the pro-business Free Democrats and the Greens.

NY Fed Dudley confirmed early retirement

The influential New York Fed President William Dudley confirmed his plan of early retirement, just four days after Jerome Powell was named as nomination to take our Janet Yellen as Fed chair by President Donald Trump. Dudley gave special thank to former Treasury Tim Geithner, former Fed chair Bernanke and Yellen for "giving me the opportunity to work closely with them during the crisis and the subsequent economic recovery."

Together with Yellen and former Vice Chair Stanley Fischer who stepped down in October, the Fed will be missing the three most important figures starting next year. The overhaul in Fed could bring fresh ideas into the most important central bank of the world. But at the same time, drastically reduce the experience level in crisis management.

On the data front

Japan labor cash earnings rose 0.9% yoy in September. UK BRC retail sales monitor dropped -1.0% yoy i9n October. German industrial production, Swiss, foreign currency reserves, Eurozone retail sales and retail PMI will be featured today.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7655; (P) 0.7673; (R1) 0.7708; More...

AUD/USD recovers ahead of 0.7624 support as consolidation continues. Intraday bias remains neutral first. Near term outlook remains bearish with 0.7896 resistance intact and deeper fall is expected. Decisive break of 0.7624 will resume whole decline from 0.8124. And, AUD/USD should target next key cluster level at 0.7322/8 next.

In the bigger picture, corrective rise from 0.6826 medium term bottom is likely completed at 0.8124, after hitting 55 month EMA (now at 0.8067). Decisive break of 0.7328 key cluster support (61.8% retracement 0.6826 to 0.8124 at 0.7322) will confirm. And in that case, long term down trend from 1.1079 (2011 high) will likely be resuming. Break of 0.6826 will target 61.8% projection of 1.1079 to 0.6826 from 0.8124 at 0.5496. This will now be the favored case as long as 0.7896 near term resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:00 | JPY | Labor Cash Earnings Y/Y Sep | 0.90% | 0.50% | 0.90% | 0.70% |

| 0:01 | GBP | BRC Retail Sales Monitor Y/Y Oct | -1.00% | 0.90% | 1.90% | |

| 3:30 | AUD | RBA Rate Decision | 1.50% | 1.50% | 1.50% | |

| 7:00 | EUR | German Industrial Production M/M Sep | -0.80% | 2.60% | ||

| 8:00 | CHF | Foreign Currency Reserves (CHF) Oct | 724B | |||

| 9:10 | EUR | Eurozone Retail PMI Oct | 52.3 | |||

| 10:00 | EUR | Eurozone Retail Sales M/M Sep | 0.60% | -0.50% |

Market Morning Briefing: Dollar-Yen Had Risen To 114.73

STOCKS

Dow (23548.42, +0.04%) is almost stable but the upside is open to test 23800 in the coming sessions. Near to medium term looks bullish.

Dax (13468.79, -0.07%) is likely to trade sideways in the 13500-13400 region for a few sessions before again resuming the uptrend. A break below 13400, if seen could take it down to 13300-13200 in the longer term.

Nikkei (22724.86, +0.78%) continues to rise higher and our earlier target of 22666 was unable to stop the upward momentum. Looking at the 3-day candles, there is scope of testing 23000-23500 levels in the coming sessions before a medium term top formation takes place. Important to see if 115 could be a decent top for the medium term on Dollar Yen. A corrective dip in Dollar Yen could prevent further rise in Nikkei.

Shanghai (3406.62, +0.54%) bounced back from 3360 as expected and could now move up towards 3425-3430 levels in the near term. Overall the short term upward channel from May’17 is likely to remain intact with an upside potential of 3450 in the medium term.

Nifty (10451.80, -0.01%) stayed above immediate support near 10400 and while that holds, the index could be sideways range-bound in the 10400-10500 region. In case it breaks below 10400, we could see a test of 10300 or slightly lower in the medium term.

COMMODITIES

Gold (1279.64) has bounced back from immediate support near 1265 as expected. Range-trade within 1260-1290 is accounted for the week with a possible extension towards 1295-1300 levels. Note that 1260 is a decent support as seen on the daily candles and is likely to hold in the coming sessions.

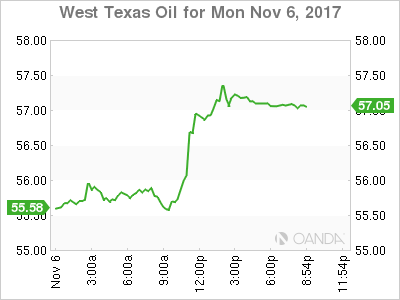

Both the Brent (64.14) and the WTI (57.25) have moved up sharply yesterday after news of high profile arrests in Saudi Arabia on an anti-corruption crackdown. Brent is trading near immediate resistance and could possibly pause before again moving up higher while WTI can test 59 before coming off from there.

Copper (3.1535) looks bullish towards 3.25-3.30 for the coming sessions and could well remain above support of 3.05 this week. Near to medium term looks bullish.

FOREX

Slight dip in the Dollar Index (94.78) which has come down from an overnight high near 95.07. The Euro (1.1608) has also recovered a bit from a low near 1.1580. However, the overall uptrend in the Dollar Index remains in force while above 94.50 and the overall downtrend remains in force on the Euro while below 1.1620 (immediate Resistance) and 1.1670 (higher Resistance). The targets are 95.50 on Dollar Index and 1.1550-30 on the Euro.

Dollar-Yen (113.78) had risen to 114.73 yesterday morning but came off sharply from there. It may try to test lower levels of 113.40 over the next couple of days while below 114.50. The Euro-Yen (132.16) has come down alongwith Dollar-Yen. Look for a relatively wide range of 131-134 over the coming days.

As it turns out, the Pound (1.3166) held above trendline Support near 1.3050 and has moved higher. A test of 1.33 looks more possible now. The Aussie (0.7686) also moved up a bit from 0.7630 but looks mixed between 0.7630-7730 for a few days.

Dollar-Yuan (USDCNY = 6.6265) trades a wee bit lower and could spend some time sideways between 6.61-65 for a few days. Dollar-Rupee (64.68) trades a little lower near 62.65 on the NDF. Support should be available in the 64.60-55 region.

INTEREST RATES

Bond Yields continue to dip across the globe even though Brent (64.10) has seen a sharp rise. This is a bit of a surprise for us.

In USA, the 30Yr (2.80%) may have an important Support near 2.78%. This is to be watched. The Yield Curve has been flattening sharply over the last few days but maybe there is some scope for a bounce from near current levels for the 30-5 (0.81%) and 30-10 (0.47%).

The German 10Yr (0.34%) has dipped further and now trades well below 0.40% suggesting that the uptrend since -0.1% (Oct-16) could be breaking.The German-US 10Yr Spread (-1.99%) has bounced from -2.05% over the last few days, but could be vulnerable to a fresh fall from current levels.

Japanese Yields (10Yr 0.03%, 5Yr -0.12%) have been falling over the last few days. The 5Yr may find Support near -0.14%.

(RBA) Statement by Philip Lowe, Governor: Monetary Policy Decision

At its meeting today, the Board decided to leave the cash rate unchanged at 1.50 per cent.

Conditions in the global economy are continuing to improve. Labour markets have tightened and further above-trend growth is expected in a number of advanced economies, although uncertainties remain. Growth in the Chinese economy is being supported by increased spending on infrastructure and property construction, with the high level of debt continuing to present a medium-term risk. Australia's terms of trade are expected to decline in the period ahead but remain at relatively high levels.

Wage growth remains low in most countries, as does core inflation. Headline inflation rates are generally lower than at the start of the year, largely reflecting the earlier decline in oil prices. In the United States, the Federal Reserve has started the process of balance sheet normalisation and expects to increase interest rates further. In a number of other major advanced economies, monetary policy has become a bit less accommodative. Equity markets have been strong, credit spreads have narrowed and volatility in financial markets remains low.

The Bank's forecasts for growth in the Australian economy are largely unchanged. The central forecast is for GDP growth to pick up and to average around 3 per cent over the next few years. Business conditions are positive and capacity utilisation has increased. The outlook for non-mining business investment has improved, with the forward-looking indicators being more positive than they have been for some time. Increased public infrastructure investment is also supporting the economy. One continuing source of uncertainty is the outlook for household consumption. Household incomes are growing slowly and debt levels are high.

The labour market has continued to strengthen. Employment has been rising in all states and has been accompanied by a rise in labour force participation. The various forward-looking indicators continue to point to solid growth in employment over the period ahead. The unemployment rate is expected to decline gradually from its current level of 5½ per cent. Wage growth remains low. This is likely to continue for a while yet, although the stronger conditions in the labour market should see some lift in wage growth over time.

Inflation remains low, with both CPI and underlying inflation running a little below 2 per cent. In underlying terms, inflation is likely to remain low for some time, reflecting the slow growth in labour costs and increased competitive pressures, especially in retailing. CPI inflation is being boosted by higher prices for tobacco and electricity. The Bank's central forecast remains for inflation to pick up gradually as the economy strengthens.

The Australian dollar has appreciated since mid year, partly reflecting a lower US dollar. The higher exchange rate is expected to contribute to continued subdued price pressures in the economy. It is also weighing on the outlook for output and employment. An appreciating exchange rate would be expected to result in a slower pick-up in economic activity and inflation than currently forecast.

Growth in housing debt has been outpacing the slow growth in household income for some time. To address the medium-term risks associated with high and rising household indebtedness, APRA has introduced a number of supervisory measures. Credit standards have been tightened in a way that has reduced the risk profile of borrowers. Housing market conditions have eased further in Sydney. In most cities, housing prices have shown little change over recent months, although they are still increasing in Melbourne. In the eastern capital cities, a considerable additional supply of apartments is scheduled to come on stream over the next couple of years. Rent increases remain low in most cities.

The low level of interest rates is continuing to support the Australian economy. Taking account of the available information, the Board judged that holding the stance of monetary policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time.

Predictably Unpredictable

Predictably Unpredictable

Being predictably unpredictable is a lot more challenging than one think but this notion has been the mainstay on FX markets this year and holding a view beyond one shift is exceptionally challenging for even the most seasoned. Whether its the plentitude of noise from headline risk or the latest reversal of fortunes from global central bankers, there's certainly no shortage of conflicting drivers in this topsy-turvy world of currency trading.

Still, we have plenty of noise to consume today whether its the tax reform cacophony, central bank musing or a possible escalation in NK geopolitical tension, the air is thick with tension and currency markets are on the move in the early trade as traders evaluate and reevaluate headline risk

With Dudley's retirement, it's out with the old and in with the new at the Fed. But overnight Dudely was at his candid best outlining his best vision for the Fed going forward. While hinting at price level targeting, I think it's safe to assume we should expect a new framework in the offing on how the Fed gauges this New Age Economy in 2018.

The Japanese Yen

Yesterday Kuroda inspired USDJPY rally was quickly snuffed out by a heavy dose of Trump protectionist rhetoric, and of course, the possible flare-up in geopolitical tension have some traders hedging their bets.

There was nothing new from Kuroda who reiterated his dovish rhetoric, but with dollar bulls looking for some apparent reason to buy dollars in the absence of domestic data this week the BoJ determined dovish tone fit the bill sending them off to the races.

But with concerns, as unlikely as they seem, that North Korea may provoke the US by launching a missile or testing a nuclear weapon during the next leg of Trumps Asia tour has put more than a few investors on edge. Even more so with an impressive US armada positioned in the western Pacific set to retaliate.

And with Trump pledging ' Era To End Of ‘Strategic Patience' Over N. Korea', things could get messy quickly. Given the escalation of geopolitical tension, the USDJPY should remain a bit soggy this week despite the BOJ's doggedly dovish efforts to weaken the JPY

The New Zealand Dollar

The New Zealand government released terms of the Reserve Act Review this morning. And the Kiwi bulls gasped a sigh of relief when the New Zealand Finance Minister stated there was no desire to have the NZD included in the RBNZ review. Predictably we've seen some hedges against this specific tail risk unwind as the minor NZD relief rally ensued. As far as other changes in the act, they appear to be more superficial and would do little more than bringing the RNBZ in line with other Central Banker Practices of having multiple decision makers, publication of minutes and the dual mandate. Overall this is positive for the NZD, but the air remains heavy with political uncertainty and traders are showing little appetite to chase the NZD higher in early trade.

The Australian Dollar

It's tough being an Aussie bear and whatever price action expected pre RBA statement from those anticipating a dovish tweak to RBA policy is just not panning out. Commodity prices are ramping higher, especially oil and iron ore and with ith the majority in the market apparently in the RBA's steady as she goes camp, despite the dismal run of economic data, price action must be respected. But with most of Australia tuning into the Melbourne Cup perhaps the RBA is in little mood to dampen local festivities anyway.Back to the drawing board for the Aussie bears

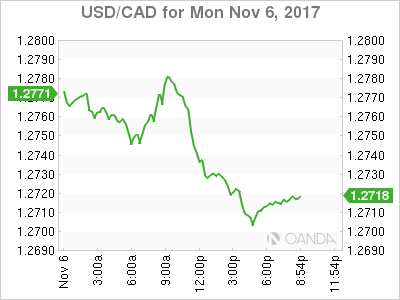

USD/CAD Canadian Dollar Higher After Dollar Struggles

The Canadian dollar appreciated 0.29 percent on Monday. Trading opened for the USD/CAD at 1.2771 and is now on track to end near the 1.2721 price level. The economic calendar looks sparse this week, but geopolitical developments around the world are driving market movements. Oil prices have surged due to the high profile arrests in Saudi Arabia that have consolidated the power of crown prince Mohammed bin Salman.

Canadian purchasing managers remain optimistic about the economy. The Ivey PMI survey beat expectations with a 63.8 reading reaching a 21 month high. The Canadian economy had a strong first half that defied expectations that prompted the Bank of Canada (BoC) to lift the benchmark interest rate twice by 25 basis points. The slowdown in the second half has been forecasted, but as the Canadian jobs number last week and today's PMI shows there are still positive signs in Canada.

The USD/CAD lost 0.29 percent on Monday. The currency pair is trading at 1.2721 after the US dollar struggled on Monday after concerns about the tax reform rose. The US dollar did not get a strong boost form the employment numbers released on Friday. The greenback fell when the U.S. non farm payrolls (NFP) report showed the US economy added 261,000 jobs, 50,000 short of the forecast. Despite the upward 18,000 revision to the September figures the biggest miss was the hourly wages remaining flat. The U.S. Federal Reserve is expected to raise interest rates in December, but lack of inflationary pressure will make further tightening more complicated.

The Canadian economy added 35,300 jobs with the gains coming in full time employment. Forecasters had predicted a 15,000 gain. Wages also rose to the biggest gain in 18 months boosting the loonie agains the dollar for a 0.38 percent gain on Friday. The improvement in economic data once again has put forth the argument for another rate hike before the end of the year. The BoC already hiked twice in 2017, but only by enough to return to 2015 levels. The Canadian benchmark rate stands at 1 percent.

Marketpulse analyst Kenny Fisher wrote about the nomination of Jerome Powell to the position of Chair of the U.S. Federal Reserve:

On Thursday, US President Trump nominated Federal Reserve Governor Jerome Powell to head the Federal Reserve. Powell will take over in February 2018 when Yellen's term expires. Powell is expected to hold the course with monetary policy, which has been marked by incremental and small rate hikes since December 2015. It's all but a given that the Fed will raise interest rates in December, but the forecast for 2018 is less clear. If the US economy continues to grow at current levels, we could see up to three rate hikes next year. Powell will also be tasked with continuing to trim the Fed's huge balance sheet of $4.2 billion. Last month, the Fed has started trimming the balance sheet by $10 billion/mth, but these cuts are expected to increase in size next year.

US President Donald Trump deliver his nomination before embarking on an Asian trip. The Trump administration is hard at work pushing the tax reform into fruition but it faces the usual obstacles that have plagued other policy initiatives as there are plenty of divisive points that could urge caution from even Republican senators ahead of next year's primaries.

The price of energy is surging on Monday. West Texas Intermediate is trading at 57.23 after rising 3 percent. The crackdown in Saudi Arabia which resulted in high profile arrests raised concerns about the stability of the kingdom. Saudi Arabia's crown prince Mohammed bin Salman has risen as the next in line to succeed his father. He has been the main driver of reform to diversify away from oil revenues and this move could end up silencing the most powerful critics of his plans.

Prince Mohammed bin Salman was the main force behind the economic boycott against Qatar in June and a showdown with Iran seems to be a question of when, not if it will happen. The Organization of the Petroleum Exporting Countries (OPEC) decision to cut production alongside Russia and other energy supplying nations has provided stability to the energy market.

Disruptions have been the main factor lifting prices above current ranges, but this last move by Saudi Arabia could unravel the OPEC as it pits major members against each other.

Weekly inventory releases will get further scrutiny, but will not have their normal effect in current rarified market conditions. The Energy Information Administration (EIA) will release oil stocks on Wednesday, November 8 at 10:30 am EDT.

Market events to watch this week:

Tuesday, November 7

1:45 pm CAD BOC Gov Poloz Speaks

Wednesday, November 8

11:30 am USD Crude Oil Inventories

4:00 pm NZD Official Cash Rate

4:00 pm NZD RBNZ Rate Statement

5:00 pm NZD RBNZ Press Conference

Thursday, November 9

9:30 am USD Unemployment Claims

8:30 pm AUD RBA Monetary Policy Statement

Friday, November 10

5:30am GBP Manufacturing Production m/m

Gold Starts Week With Strong Gains

Gold has posted considerable gains in the Monday session. In North American trade, the spot price for an ounce of gold is $1282.27, up 1.05% on the day. On the release front, there are no major events on the schedule. William Dudley, President of the New York Federal Reserve, announced his retirement. On Tuesday, Fed Chair Janet Yellen will speak at an event in Washington.

US numbers ended the week on a disappointing note, as payrolls and wage growth missed their forecasts. After a decline in September, a result of the hurricanes which battered the US, nonfarm payrolls rebounded sharply with a reading of 261 thousand. This was a respectable number, but still fell short of the forecast of 312 thousand. Wage growth also disappointed, slowing to 0.0%, short of the estimate of 0.2%. This marked the first time in 2017 that wage growth did not increase, underlining persistent weak inflation. Although Fed Chair Yellen and other Fed policymakers have expressed confidence that inflation levels will rise, this is still yet to occur, despite strong growth and a labor market at capacity.

The Federal Reserve remains in the news, after FOMC member William Dudley announced that he will retire in mid-2018. This move could have implications for monetary policy, depending on who will replace Dudley. A possible candidate is Kevin Warsh, who made the short list for the successor to Fed Chair Janet Yellen. Warsh is in favor of higher rates and favors less regulation of the banking sector, and if he would certainly support a more hawkish stance on monetary policy.

Pound Gains on Brexit Optimism; Euro Struggles Despite Robust Economic Data

During the European trading hours, the pound outperformed its peers as investors stood optimistic about Brexit developments, while the euro failed to find support on robust economic data out of the eurozone.

With Brexit negotiations expected to resume on Thursday, the pound was on track to post gains for the second consecutive trading day supported mainly by encouraging remarks made by the British Prime Minister Theresa May in front of business leaders. May backed a deal on a transitional period crucial for businesses so as not to face a cliff-edge after the country leaves the EU, saying that she wants to reach a detailed agreement on this period as "early as possible". She also mentioned that throughout this period both sides (the other side of course being the EU) should have access to one another's markets under current conditions, but she called businesses to be "realistic" about the time-frame needed to finalize the new long-term relationship with the EU. Pound/dollar gained 0.37% on the day, rising to an intra-day high of 1.3126.

In Eurozone, the IHS final composite Purchasing Manager's Index (PMI) fell from 56.7 to 56.0 in October as expected, remaining at multi-year high levels and above the threshold of 50 that separates growth from contraction in the sector. Regarding the services sector PMI, it came in solid at 56.0 as anticipated, though, among the readings for the largest European economies, Spain posted the smallest growth with the relevant index declining more than expected to a nine-month low of 54.6 from 56.7, harmed by the political uncertainties in the country.

In another report, the Sentix index which gauges investors' confidence in the eurozone jumped surprisingly to the highest level since July 2007 in November, climbing from 29.7 to 34.0, while analysts projected a smaller increase to 30.8.

Despite the mostly positive data, the euro followed a downtrend, breaking below the $1.16 key level, last trading at $1.1582 (-0.22%). Against the pound, the euro lost 0.44% on the day, falling to 0.8837 pounds.

In the US, the Senate started revising the tax code, with the House Speaker, Paul Ryan, arguing on Sunday that the outline is expected to remain similar to the current draft so that the tax bill could be agreed by both the Senate and the House of Representatives before the year-end. However, the idea that tax reforms could excessively widen the federal deficit concerns several Republicans as they recently claimed they would not support the package.

Besides that, investors have turned their focus to Trump's tour in Asia, where he will have bilateral meetings with five countries including in his agenda issues on trade and North Korea.

Next on the day, the New York Fed President, William Duddley who is expected to retire in the mid-2018, will give a speech at the Economic Club of New York.

The dollar index was moving sideways around the 95 key-level during the session. Dollar/yen was also trading flat around 114.

The aussie managed to climb higher to $0.7657 ahead of the RBA's policy meeting early on Tuesday. The kiwi reversed part of its earlier losses, though remained 0.12% down on the day at $0.6896.

Turning to commodities, oil prices stood near 2-year high levels after Saudi Arabia's Crown Prince, Mohammed bin Salman who backs OPEC supply cuts, applied anti-corruption measures, arresting royals and ministers. WTI crude moved up by 0.70% to $56 per barrel and Brent surged by 1.18% to $62.80. Gold increased by 0.28% to $1,272.70 per ounce.