Sample Category Title

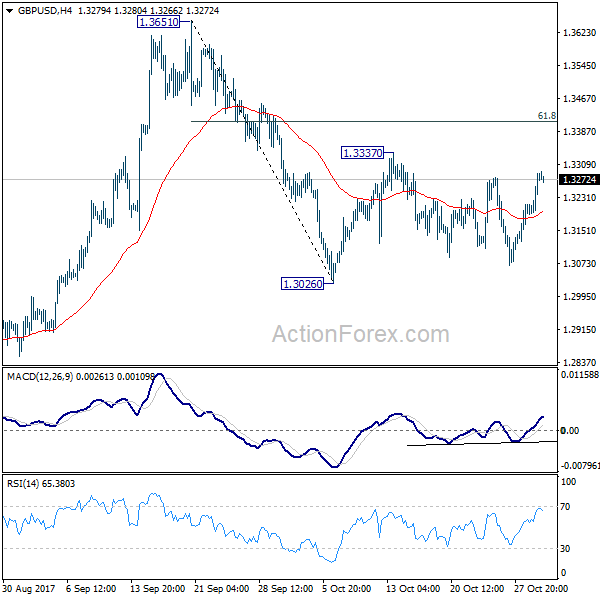

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3219; (P) 1.3253; (R1) 1.3316; More....

Intraday bias in GBP/USD remains neutral for the moment. On the downside, firm break of 1.3026 support will resume the decline from 1.3651 and target 1.2773 key support level. This will also revive the case of medium term reversal. On the upside, in case of another rally, upside should be limited by 61.8% retracement of 1.3651 to 1.3026 at 1.3412 to bring fall resumption finally.

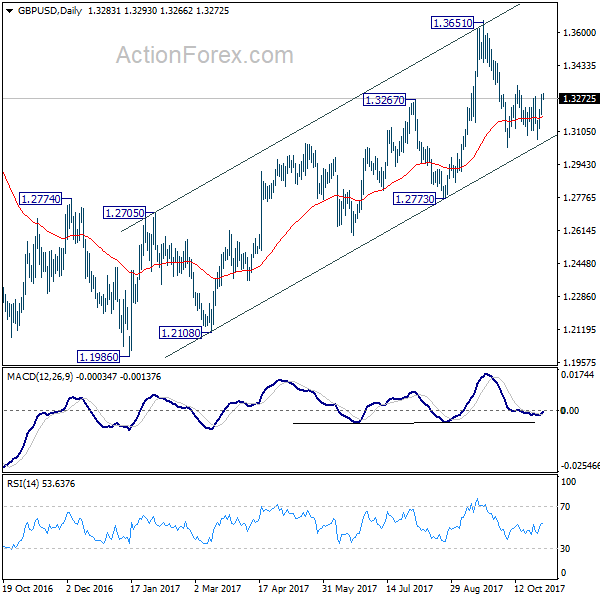

In the bigger picture, while the medium term rebound from 1.1946 was strong, GBP/USD hit strong resistance from the long term falling trend line. Outlook is turned a bit mixed and we'll stay neutral first. On the downside, decisive break of 1.2773 key support will argue that rebound from 1.1946 has completed. The corrective structure of rise from 1.1946 to 1.3651 will in turn suggest that long term down trend is now completed. Break of 1.1946 low should then be seen. On the upside, break of 1.3835 support turned resistance will revive the case of trend reversal and target 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466 .

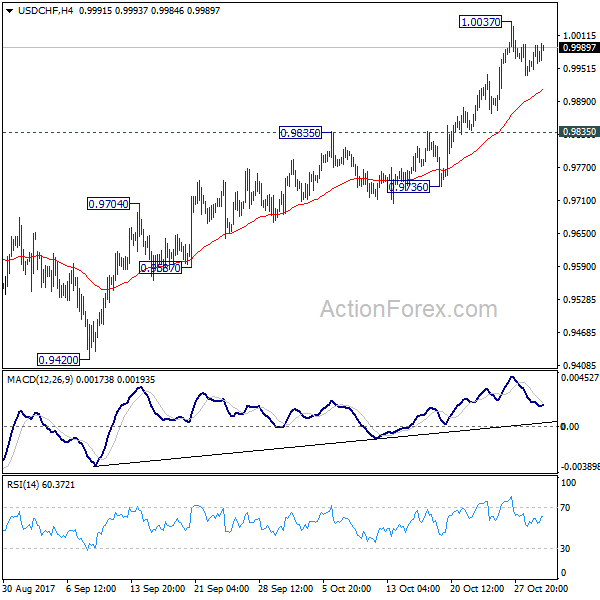

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9945; (P) 0.9969; (R1) 1.0001; More....

Intraday bias in USD/CHF remains neutral as consolidation from 1.0037 temporary top continues. Deeper retreat cannot be ruled out. But downside should be contained above 0.9835 resistance turned support and bring rally resumption. Since 61.8% retracement of 1.0342 to 0.9420 at 0.9990 is already met, break of 1.0037 will turn bias to the upside for 1.0342 key resistance next.

In the bigger picture, current development suggests that USD/CHF has defended 0.9443 (2016 low) key support level again. Rise from 0.9420 could is a medium term up move and should target a test on 1.0342 high. This represents the upper end of a long term range that started back in 2015. On the downside, break of 0.9736 support is now needed to indicate completion of the rise from 0.9420. Otherwise, further rally will remain in favor in medium term.

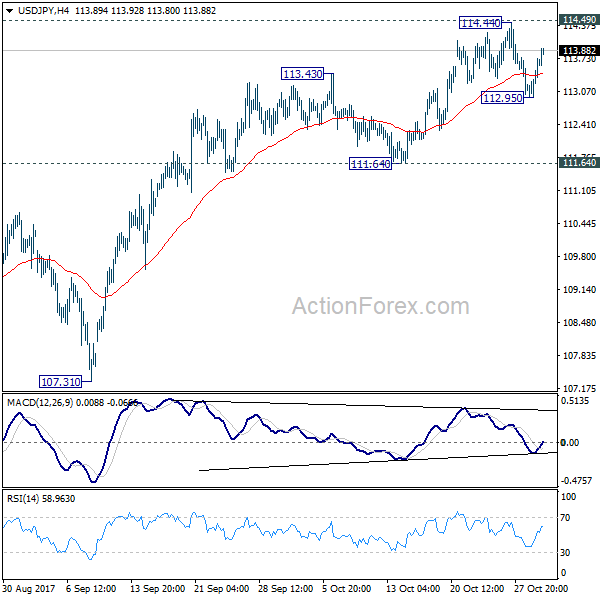

USD/JPY Daily Outlook

Daily Pivots: (S1) 113.14; (P) 113.44; (R1) 113.92; More...

USD/JPY recovers after dipping to 112.95 but it's staying below 114.49 key resistance. Intraday bias remains neutral at this moment. Near term outlook will stays cautiously bullish as long as 111.64 support holds. Decisive break of 114.49 key resistance will confirm that correction pattern from 118.65 has completed at 107.31 already. And USD/JPY should then target a test on 118.65. However, sustained break of 111.64 will argue that rebound from 107.31 has completed and bring retest of this low.

In the bigger picture, medium term rise from 98.97 (2016 low) is not completed yet. It should resume after corrective fall from 118.65 completes. Break of 114.49 resistance will likely resume the rise to 61.8% projection of 98.97 to 118.65 from 107.31 at 119.47 first. Firm break there will pave the way to 100% projection at 126.99. This will be the key level to decide whether long term up trend is resuming.

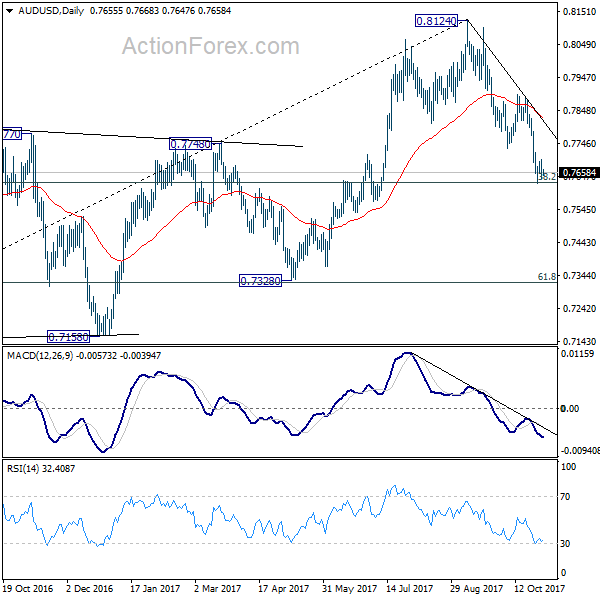

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7630; (P) 0.7664; (R1) 0.7689; More...

Intraday bias in AUD/USD remains neutral for consolidation above 0.7624 temporary low. In case of another rise, upside of recovery should be limited well below 0.7896 resistance to bring decline resumption. Firm break of 0.7624 will resume whole decline from 0.8124 and target next key cluster level at 0.7322/8.

In the bigger picture, corrective rise from 0.6826 medium term bottom is likely completed at 0.8124, after hitting 55 month EMA (now at 0.8067). Decisive break of 0.7328 key cluster support (61.8% retracement 0.6826 to 0.8124 at 0.7322) will confirm. And in that case, long term down trend from 1.1079 (2011 high) will likely be resuming. Break of 0.6826 will target 61.8% projection of 1.1079 to 0.6826 from 0.8124 at 0.5496. This will now be the favored case as long as 0.7896 near term resistance holds.

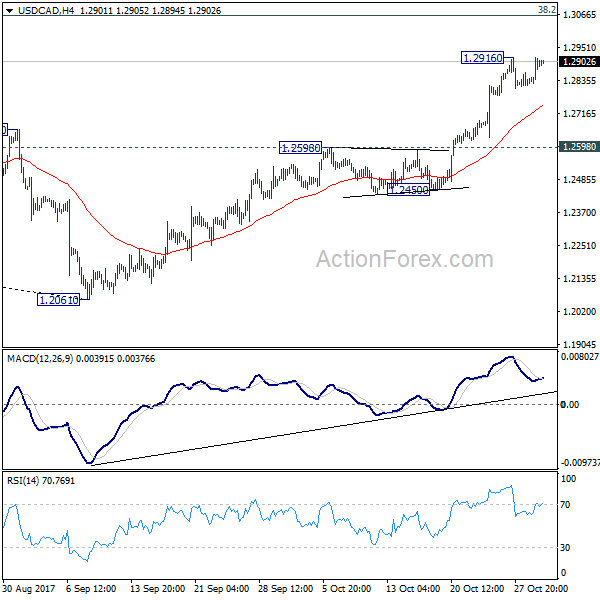

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2835; (P) 1.2875; (R1) 1.2927; More....

USD/CAD is still limited below 1.2916 temporary top and intraday bias remains neutral for the moment. More consolidative trading cannot be ruled out. But downside should be contained well above 1.2598 resistance turned support and bring rally resumption. Medium term trend in USD/CAD should have reversed. Break of 1.2916 will extend the rise from 1.2061 to 38.2% retracement of 1.4689 to 1.2061 at 1.3065.

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4689 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Rise from 1.2061 medium term bottom should now target 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Firm break there will target 1.3793 key resistance next (61.8% retracement at 1.3685). We'll now hold on to this bullish view as long as 1.2450 support holds.

Fed Chair Nomination and Tax Plan to Overshadow FOMC Rate Decision, Dollar Firm

Dollar trades mildly firmer today as markets await FOMC rate decision. Nonetheless, that would likely be a non-event. Fed is widely expected to stand pat. And, December is the month for rate hike, not the current one. Also, traders mind are probably more on the path beyond December. And that heavily ties to who US President Donald Trump will nominate to succeed Janet Yellen as Fed chair after February. It's reported that Trump will announce to nominate Fed Governor Jerome Powell on Thursday. Meanwhile, House Republicans are delaying the rollout of the tax bill due to unresolved questions on some key elements. The announcement was originally scheduled for today but is now delayed by one day to Thursday. Economic data to be released today will also be closely watched including ADP employment and ISM manufacturing from US and PMI manufacturing from UK. We're expecting a lot of volatility for the rest of the week.

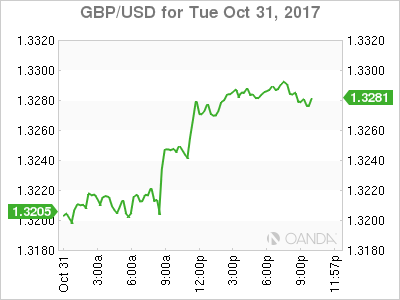

Sterling jumped as EU Barnier ready to speed up talks

Sterling jumped sharply yesterday on positive news on Brexit negotiations. EU's chief Brexit negotiator Michel Barnier said that he's ready to speed up the negotiations with UK. And the schedule for next round of talks would be see in the coming days. Meanwhile, UK Brexit Secretary David Davis told a House of Lords committee that "the withdrawal agreement, on balance, will probably favour the [European] Union in terms of things like money and so on. Whereas the future relationship will favour both sides and will be important to both of us." This is taken as an signal that the UK team is finally ready to clear out all the smokescreens to move on quickly with the talks. And that would likely raise the chance of making sufficient progress by EU summit in December to move on to trade talks afterwards.

Nonetheless, GBP/USD is staying in range of 1.3026/3337, lacking a clear direction. BoE rate decision will be one of the most critical factors in determining the pair's near term direction. BoE is widely expected to raise the Bank Rate by 25bps to 0.50%, first hike in a decade. In our view, this will be a one-off as the Bank Rate will be brought back to pre-Brexit referendum level. The vote split of the decision is the first key point to watch. The tighter the decision, the more unlikely for another hike in near term. In addition, BoE will release the quarterly inflation report. Revision in inflation projection there will tell us how policymakers general feel about the recent surge in inflation.

BoC Poloz: Canada economy at a crucial spot

BoC Governor Stephen Poloz sounded cautious yesterday as he told the parliament that Canada is at a "crucial spot in the economic cycle". He also warned that "significant uncertainties are clouding the way forward". Poloz also reiterated the central bank's statement that any future adjustments in rate will be "cautious". Recent economic data from Canada has been disappointing. GDP showed -0.1% mom in August, below expectation of 0.1% mom rise. That raised some concerns that BoC's two consecutive rate hikes this year are a little too quick.

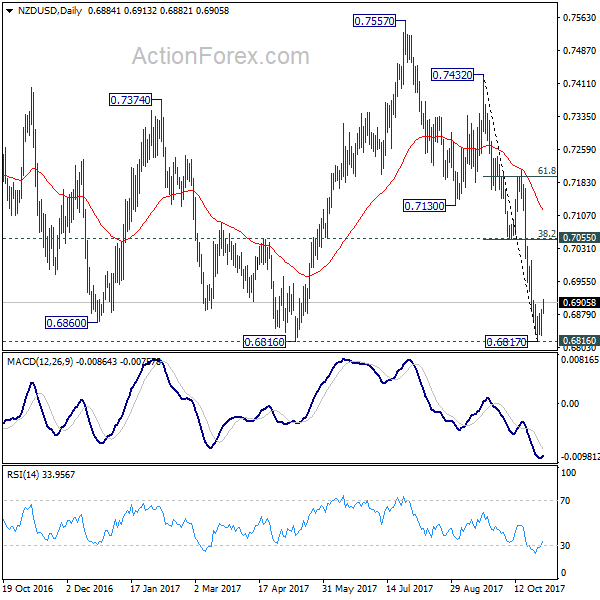

Kiwi rebounds after strong job data

New Zealand Dollar rebounds notably today after solid job data. Employment rose 2.2% qoq in Q3, well above expectation of 0.8% qoq. Unemployment dropped to 4.6%, down from 4.8%, better than expectation of 4.7%. That's also the lowest level since 2008. Nonetheless, the support to Kiwi could be temporary as there shouldn't be any change in RBNZ's neutral stance. The central bank is far from hiking interest rate from the current 1.75% level.

Additionally, markets are concerned with the uncertainties from the new government's policies. Reform on RBNZ is expected after appointment of a new governor in March 2018. Finance Minister Grant Robertson confirmed earlier this week that the government will push for a broader mandate for RBNZ. Robertson expressed that RBNZ would not be tie to a specific target on employment. But " we want to be clear about the bank's role not only in managing inflation, which is extremely important, but also in terms of the overall health of the economy".

NZD/USD should have formed a short term bottom at 0.6817, after being supported by 0.6816 key support level. Some recovery should be seen in near term. But upside should be limited below 0.7055 cluster resistance (38.2% retracement of 0.7432 to 0.6817 at 0.7052) bring fall resumption. It should also be noted that decisive break of 0.6816 key support level will carry larger bearish implication and would pave the way to 0.6102 (2015) low.

Elsewhere

UK BRC shop price dropped -0.1% yoy in October. Japan PMI manufacturing was finalized at 52.8 in October. China Caixin PMI manufacturing was unchanged at 51.0 in October. Swiss and UK PMI manufacturing will be the main focus in European session. US will release ADP employment, ISM manufacturing and construction spending later in the day. Also, FOMC will announce November rate decision.

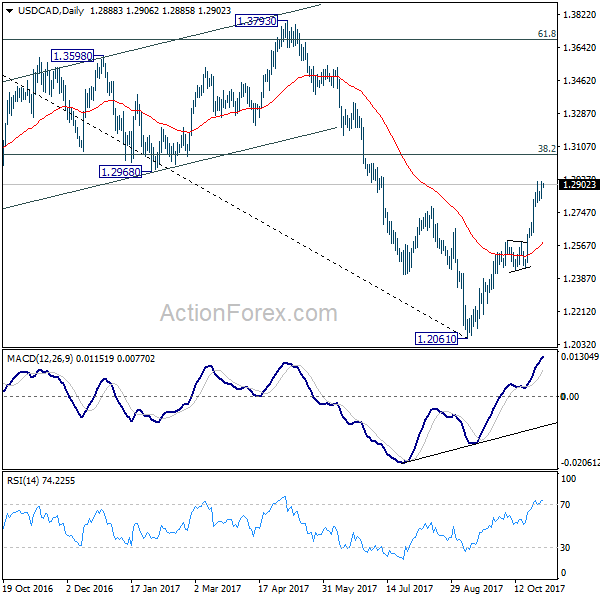

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2835; (P) 1.2875; (R1) 1.2927; More....

USD/CAD is still limited below 1.2916 temporary top and intraday bias remains neutral for the moment. More consolidative trading cannot be ruled out. But downside should be contained well above 1.2598 resistance turned support and bring rally resumption. Medium term trend in USD/CAD should have reversed. Break of 1.2916 will extend the rise from 1.2061 to 38.2% retracement of 1.4689 to 1.2061 at 1.3065.

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4689 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Rise from 1.2061 medium term bottom should now target 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Firm break there will target 1.3793 key resistance next (61.8% retracement at 1.3685). We'll now hold on to this bullish view as long as 1.2450 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Unemployment Rate Q3 | 4.60% | 4.70% | 4.80% | |

| 21:45 | NZD | Employment Change Q/Q Q3 | 2.20% | 0.80% | -0.20% | -0.10% |

| 0:01 | GBP | BRC Shop Price Index Y/Y Oct | -0.10% | -0.10% | ||

| 0:30 | JPY | PMI Manufacturing Oct F | 52.8 | 52.5 | 52.5 | |

| 1:45 | CNY | Caixin PMI Manufacturing Oct | 51 | 51 | 51 | |

| 8:30 | CHF | PMI Manufacturing Oct | 61.4 | 61.7 | ||

| 9:30 | GBP | PMI Manufacturing Oct | 55.9 | 55.9 | ||

| 12:15 | USD | ADP Employment Change Oct | 200K | 135K | ||

| 13:30 | CAD | Manufacturing PMI Oct | 55 | |||

| 13:45 | USD | Manufacturing PMI Oct F | 54.5 | 54.5 | ||

| 14:00 | USD | ISM Manufacturing Oct | 59.4 | 60.8 | ||

| 14:00 | USD | ISM Prices Paid Oct | 67.3 | 71.5 | ||

| 14:00 | USD | Construction Spending M/M Sep | -0.20% | 0.50% | ||

| 14:30 | USD | Crude Oil Inventories | 0.9M | |||

| 18:00 | USD | FOMC Rate Decision | 1.25% | 1.25% |

Market Morning Briefing: The Rise In Dollar-Yen

STOCKS

Dow (23377.24, +0.12%) closed at slightly higher levels but overall remains stable near current levels. 23250-23200 could act as an immediate and decent support for the coming sessions which could again push the index up towards 23500-23750 levels.

Dax (13229.57, +0.09%) looks bullish for the coming sessions and could head towards 13300-13500 levels in the near to medium term.

The fall in Dollar Yen from levels near 114.50 mentioned yesterday has not sustained, bringing a bounce yesterday. Nikkei (22324.64, +1.42%) also opened with a gap up and is trading higher almost certain to test the 22666 levels that we have been mentioning for quite sometime now. Near term looks bullish.

Shanghai (3398.17, +0.14%) tested 3410 on the upside but is trading at lower levels just now. Overall the 3425-3360 region is likely to hold for some more time. No major movement expected outside the given range just now.

10400 is holding so far in Nifty (10335.30, -0.27%). Looking at the 3-day candles a short correction is expected in the near term heading towards 10200-10000 levels before resuming the upward rally. In case, the index fails to see a correction and breaks above 10400, we could see a test of 10500-10600 levels but that is the less preferred scenario while below 10400.

COMMODITIES

Gold (1269.68) may trade above 1260 for some time. A break below 1260 could open up downside towards 1240 which could be tested in November. Else a bounce back from 1260 would be the preferred scenario just now.

Silver (16.73) could test 16.50 on the downside before bouncing back again towards 17 in the coming sessions.

Brent (61.23) is trading above important resistance near 61 as seen on the weekly candles. If the rise sustains, 63 would be the next immediate target on the upside. Else a short dip from current levels is a possibility.

WTI (54.66) has some more room on the upside on the 3-day candles and could test 55-56 on the upside before starting a short term correction towards 53 again. Near term looks bullish followed by a correction thereafter.

Copper (3.1435) has risen from levels above 3.05 support and while that holds, the price could be ranged within 3.17-3.05 region for a few sessions.

FOREX

As it turns out, Dollar-Yen (113.87) did not break below 113.00 and has moved up sharply instead, pulling Euro-Yen (132.50) along with it, which has been helped by a bit or recovery in the Euro (1.1635) as well. The Dollar Index (94.67) remains strong.

The rise in Dollar-Yen (113.87), which negates the chances of a near-term fall to 112, has been aided by a bit of recovery in US yields yesterday after the slide on Monday. 113.00 is now established as a near term Support and a test of 114.50+ again comes into the picture. Intra-day Supports seen at 113.60 and 113.00.

The Euro-Yen (132.50) has disappointed by not falling towards 130 and bouncing back from 131.50 instead. Need to see if it manages to rise past intra-week Resistance in the 132.93-133.35 region now.

Although the Euro moved up to 1.1661 yesteday, there's a small Bear Flag which could yet push the Euro down to the Bear SHS target near 1.15 if the market remains below 1.1660 today. Let us see how this unfolds today, especially with the FOMC in the evening.

As expected, the Pound (1.3275) has moved up to the upper end of the 1.31-33 range and might try and move down again towards 1.31 in the coming days. The Aussie (0.7665) dipped yesterday instead of moving up further, but the Support at 0.7630-20 is holding as of now. Need to see if this Support holds/ breaks over the next couple of days. We are ambivalent.

Dollar-Yuan (6.6268) ought to be moving up towards 6.70 in the coming weeks, but seems to be taking time for it. Dollar-Rupee (64.75) might well find Support in the 64.70-60 region today.

INTEREST RATES

US FOMC today. Market looking to see what is the outlook on Inflation in the wake of recent strong data like the GDP (+3.03%) and Core CPI (+2.23%). Bond Yields have picked up a bit again yesterday after having fallen the day before. At best the 30Yr (2.88%) might move sideways between 2.75-3.00% in November before trying to break higher later.

The US Yield Curve is flattening again, with the 30-5 down to 0.87% and 30-10 down to 0.50%. Both can dip by another 1bp.

As Dollar-Yen (113.87) surprised by moving up yesterday, need to watch whether the US-Japan 10Yr Spread (2.31%) will bounce from current levels today.

Another Taxing Day For Dollar Bulls

Another Taxing Day for Dollar Bulls

Month-end flow distortions, Fed Chair announcement and the anticipation of House Republicans to release a draft of legislation on tax reform tomorrow likely explains the dollars reluctance to move higher but hopefully, Thursday's FOMC will have traders cranked up for some tangible offerings as the FX market's focus has been wholly purposeless the past 24 hours or so.

But if you thought the tax reform debate would become less muddled, don't get too excited as the Senate is planning on releasing its watered down version next week aimed at appeasing the Republican moderates and even some Democrats.

While the Fed Chair nomination( expected Thursday) and the specificities around the tax proposals will continue to dominate headlines, given the high performance in US economic data there is entirely no reason to expect anything but a reasonably hawkish tone from Yellen. More so with the recent US Q3 GDP coming in at 3.0% showing no dismissive impact from the Hurricanes, suggesting the US economy is roaring. With December rate hike running at 85 % probability a definitive signal from Yellen that the US' economic performance is cause enough to warrant gradual rate hikes, we could see a more aggressive reprice for the 2018 Fed campaign. There are 22 bps of hikes priced into Dec FOMC with around a further two rate hikes priced for 2018.

.Keep in mind, these are gloomy forecast and if inflation were to strike like a thunderbolt out of nowhere, the market would have to do some giddy-up to pricing in a much more aggressive Fed tack. Speaking of which and looking through the Fed Chair nomination which is debatably fully priced in, the markets will be very focused on Friday's AHE more so after the dramatic September reading. The market was a bit dismissive of that print due to hurricane distortions, but if this month reading indicates any hint of wage pressure the dollar will rocket higher.

The New Zealand Dollar

It's been a tough slog for the Kiwi bulls of late, but the resounding beat on this morning's jobs data with massive 2.2% rise in employment in Q3, easily outpacing the consensus forecast of 0.8% a significant short squeeze has unfolded And while this outsized print will unlikely have any significant bearing on the RBNZ policy given the increased political surveying and involvement in the system, it will none the less underpin sentiment until the FOMC release.

The British Pound

The BoE is expected to raise rates, but the fate of the pound remains on guidance. If the market perceived a one and done, which is the most likely scenario, the Pound is at risk of a sharp retracement. However, if the statement signals the early stages of a rate hike cycle, traders will be tripping over one another to buy topside exposure on the Pound. But like so many other central banks the BoE is also dealing with tepid wage growth, despite some exchange drove inflationary pressure, the market leaning towards the one and done camp.

The Australian Dollar

The most active persuasion trade continues to be the short AUD as its one of those wake-ups and smells the coffee type scenarios.The evolving data divergence between the US and Australia is too poignant to ignore, and the market should remain in sell the rally mode looking for a significant break lower on a more aggressive Fed narrative. Even a moderately hawkish fed should do the trick

The Japanese Yen

The firm Chicago PMI date overnight Up 66.2 versus just 60.0 expected and 65.2 prior has put, but a small bounce in the USDJPY bulls step. But to be honest, the follow through has been rather insipid given the plethora of data and position risk yet to unfold this week

EM Asia

The sharp drop in US yields on the back of the Mueller investigation and the less hawk appeal for odds on Fed Chair favourite, Jerome Powell. USDAsia has had a good run on the headline. And with Boj remaining faithful to their overtly dovish forward guidance, regional sentiment has remained buoyant.

Also, the KRW bulls are toasting South Korea improving bilateral relations with China which portends exceptionally bullish for regional sentiment on the de-escalation of geopolitical risk.

With the majority of central banks within the Group of 10 turning dovish, the ECB surprising so, this may reel in EM Asia investment flows which should offset regional risks to higher US interest rates and a slightly stronger

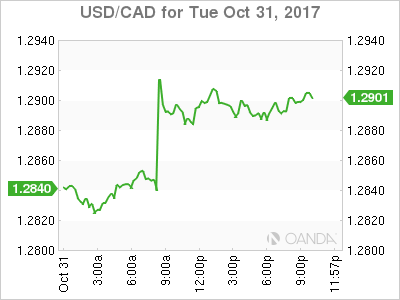

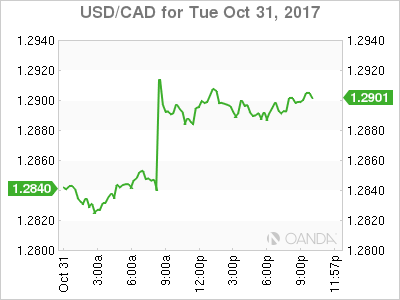

USD/CAD Canadian Dollar Falls After GDP Contraction And Dovish Poloz

The Canadian dollar depreciated on Tuesday versus its American counterpart. The monthly gross domestic product report published by Statistics Canada showed a 0.1 percent contraction in August. Declines in manufacturing, mining and the energy industry edged down the indicator despite rises in other sectors. The biggest red flag was the drop in manufacturing which contracted 1.0 percent. Manufacturing was down across the board with the biggest loses coming in chemical manufacturing.

Bank of Canada (BoC) Governor Stephen Poloz discussed the Monetary policy report (MPR) that was published last week before the Canadian Senate Banking Committee. The central bank chief reinstated his forecast of economic expansion at 3.1 percent in 2017 and 2.1 percent in 2018. The Governor focused on four factors of uncertainty: inflation, excess capacity, wage growth softness and high levels of household debt.

The speech in Ottawa was read as dovish with Governor Poloz admitting that: “the economy is likely to require less monetary stimulus over time, but we will be cautious in making future adjustments to our policy rate”.

The USD/CAD gained 0.46 percent on Tuesday. The currency pair is trading at 1.2892 after a disappointing contraction of Canadian gross domestic product (GDP) of 0.1 percent in August. The Canadian economy is facing a slowdown after an impressive first half. The July GDP reading was flat, and with a small forecasted gain of 0.1 that never materialized investors sold the loonie against the greenback.

The Bank of Canada (BoC) held rates unchanged last week at 1.00 percent. The central bank had already hiked twice in 2017. BoC Governor Stephen Poloz spoke in Ottawa today in front of the Senate Committee on Banking, Trade and Commerce. The policy maker outlined the crucial spot in the economy cycle the Canadian economy is facing. Poloz used the word “caution” when talking about future adjustment to the policy rate which has been read as the two rate hikes will be it for 2017.

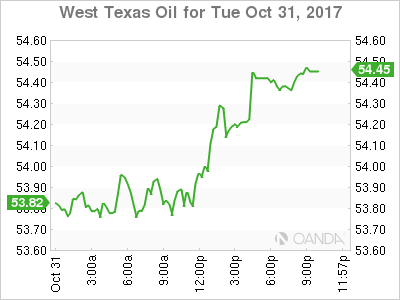

Oil prices surged on Tuesday. The price of West Texas Intermediate is trading at $54.37 ahead of the weekly US crude inventories to be released by the Energy Information Administration (EIA) on Wednesday, November 1 at 10:30 am EDT. The supply cuts by the Organization of the Petroleum Exporting Countries (OPEC) and other major producers have pushed prices higher as there is talk of a further extension to achieve balance in the energy markets. The rise in prices could unleash a rise in US oil rigs that could offset the gains as more supply is added to the market. This has been the pattern in the market of the last couple of years.

Crude inventories in the US are expected to have fallen 1.5 million barrels last week. Iraqi supply is not to full speed as the government is routing some of the northern Kurdish field production through the south. OPEC members will meet again in Vienna on November 30 to discuss the plans for a supply cut extension.

Market events to watch this week:

Wednesday, November 1

5:30 am GBP Manufacturing PMI

8:15 am USD ADP Non-Farm Employment Change

10:00 am USD ISM Manufacturing PMI

10:30 am USD Crude Oil Inventories

2:00 pm USD FOMC Statement

2:00 pm USD Federal Funds Rate

8:30 pm AUD Trade Balance

Thursday, November 2

5:30 am GBP Construction PMI

8:00 am GBP BOE Inflation Report

8:00 am GBP MPC Official Bank Rate Votes

8:00 am GBP Monetary Policy Summary

8:00 am GBP Official Bank Rate

8:30 am GBP BOE Gov Carney Speaks

8:30 am USD Unemployment Claims

8:30pm AUD Retail Sales m/m

Friday, November 3

5:30 am GBP Services PMI

8:30 am CAD Employment Change

8:30 am CAD Trade Balance

8:30 am CAD Unemployment Rate

8:30 am USD Average Hourly Earnings m/m

8:30 am USD Non-Farm Employment Change

8:30 am USD Unemployment Rate

10:00 am USD ISM Non-Manufacturing PMI

Dollar Rebounds Ahead Of Private Jobs And Fed Statement

Fed Expected to Hold Rates Awaiting December meeting

The US dollar is higher against most major pairs on Tuesday ahead of the release of private payrolls data and the statement by the Federal Open Market Committee (FOMC). With employment data due for some good news after the hurricane season, a Fed Chair appointment now imminent before the end of the week and progress in the tax reform front the USD has been bid.

The ADP non-farm employment report will be released on Wednesday, November 1 at 8:15 am EDT. The number of jobs gained in the private sector is forecasted to top 200,000 after the negative effects that impacted last month’s report have subsided.

The U.S. Federal Reserve will ends its two day Federal Open Market Committee (FOMC) meeting on Wednesday and release the statement at 2:00 pm. The Fed is not expected to make any changes to the benchmark interest rate that currently sits in the 100–125 basis points range. The CME FedWatch tools shows a 0.5 percent of the rate going down. The December meeting in stark contrast is at a 99.5 percent of it being higher than the current range.

The EUR/USD is flat on Tuesday. The single currency is trading at 1.1653 with the EUR appreciating 0.40 in the first two trading sessions of the week. The balance in the currency pair could break on the USD side on the anticipation of improved private jobs data to be released on Wednesday and ahead of the U.S. non farm payrolls (NFP) report due Friday. The FOMC statement will offer little clues going forward but investors will be looking closely at the language used by the central bank for more hints on the December rate setting meeting.

The Trump choice for the Fed Chair position is now down to Jerome Powell at the Federal Reserve and John Taylor, an economist at Stanford University. Given the opportunity the Trump administration has to reshape the Fed they both could end up in leadership positions as the Vice Chair role is also vacant. Of the two Taylor is thought to be the more hawkish as Powell is part of the current central bank staff that has hiked rates twice this year and on its way for a third, but Powell is certainly not a dove.

The GBP/USD rose 0.57 percent on Tuesday. The currency pair is trading at 1.3283 due to improving odds of a softer Brexit. The pound has also been appreciating ahead of Thursday’s Bank of England (BoE) monetary policy meeting. The UK central bank is thought to have a rate hike ready after a rise in inflation and promising economic recovery. The UK interest rate would rise to 0.50 percent the same level it was before the Brexit referendum.

The USD/CAD gained 0.46 percent on Tuesday. The currency pair is trading at 1.2892 after a disappointing contraction of Canadian gross domestic product (GDP) of 0.1 percent in August. The Canadian economy is facing a slowdown after an impressive first half. The July GDP reading was flat, and with a small forecasted gain of 0.1 that never materialized investors sold the loonie against the greenback.

The Bank of Canada (BoC) held rates unchanged last week at 1.00 percent. The central bank had already hiked twice in 2017. BoC Governor Stephen Poloz spoke in Ottawa today in front of the Senate Committee on Banking, Trade and Commerce. The policy maker outlined the crucial spot in the economy cycle the Canadian economy is facing. Poloz used the word “caution” when talking about future adjustment to the policy rate which has been read as the two rate hikes will be it for 2017.

Market events to watch this week:

Wednesday, November 1

5:30 am GBP Manufacturing PMI

8:15 am USD ADP Non-Farm Employment Change

10:00 am USD ISM Manufacturing PMI

10:30 am USD Crude Oil Inventories

2:00 pm USD FOMC Statement

2:00 pm USD Federal Funds Rate

8:30 pm AUD Trade Balance

Thursday, November 2

5:30 am GBP Construction PMI

8:00 am GBP BOE Inflation Report

8:00 am GBP MPC Official Bank Rate Votes

8:00 am GBP Monetary Policy Summary

8:00 am GBP Official Bank Rate

8:30 am GBP BOE Gov Carney Speaks

8:30 am USD Unemployment Claims

8:30pm AUD Retail Sales m/m

Friday, November 3

5:30 am GBP Services PMI

8:30 am CAD Employment Change

8:30 am CAD Trade Balance

8:30 am CAD Unemployment Rate

8:30 am USD Average Hourly Earnings m/m

8:30 am USD Non-Farm Employment Change

8:30 am USD Unemployment Rate

10:00 am USD ISM Non-Manufacturing PMI