Sample Category Title

Trade Idea Update: GBP/USD – Sell at 1.3255

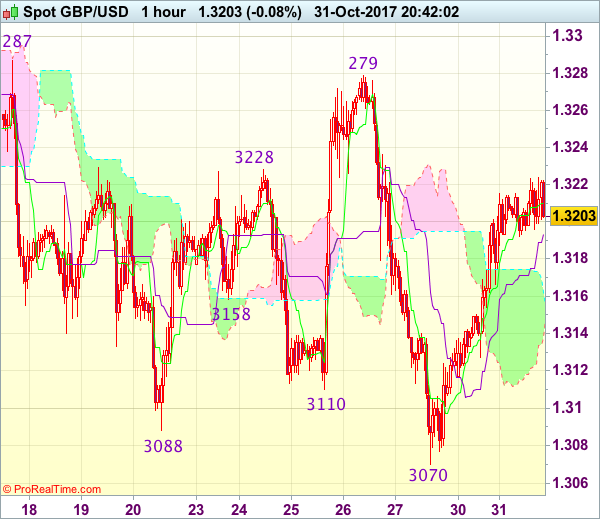

GBP/USD - 1.3205

Original strategy :

Sell at 1.3255, Target: 1.3135, Stop: 1.3290

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.3255, Target: 1.3135, Stop: 1.3290

Position : -

Target : -

Stop : -

As cable has maintained a firm undertone after staging a strong rebound from 1.3070, suggesting near term upside risk remains for further gain to 1.3240-50, however, as broad outlook remains consolidative, reckon upside would be limited and indicated strong resistance at 1.3279-87 would remain intact, bring retreat later, below 1.3120-25 would signal the rebound from 1.3070 has ended, bring weakness to 1.3100, then retest of 1.3070, break there would extend the erratic decline from 1.3338 to 1.3050, then towards recent low at 1.3027.

In view of this, we are looking to sell cable on further subsequent recovery as 1.3255-60 should limit upside. Only above indicated strong resistance at 1.3279-87 would abort and shift risk to the upside for the erratic rise from 1.3027 low is still in progress for further gain to 1.3300-10, then towards 1.3340-50.

USD/JPY Mid-Day Outlook

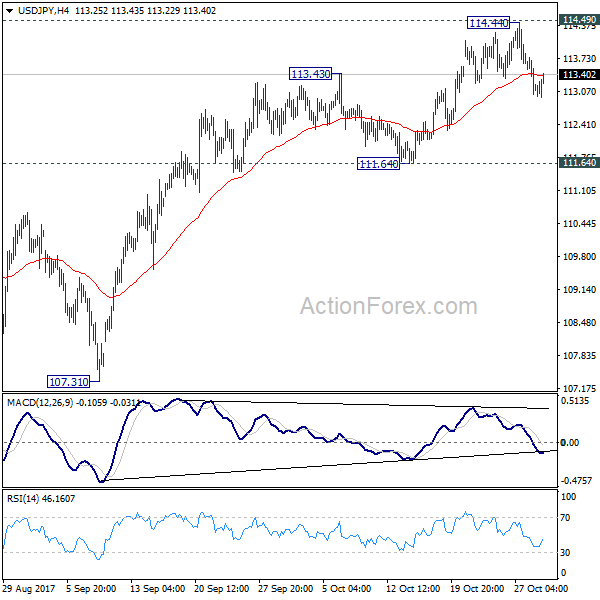

Daily Pivots: (S1) 113.39; (P) 113.91; (R1) 114.20; More...

Intraday bias in USD/JPY remains neutral as consolidation from 114.44 is still in progress. Another fall could be seen. But in any case, outlook will stays cautiously bullish as long as 111.64 support holds. Decisive break of 114.49 key resistance will confirm that correction pattern from 118.65 has completed at 107.31 already. And USD/JPY should then target a test on 118.65. However, sustained break of 111.64 will argue that rebound from 107.31 has completed and bring retest of this low.

In the bigger picture, medium term rise from 98.97 (2016 low) is not completed yet. It should resume after corrective fall from 118.65 completes. Break of 114.49 resistance will likely resume the rise to 61.8% projection of 98.97 to 118.65 from 107.31 at 119.47 first. Firm break there will pave the way to 100% projection at 126.99. This will be the key level to decide whether long term up trend is resuming.

Trade Idea Update: EUR/USD – Sell at 1.1700

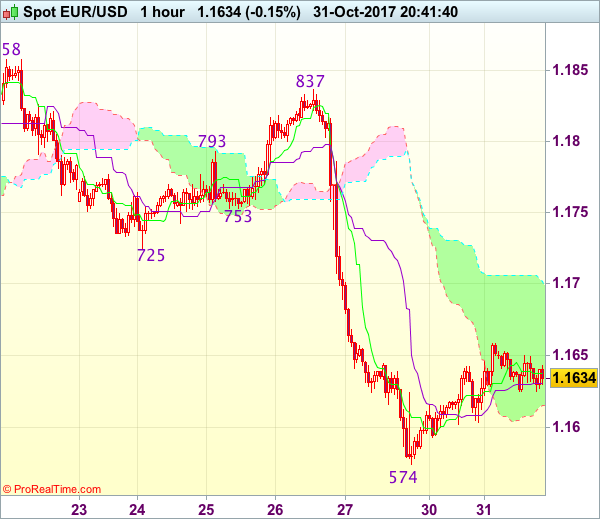

EUR/USD - 1.1635

Original strategy :

Sell at 1.1700, Target: 1.1595, Stop: 1.1735

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.1700, Target: 1.1595, Stop: 1.1735

Position : -

Target : -

Stop : -

Euro’s recovery after falling to 1.1574 late last week has retained our view that further consolidation above this level would be seen and corrective bounce to 1.1660-65 cannot be ruled out, however, reckon upside would be limited to the upper Kumo (now at 1.1706) and bring another decline later, below said support at 1.1574 would extend recent decline from 1.2093 top to 1.1550-55 but loss of downward momentum should prevent sharp fall below 1.1520-25 and reckon 1.1500 would hold from here.

In view of this, we are looking to sell euro on subsequent recovery as the upper Kumo (now at 1.1706) should limit upside and bring another decline. Only above previous support at 1.1725 (now resistance) would signal low is formed instead, bring retracement of recent decline to 1.1750-55 first.

Trade Idea Update: USD/JPY – Sell at 114.00

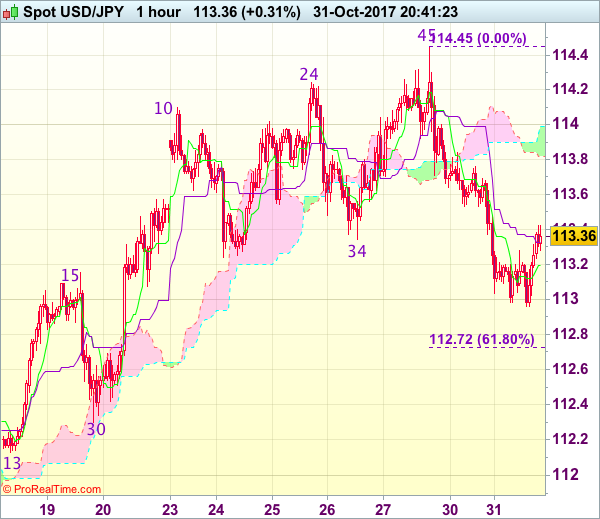

USD/JPY - 113.38

Original strategy :

Sell at 113.80, Target: 112.80, Stop: 114.15

Position : -

Target : -

Stop : -

New strategy :

Sell at 114.00, Target: 113.00, Stop: 114.35

Position : -

Target : -

Stop : -

As the greenback has remained under pressure after dropping from 114.45 (last week’s high), adding credence to our view that top has been made there and consolidation with downside bias remains for this fall to bring retracement of recent upmove, hence further fall to 112.70-75 (61.8% Fibonacci retracement of 111.65-114.45) is likely, however, near term oversold condition should limit downside to 112.50 and reckon previous support at 112.30 would hold from here, bring rebound.

In view of this, we are looking to sell dollar on recovery but at a higher level as the upper Kumo (now at 114.00) should cap upside and bring another decline. Above 114.20-25 would abort and signal the retreat from 114.45 has ended, bring retest of indicated strong resistance at 114.45-50 which is likely to hold on first testing.

CRUDE OIL: Retains Broader Uptrend, Eyes The 55.21 Zone

CRUDE OIL: The commodity may be hesitating but it retains its broader medium term uptrend. On the downside, support resides at the 53.50 level where a break will expose the 53.00 level. A cut through here will set the stage for a run at the 52.50 level. Further down, support resides at the 52.00 level. On the upside, resistance resides at the 54.50 level. Further out, resistance comes in at the 55.00 level. A break above here will aim at the 55.50 level and then the 56.00 level followed by the 56.50 level. Its weekly RSI is bullish and pointing higher suggesting more strength in the medium term. All in all, CRUDE OIL remains biased to the upside in the medium term.

US Futures Lower With Earnings Eyed

- US Employment Costs Expected to See Moderate Growth;

- EUR Edges Lower on Mixed Inflation and Growth Data;

- BoJ Revises Inflation Forecasts Lower and Retains Accommodative Stance.

US equity markets are on course to open a little higher on the final trading day of the month, with the S&P 500 and Dow eyeing new record highs as more companies line up to report on the third quarter.

US Employment Costs Expected to See Moderate Growth

While it's been a busy session in Europe with notable economic releases from the eurozone and overnight with the Bank of Japan making its latest monetary policy decision, the US is looking a little quieter, with the bulk of the week's economic events coming over the course of the next few days. The only notable US releases due today is the employment cost index which has been gradually improving but remains quite volatile. Higher costs typically mean higher prices and goes some way to explaining why the inflation data has underperformed expectations.

The euro is edging lower on Tuesday following a mixed batch of economic data that will likely complicate matters should it continue into next year. The eurozone economy grew by 2.5% last quarter compared to a year ago, while unemployment fell below 9% for the first time since January 2009, in a clear sign that the region remains on a positive trajectory and is continuing to gather momentum.

EUR Edges Lower on Mixed Inflation and Growth Data

While that will be reassuring to ECB policy makers as they wind down their stimulus program on the expectation that it will lead to higher inflation, the CPI numbers themselves will be less encouraging. Prices rose by 1.4% in October compared to a year ago, while core prices rose by only 1.1%, both of which are well below the ECBs sole mandate of below but close to 2% inflation. While the other economic data may give the impression that this will improve over the medium term, the experience of other central banks should act as a warning against such assumptions and discourage against being too keen to tighten.

One of those that can vouch for this is the BoJ, which is dealing with unemployment at 2.8%, annualised growth of 2.5% and yet inflation remains at only 0.7% which is the highest in two and a half years, at which point it was only higher as a result of the sales tax increase. The central bank overnight left its monetary policy unchanged and reduced its inflation forecasts to the year to March 2018 to 0.8% from 1.1% in a further sign that the job of driving inflation to 2% is far from straightforward in the current economic environment.

BoJ Revises Inflation Forecasts Lower and Retains Accommodative Stance

Still, the central bank is convinced it will happen gradually and remains committed to achieving its target, albeit not yet through more stimulus as one dissenter on the board preferred. The yen softened a little overnight in response to the downward revision to inflation expectations and continues to trade around its lowest levels in six months against the dollar. Should the dollar have a strong end to the year as looks possible, we could see the pair trading back at levels not seen since the end of last year.

DAX Steady on Mixed Eurozone Data

The DAX has inched higher in the Tuesday session. Currently, the DAX is at 13,229.50, up 0.09% on the day. On the release front, Eurozone data was a mix. CPI reports missed their estimates, while Preliminary Flash GDP beat the forecast. On Wednesday, the markets will be keeping a close eye on the Federal Reserve, which will release its monthly rate statement.

The eurozone released key inflation and GDP data, and the results were lukewarm. CPI Flash Estimate edged down to 1.4%, shy of the forecast of 1.5%. Core CPI Flash Estimate dipped to 0.9%, short of the estimate of 1.1%. There was better news from Preliminary Flash GDP, which remained unchanged at 0.6%, above the estimate of 0.5%. Unemployment continues to head lower, dropping to 8.9%. This is the lowest level since March 2009. The ECB has announced that it will begin tapering its asset purchase program, as the eurozone economy has rebounded in 2017. Still, inflation remains persistently below the ECB's target of around 2 percent. The asset purchase program has been extended to April 2018, but the ECB could implement an extension if economic data tails off or if inflation fails to move upwards.

In Germany, retail sales rebounded in impressive fashion, gaining 0.5% after two straight declines. On an annualized basis, retail sales gained 4.1%, indicative of strong consumer spending. Germany Preliminary CPI edged down to 0.0%, shy of the forecast of 0.1%. This follows two consecutive readings of 0.1% and points to continuing low inflation in an otherwise robust economy.

The uncertainty and tension remain at fever pitch in Catalonia. The central government has dissolved the Catalan government and parliament, after imposing direct rule on Catalonia. The Catalan government declared independence just before Madrid invoked Article 155 of Spain's constitution. The Spanish government has drawn up charges of rebellion against Catalan President Carles Puidgemont, but he has skipped town, and is reportedly in Belgium. It remains unclear what Puidgemont will do next - he could request political asylum or even declare a government-in-exile. Elections have been slated for December 21, and two parties from Puidgemont's coalition have declared they will participate in the election. With Catalans split down the middle on independence, this saga is likely to continue for some time.

GBPUSD Further Bullish Above 1.3201

The British pound continues to move higher against the U.S dollar during the European trading session, after breaking above the key 1.3201 level. Intraday U.S dollar weakness and the expected rate hike from the Bank of England on Thursday are supporting British pound buying interests. The GBPUSD pair currently trades around the price-highs of the day, ahead of the release of Consumer Confidence in the upcoming U.S trading session.

Buying interest in the GBPUSD pair remains firm whilst price-action holds above the key 1.3201 technical level. Further buying interest towards the 1.3222 and 1.3268 levels should be expected.

Should the GBPUSD move below the 1.3201 technical level in the upcoming trading session, selling towards the 1.3178 and 1.3157 support remains likely.

EURUSD Still Bearish While Below 1.1644 Level

The EURUSD pair continues to struggle to gain traction above the key 1.1644 resistance level, as weaker than expected eurozone inflation data and political woes in Spain, weigh on euro intraday trading sentiment. Multiple technical price failures around the 1.1644 level during the European session, have pressured the EURUSD pair back towards the 1.1630 region. Traders now look to the release of key United States Consumer Confidence data, which due out in the upcoming U.S session.

The EURUSD pair remains intraday bearish while trading below the 1.1644 level, further declines towards the 1.1610 and 1.1580 support level look increasingly likely.

Should EURUSD pair hold price-action above the 1.1644 level for on a multi-time frame basis, further buying towards the 1.1680 and 1.1713 can be expected.

SNB Publishes Interim Results, USD Edges Higher

SNB report solid interim results

The Swiss National Bank published interim results for the first three quarters of the year. After mixed mid-year results - the SNB reported an interim profit of CHF 1.2 billion - the last update brought the smile back to the SNB and all Swiss cantons. As of 30 September, the SNB reported a profit of CHF 33.7bn, which results mostly from a profit on foreign currency positions (30.3bn). Gold holdings appreciated by CHF 2.3bn. The central bank made a profit of CHF 1.5bn from negative interested it charges.

Looking at the details, the SNB benefited from a solid equity market that increased the valuation of its equity positions by CHF 14.4bn, plus a dividend income of CHF 2.5bn. On the other hand, the central bank suffered a valuation loss of CHF 4bn on its bond positions that was however offset by an interest income of CHF 6.8bn. Finally, the continuous depreciation of the Swiss franc over the summer months allowed the SNB to record exchange rate-related gains of CHF 10bn. Indeed, on a trade-weighted basis the Swiss franc fell more than 4.1% between July and September. The CHF depreciation was particularly pronounced against the EUR (-4.50%), the British pound (-4%) and most Scandinavian currencies.

Although Swiss cantons will almost surely receive a piece of the cake, they will have to wait to get the final result and the year is not over yet. The Swiss franc really had a nice ride over the last few months, however one cannot rule out a slight correction as investors are slowly trimming their risky positions as we move into the next year. On Tuesday morning, EUR/CHF has stabilized at around 1.16.

JPY reliant on US policy

As was widely expected the BoJ held its policy strategy unchanged. The vote was 8-1 with the lone dissenter (policy board member Goushi Kataoka) voting for additional easing measures such as examining 10 year 0.0% and 15 year 0.20% yield targets. In their quarterly outlook report, the bank downgraded core inflation forecasts to 0.8% from 1.1% in 2017 and 1.4 from 1.5% in 2018. Member continued to expect their 2% inflation target rate would be reached by 2019. A bright spot was growth, which was revised marginally higher to 1.9% from 1.8%. At the accompanying press conference Governor Kuroda reiterated, that discussion of exit strategy was premature.

Effect on JPY was muted, as USDJPY was range-bound between 112.95 and 113.25. In regards to FX, BoJ policy is losing effectiveness to debase the JPY as years of Abenomics has exhausted traders. Any adjustment in the BoJ ultra-accommodative policy would be unlikely unless CPI climbed well above 1% in a smooth trend. However, markets could see micro tuning with slowing its purchasing this year limitations on the volume of JGBs in rotation, but a maintenance of YCC should not be a problem.

FX prices has reconnected with US yields (especially US 10yr yields) indicated that the fate of USDJPY is no longer in the hands of BoJ but dependent on policy decision in the US. The failure of the USDJPY to break 115 suggests correction to 112.30 to loosen extended longs. PM Abe recent decisive electoral victory and probability that BoJ Governor Haruhiko Kuroda will be reappointed in April indicated JPY weakening policy will remain although less effective, in effect.