Sample Category Title

EUR/AUD Weekly Outlook

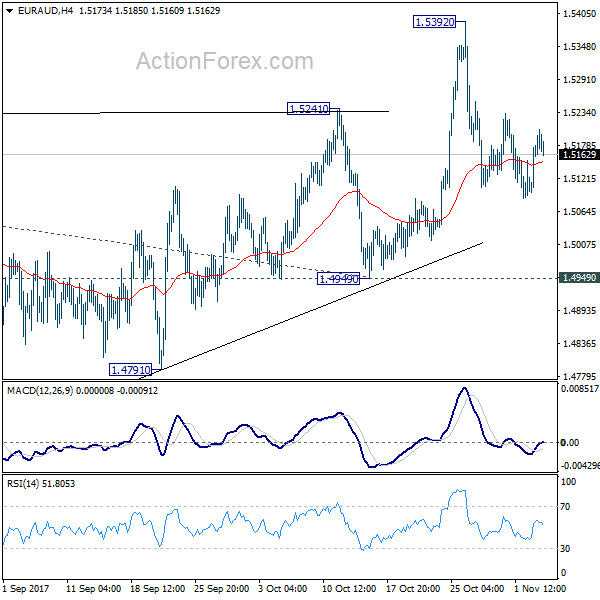

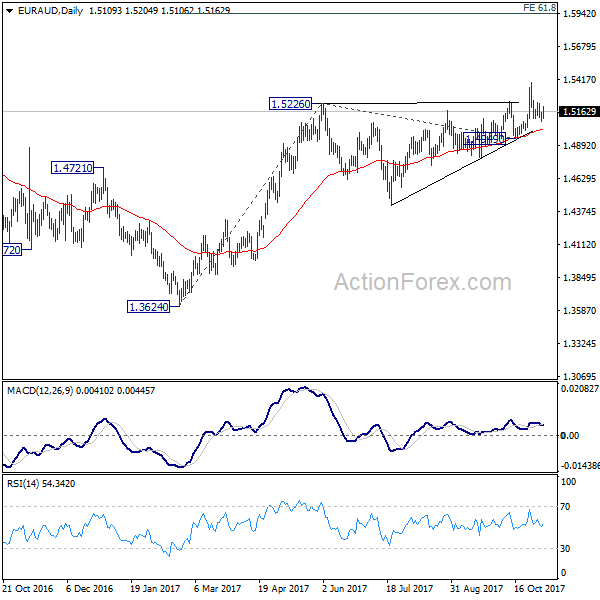

EUR/AUD stayed in consolidation below 1.5392 last week and outlook is unchanged. As long as 1.4949 support holds, outlook remains bullish and further rise is in favor. Break of 1.5392 will resume medium term rise from 1.3624 and target 61.8% projection of 1.3624 to 1.5226 from 1.4949 at 1.5939 first. However, decisive break of 1.4949 will carry larger bearish implication and turn bias to the downside.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term top has completed at 1.3624. Rise from 1.3624 is expected to extend to retest 1.6587. However, break of 1.4949 support will dampen our view and argue that rise from 1.3624 has completed. In that case, EUR/AUD would turn southward for retesting 1.3624 low.

In the longer term picture, the rise from 1.1602 long term bottom isn't over yet. We'll keep monitoring the development but there is prospect of extending the rise to 61.8% retracement of 2.1127 to 1.1602 at 1.7488 and above. However, sustained trading below 1.3671 should confirm trend reversal and target 1.1602 long term bottom again.

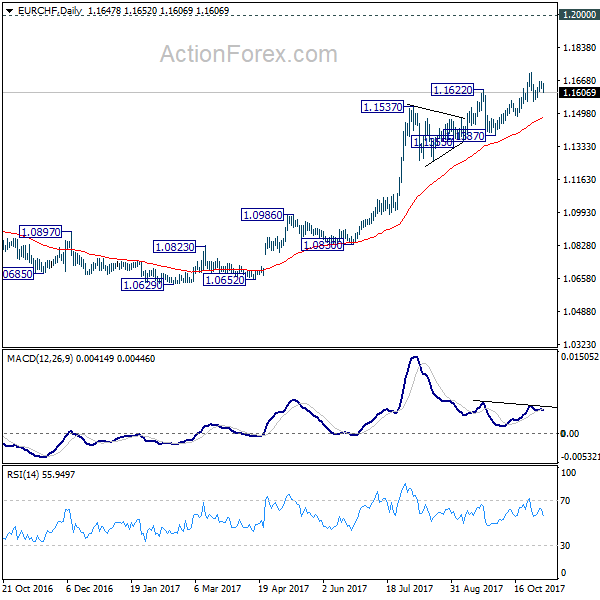

EUR/CHF Weekly Outlook

EUR/CHF stayed in consolidation below 1.1709 last week and outlook is unchanged. More corrective trading would be seen this week first. Below 1.1559 minor support will bring deeper fall. But overall outlook will stays bullish as long as 1.1483 support holds. Above 1.1663 will turn bias back to the upside for 1.1709 high. Break will resume medium term rally to 1.2 key level. However, break of 1.1483 will be an early sign of reversal. In that case, deeper decline should be seen back to 1.1355 support.

In the bigger picture, long term rise from SNB spike low back in 2015 is still in progress. EUR/CHF should now be heading back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.1355 support holds. However, break of 1.1355 will indicate medium term topping. In that case, EUR/CHF should head back to 55 week EMA (now at 1.1104) and possibly below.

Dollar Survived Key Event Risks, Set to Resume Rally Soon

It was a week full of high profile events and much volatility was seen. But in the end, most forex pairs and crosses ended inside prior week's range. Canadian Dollar closed as the second strongest, next to Kiwi, thanks to strong October job numbers. In addition, the Loonie was lifted further as WTI crude oil surged through 55.24 key resistance to resume the up trend that started back in February 2016. Sterling was the weakest one as markets responded negatively to the dovish BoE rate cut. But the pound is stubbornly holding on to key near term support against Dollar, Euro and Yen so far. Dollar ended the week mixed after all the events. FOMC delivered a forgettable statement, Jerome Powell was confirmed as President Donald Trump's nomination as next Fed chair, House released the tax bill. Nonetheless, resilience of the greenback after non-farm payroll miss could be seen as hint of underlying strength. And Dollar could be back into driving seat soon.

US yield curve flattening

One of the most discussed topic last week as the flattening yield curve. The difference between 10 year yields and 2 year yields dropped to 74.58 basis points, hitting the lowest level since November 2007. The development was highly cited because flattening yield curve has historically been a reliable factor in predicting recessions. Some attributed the flattening to Powell, who is expected to carry on the policy path laid by Fed chair Janet Yellen. That is, Fed is still going to hike interest rates in December and three times next year, despite sluggish inflation. On the other hand, some attributed that to the prospect of tax reforms. Either the tax bills would find it too difficult to pass through all legislation to be enacted by December. Or, the eventual tax cuts won't be as expansionary as economists expected.

But to us, the main reason for the pull back in 10 year yield was a decline in equivalent global yields. UK 10 year gilt yields dropped from Oct 25's 1.404 to close on Nov 3's 1.262, with downside acceleration after dovish BoE rate hike. 10 year German bund yields dropped from Oct 25's 0.482 to Friday's 0.364, with acceleration after ECB's tapering "cautious" tapering announcement. It seems that markets are expecting less aggressive global policy tightening.

UK 10 year gilt yield (source: bloomberg)

German 10 year bund yield (source: bloomberg)

TNX in consolidation, but stays bullish

This is reflected in 10 year US yield too as TNX extended Oct 25's high at 2.475 to close at 2.343 last week. Some consolidation would be seen in TNX in near term. But with 2.273 support intact, outlook remains bullish. And, we're holding on to the view that medium term correction from 2.621 is completed at 2.034. We'd expect further rally ahead through 2.475 to retest 2.621 high, in near term.

US stocks made new record highs

Also, other than yields, the markets responded quite positively last week. DOW, S&P 500 and NASDAQ closed at record highs on Friday. DOW's up trend accelerated again back in September and judging from weekly MACD and RSI, it's still having solid momentum. It now looks like the index is finally gathering some more strength to break through 100% projection of 10404.49 (2011 low) to 18351.35 (2015 high) from 15450.56 (2016 low) at 23397.43. The coming weeks will be important to see if DOW could really sustain above this level. And, if so, next medium term target will be 161.8% projection at 28308.59.

Dollar index rebound sets to resume soon

Dollar index was also firm last week. Price actions from prior week's high at 95.15 were clearly correctively. And rebound from 91.01 is still in progress. Friday's post NFP rebound suggests that the index would likely takes out 95.15 to resume the rise this week. Next target will be 38.2% retracement of 103.82 to 91.01 at 95.90. As we mentioned in previous reports, the whole medium term fall from this year's high at 103.82 has completed at 91.01 after drawing support from long term cluster at 91.91/93 (38.2% retracement of 72.69, 2011 low, to 103.82, 2016 high). As long as 93.47 support holds, we're expecting further rally to 61.8% retracement at 98.92 and above.

Trading strategy

Based on the above analysis, we'd stay bullish in Dollar and would look for buying opportunities. We already have USD/JPY long (bought at 114.50). We'll raise the stop from 112.50 to 112.80. As noted before, the medium term correction from 118.65 should have completed at 107.31. We'd expect a strong break of 114.49 key resistance to confirm this bullish view. 118.65 is the first target. We'll look at the upside momentum on rally resumption to gauge the chance of hitting 2015 high at 125.85 at a later stage.

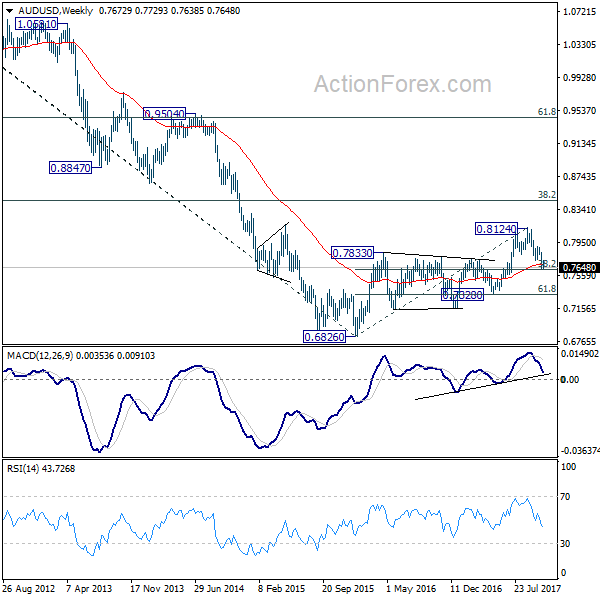

Meanwhile, we'll sell AUD/USD on break of 0.7624 this week. In our view, the medium term rise from 0.6826 should have completed with three waves up to 0.8124. Going forward, first target is 0.7328 cluster support (61.8% retracement of 0.6826 to 0.8124). But we'll also look at downside momentum to assess the chance of breaking through 0.6826 low to resume the long term down trend. Stop will be placed at 0.7735, slightly above last week's high.

GBP/USD Weekly Outlook

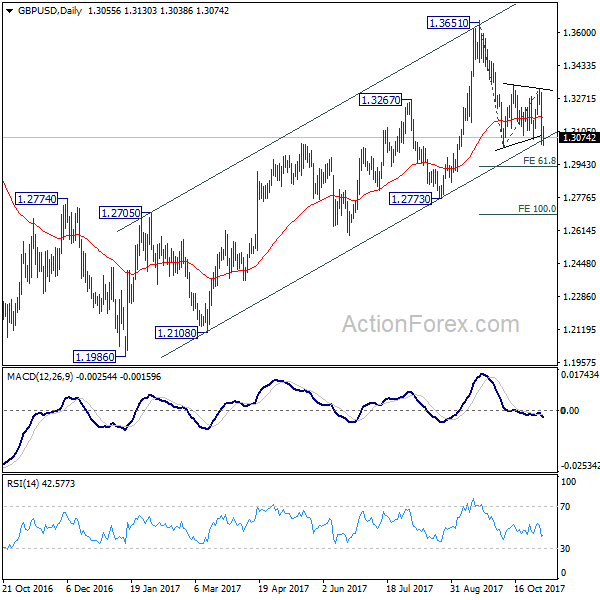

GBP/USD's sharp decline last week argues that fall from 1.3651 might be resuming. Initial bias remains on the downside this week with focus on 1.3026 support. Break will confirm this bearish case and target 61.8% projection of 1.3651 to 1.3026 from 1.3320 at 1.2934 first. Break will bring deeper decline to 1.2773 key support level. On the upside, above 1.3138 minor resistance will extend the consolidation from 1.3026 with another rise.

In the bigger picture, as noted before, GBP/USD hit strong resistance from the long term falling trend line. Current development is starting to favor that corrective rebound from 1.1946 low has completed at 1.3651. Decisive break of 1.2773 will confirm this bearish case and target a test on 1.1946 low next, with prospect of resuming the low term down trend. Nonetheless, break of 1.3320 resistance will restore the rise from 1.1946 for 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466 .

In the longer term picture, long the outlook is turned a bit mixed as GBP/USD failed to break through falling tend line resistance. We'll stay neutral first and assess the outlook again and price actions unfold.

Eco Data 11/10/17

[php_everywhere] [/php_everywhere]

Eco Data 11/9/17

[php_everywhere] [/php_everywhere]

Eco Data 11/8/17

[php_everywhere] [/php_everywhere]

Eco Data 11/7/17

[php_everywhere] [/php_everywhere]

Eco Data 11/6/17

[php_everywhere] [/php_everywhere]

Summary 11/6 – 11/10

Monday, Nov 6, 2017

[php_everywhere] [/php_everywhere]

Tuesday, Nov 7, 2017

[php_everywhere] [/php_everywhere]

Wednesday, Nov 8, 2017

[php_everywhere] [/php_everywhere]

Thursday, Nov 9, 2017

[php_everywhere] [/php_everywhere]

Friday, Nov 10, 2017

[php_everywhere] [/php_everywhere].

Weekly Economic and Financial Commentary: Economic News Broadly Positive

U.S. Review

Everything is Awesome

- The data calendar this week was packed with major economic indicators that came in largely positive. This morning's jobs report came in slightly lower than expected, but it was still solid, and the decline in September payrolls was revised away. The further drop in the unemployment rate to 4.1 percent underscored the labor market's underlying strength.

- Cycle-high consumer confidence and expectation-beating personal consumption figures, combined with still-elevated readings from the ISM surveys, underscored the broad-based U.S. economic expansion.

Economic News Broadly Positive

The FOMC still appears ready to raise rates in December despite recent inflation misses. The Committee met this week but kept policy unchanged as expected. The statement released Wednesday was notably upbeat about the economy, as the FOMC upgraded the assessment of a "moderate" pace of expansion to "solid"—quite a strong word for this committee, which signals their confidence the planned December rate hike is on course.

Consumer spending accelerated at the end of Q3, with nominal consumption rising 1.0 percent in September. Inflation trimmed off 0.4 percent, leaving real consumer spending up 0.6 percent on the month. Spending was higher for both services and goods, with durable goods posting an especially strong increase. Hurricane related purchases were likely at work in September's gain, and the absence of equally significant income growth on the month meant Americans dipped into savings to fund spending, which we delve into in the Credit Market Insight section of this report. The Fed's preferred gauge of inflation, the PCE deflator, rose 0.4 percent on temporarily high gas prices caused by Harvey, but core inflation rose only 0.1 percent. Core inflation is up 1.3 percent over the year, stubbornly lower than the Fed's target.

The employment cost index gained 0.7 percent in Q3, pushing the year-to-year growth up to 2.5 percent, which is close to the cycle high hit in 2015. The current upward trend should be more durable now that unemployment has fallen so low. Sustained strength in ECI growth would signal the Phillips curve still exists if slightly flatter, which should help inflation in the medium term.

Consumers are also remarkably confident about the economy. The Conference Board's index of consumer confidence surged in October to 125.9—the highest level since 2000. While consumer confidence is now at its highest level since December 2000, the run-up in consumer confidence looks more reminiscent of the 1997 period, when consumer confidence surged out ahead of what had been an unusually slow economic recovery and eventually became the longest and one of the strongest expansions on record. Consumers' broadly positive view on the present situation has been bolstered by continued strength in the job market and likely the upswing in the stock market. Expectations are back on the rise after losing some election-driven steam during summer months—an encouraging turnaround that we will watch closely.

The ISM manufacturing survey for October reiterated that the recovery in the factory sector is in full swing. October's gauge fell only slightly from its cycle high point in September, underscoring the sector's resilience from the recent hurricanes. New orders and employment held up well, though supplier deliveries were influenced by weather disruptions.

This morning's jobs report was an apt bookend to the week of solid economic news. The U.S. added 261,000 jobs in October and the September drop was revised away. The jobless rate fell again, now at 4.1 percent—though there was also a big drop in the labor force that was more likely reflective of seasonal adjustment quirks than large scale workforce disengagement.

U.S. Outlook

JOLTS • Tuesday

The JOLTS report for September is due to be released next Tuesday morning. The job openings rate remained at a record high 4.0 percent in August as the level of openings ticked down only slightly. Compared to a year ago, postings are up 10.8 percent. The elevated level of job openings at the end of last month underscores that the September drop in payrolls was the result of the recent hurricanes and that demand for labor is holding up.

Turnover was lower in August, with both gross hires and separations falling over the month. Separations were dragged down by fewer layoffs, but also fewer workers quitting their job. The quit rate has stayed within the band of 2.1-2.2 percent this year, on par with the highs of the previous cycle. The higher rate of workers quitting should put some modest upward pressure on wages as jobs switchers tend to see stronger earnings growth.

Previous: 6,082K

Consumer Credit • Tuesday

Next Tuesday will also see the release of the Federal Reserve's consumer credit report for September. More recently, this indicator has garnered attention as the business cycle continues to lengthen. Potential softness in consumer purchases on credit in a rising rates environment may signal a greater economic slowdown around the corner. In August, consumer credit growth undershot expectations, with notable softness in nonrevolving credit. Nonrevolving credit is up just 3.2 percent year over year, compared to revolving credit which is up 7.0 percent on a year-ago basis.

Revolving credit remains a shade below its pre-recession peak while nonrevolving credit continues to set a new record each month. We expect both series to gradually climb from here. If the Fed continues to raise rates in the 'slow and steady' manner in which they have over the past year, then a sharp uptick in consumer debt delinquencies will likely not occur, all else equal.

Previous: $13.1 billion Consensus: $18.2 billion

U. Michigan Consumer Sentiment • Friday

While the hard data are slowly catching up to the softer sentiment data, the gap still exists. This speaks more to the elevated levels of confidence data than any notable weakness in the hard data. The University of Michigan's consumer sentiment index jumped 5.6 points in October to a new cycle high of 100.7. The proportion of consumers stating the country will have continuous "good times" rose by 8 percentage points, while the proportion that expects "bad" times fell 6 points. This survey tends to focus more on financial questions and is likely being pulled higher by the roaring stock market.

Inflation expectations for the next 12 months plunged to just 2.4 percent, which may raise a red flag at the Fed. The drop likely reflects lower gasoline prices following the earlier hurricane driven spike.

Previous: 100.7 Consensus: 101.0

Global Review

Growth Strengthens in Europe, Weakens in Mexico.

- As we continue to see higher economic growth across the global economy, market expectations have shifted and are starting to believe that higher interest rates are actually possible, something that until a few years ago was almost unthinkable.

- The Bank of England increased interest rates for the first time in 10 years while the Eurozone economy grew at the fastest pace since Q1 2011, up 2.5 percent on a year-earlier basis. The Mexican economy slowed down further in Q3, up 1.6 percent on a year-earlier basis while declining 0.2 percent sequentially and not annualized.

Growth Strengthens in Europe, Weakens in Mexico.

As we continue to see higher economic growth across the global economy, market expectations have shifted and are starting to believe that higher interest rates are actually possible, something that until a few years ago was almost unthinkable.

To make the case even more interesting, on Thursday the Bank of England, which had not increased interest rates in more than ten years—it increased the rate the last time, from 5.50 percent to 5.75 percent, in July of 2007—joined the global bandwagon, increasing its target rate by 25 basis points, from 0.25 percent to 0.50 percent. Recall the Bank of England had lowered the rate from 0.50 percent to 0.25 percent in August of last year just after the Brexit referendum.

Meanwhile, earlier in the week and across the English channel, the Eurozone economy reported a better than expected advanced Q3 GDP result, up 0.6 percent, sequentially and not annualized, and 2.5 percent compared to the same quarter a year earlier. Furthermore, second quarter growth was revised up from 0.6 percent to 0.7 percent. The year-over-year growth rate was the strongest performance by the Eurozone economy since the first quarter of 2011 as the Eurozone continues to recover from the effects of the global financial crisis.

In the Americas, other than the better than expected increase in U.S. GDP in Q3, the news this week was not as positive, with Mexico reporting a decline of 0.2 percent in economic activity during the third quarter of the year, not annualized, and a growth rate of only 1.6 percent on a year-earlier basis. Although some analysts partially blamed the Mexico City earthquake for the weakness, we did not see much overall economic disruption in the aftermath of the earthquake in September. In fact, the performance of the supply sectors does not seem to have been disrupted by the natural event but by an overall weakening trend we have already written about in the past several quarters.

Furthermore, the Mexican central bank has been raising interest rates since December 2015, taking the benchmark interest rate to 7.0 percent from 3.0 percent in November 2015. Thus, there is some argument to be made that interest rates increases are also partially to blame for the weak performance of the Mexican economy. But perhaps the most important component of this weakness may have to do with uncertainty regarding the future of NAFTA and what this is doing to investment in the country, as measured by gross fixed investment, which tends to be the most volatile component of GDP year-in-year-out. Gross fixed investment declined 2.5 percent in July, year over year, and has been very weak during 2017, reflecting some of the uncertainty in the future of NAFTA and the Mexican economy. Having said this, the performance of the Mexican economy seems to be the exception that confirms the rule. And the rule lately is that global economic activity is not booming but has improved to a point that central banks across the world are taking back the massive monetary expansion of the last decade or so.

Global Outlook

Chinese International Trade • Tuesday

Growth in the value of Chinese exports and imports turned negative last year as the global economy decelerated and as commodity prices collapsed. However, Chinese international trade has perked up again this year as growth in global economic activity has firmed. Data that are slated to print next week will offer some insights into the state of Chinese trade at the beginning of Q4. The consensus forecast anticipates that the trade surplus rose significantly in October.

The slowdown that has occurred in the Chinese economy over the past few years has kept inflationary pressures in China at bay. CPI data for October will be released on Thursday, but we are not expecting a marked increase in inflation anytime soon. Money supply and credit data for October may be released at the end of next week. These data will offer some insights into the state of the monetary side of the Chinese economy at present.

Previous: $28.5 billion Consensus: $39.4 billion (trade balance)

German Industrial Production • Tuesday

As noted above, growth in global economic activity has strengthened this year, and the German economy has participated in this development. Indeed, the year-over-year growth rate in German industrial production (IP) has risen markedly this year. Some payback in September following the surge in IP in August seems likely, but the factory sector in Germany probably remains resilient overall. Data on factory orders (Monday) and international trade (Thursday) will offer more soundings on the state of the German industrial sector at present. Analysts will use these data points to sharpen their estimates of German GDP growth in the third quarter, which will print on November 14.

Data on French and Italian IP for September, which are both on the docket on Friday, will offer a more comprehensive view of the Eurozone industrial sector at the end of Q3.

Previous: 2.6% Consensus: -0.8% (Month-Over-Month)

U.K. Industrial Production • Thursday

Growth in British IP has slowed this year along with the rest of the economy. Not only has uncertainty associated with Brexit restrained capital spending, but the rise in inflation has eroded growth in real income which has depressed growth in consumer spending. Both factors have contributed to the slowdown in British IP growth. The consensus forecast looks for IP to edge higher in September following its modest increase during the previous month.

Real GDP in the United Kingdom rose at an annualized rate of 1.6 percent in Q3-2017. The National Institute of Economic and Social Research, a well-respected think tank, will release its estimate of monthly GDP growth (for October) on Friday. We look for the British economy to continue to expand in coming quarters, but acknowledge that uncertainties associated with Brexit cloud the outlook.

Previous: 0.2% Consensus: 0.3% (Month-Over-Month)

Point of View

Interest Rate Watch

Growth, Inflation and Rates

Fundamentals for growth and inflation continue to support a move by the FOMC to raise rates in December and again in the first half of 2018.

Growth Story: Solid

Signals from the ISM manufacturing, personal consumption and the capital goods orders reports support the case for growth in the current quarter and for the first half of 2018. The ISM index (top graph) showed continued strength in the manufacturing sector with solid above break-even indications in production, new orders and employment. Meanwhile, supplier delivery delays remained high indicating continued manufacturing production ahead.

Real personal consumption has risen at a 3.4 percent annual rate over the last three months. Both goods and services spending were strong. Finally, nominal nondefense capital goods orders are up 11.6 percent (annualized) over the last three months signaling stronger capex spending ahead.

Inflation: Upward Drift

As illustrated in the middle graph, the employment cost index (ECI) for both private industry and state & local government has risen steadily since mid- 2014. At 2.5 percent, the ECI is ahead of the 2.3 percent increase registered this time last year. The latest third increase was driven by a pickup in both wages & salaries and benefits.

For the private sector, the gains were widespread in professional & business services, manufacturing and transportation & warehousing. Interestingly, benefits expenses have slowed a touch as more health care benefit costs appear to be shifted onto the workers themselves.

The Result: FOMC to Raise Rates Ahead

Our outlook remains that the FOMC will raise the Fed funds rate at the December meeting and twice again next year. The bottom graph illustrates the implied path of the Fed funds rate along with the anticipated path for the PCE deflator.

What is intriguing here is that the path of the future Fed funds rate passes above the path of the PCE This creates a scenario with a positive real interest rate at the short end of the yield curve—a situation we have not seen for quite some time. This will alter the benefit/cost ratio for financing those credit-dependent sectors of the economy.

Credit Market Insights

Consumers Using Savings as ATMs

This week's personal income and spending figures showed strong spending among consumers in September that was supported not by impressive income gains, but by consumers' savings accounts. The savings rate is at a cycle low of just 3.1 percent now, down from 3.6 percent in the first two months of Q3. Driving this substantial drop in savings despite relatively weak income growth is sky high confidence.

Consumer confidence has not been as high as it is today since 2000. Confidence is abundant broadly over the overall economic situation, but with respect to personal spending and personal income's divergence, perhaps the most telling results of October's consumer confidence survey is the measure of income expectations. Survey respondents across all income distributions believe that they will be better off financially over the next five years. The optimism of personal income growth as well as rapidly accelerating home prices and record stock market highs is likely what led consumers to dipping into savings to fund spending increases in September.

While spending and consumer confidence measures may seem to point to prolonged periods of prosperity, this kind of consumer behavior is unsustainable other than on a short-term basis. The only way this level of spending can be maintained is if income growth picks up, or if consumer borrowing increases to support expenditures, as current spending levels cannot be supported by savings in the long run.

Topic of the Week

Powell Nominated to Lead Fed

Jerome Powell has been nominated to head the Federal Reserve Board as we explored in a special report, which is available upon request. The official changing of the guard will not occur until Chair Yellen's term expires on February 3, 2018. Not surprisingly, financial markets have not reacted strongly one way or the other on the heels of this announcement, as Governor Powell is largely expected to pick up where Chair Yellen leaves off. Powell's nomination does not change our outlook for monetary policy at this time. However, reviewing Powell's previous public comments is an interesting exercise to discern how his views may differ slightly from the current Fed Chair. How might we view his comments on policy and financial markets? What would we ask at confirmation hearings?

Normalization of Policy

The Economic Club of New York, (June 1, 2017) "While monetary policy can contribute to growth…, it cannot reliably affect the long-run sustainable level of the economy's growth." From an economist's point of view, this is well-said. However, how will the Senators respond to the case for monetary neutrality? Question— what is your estimate of that long-run sustainable pace? "The normalization process is projected to have several years to run…the endpoint long-run neutral rate of interest." OK, but what is your estimate of that rate— especially given that the FOMC's estimated rate has declined in recent years (Figure 1)?

"Once the process of balance sheet normalization has begun, it should continue as planned as long as there is no material deterioration in the economic outlook." Excellent, judgement matters but how will you recognize "material deterioration" given the difficulty of forecasting, especially recessions, and given the perception of lags in the impact of monetary policy?

Likely More of the Same

Against the backdrop of cycle-low unemployment and modest economic growth, the new Fed chairman should be able to continue to gradually raise interest rates from historic lows.