Sample Category Title

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9953; (P) 0.9988; (R1) 1.0039; More....

Intraday bias in USD/CHF remains neutral for the moment. Consolidation from 1.0037 could extend. In case of another fall, downside should be contained above 0.9835 resistance turned support and bring rally resumption. On the upside break of 1.0037 will resume whole rally from 0.9420. And with sustained trading above 61.8% retracement of 1.0342 to 0.9420 at 0.9990, USD/CHF should then target a test on 1.0342 key resistance.

In the bigger picture, current development suggests that USD/CHF has defended 0.9443 (2016 low) key support level again. Rise from 0.9420 could is a medium term up move and should target a test on 1.0342 high. This represents the upper end of a long term range that started back in 2015. On the downside, break of 0.9736 support is now needed to indicate completion of the rise from 0.9420. Otherwise, further rally will remain in favor in medium term.

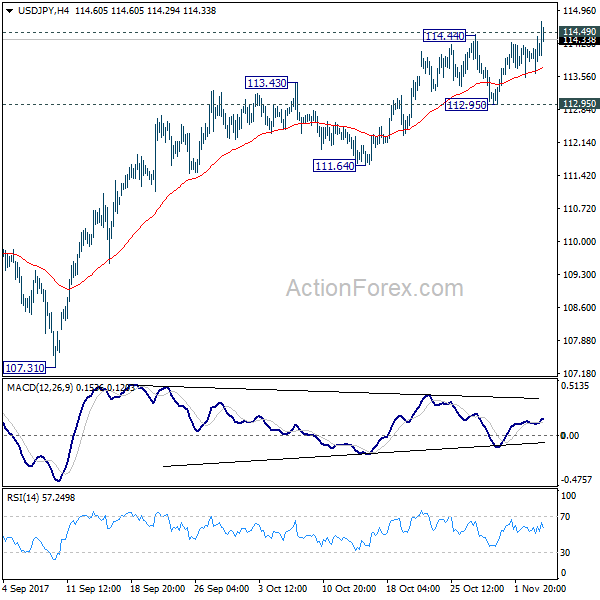

USD/JPY Daily Outlook

Daily Pivots: (S1) 113.60; (P) 114.01; (R1) 114.44; More...

USDJPY surges in initial trading and breaches 11449 key resistance. The development argues that rally from 107.31 is possibly resuming. Intraday bias is now cautious on the upside. Sustained trading above 114.49 will pave the way to retest 118.65 high. However, break of 112.95 support will now indicate rejection from 114.49 and turn bias to the downside for 111.64 support and below.

In the bigger picture, medium term rise from 98.97 (2016 low) is not completed yet. It should resume after corrective fall from 118.65 completes. Break of 114.49 resistance will likely resume the rise to 61.8% projection of 98.97 to 118.65 from 107.31 at 119.47 first. Firm break there will pave the way to 100% projection at 126.99. This will be the key level to decide whether long term up trend is resuming.

Yen Broadly Lower as a Light Week Starts; Trump Cries Trade Victim in Japan

Yen opens the weak generally lower. USD/JPY's break of 114.49 key resistance could now open up further rally to 118.65 key resistance. But more is needed to confirm underlying bullish momentum. BoJ Governor Haruhiko Kuroda sounds quite upbeat in his latest assessment in the Japanese economy. US President Donald Trump started his Asian tour by crying that the US has suffered at hands of Japan for many many years, but markets paid little attention. The forex markets are mixed elsewhere with mild strength in Euro. But the initial focus of the week will on whether Dollar can ride on Friday's strength to resume recent uptrend.

BoJ Kuroda: Economic expansion highly sustainable

BoJ Governor Haruhiko Kuroda said today that the current economic expansion in Japan is "highly sustainable" because it "doesn't rely on specific factors and is supported by various elements." Also, "the BoJ is mindful of the risk that its low-interest rate policy, if prolonged, could weigh on financial institutions' profits." These comments are seen as sign that BoJ is not in a position to expand stimulus further, even though it's still far from an exit.

Trump: US has suffered at the hands of Japan for many, many years

US President Donald Trump started his five nation Asian tour in Japan over the weekend. Trump criticized one of the closest allies of US in their their home land and said that "the United States has suffered massive trade deficits at the hands of Japan for many, many years." He went further and said that "right now our trade with Japan is not free and it's not reciprocal" and pledged that "it will be done in a quick and very friendly manner."

General HR McMaster said Trump's focuses will be on three goals, including promoting an open and free Indo-Pacific region, boosting fair trade, and strengthening international resolve to denuclearize North Korea. Trump will also visit South Korea, China, Vietnam and the Philippines during the 11 day trip.

New York Fed Dudley to announce early retirement

It's reported that outspoken New York Fed President William Dudley is going to announce retirement as soon as this week. And, the data is pulled head from January 2019 to spring 2018. That would come after Fed Governor Jerome Powell take over the Fed chair job from Janet Yellen in February. Dudley is widely regarded as a close ally of Yellen and her predecessor Ben Bernanke. Dudley's departure is seen as another sign that Fed would further depart from the path laid down by Bernanke and Yellen after the global financial crisis.

BoE Carney: Brexit could limit rate cuts to boost slow growth

BoE Governor Mark Carney said on Sunday that growth will slow if UK fails to secure a trading agreement with EU after Brexit. He noted that "in the short term, without question, if we have materially less access (to the EU's single market) than we have now, this economy is going to need to reorient and during that period of time it will weigh on growth." And there is an "extreme possibility" that if inflation gets out of control in a no-deal scenario, BoE would have no room to cut interest rate to lift growth back on track. .

UK Prime Minister Theresa May will emphasize in a speech to the Confederation of British Industry that the transition period for Brexit is crucial. In an extract of her speech released by office, she said "I know how important it is for business and industry not to face a cliff-edge and to have the time it needs to plan and prepare for the new arrangements." And therefore, "a strictly time-limited implementation period will be crucial to our future success."

RBA and RBNZ to headline a light week

On the data front, Australia TD securities inflation rose 0.3% mom in October. RBNZ 2 year inflation expectations slowed to 2.0% in Q4. Looking ahead, German will release factory orders in European session. Eurozone will release Sentix Investor Confidence, PPI and PMI revision. Swiss will release CPI. Later in the day, Canada will release Ivey PMI.

For the week ahead, RBA and RBNZ rate decisions are the main focus in a rather light week. Both are widely expected to keep interest rates unchanged. Here are some highlights:

- Tuesday: Japan labor cash earnings; UK BRC retail sales monitor; RBA rate decision; German industrial production, Eurozone retail sales and retail PMI; Swiss foreign currency reserves

- Wednesday: China trade balance; Japan leading indicator; Canada housing starts and building permits

- Thursday: RBNZ rate decision; Japan machine orders, current account; Australia home loans, China CPI and PPI; Swiss unemployment; German trade balance; Canada new housing price index; US jobless claims, whole sale inventories

- Friday: RBA monetary policy statement; Japan tertiary index; UK productions, trade balance

USD/JPY Daily Outlook

Daily Pivots: (S1) 113.60; (P) 114.01; (R1) 114.44; More...

USDJPY surges in initial trading and breaches 11449 key resistance. The development argues that rally from 107.31 is possibly resuming. Intraday bias is now cautious on the upside. Sustained trading above 114.49 will pave the way to retest 118.65 high. However, break of 112.95 support will now indicate rejection from 114.49 and turn bias to the downside for 111.64 support and below.

In the bigger picture, medium term rise from 98.97 (2016 low) is not completed yet. It should resume after corrective fall from 118.65 completes. Break of 114.49 resistance will likely resume the rise to 61.8% projection of 98.97 to 118.65 from 107.31 at 119.47 first. Firm break there will pave the way to 100% projection at 126.99. This will be the key level to decide whether long term up trend is resuming.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BOJ Minutes Sep Meeting | ||||

| 0:00 | AUD | TD Securities Inflation M/M Oct | 0.30% | 0.30% | ||

| 2:00 | NZD | RBNZ 2-Year Inflation Expectation Q4 | 2.00% | 2.10% | ||

| 7:00 | EUR | German Factory Orders M/M Sep | -1.10% | 3.60% | ||

| 8:15 | CHF | CPI M/M Oct | 0.10% | 0.20% | ||

| 8:15 | CHF | CPI Y/Y Oct | 0.70% | 0.70% | ||

| 8:45 | EUR | Italy Services PMI Oct | 53 | 53.2 | ||

| 8:50 | EUR | France Services PMI Oct F | 57.4 | 57.4 | ||

| 8:55 | EUR | Germany Services PMI Oct F | 55.2 | 55.2 | ||

| 9:00 | EUR | Eurozone Services PMI Oct F | 54.9 | 54.9 | ||

| 9:30 | EUR | Eurozone Sentix Investor Confidence Nov | 31 | 29.7 | ||

| 10:00 | EUR | Eurozone PPI M/M Sep | 0.40% | 0.30% | ||

| 15:00 | CAD | Ivey PMI Oct | 59.6 |

Market Morning Briefing: There Was A False Spike To 1.1690 On The Euro After The US NFP

STOCKS

Dow (23539.19, +0.10%) closed the previous session at slightly higher levels. Upside is open for a test of 23800. Near term looks bullish.

Dax (13478.86, +0.28%) is almost quiet at current levels and has been stable since Friday. The index could try to attempt a rise towards 13600-13700 in the near term. Although there little scope for upside just now, a rejection is around the corner, may be by the later half of this month.

Nikkei (22540.17, +0.00%) is trading near our target levels of 22666. We need to see if this holds for the medium term or the index manages to rise past 22666 in the medium term to head towards 23000 and higher.

Shanghai (3360.15, -0.34%) has fallen sharply to test support near 3360. A bounce back from current levels would take it towards 3400 and higher again; else if the falling momentum continues, we could see a test of 3340 or lower in the coming sessions.

Nifty (10452.50, +0.28%) is likely to dip towards 10400 over today and tomorrow. It would be important to see if the index comes off below 10400 or manages to rise past the high made last week. A pause and some corrective dip is preferred for some time.

COMMODITIES

Gold (1269.00) is trading above support near 1260 and while that holds, we could see some consolidation in the 1260-1290 region. Unless there is some directional clarity on the US Dollar Index, Gold is likely to remain range bound for the medium term. A break below 1260 could open up lower target of 1240.

Brent (62.25) has surprised by moving above 62 on the first attempt and while 62 holds, Brent could well test 63-65 levels in the coming sessions. Near to medium term looks bullish. WTI (55.75) has also risen sharply on Friday and is trading higher today. While the price has resistance on the 3-day candles, it is likely to break on the upside moving higher towards 57-58 levels soon. Near term view is bullish.

Copper (3.1335) is overall bullish for the medium to long term. 3.05 is the immediate support and while that holds, the price may move up towards 3.25-3.30 levels.

FOREX

There was a false spike to 1.1690 on the Euro (1.1614) after the US NFP release on Friday, but the currency fell again later on. This increases its bearishness, suggesting some more dip towards 1.1550-30 this week. Note that Dollar Index (94.895) has seen a high of 95.10 so far, in line with our target of 95.50.

Dollar-Yen (114.36) rose past the 114.50 Resistance to 114.73 today, but has come off a bit from there. As we said on Friday, "A break of Resistance, if seen, could propel the market much higher, but we would not like to pre-empt such a move." Even so, a fresh rise past 114.50-75 can test 114.90-115.00. That said, we are ambivalent about a rise past those levels.

Contrary to expectation of a dip towards 130, the Euro-Yen (132.82) now appears ranged near current levels as both the Euro and Yen seem to be gaining/ losing to the same degree against the Dollar.

No movement in the Pound (1.3075) which trades exactly where it was on Friday. So we repeat, "This is in line with our suggested view of range trade between 1.31-33. However, be careful now as a further decline from here could herald 1.2750 in the medium/ long term. Watch today."

Overall Dollar strength has prevented the Aussie (0.7651) from rising past 0.7715-30. Maybe we have to consider chances of a slow, grinding dip towards 0.7530 while below the important Resistance at 0.7750. Interim Support seen at 0.7600 as well.

Dollar-Yuan (USDCNY = 6.6365) has moved up again after dipping to 6.5829 last week. Dollar-Rupee (64.55) may also rise towards 64.70 this week.

INTEREST RATES

Yields have softened across the globe as the US NFP came in a little softer than expected on Friday. The US 10Yr (2.34%) is down from 2.35%, German 10Yr (0.36%) is down from 0.38% and Japan 10Yr (0.04%) down sharply from 0.05%.

However, as stated on Friday, there should be Support near 2.25% on the US 10Yr. We would keep an eye on Brent Crude (62.19) which could possibly rise towards 63-65. A rise in Brent has potential to pull US yields higher.

Indian GOI (6.8576%) has come off a bit from the high of 6.8930% seen last week. This could help in weakening the Rupee a bit.

EUR/JPY Levels, Like Library Staircases

On the daily chart below, you can see that after breaking down through the trend line, price hasn't been able to make a lower low and has in fact stalled at the previous resistance turned support level that we have been speaking about:

EUR/JPY Daily:

With trend lines being relatively subjective, when these horizontal levels form, they are perfect to manage risk around. Added significance can also be given to the level if it's on a higher time frame, such as the daily chart that we've highlighted it on above.

RBNZ Faces Uncertainty Over New Labour Government’s Direction

Key Points:

- NZ Inflationary pressures rising in the short term.

- Wage inflation likely to rise as immigration set to be reduced.

- NZD continues to depreciate impacting import prices.

The past week has zipped past with the newly installed Labour Government readying their swords to slash away at the prior incumbents work. Understandably, there is plenty of concern that the Labour led social programs will erode some of the economic gains made by National over the past decade. However, the Government's announced policies are surprisingly likely to have a larger impact over monetary policy, at least in the foreseeable future.

Subsequently, the RBNZ has entered a period of uncertainty over the potential changes, both to their enacting legislation and the present economic cycle. In particular, currency depreciation and inflationary pressures are all looming and this could have quite an impact over nominal interest rates in the medium term.

NZD Depreciation

You would be forgiven for missing the RBNZ's latest announcement of their Trade Weighted Index (TWI) for 2018 which demonstrates a significant depreciation for the NZD. In fact, the Kiwi Dollar is presently off by around 5% and this change is yet to flow through to general import prices. Subsequently, the question remains as to when importers will raise their domestic prices to counter the cost of the falling NZD given the normal lag time of 6-9 months.

Fuel Price Inflation

Anyone doing lots of driving within New Zealand is already aware of something that most economists are not. Fuel prices are already on the rise in response to the NZD's concerted depreciation. In addition, there could be further upward pressure on the way as oil prices continue to rise and OPEC discusses extending the production caps into next year.

Subsequently, there is likely to further rises in the near term whilst a Labour Government seeks to introduce regional fuel tax in Auckland to support infrastructure projects. So there are plenty of reasons to see a rise in inflation coming given that the vast majority of our consumption relies upon transport modes that utilise crude oil products.

Wage Inflation

It's been almost a decade since most of the Western world has seen strong levels of wage growth and there is plenty of debate in economic circles as to why this is. However, there is some consensus that the large economies are likely to see a cycle of inflation in the coming calendar year as central banks, such as the Fed and the BOE, look to normalise rates and trim their balance sheets. The reality is that New Zealand has record levels of employment not seen for the better part of a decade. Subsequently, it's interesting that as we approach the natural rate of unemployment that the Government of the day would seek to restrict immigration, especially at the lower tiers of experience.

The reality is that New Zealand requires those workers to remain buoyant in an era where sustained GDP growth is difficult to come by. The likely axing of various immigration programs is likely to only bring about skills shortages and wage inflation as employers desperately search for qualified employees. Further adding to wage gains is the plan to lift the minimum wage to $20.00 an hour which creates symmetrical issues for those above that level.

Ultimately, there are multiple factors to suggest that we are about to embark upon a cycle of inflation in New Zealand over the next 18-24 months and this brings with it plenty of scope for increases to the Official Cash Rate (OCR). In fact, this is likely to hit right when Labour wants it the least, during their campaign to increase housing and give home owners a leg up into the market.

Subsequently, it's going to be interesting to see which way the RBNZ moves over the next six months with the political pressure likely to be hanging over their heads with Winston Peter's threat of changes to the RBNZ Act. The likely course will be one of wait and see…but when inflation starts to appear the bank will have no choice but to act decisively and damn the political fallout.

Daily Technical Analysis: EURUSD, GBPUSD, USDJPY, USDCHF

EURUSD

The EURUSD attempted to push higher last week slipped above 1.1670 resistance but closed lower at 1.1608. The bias is bearish in nearest term testing 1.1500 – 1.1450 region as a part of the “head and shoulders” bearish reversal scenario as you can see on my daily chart below. Immediate resistance is seen around 1.1670. A clear break above that area could lead price to neutral zone in nearest term but as long as stay below 1.1900 I remain bearish and any upside pullback should be seen as a good opportunity to sell.

GBPUSD

The GBPUSD attempted to push higher last week topped at 1.3320 but whipsawed to the downside and closed lower at 1.3074. The bias is bearish in nearest term testing 1.3000 key support which remains a good place to buy with a tight stop loss as a clear break below that area would stop the major bullish trend and could be an early signal of a bearish reversal scenario. Immediate resistance is seen around 1.3130. A clear break above that area could lead price to neutral zone in nearest term testing 1.3200 region but key resistance remains at 1.3330 area.

USDJPY

The USDJPY was indecisive last week. Price attempted to push lower bottomed at 112.96 but closed higher at 114.08. The bias is neutral in nearest term probably with a little bullish bias testing 114.50 key resistance which remains a good place to sell with a tight stop loss as a clear break above that area would expose 115.50 or higher. Immediate support is seen around 113.75/50. A clear break below that area could trigger further bearish pressure testing 113.20/00 region. Overall I remain neutral.

USDCHF

The USDCHF was indecisive last week. Price trapped between 1.0037 – 0.9940 range area as you can see on my daily chart below suggests a consolidation phase. The bias is neutral in nearest term. Overall I remain bullish but need a clear break above 1.0037 to resume the bullish trend testing 1.0100 or higher. On the downside, a clear break and daily close below 0.9940 would expose 0.9835 support area.

Danger From Downunder

Tax Reform -Tump – Asia

There is a very light US economic diary this week, but there will be no lack of political bluster as the US tax reform debate rages while Trump deals with North Korean nuclear ambitions and regional trade relations during his whirlwind tour of Asia. But make no mistake the focus is squarely on North Korea headlines.

In a show of military might, an entourage of F-35’s will accompany Trump( actually deployed to Okinawa), and the mainstay of the US Navy’s power projection, two more Aircraft Carriers will be positioned in the Western Pacific bring the total to three.

The Forex market’s reaction to last weeks tax announcement was underwhelming, but there remains USD positivity as investors continue to reweight into US equities, but indeed, that tank is starting to dry up. There remains a lot of puzzlement concerning some of the Houses latest amendments, but hopefully, some clarity is offered today

Political Noise

NY Federal Reserve Governor Dudley is rumoured to be retiring in either spring or summer of 2018. His term was set to end in January 2019.

US political pundits will be paying close attention to the Virginia Governor race on Tuesday which appears to be a very tight contest between Democrat, Ralph Northam and Republican, Ed Gillespie, with many of the same issues as the presidential election likely to be top of the votes agenda.With President Trump approval ratings plummeting, markets will look for confirmation on the election front to validate the polling data.

Key for the USD

For the dollar, to make significant headwinds, it’s in need of a heavy dose of interest rate support from economic data.But given the scarcity of such this week; the dollar may struggle to gain momentum without a helping hand from non-domestic influence. Critical levels of the UST 10’s remain 2.30-2.40 where last week’s weeks topside breach of the Key 2.40 % level was fleeting and did not signal the critical breakout some had expected ( me included) On the downside a test of 2.30 could prove to be the dollar bull undoing.

The Fear of the Fed is the key to a US dollar strength, and without a perceived acceleration of the Fed’s rate-tightening schedule, we may top out on the dollar momentum until the next set of meaningful US economic data convinces.

Danger from Downunder

This week both the RBA and RBNZ policy meeting take centre stage and should offer up some significant volatility.

The Australian Dollar

The Australian Dollar remains vulnerable to RBA dovish guidance even more so post a dismal nationwide plummet in retails sales and weaker CPI. While the data suggests traders will continue to sour on the Aussie, but with the evidentiary erosion of the carry vs USD, it should lead to a clean extension for Australian dollar weakness from this point.

The New Zealand Dollar

The NZD is a bit more complicated given extended short positions established on local political noise.These shorts are incredibly vulnerable to a more hawkish RBNZ bias than the market is forecasting.

Keep in mind traders have been selling Kiwi the better part of two weeks and my start to unwind positions ahead of the RBNZ. And while the RBNZ could offer up some divergent( USD) opportunity but given the possible short covering from overextended positions, best be nimble in this trade

However given this setup, an excellent way to express AUD weakness is through NZD especially ahead of the RBNZ as there is a chance for a more hawkish bias than priced in at current spot levels.

The Euro

The market remains very constructive on US assets, but 1.1575-1.1600 remains solid support. I suspect the market continues to play the ranges until something breaks.

The Chinese Yuan

The RMB has remained within a range of 6.45-6.65 of late However, following the 19th National Congress positivity and given the robust fundamentals we expect inflows to continue. Also, policymakers will open up domestic capital markets while adding more market reforms to attract foreign investment for some critical fiscal initiatives.

The Malaysian Ringgit

The Ringgit weathered the latest US interest sell off much better than the markets expected. A few things stand out in the Ringgit favour. The MYR remains undervalued on many models given the surprising levels of economic expansion which creating a considerable punch. But positioning in the MYR remains light, and the absence of an active NDF market, when regional currencies weaken the Ringgit is less likely to do so aggressively given the lack of NDF speculation pressure. And while there is a need to add some much-needed reserves, perhaps with OIL prices looking to move higher, the BNM may be able to add to the reserve coffers at much lower levels than currently offered.

Oil Markets could play more influence

WTI enjoyed a ceaseless move higher on Friday on the back of few if any headlines and while Baker Hughes Rig Count did fall by 1.1%, that came well after the meat of the rally kicked in.All in all, it appears support for OPEC to extend production cuts looks to be growing, and when factoring in the decline in US inventories and rig count, the bulls are smiling

But with the shale output effect not living up the skyscraping market’s expectation, OPEC may sense some weakness and may now be thinking 70 not 60 dollars per barrel; before abandoning the agreement.But given a long way between now and November 30, we anticipate either consolidation or a correction before a push higher to $ 60.00 on WTI.

Turkish Lira and South African Rand carry trades

Both the Lira and Rand came under dealers crosshairs on Friday

TRY

The Lira was trading off the back foot after domestic core inflation hit the highest level in 13 years but cratered when headlines surfaced that President Erdogan has been accused of helping Iran avoid US/international sanction but.Given the tenuous USA-Turkey relationships this latest headline has carry trade investors running for cover once again

On the inflation front, with inflation touching 13 years higher there little to no expectation the Central Bank will loosen monetary policy to spur the economy which saw the Lira fell nearly 1 %

ZAR

The Rand weakness is likely to a combination of some moving parts, but the sell-off appears to be more a function of credit rating jitters as the market is awaiting word from both S&P and Moody’s

Post NFP Market Action

While the NFP came below the market towering expectations, but with a +90k revision to Aug-Sept jobs, the data implies the hurricane influence was terrible, but not as bad as had been reported, so this months rebound was less influential

However, wage growth came in dismally low, but with the hurricane’s distorting effects thought to be skewing the data, there should be no muss or any fuss from the Fed. And while the inflation watchdogs on the FOMC will fret but given the booming US economy, the Fed is pushing forward with December rate hike despite the skinny paychecks fully expecting that wages should respond to the strength in the other payroll headlines. Overall the markets didn’t read too much into weak October AHE growth, which should bounce back in November.

After the USD knee-jerk, astute traders bought dollar on the dip, and ISM non-manufacturing confirmed that fading the primary post-NFP USD weakness was the correct call. The robust print greenlighted a wave USD buying into the weekend, although in G10 ranges were respected.

To be honest, if you didn’t know there was an NFP release on Friday, you might have missed it as price action was neither USD hostile or supportive.

Jay Powell

Munchin finally got his man convincing Trump that continuity and stability at the Fed helm were essential and Jay Powell appointment suggests just that. Powell will not deviate too far from current Fed policy stance while supporting Tumps self-proclaimed stance of being a ” low-interest rate person.” And while his appointment proved to be anticlimactic market chatter was picking up on Friday debating not only the makeup of the new FOMC board but who will be the essential Vice Fed Chair as that post is now the high unknown

GBPJPY – Eyes More Downside Pressure

GBPJPY - The cross eyes further downside pressure with more weakness envisaged in the new week. On the downside, support comes in at the 148.50 level where a violation will aim at the 148.00 level. A break below here will target the 147.50 level followed by the 147.00 level. Conversely, resistance is seen at the 150.00 level followed by the 150.50 level. A cut through that level will set the stage for a move further higher towards the 151.00 level. Further out, resistance resides at the 151.50 level. All in all, GBPJPY remains biased to the upside short term

EURUSD – Remains Vulnerable To The Downside On Bear Pressure

EURUSD - With the pair trading flat following price rejection the past week, more weakness is likely. Resistance comes in at 1.1650 level with a cut through here opening the door for more upside towards the 1.1700 level. Further up, resistance lies at the 1.1700 level where a break will expose the 1.1750 level. Conversely, support lies at the 1.1600 level where a violation will aim at the 1.1550 level. A break of here will aim at the 1.1500 level. Below here will open the door for more weakness towards the 1.1450. All in all, EURUSD faces further recovery higher.