Sample Category Title

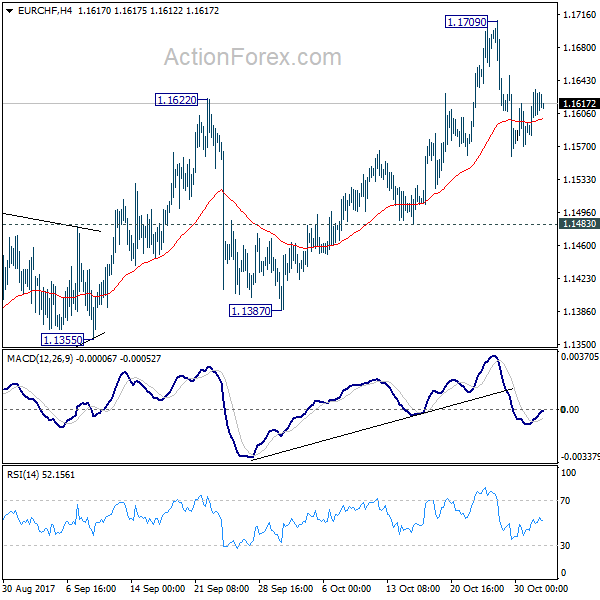

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1588; (P) 1.1610; (R1) 1.1640; More...

Intraday bias in EUR/CHF remains neutral for consolidation below 1.1709. Deeper pull back cannot be ruled out. But still, as long as 1.1483 minor support holds, outlook remains bullish and we'd expect further rally ahead. Break of 1.1709 will target 1.2 key level. However, break of 1.1483 will be an early sign of reversal. In that case, deeper decline should be seen back to 1.1355 support. .

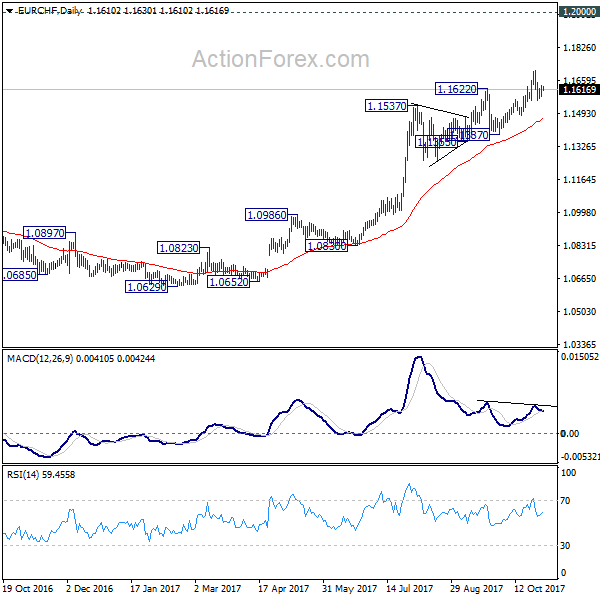

In the bigger picture, long term rise from SNB spike low back in 2015 is still in progress. EUR/CHF should now be heading back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.1355 support holds. However, break of 1.1355 will indicate medium term topping. In that case, EUR/CHF should head back to 55 week EMA (now at 1.1067) and possibly below.

Australia’s Manufacturing Sector Growth Slowed In October

For the 24 hours to 23:00 GMT, the AUD declined 0.46% against the USD and closed at 0.7654.

LME Copper prices declined 0.3% or $21.0/MT to $6802.0/MT. Aluminium prices fell 0.1% or $3.0/MT to $2140.0/MT.

Overnight data revealed that Australia's AiG performance of manufacturing index eased to 51.1 in October from a level of 54.2 in the previous month. The decline in the sector was due to a surge in energy costs, a higher Australian Dollar and closures in the automotive industry.

Earlier today, in China, Australia's largest trading partner, the Caixin manufacturing PMI remained flat at 51.0 for October, meeting market expectations, thus indicating a stable pace of expansion in the sector.

In the Asian session, at GMT0400, the pair is trading at 0.7666, with the AUD trading 0.16% higher from yesterday's close.

The pair is expected to find support at 0.7640, and a fall through could take it to the next support level of 0.7613. The pair is expected to find its first resistance at 0.7693, and a rise through could take it to the next resistance level of 0.7719.

Investors will now await the release of Australia's trade balance and building permits data, both for September, due overnight.

The currency pair is trading between its 20 Hr and 50 Hr moving averages.

Eurozone GDP Advanced For The Third Quarter, But Inflation Growth Slowed In October

For the 24 hours to 23:00 GMT, the EUR rose marginally against the USD and closed at 1.1649, following solid reports on the Eurozone economic growth and unemployment rate.

Data showed that the region’s GDP grew by 0.6% QoQ in the three months to September, more than market expectations for an advance of 0.5%. Additionally, the unemployment rate in the Eurozone unexpectedly dropped to 8.9%, from a revised rate 9.0% in the previous month. Market participants had called for an unchanged reading. On the other hand, the Eurozone inflation slowed in October, supporting the case for the ECB to trim its monetary stimulus only gradually. The flash consumer price index rose 1.4% on a yearly basis in October in the Euro area, compared to a rise of 1.5% in the previous month.

In the US, upbeat economic reports reinforced investor confidence and US growth prospects. US CB consumer confidence index jumped to 125.9 in October, compared to a revised reading of 120.6 in the prior month. Markets were expecting the index to advance to a level of 121.5. Also, US Chicago Fed PMI surprisingly rose to a level of 66.2 in October, compared to a reading of 65.2 in the previous month. Markets had anticipated the Chicago Fed PMI to ease to 60.0.

In the Asian session, at GMT0400, the pair is trading at 1.1632, with the EUR trading 0.15% lower from yesterday’s close.

The pair is expected to find support at 1.1618, and a fall through could take it to the next support level of 1.1603. The pair is expected to find its first resistance at 1.1654, and a rise through could take it to the next resistance level of 1.1675.

This afternoon will bring some major economic releases from the US, namely the ISM manufacturing PMI and the ADP employment change, both for October, along with weekly mortgage applications. Later in the day, the FOMC interest rate decision will be watched by investors for further direction.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

Pound Trading Lower This Morning Ahead Of Britain’s Manufacturing PMI

.

For the 24 hours to 23:00 GMT, the GBP rose 0.61% against the USD and closed at 1.3287, amid news that the EU's Chief Brexit negotiator, Michel Barnier, indicated that he was ready to speed up talks with the UK. He further stated that the next round of Brexit talks would be set “in next few hours or days”.

In another report, the UK government agreed to appoint an additional 5,000 staff for post-Brexit planning.

In the Asian session, at GMT0400, the pair is trading at 1.3274, with the GBP trading 0.10% lower from yesterday's close.

The pair is expected to find support at 1.3216, and a fall through could take it to the next support level of 1.3157. The pair is expected to find its first resistance at 1.3313, and a rise through could take it to the next resistance level of 1.3351.

Trading trends in the pair today are expected to be determined by UK's manufacturing PMI figures for October, scheduled to be released in a few hours.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Japanese Manufacturing PMI Dropped Less Than Expected In October

For the 24 hours to 23:00 GMT, the USD rose 0.45% against the JPY and closed at 113.64.

Overnight data indicated that the final Nikkei manufacturing PMI in Japan fell less than previously expected to a level of 52.8 in October, compared to a four-month high reading of 52.9 in the prior month. The preliminary figures had indicated a fall to 52.5.

In the Asian session, at GMT0400, the pair is trading at 113.85, with the USD trading 0.18% higher from yesterday’s close.

The pair is expected to find support at 113.23, and a fall through could take it to the next support level of 112.6. The pair is expected to find its first resistance at 114.21, and a rise through could take it to the next resistance level of 114.56.

With no major economic release in Japan today, traders will look forward to the consumer confidence index for October, set to release in early hours of tomorrow.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Swiss Franc Trading Lower Ahead Of The SVME – PMI Data

For the 24 hours to 23:00 GMT, the USD rose 0.17% against the CHF and closed at 0.9973.

Meanwhile, the Swiss National Bank reported a record profit of CHF32.5 billion for the third quarter amid a drop in the Franc’s value and strength in equity markets. Earnings included a gain of CHF1.9 billion from the increased value of its gold holdings and of CHF520.0 million from negative interest rates it charges banks to hold deposits.

In the Asian session, at GMT0400, the pair is trading at 0.9987, with the USD trading 0.14% higher from yesterday’s close.

The pair is expected to find support at 0.9959, and a fall through could take it to the next support level of 0.9931. The pair is expected to find its first resistance at 1.0006, and a rise through could take it to the next resistance level of 1.0025.

Moving ahead, traders will now focus on Switzerland’s SVME – PMI data for October, due to release in a few hours.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Canadian Economy Showed An Unexpected Contraction In August

For the 24 hours to 23:00 GMT, the USD rose 0.51% against the CAD and closed at 1.2897, after macroeconomic data showed that Canada's economy unexpectedly contracted in August, supporting the Bank of Canada's (BoC) view to take some caution on further interest rate hikes.

Canada's GDP registered an unexpected drop of 0.1% in August, as slump in oil & gas and manufacturing more than offset gains in other industries. Market had anticipated for a 0.1% rise in GDP following an unchanged reading in the previous month.

Meanwhile, the BoC Governor, Stephen Poloz, stated that Canada is at a 'crucial' spot in the economic cycle and its economy faces a number of significant risks. He highlighted the major sources of uncertainty for the central bank, including weak inflation and wage growth, as well as high household debt.

In the Asian session, at GMT0400, the pair is trading at 1.2899, with the USD trading 0.02% higher from yesterday's close.

The pair is expected to find support at 1.2843, and a fall through could take it to the next support level of 1.2787. The pair is expected to find its first resistance at 1.2935, and a rise through could take it to the next resistance level of 1.2971.

Later in the day, investors will closely monitor Canada's manufacturing PMI data for October and BoC Governor, Stephen Poloz's testimony to Senate.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Market Update – Asian Session: Markets Continue Higher, Metals Also Gaining Ahead Of Fed And BOE Meetings

Asia Summary

Asian equity markets opened generally higher, tracking the gains seen in the New York session.

Honda has gained over 1%, ahead of its earnings report which is expected later today. Nissan and Toyota are also trading higher. Electronic parts manufacturer Murata Manufacturing has declined by over 7%, after reducing its profit forecast. Australian building products manufacturer, CSR, has declined by over 5% after releasing its H1 results and guidance.

In the tech sector, Sony has gained over 9%, as the company reported better than expected Q2 results and raised its FY outlook. Shares of Softbank have rebounded by over 0.5%, after dropping over 4% during the prior session.

Chip equipment firm, Tokyo Electron has also gained over 9% after raising its FY forecast. In South Korea, Samsung Electronics is higher by over 3%. The company has added on to the gains seen in the prior session when it announced its financial results, shareholder return plan and management changes. Hynix has gained over 2%. During yesterday's New York session, chipmaker Micron gained over 6% on above average volume.

Australian retailer Woolworth's has risen by over 1%. During the prior session, the company's shares rose by over 2% after it reported growth in its quarterly sales. Shares of Harvey Norman are higher by over 6% after Australia's securities regulator (ASIC) said that it would not make any further inquiries related to the way the company consolidates its sales figures. Department store Myer Holdings has declined by more than 4%, after reporting a decline in Q1 sales and updating some of its medium-term targets.

Amid the gains being seen in oil prices, Australian energy producer Santos has risen by over 1%, while Woodside Petroleum is also trading higher. Oil Search has declined by over 2% after agreeing to pay $400M to acquire assets in Alaska's North Slope.

In the steel sector, Kobe Steel has risen by over 3%. On yesterday's session, the company's shares gained over 3% amid the release of its most recent earnings report. Following the US equity close, shares of US Steel rose by over 7% on better than expected quarterly earnings.

Mega banks in Japan are generally higher with shares of Mitsubishi UFJ up over 0.7%. In Australia, the ‘big four' banks are also trading generally higher. In China, insurers are trading higher, with shares of China Life up by over 2% and PICC Property P&C has gained over 6%. The Hang Seng Property Index has risen over 0.5%, as shares of Vanke are higher by more than 3%.

Hong Kong listed retailer Tapestry, formerly Coach, said it plans to withdraw its HK listing amid low trading volumes. Earlier in the week, miner Glencore made a similar announcement.

China's Oct Caixin manufacturing PMI met market expectations and was unchanged from the prior figure.

Oct PMI data from Indonesia, Malaysia, Taiwan, Thailand, Vietnam and South Korea declined versus the prior month.

In South Korea, the Oct CPI and Trade Balance data also missed expectations. On yesterday's session, Bank of Korea (BOK) Gov Lee said while Q3 GDP growth was ‘good', he was still monitoring to see if growth continued for a rate hike.

In Japan, there has been renewed speculation in the press that PM Abe is expected to request an extra budget and that Kuroda is likely to be named to another term as governor of the Bank of Japan (BOJ).

USD/JPY has gained over 0.1%, ahead of the later today US Fed decision. The Kiwi has risen by over 0.7% after Q3 jobs data beat expectations.

Looking ahead, US House Tax Committee Chairman Brady said the text of the Republicans tax bill will be released on Thursday. He had previously said there was ‘no announcement of [a] change to Wed's release for the tax bill.'

Japanese companies expected to report earnings later today include ANA Holdings, Hino Motors, IHI Corp, JFE Holdings, Japan Tobacco, KDDI, Mitsubishi Gas Chemical, Mitsui Chemicals, NSK, Rohm, Shinsei Bank, Takeda Pharmaceuticals, Ube Industries and Yamaha.

Key economic data

(NZ) NEW ZEALAND Q3 UNEMPLOYMENT RATE: 4.6% V 4.7%E, EMPLOYMENT CHANGE Q/Q: 2.2% V -0.2% PRIOR; Y/Y: 4.2% V 3.1% PRIOR

(KR) SOUTH KOREA OCT CPI M/M: -0.2% V 0.0%E; Y/Y: 1.8% V 1.9%E; CORE CPI Y/Y: 1.3% V 1.4%E

(KR) SOUTH KOREA OCT TRADE BALANCE: $7.3B V $8.7BE

(JP) JAPAN OCT FINAL PMI MANUFACTURING:52.8 V 52.5 PRELIM

(CN) CHINA OCT CAIXIN MAUFACTURING PMI: 51.0 V 51.0E (weakest pace since June, unchanged from prior)

Speakers and Press

Japan

(JP) BOJ Gov Kuroda being considered for another term - Japan press

(JP) BOJ Gov Kuroda: Reiterates that domestic economy is expanding moderately; downside risks to prices are larger - post rate decision press conference (yesterday)

(JP) Japan PM Abe expected to request extra budget at today's cabinet meeting – Kyodo

(JP) Japan FIn Min Aso: Current economic trends aren't 'bad'

Korea

(KR) US said to pursue direct diplomacy with North Korea - financial press

(KR) South Korea President Moon seeking approval for 2018 budget - speaking at parliament

China/Hong Kong

(CN) PBOC Adviser: See conditions for additional FX reforms - Chinese press

US

(US) Follow Up: House GOP said to delay rolling out tax bill until Thursday - US financial press

Asian Equity Indices/Futures (00:00ET)

Nikkei +1.3%, Hang Seng +0.5%; Shanghai Composite +0.2%; ASX200 +0.5%, Kospi +1.1%

Equity Futures: S&P500 +0.2%; Nasdaq100 +0.3%, Dax +0.7%; FTSE100 +0.2%

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.1655-1.1629; JPY 113.94-113.61; AUD 0.7669-0.7648;NZD 0.6914-0.6883

Dec Gold +0.0% at $1,270/oz; Dec Crude Oil +0.4% at $54.62/brl; Dec Copper +1.1% at $3.14/lb

(AU) Australia sells A$900M in 2.25% 2028 bonds; avg yield 2.7273%; bid-to-cover 5.3x

USD/CNY *(CN) PBOC SETS YUAN REFERENCE RATE AT 6.6300 V 6.6487 PRIOR

(CN) PBoC OMO: Injects CNY240B combined in 7-day, 14-day and 63-day reverse repos v CNY300B prior; Net injection CNY0B v CNY80B prior

(CN) China MOF sells 1-year bonds at 3.54%, bid-to-cover 2.19x; Sells 10-year at 3.82%; bid-to-cover 4.16x

Equities notable movers

Australia/New Zealand

WLD.AU Reports first beef shipment to China after lifting of ban; +12.5%

Japan

6758.JP Reports H1 Net ¥211.7B v ¥26.0B y/y; Op ¥361.8B v ¥ 101.9B y/y; Rev ¥3.92T v ¥3.92T y/y; Raises FY17/18 guidance; +10%

2206.JP Reports H1 Net ¥11.4B v ¥11.6B y/y; Op ¥15.5B v ¥16.4B y/y; Rev ¥187.6B v ¥186.2B y/y; -10%

Korea

006400.KR Reports Q3 (KRW) Net 134.9B v -35.2B y/y, Op 60.2B v -110.4B y/y, Rev 1.71T v 1.63Te; +8%

Daily Technical Analysis: EURUSD, GBPUSD, USDJPY, USDCHF

EURUSD

The EURUSD was indecisive yesterday. The bias remains neutral in nearest term. Immediate resistance is seen around 1.1670. A clear break above that area could trigger further bullish pressure testing 1.1725 area but as long as stay below 1.1900 I remain bearish and any upside pullback should be seen as a good opportunity to sell. Immediate support is seen around 1.1625. A clear break below that area could trigger further bearish pressure testing 1.1575 or lower as a part of the “head and shoulders” bearish reversal scenario as you can see on my daily chart below.

GBPUSD

The GBPUSD continued to trade higher yesterday topped at 1.3288 and hit 1.3293 earlier today in Asian session. The bias remains bullish in nearest term testing 1.3330 key resistance. A clear break and daily close above that area would retest 1.3615 resistance area. Immediate support is seen around 1.3250. A clear break below that area could lead price to neutral zone in nearest term testing 1.3200 area. Overall I remain bullish.

USDJPY

The USDJPY failed to continue its bearish momentum yesterday after unable to make a clear break below 113.20 support area, topped at 113.73 and hit 113.81 earlier today in Asian session. The bias is bullish in nearest term testing 114.50 key resistance which is a good place to sell with a tight stop loss. Immediate support is seen around 113.50. A clear break below that area could lead price to neutral zone in nearest term retesting 113.20 key support which need to be clearly broken to the downside to continue the bearish pin bar scenario testing 112.50 – 111.65 region. On the upside, a clear break and daily close above 114.50 would expose 115.50 or higher. Overall I remain neutral.

USDCHF

The USDCHF failed to continue its bearish momentum yesterday topped at 0.9994. The bias is neutral in nearest term. Overall I remain bullish but need a clear break above 1.0037 to nullify the bearish pin bar scenario targeting 1.0100 or higher. Immediate support is seen around 0.9940. A clear break and daily close below that area would resume the bearish pin bar scenario testing 0.9880 or lower.

Elliott Wave View: DAX Short-Term

Rally from 8/29 low in DAX is unfolding as a double three Elliott Wave structure where Intermediate wave (W) ended at 13089 and Intermediate wave (X) ended at 12903. Up from there, the rally from 12903 low appears to be unfolding as an impulse. Minute wave ((i)) ended at 13066, Minute wave ((ii)) ended at 12906.5, and Minute wave ((iii)) ended at 13249.5. Near term, while pullbacks stay above 12903 low, expect Index to extend higher.

Alternatively, the rally from 10/19 low (12903) can also be unfolding as a flat Elliott Wave structure. In this alternate scenario, DAX can start to correct cycle from 10/19 low now in 3, 7, or 11 swing without making another push higher in Minute wave ((v)). However, regardless whether DAX makes another leg higher or not, we expect Index to remain supported and dips remain to be bought in 3, 7, or 11 swing as far as pivot at 12903 stays intact.

DAX 1 Hour Elliott Wave Analysis