Sample Category Title

Canada: Job Growth Perks Up in October on Full Time Hiring

Canada recorded an eleventh straight month of job gains as 35.3k net new positions were added in October. The unemployment rate ticked up a touch to 6.3% after holding at 6.2% for two months, as more people entered the labour force.

Full-time jobs dominated gains in the month, adding 88.7k jobs. However, about 53.4k part-time jobs were shed in the month, the second consecutive month of part-time job losses. The private sector added 39k jobs in October, while there was little change in public sector employment. Self-employment was little changed in the month.

Jobs in good-producing industries led the gain, adding 33.9k positions, driven largely by construction (+18.4k), and a notable uptick in manufacturing (+7.8k). The services side of the economy remained subdued for the second consecutive month (+1.4k), as healthy gains in sectors such as other services (+21.4k) and information culture and recreation (+15.3k) were largely offset by a large decline in trade (-35.9k). Statistics Canada notes that "Other Services" includes services related to civic and professional organizations, and personal and laundry services.

Regionally, Quebec recorded strongest job gain (+18k), adding net 33k full-time jobs while part-time jobs fell back 15k. Job gains elsewhere were less robust, with net increases recorded everywhere except Ontario and British Columbia; both provinces saw employment little changed in October.

Growth in both hourly wages and hours worked accelerated in October. The headline hourly wage rate accelerated further, to 2.4% on a year-on-year basis, while hours worked rose 2.7% y/y, albeit from a weak base, with the month-on-month increase much more modest.

Key Implications

Overall, October was a strong report, with robust full-time job gains, a slight uptick in the participation rate, and acceleration in hourly wage growth and growth in hours worked. This morning's data extends the streak of job gains to 11-months.

Hourly wage growth is likely to raise some eyebrows at the Bank of Canada, holding above 2% for the second consecutive month and even accelerating a touch. With Governor Poloz emphasizing labour market developments as a key indicator of capacity pressures in last week's interest rate announcement, the persistent move back up to over 2.0% growth in wages will be viewed as confirmation that economic slack has largely diminished.

Broader measures of labour market slack have improved so far this year. For example, the unemployment rate measure including discouraged searchers, and involuntary part-timers (R8) has trended down sufficiently such that it's only a touch elevated relative to the pre-crisis trough. Moreover, there has been some progress on the share of discouraged workers who are not part of the labour force but want to work. On the other hand, youth employment participation rates remain stubbornly below pre-crisis levels, and it remains unclear if this trend can be fully attributed to students focusing on studies.

The Canadian labour market remains consistent with a view that the Canadian economy is operating at or very near to capacity. As such, we reiterate what we said last week after the Bank of Canada decision. The economy is in something of a sweet spot, as economic slack is gradually giving way to rising capacity pressures and growth evolving back towards its longer-term trend. But, inflation remains relatively subdued with some evidence that wage growth is persistently ticking upward, and housing and trade risks help skew risks toward the downside. Altogether, this removes any immediate urgency to raise interest rates from current levels, but more signs of rising capacity pressures will eventually lead to another rate hike as early as January 2018.

A Hot Canadian and U.S Jobs Market

- US Labor Oct non-farm payrolls +261k; consensus +315k

- US Oct Unemployment Rate +4.1%; Consensus +4.2%

- US Oct Average Hourly Earnings -0.04%, or -$0.01 to $26.53; Over Year +2.4%

- US Oct Private Sector Payrolls +252k and Government Payrolls +9k

- US Oct Labor-Force Participation Rate 62.7%

- US Sep Payrolls Revised to +18K; Aug Revised to +208K

U.S. employers hired at a strong pace last month, and revisions showed the labor market weathered hurricane damage better than previously estimated.

Disappointing was wages, it failed to break out, rising +2.4% from a year earlier, a slowdown from last month.

Strong revisions

Payroll growth was significantly stronger than previously estimated in recent months. Upward revisions showed +90k more jobs were added to payrolls in August and September than previously reported.

September hiring was revised to a gain of +18k from an initial estimate of down -33k. When combined with August and September's job growth, data show the economy added jobs over the last three months at a pace of +162k a month.

Despite being a strong print, it did not beat market expectations. The dollar is trying to gain some traction across the board (€1.1663, £1.3030 and ¥113.34), with the one exception CAD (C$1.2742).

Canadian Job Market on Fire

- Canada Oct net jobs +35,300 from Sep vs. forecast at +15,000

- Canada Oct full-time jobs +88,700; part-time -53,400

- Canada Oct jobless rate +6.3%; Sep +6.2%

- Canada Oct avg. hourly wages +2.4% y/y

Canada added jobs (+ 35.3k) in October at a stronger-than-expected pace amid a slowing economic backdrop, with full-time employment surging and wage gains accelerating for a second straight month.

The unemployment rate rose from a post crisis low of +6.2% to +6.3%, but that was due to more young people searching for work.

October's advance marked the 11th straight month of job gains, which is the longest streak in over a decade. All of the net new jobs added were in the private sector and of the full-time variety, which tend to offer higher pay and steady benefits compared with part-time work.

The 'loonie' has strengthened across the board +0.64% to C$1.2729 outright and +0.74% EUR/CAD to €1.4832.

U.S. Economy Bounces Back from Hurricane Disruptions

Non-farm payrolls rebounded 261k positions in October, after hurricane-related disruptions held back job growth to a meagre 18k in September (that figure was revised up from an earlier-reported 33k loss). Still, the unemployment rate ticked even lower to 4.1%.

Given the disruptions from the hurricanes, the details of the payrolls report must be taken with a grain of salt. Employment in food services and drinking places increased sharply (+89k) over the month, mostly offsetting a decline in September that reflected the impact of the hurricanes. Business services (+50k) and education and health sector (+41k) hiring continue to be solid. On the goods side, employment also accelerated to 33k new jobs, on healthy hiring in manufacturing (+24k).

On the household side, the decline in unemployment rate is less positive given it was driven by a sizeable drop in the labor force (-765k). The participation rate declined to 62.7%, and has shown little movement over the past 12 months. The employment to population ratio also fell to 60.2%, but is still 0.5%-points higher than a year ago.

Average hourly earnings were unchanged in October, taking the year-on-year pace to a modest 2.4%.

Key Implications

Given September's hurricane-related payroll disappointment, the bar was set high for October, and on the surface September fell short. However, revisions over the past two months totaled 90k jobs, should vanquish any disappointment.

Today's sold rebound combined with the strong economic momentum in the third quarter, certainly argues for a rate hike by the FOMC in December. However, we still have yet to see a notable pick-up in core inflation and now wage growth has disappointed. We expect that Yellen will still be comfortable taking rates another 25 bps higher in what will likely be her second last meeting as Chair

Canada’s Trade Deficit Unchanged in September

Canada's trade deficit was unchanged at $3.2 billion in September as both imports and exports were down 0.3%. In real terms, export and import volumes both edged down 0.2%.

The decline in exports was driven largely by motor vehicles and parts, with a strike that began mid-month contributing to a 16% drop in exports of passenger cars and light trucks. Most other industries recorded gains during the month, led by energy exports which were up 7.2% during the month.

The drop in imports was fairly widespread, however an 18.5% surge in energy product imports and a 7% increase in metal ores and non-metallic minerals provided some offset.

Canada's trade surplus with the U.S. narrowed to $2.2B in September (preciously $2.7B), as exports were down 1.2% and imports rose 0.4%. Canada's trade deficit with the rest of the world narrowed to $5.3 billion (previously $5.8B), with exports up 2.4% and imports down by 1.4%.

Key Implications

September marks the fourth consecutive month in which export volumes declined. For the quarter as a whole, they were down 3.8%. With imports falling by a slight 0.2% over the same period, net trade will weigh on overall growth in Q3 - which is now tracking under 2% - and provides a weak hand off for the fourth quarter.

Going forward, conditions should remain supportive for exports to resume growth, with a solid U.S. economy likely to keep demand for Canadian-made goods healthy and a Canadian dollar that has fallen back to around 78 US cents. However, the strike at an auto assembly plant that lasted into mid-October will limit output and thus exports during the month.

With the Bank of Canada's next move heavily data dependent, the soft export performance does not support a move higher. However, several data reports will be released between now and the Bank's next meeting in December. At this point, we don't expect the Bank to hike until early next year.

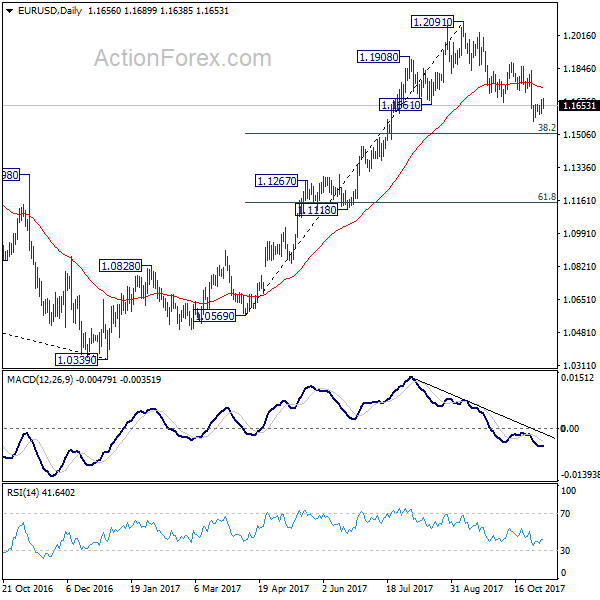

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1618; (P) 1.1652 (R1) 1.1693; More...

EUR/USD recovers further in early US session but struggles to take out 4 hour 55 EMA firmly. Intraday bias remains neutral and consolidation from 1.1574 could extend. As noted before, break of 1.1879 resistance is needed to confirm completion of the decline from 1.2091. Otherwise, near term outlook will stay bearish. Below 1.1574 will target 38.2% retracement of 1.0569 to 1.2091 at 1.1510.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be cautious on 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

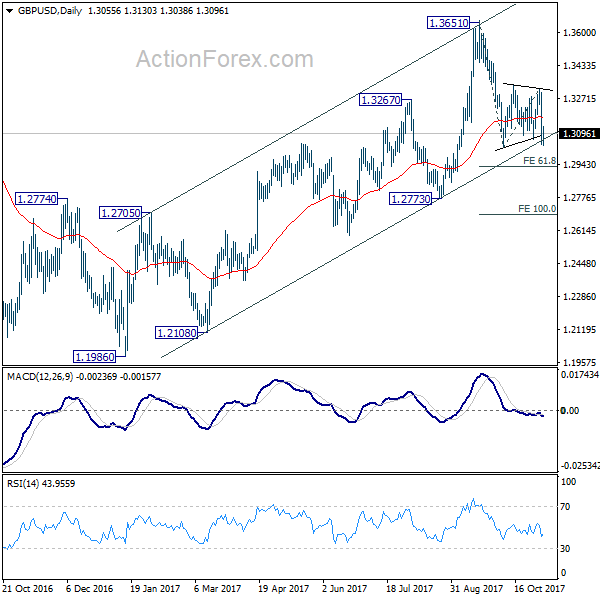

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2966; (P) 1.3133; (R1) 1.3224; More....

GBP/USD recovers today but stays below 1.3138 minor resistance. Deeper fall remains mildly in favor. Firm break of 1.3026 support will resume whole decline from 1.3651 and target 61.8% projection of 1.3651 to 1.3026 from 1.3320 at 1.2934 first. Break will bring deeper decline to 1.2773 key support level. On the upside, above 1.3138 minor resistance will extend the consolidation from 1.3026 with another rise.

In the bigger picture, as noted before, GBP/USD hit strong resistance from the long term falling trend line. Current development is starting to favor that corrective rebound from 1.1946 low has completed at 1.3651. Decisive break of 1.2773 will confirm this bearish case and target a test on 1.1946 low next, with prospect of resuming the low term down trend. Nonetheless, break of 1.3320 resistance will restore the rise from 1.1946 for 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466 .

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9950; (P) 0.9991; (R1) 1.0035; More....

USD/CHF spikes lower in early US session but stays in tight range below 1.0037 temporary top. Intraday bias remains neutral for the moment. On the upside break of 1.0037 will resume whole rally from 0.9420. And with sustained trading above 61.8% retracement of 1.0342 to 0.9420 at 0.9990, USD/CHF should then target a test on 1.0342 key resistance. In case of another fall, downside should be contained above 0.9835 resistance turned support and bring rally resumption.

In the bigger picture, current development suggests that USD/CHF has defended 0.9443 (2016 low) key support level again. Rise from 0.9420 could is a medium term up move and should target a test on 1.0342 high. This represents the upper end of a long term range that started back in 2015. On the downside, break of 0.9736 support is now needed to indicate completion of the rise from 0.9420. Otherwise, further rally will remain in favor in medium term.

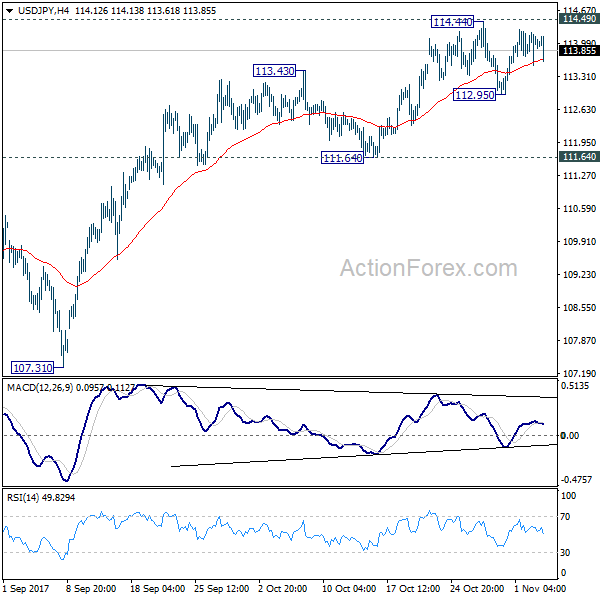

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 113.67; (P) 113.94; (R1) 114.35; More...

USD/JPY dips notably in early US session but stays in range of 112.95/114.44. Intraday bias remains neutral first. On the upside, decisive break of 114.49 will confirm that correction pattern from 118.65 has completed at 107.31 already. And USD/JPY should then target a test on 118.65. On the downside, below 112.95 will bring deeper pull back. But strong support should be seen from 111.64 support to maintain bullishness and bring rebound.

In the bigger picture, medium term rise from 98.97 (2016 low) is not completed yet. It should resume after corrective fall from 118.65 completes. Break of 114.49 resistance will likely resume the rise to 61.8% projection of 98.97 to 118.65 from 107.31 at 119.47 first. Firm break there will pave the way to 100% projection at 126.99. This will be the key level to decide whether long term up trend is resuming.

Dollar Lower after Mixed Non-Farm Payrolls, Weakness Limited

Quick update: Dollar strengthens again after ISM services beat expectation and rose to 60.1 in October.

Dollar weakens mildly in early US session after mixed employment data. Headline job growth as shown in non-farm payrolls report was at 261k in October, below expectation of 310k. But prior months figure was revised up from -33k contraction to 18k rise, roughly makes up the miss. Unemployment rate dropped to 4.1%, below expectation of being unchanged at 4.2%. The biggest disappointment is that average hourly earnings stalled at 0.0% mom, below expectation of 0.2% mom growth. While the greenback is sold off after the report, weakness is so far limited. Also from US, trade deficit widened slightly to USD -43.5b in September.

Canadian Dollar, on the other hand, jumps on strong employment data. Job market grew 35.3k in October, nearly triple of expectation of 15.5k. Unemployment rate, though, rose 0.1% to 6.3%. Trade deficit was unchanged at CAD -3.18b.

Sterling rebounds strongly today after better than expected services data. UK services PMI rose to 55.6 in October, up from 53.6 and beat expectation of 53.3. That's also the highest level since April and the biggest one month gain since August 2016. However, Markit noted that "while an upturn in business activity growth adds some justification to the Bank of England' decision to hike interest rates ... a deeper dive into the numbers highlights the fragility of the economy." Also, as across the economy as a whole, PMI showed that job growth was weakest since March. And Markit also noted that "squeezed margins and concerns about the economic outlook had led to more cautious hiring strategies."

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 113.67; (P) 113.94; (R1) 114.35; More...

USD/JPY dips notably in early US session but stays in range of 112.95/114.44. Intraday bias remains neutral first. On the upside, decisive break of 114.49 will confirm that correction pattern from 118.65 has completed at 107.31 already. And USD/JPY should then target a test on 118.65. On the downside, below 112.95 will bring deeper pull back. But strong support should be seen from 111.64 support to maintain bullishness and bring rebound.

In the bigger picture, medium term rise from 98.97 (2016 low) is not completed yet. It should resume after corrective fall from 118.65 completes. Break of 114.49 resistance will likely resume the rise to 61.8% projection of 98.97 to 118.65 from 107.31 at 119.47 first. Firm break there will pave the way to 100% projection at 126.99. This will be the key level to decide whether long term up trend is resuming.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Retail Sales M/M Sep | 0.00% | 0.40% | -0.60% | |

| 01:45 | CNY | Caixin PMI Services Oct | 51.2 | 50.8 | 50.6 | |

| 09:30 | GBP | Services PMI Oct | 55.6 | 53.3 | 53.6 | |

| 12:30 | CAD | International Merchandise Trade (CAD) Sep | -3.18B | -2.95B | -3.41B | -3.18B |

| 12:30 | CAD | Net Change in Employment Oct | 35.3K | 15.5K | 10.0K | |

| 12:30 | CAD | Unemployment Rate Oct | 6.30% | 6.20% | 6.20% | |

| 12:30 | USD | Trade Balance Sep | -43.5B | -43.5B | -42.4B | -42.8B |

| 12:30 | USD | Change in Non-farm Payrolls Oct | 261K | 310K | -33K | 18K |

| 12:30 | USD | Unemployment Rate Oct | 4.10% | 4.20% | 4.20% | |

| 12:30 | USD | Average Hourly Earnings M/M Oct | 0.00% | 0.20% | 0.50% | |

| 14:00 | USD | ISM Non-Manufacturing/Services Composite Oct | 60.1 | 58.5 | 59.8 | |

| 14:00 | USD | Factory Orders Sep | 1.40% | 1.20% | 1.20% |

USDJPY: Threatens Further Upside Pressure Medium Term

USDJPY: The pair retains its upside leaving risk of more strength on the cards. On the downside, support comes in at the 113.50 level where a break if seen will aim at the 113.00 level. A cut through here will turn focus to the 112.50 level and possibly lower towards the 112.00 level. On the upside, resistance resides at the 114.50 level. Further out, we envisage a possible move towards the 115.00 level. Further out, resistance resides at the 115.50 level with a turn above here aiming at the 116.00 level. Its daily RSI is bearish and pointing higher suggesting further upside pressure. On the whole, USDJPY faces upside threats.