Sample Category Title

Market Update – Asian Session: BOJ Gov Kuroda Affirms Easing Stance, Weakens Yen

Asia Summary

Asian equity markets opened the session mixed. The Nikkei 225 resumed trade slightly higher, following Friday's holiday.

However, Japanese tech name, Furukawa Electric, has traded lower by over 16%, following disappointing earnings.

Softbank has declined by over 2%, amid reports that T-Mobile and Sprint would end their merger talks. Following this news, Softbank also announced that it was planning to raise its stake in Sprint to less than 85%. The Japanese company owned an ~83% stake as of June 5th, according to Sprint's proxy statement.

In other tech M&A news, it was reported on Friday that Broadcom was said to consider an ~$103B cash and stock bid for Qualcomm.

Nasdaq Futures are currently lower by over -0.1%. Supplier Foxconn is said to have been asked by Apple to accelerate its production of the iPhone X amid strong sales, said a Taiwanese press report. Samsung and Hynix have declined by over 0.4%, in South Korea.

SK Telecom has declined by over 2%, as Q3 operating profits missed expectations.

South Korean consumer discretionary companies, including Lotte Shopping, are gaining amid speculation that China tourist numbers may rise in 2018. Fast Retailing has gained over 1.5%, as the company reported a 8.9% rise in its Oct domestic SSS. Cathay Pacific has declined over 3%, as Qatar Airways will acquire a 9.6% stake in the company from Kingboard Chemical.

Air China, which owns an over 29.9% stake in Cathay, has declined by over 2%. The overall Hang Seng China Enterprise index has declined by over 1% on the session amid weakness in the property sector. Real estate sales firm Sunac China has dropped over 6%.

Financials in China have also declined, as China's 10-year bond yield has declined on the session. HNA Holdings Group has declined over 3%. On Friday's session, China's NDRC (state planner) announced that it had issued draft guidelines on overseas investment by Chinese companies.

Australia's Westpac has traded lower by over 2%, as FY earnings missed market expectations. Shares of DBS in Singapore are lower by over 0.5%. The company's Q3 profit missed market expectations, amid a rise in the allowance for credit losses related to the oil/gas sector. Japanese mega banks are trading lower, as Mitsubishi UFJ and Mizuho have declined by over 0.5%. Both companies are due to report earnings on Monday, November 13th.

In the auto sector, Honda, which reported its earnings last week (Nov 1st) has gained over 1.5%. Shares of Toyota, which is due to report results on Tuesday, are higher by over 0.3%. Isuzu Motor has gained over 2% amid speculation that H1 operating profits may rise by 7%. Meanwhile, Mazda has declined by more than 3% as its quarterly earnings missed expectations. Subaru has dropped over 2%, after cutting its FY forecast.

Japan steelmakers are trading generally lower. Nippon Steel has declined by over 1.5%. Kobe Steel, which gained over 10% last week, is lower by over 2%. There has been speculation on today's session that certain executives at the steel company could seek to resign amid the recent data falsification issue.

Australian commercial blasting systems manufacturing Orica has declined by over 8% after reporting a drop in FY profits.

Energy companies in Australia are trading generally higher. Santos has gained over 2%, while shares of Woodside Petroleum are up over 1.5%. Brent Crude prices have risen on the session to trade at highs not seen since July 2015.

Over the weekend, it was reported that Saudi Arabia's Crown Prince ordered the arrest of individuals including members of the royal family, ministers and investors. On Sunday, it was also reported that a Saudi-led coalition intercepted a ballistic missile that was fired towards Saudi Arabia. The Saudi coalition has called the incident a 'direct Iran military aggression' and said it would temporarily close all Yemeni crossings.

USD/JPY has risen by over 0.4% to trade at highs not seen since March. Speaking from Japan, US President Trump, who has started his 12-day trip to Asia, said currently trade with Japan is not fair as he noted the US' trade deficit with Japan. Bank of Japan (BoJ) Gov Kuroda reiterated that the central bank will continue with its ‘powerful easing' and it is crucial that people actually experience inflation above 2%.

US Long Bond Futures are lower by over 0.1%. NY Fed President Dudley (FOMC voter) is expected to retire before his term expires in Jan 2019, according to a US financial press report.

Looking ahead, the Reserve Bank of Australia (RBA) is expected to hold its monetary policy meeting on Tuesday's session. Wednesday is the tentative release date for China's Oct Trade Balance. The Reserve Bank of New Zealand (RBNZ) is due to meet on Thursday's session, while's the RBA's Quarterly

Monetary Policy Statement and economic forecasts are due to be released on Friday.

Key economic data

(JP) Japan Oct PMI Composite: 53.4 v 51.7 prior (5-month high); Services:53.4 v 51.0 prior (26-month high)

(NZ) NEW ZEALAND Q4 2-YR INFLATION EXPECTATION: 2.0% V 3.2%E

(NZ) New Zealand Oct ANZ Commodity Price m/m: -0.3% v 0.8% prior

(JP) Bank of Japan (BOJ) Sept 20-21st Policy Meeting Minutes: momentum towards price goal is being maintained

Speakers and Press

Japan

(JP) Bank of Japan (BOJ) Gov Kuroda: Reiterates BOJ will continue with powerful easing; Price moves weak compared with improvement in the economy

Korea

(KR) South Korea, US and Australia to conduct joint naval drills near Jeju

Australia

(AU) Fitch: Australia major banks will face earnings pressure in FY18

China/Hong Kong

(CN) PBOC Gov Zhou: The market should play a "decisive role" in allocating financial resources, but also needs to be stronger regulation and Communist Party leadership in guiding financial reform - Chinese press

(CN) Moody's Report: Property developers in China face record bond maturities in 2018

Outside Asia

(JP) During President Trump's visit to the country, Japan to tell US it will strengthen sanctions against North Korea - Japanese Press

(US) NY Fed President Dudley (FOMC voter) to retire before term expires in Jan 2019; could leave as soon as the Spring of 2018 – financial press

(SA) Saudi-coalition calls weekend missile incident a 'direct Iran military aggression'; to temporarily close all Yemeni crossings

(SA) Saudi Arabia's Crown Prince ordered the arrest of individuals including members of the royal family, ministers and investors – financial press

Asian Equity Indices/Futures (23:00ET)

Nikkei -0.0%, Hang Seng -1.0%; Shanghai Composite -0.1%; ASX200 -0.1%, Kospi -0.8%

Equity Futures: S&P500 -0.2%; Nasdaq100 -0.2%, Dax -0.1%; FTSE100 -0.2%

FX ranges/Commodities/Fixed Income (23:00ET)

EUR 1.624-1.1596; JPY 114.74-113.96; AUD 0.7659-0.7638;NZD 0.6914-0.6887

Dec Gold +0.1% at $1,269/oz; Dec Crude Oil +0.2% at $55.76/brl; Dec Copper +0.8% at $3.14/lb

(AU) Australia buys back A$400M in Oct 2018, 2019 bonds

(AU) Australia sells A$400M in 2037 bonds; avg yield 3.0580%; bid-to-cover 2.54x

(CN) PBoC OMO: Skips OMO v skipped prior (3rd consecutive skip); Net drains CNY160B

USD/CNY *(CN) PBOC SETS YUAN REFERENCE RATE AT 6.6247 V 6.6072 PRIOR

(KR) Bank of Korea (BoK) sells KRW270B in 6-month monetary stabilization bonds at 1.55% v 1.59% prior

Equities notable movers

Australia/New Zealand

WBC.AU Reports FY17 (A$) Cash Earnings A$8.06B, +3% y/y; Net A$7.99B v A$7.45B y/y; Rev A$21.8B, +3.9% y/y; -2.4%

ORI.AU Reports FY17 (A$) Net profit 386.2M, -0.7% y/y; EBIT A$635M, -1% y/y; Rev 5.04B, -1% y/y; -8.1%

MEA.AU Guides FY18 EBITDA not likely to reach A$16.6M (below expectations); initial plan is to cut expenses by A$5M/year; -14%

Japan

2371.JP Reports H1 Net profit ¥7.14B v ¥6.98B y/y, Op profit ¥10.5B v ¥10.1B y/y, Rev ¥21.7B v ¥20.8B y/y; +7.6%

5801.JP Reports H1 Net ¥21.7B v ¥6.7B y/y, Op ¥21.8B v ¥13.3B y/y; Rev ¥457.5B v ¥397.6B y/y; -16.5%

US

S Announces strategic MVNO agreement with Altice USA; financial terms not disclosed

TMUS T-Mobile and Sprint End Merger Discussions

S Softbank announces its intention to raise stake through open market transactions or otherwise, subject to market conditions and other factors

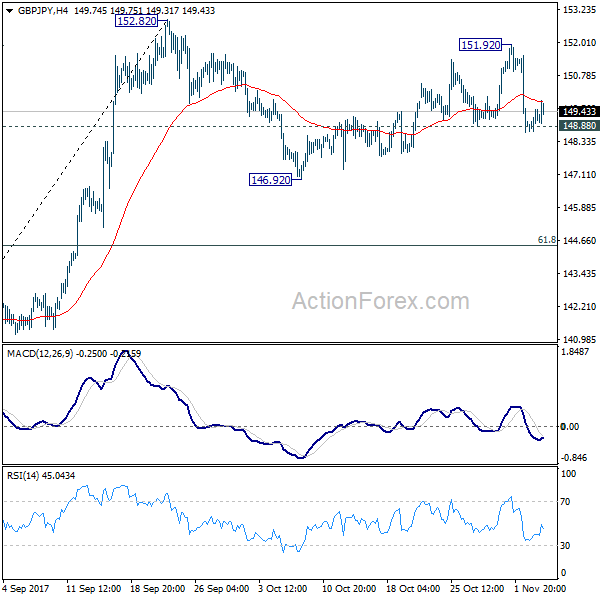

GBP/JPY Daily Outlook

Daily Pivots: (S1) 148.68; (P) 149.10; (R1) 149.52; More

Intraday bias GBP/JPY remains mildly on the downside for the moment. As noted before, corrective recovery from 146.92 has completed at 151.92. Further fall should be seen to 146.92. Break will resume the decline from 152.82. At this point, we'd expect strong support from 61.8% retracement of 139.29 to 152.82 at 144.45 to contain downside and bring rebound. On the upside, above 151.92 will retest 152.82 high instead.

In the bigger picture, medium term rebound from 122.36 is still expected to resume after corrective pull back from 152.82 completes. Firm break of 38.2% retracement of 196.85 to 122.36 at 150.43 will carry long term bullish implications. In that case, GBP/JPY could target 61.8% retracement at 167.78. However, break of 139.29 will indicate rejection from 150.43 key fibonacci level. And the three wave corrective structure of rebound from 122.36 will argue that larger down trend is resuming for a new low below 122.26.

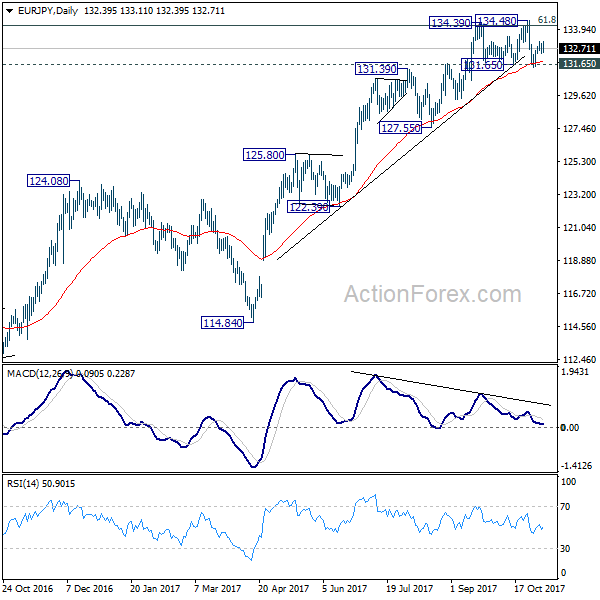

EUR/JPY Daily Outlook

Daily Pivots: (S1) 132.19; (P) 132.60; (R1) 132.80; More....

Intraday bias in EUR/JPY remains neutral for the moment. As noted before, decisive break of 134.39/48 resistance zone is needed to confirm up trend resumption. Otherwise, even in case of rebound, near term outlook is neutral at best. On the downside, decisive break of 131.65 will confirm rejection from 134.20 fibonacci level and confirm near term reversal. And, in such case, intraday bias will be turned to the downside for 127.55 key support level.

In the bigger picture, medium term rise from 109.03 (2016 low) is seen as at the same degree as the down trend from 149.76 (2014 high) to 109.03 (2016 low). 61.8% retracement of 149.76 to 109.03 at 134.20 is already met. Sustained break there will pave the way to key long term resistance zone at 141.04/149.76. However, break of 127.55 support will argue that the medium term trend has reversed and will turn outlook bearish for deeper fall back to 114.84/124.08 support zone at least.

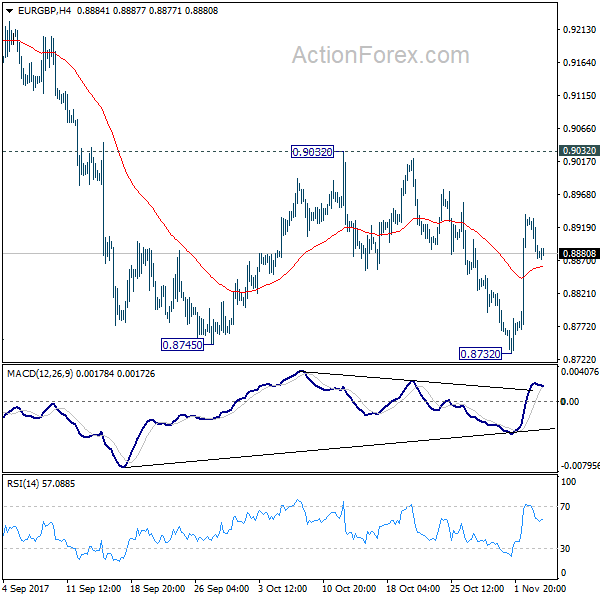

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8854; (P) 0.8894; (R1) 0.8915; More...

At this point, intraday bias in EUR/GBP remains neutral first. On the upside, decisive break of 0.9032 will confirm completion of the decline from 0.9305. In such case, intraday bias will be turned back to the upside for retesting 0.9305 key resistance. On the on the downside, break of 0.8732 will resume the fall and target 0.8303 key support level instead.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

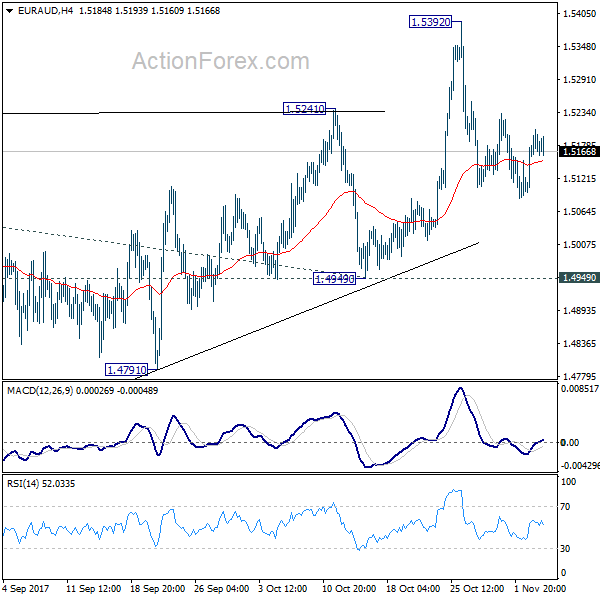

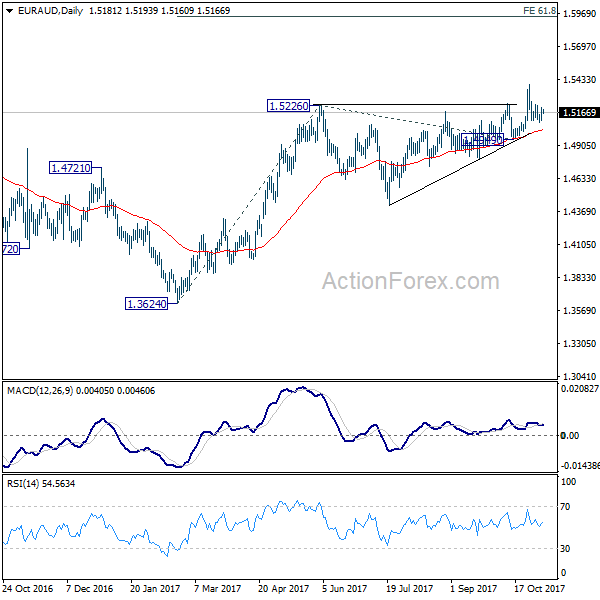

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5114; (P) 1.5159; (R1) 1.5214; More....

Intraday bias in EUR/AUD remains neutral as consolidation from 1.5392 continues. As long as 1.4949 support holds, outlook remains bullish. Medium term rally from 1.3624 is in favor to continue. On the upside, break of 1.5392 will resume medium term rise from 1.3624 and target 61.8% projection of 1.3624 to 1.5226 from 1.4949 at 1.5939 first. However, decisive break of 1.4949 will carry larger bearish implication and turn bias to the downside.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term top has completed at 1.3624. Rise from 1.3624 is expected to extend to retest 1.6587. However, break of 1.4949 support will dampen our view and argue that rise from 1.3624 has completed. In that case, EUR/AUD would turn southward for retesting 1.3624 low.

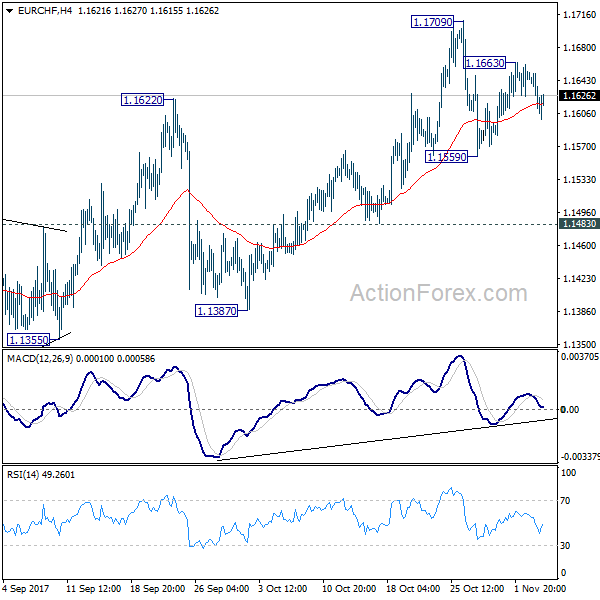

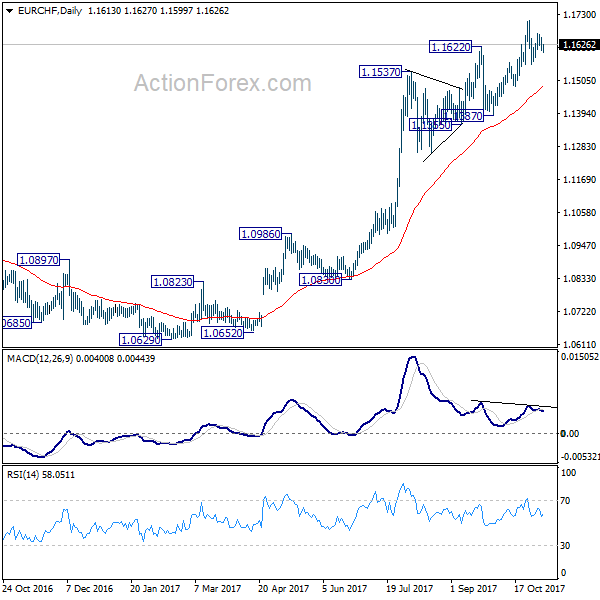

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1597; (P) 1.1624; (R1) 1.1638; More...

Intraday bias in EUR/CHF remains neutral as consolidation from 1.1709 is still in progress. Below 1.1559 minor support will bring deeper fall. But overall outlook will stays bullish as long as 1.1483 support holds. Above 1.1663 will turn bias back to the upside for 1.1709 high. Break will resume medium term rally to 1.2 key level. However, break of 1.1483 will be an early sign of reversal. In that case, deeper decline should be seen back to 1.1355 support.

In the bigger picture, long term rise from SNB spike low back in 2015 is still in progress. EUR/CHF should now be heading back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.1355 support holds. However, break of 1.1355 will indicate medium term topping. In that case, EUR/CHF should head back to 55 week EMA (now at 1.1104) and possibly below.

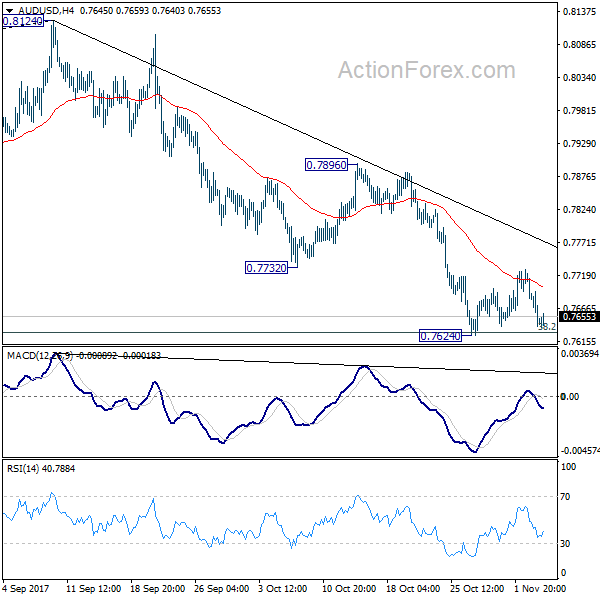

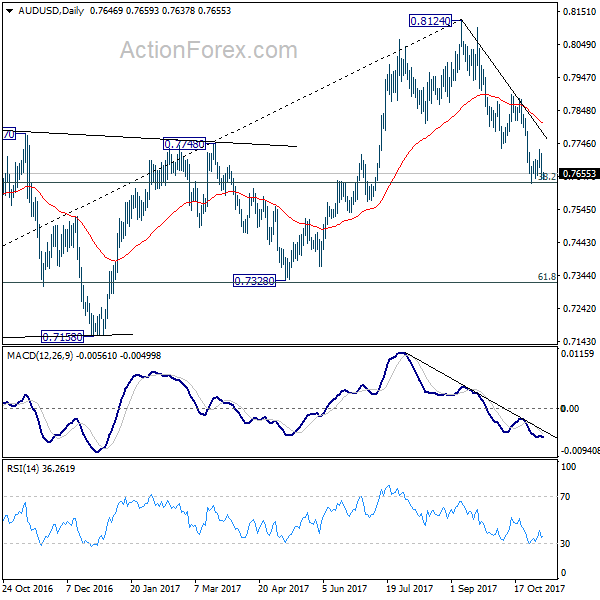

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7620; (P) 0.7667; (R1) 0.7697; More...

Intraday bias in AUD/USD remains neutral with focus on 0.7624 support. Decisive break there will resume the whole decline from 0.8124. And, AUD?USD should target next key cluster level at 0.7322/8. In case of another rise, upside of recovery should be limited well below 0.7896 resistance to bring fall resumption.

In the bigger picture, corrective rise from 0.6826 medium term bottom is likely completed at 0.8124, after hitting 55 month EMA (now at 0.8067). Decisive break of 0.7328 key cluster support (61.8% retracement 0.6826 to 0.8124 at 0.7322) will confirm. And in that case, long term down trend from 1.1079 (2011 high) will likely be resuming. Break of 0.6826 will target 61.8% projection of 1.1079 to 0.6826 from 0.8124 at 0.5496. This will now be the favored case as long as 0.7896 near term resistance holds.

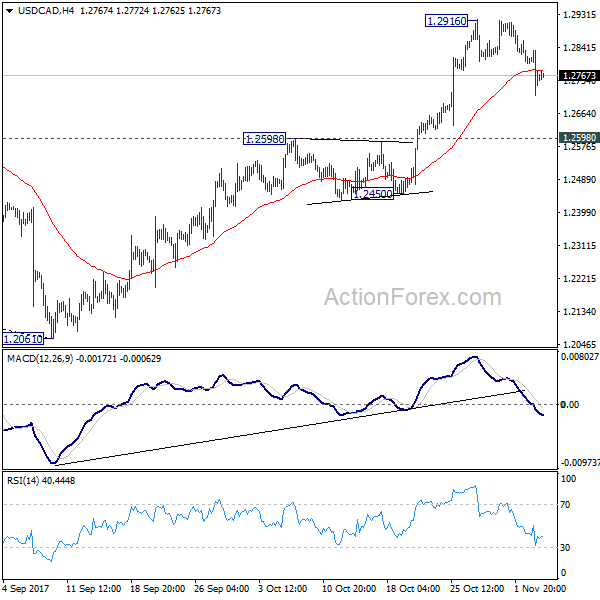

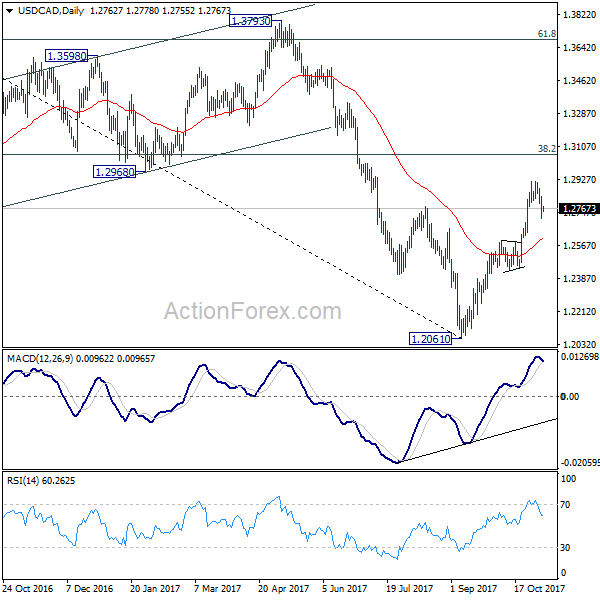

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2705; (P) 1.2770; (R1) 1.2826; More....

USD/CAD's correction from 1.2916 is still in progress and could dip lower. But after all, as long as 1.2598 resistance turned support holds, near term outlook remains bullish. On the upside, break of 1.2916 will extend the rise from 1.2061 to 38.2% retracement of 1.4689 to 1.2061 at 1.3065. However, sustained break of 1.2598 will argue that rebound from 1.2061 has completed after hitting 55 week EMA (now at 1.2916). Near term outlook will be turned bearish in this case.

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4689 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Rise from 1.2061 medium term bottom should now target 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Firm break there will target 1.3793 key resistance next (61.8% retracement at 1.3685). We'll now hold on to this bullish view as long as 1.2450 support holds.

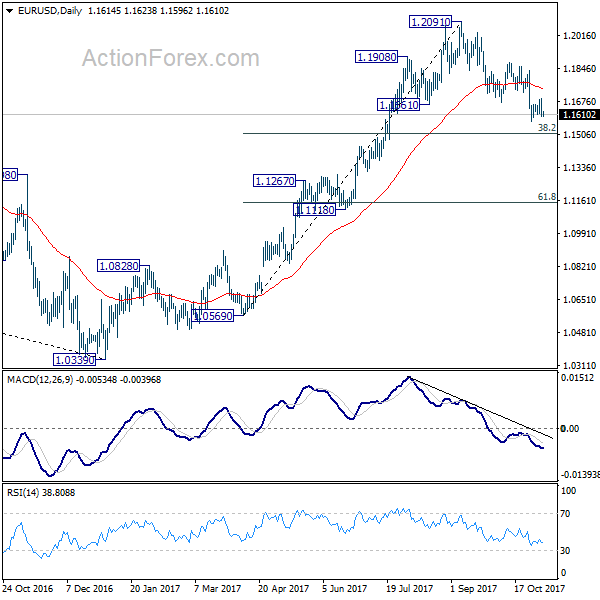

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1574; (P) 1.1632 (R1) 1.1666; More...

Intraday bias in EUR/USD remains neutral as consolidation from 1.1574 continues. Overall, break of 1.1879 resistance is needed to confirm completion of the decline from 1.2091. Otherwise, near term outlook will stay bearish. Below 1.1574 will target 38.2% retracement of 1.0569 to 1.2091 at 1.1510.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be cautious on 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

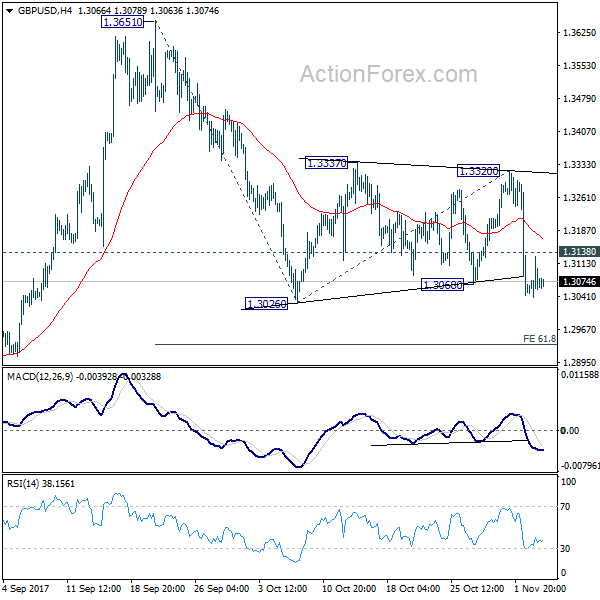

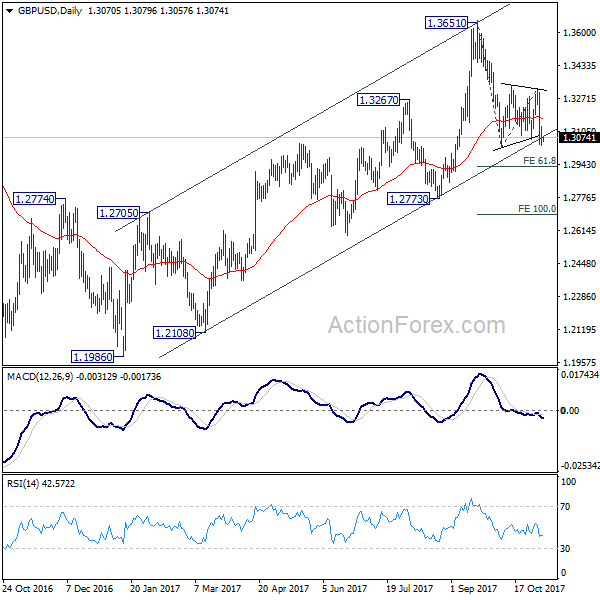

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3032; (P) 1.3079; (R1) 1.3118; More....

With 1.3138 minor resistance intact, intraday bias in GBP/USD remains mildly on the downside. Break of 1.3026 support will confirm resumption of decline from 1.3651. Next target will be 61.8% projection of 1.3651 to 1.3026 from 1.3320 at 1.2934 first. Break will bring deeper decline to 1.2773 key support level. On the upside, above 1.3138 minor resistance will extend the consolidation from 1.3026 with another rise.

In the bigger picture, as noted before, GBP/USD hit strong resistance from the long term falling trend line. Current development is starting to favor that corrective rebound from 1.1946 low has completed at 1.3651. Decisive break of 1.2773 will confirm this bearish case and target a test on 1.1946 low next, with prospect of resuming the low term down trend. Nonetheless, break of 1.3320 resistance will restore the rise from 1.1946 for 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.