Sample Category Title

Elliott Wave Analysis: EURUSD And S&P500 Intra-Day Updates

EURUSD is slow and it may be because of closed markets in Germany because of Reformation Day. So DAX is not moving at the moment, but it may open much higher tomorrow if US stocks will continue to move higher. In fact, there was a three wave retracement on E-mini S&P500 which looks like a completed wave four so price may be back at the highs soon.

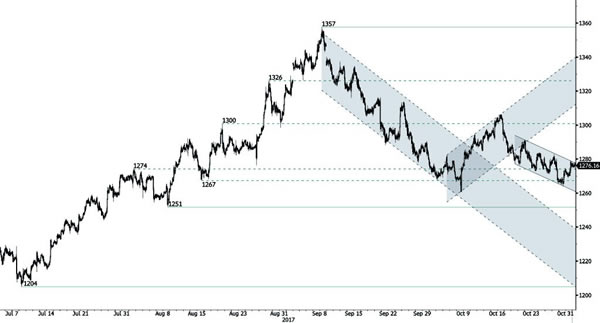

S&P500, 1H

While stocks are headed up we may continue to see stronger dollar, especially against commodity currencies and against euro now as well. There is a nice rally from 1.1570, but it’s slow so probably a corrective leg that can stop at 1.1670/80 intraday resistance, where fourth wave rally can be limited. A drop back to the lows is in our view as long as 1.1729 is not breached.

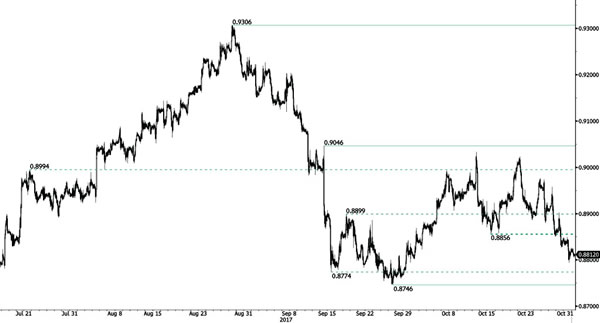

EURUSD, 1H

Market Update – European Session: Central Banks In Focus

Notes/Observations

Overnight

Asia:

China Oct Manufacturing PMI (official govt) 51.6 v 52.0e; Non-Manufacturing PMI: 54.3 v 55.4 prior; Policy makers may be incrementally more relaxed about supporting growth after the Party Congress

Bank of Japan (BOJ) left its policy steady (as expected). Left Interest Rate on Excess Reserves (IOER) unchanged at -0.10% and maintained its policy framework of "QQE with Yield Control" around 0.00% and asset purchases at annual pace of ¥80T. Vote was 8 to 1 with Kataoka (new member) again dissenting

BOJ Outlook for Economic Activity and Prices raised FY17/18 GDP growth outlook from 1.8% to 1.9% and maintained FY18/19 GDP growth outlook at 1.4% and FY19/20 GDP growth outlook at 0.7%. Cut FY17/18 core CPI outlook from 1.1% to 0.8%; Cut FY18/19 core CPI outlook from 1.5% to 1.4% but maintained FY19/20 core CPI (excluding effect of consumption tax hike) at 1.8%

Japan Sept Jobless rate in-line at 2.8% and again matched its lowest rate since Jun 1994

Europe:

Chancellor of Exchequer Hammond (Fin Min) is under pressure to abandon fiscal targets, but pledges to respect fiscal rules

Fitch on Spain: Sovereign rating reflects persistent Catalonia tension. Escalation that significantly worsened the outlook for Spanish growth and public finances could prompt negative action on the sovereign rating (**Reminder: On July 21st Fitch affirmed Spain sovereign rating at BBB+; revises outlook to Positive from Stable)

UK Oct GFK Consumer Confidence: -10 v -10e

Americas:

White House Press Sec Sanders: White House wants to pass House tax bill by Thanksgiving (the same time frame given by Speaker Ryan). President Trump has no intention of firing Special Counsel Mueller; indictments announced today have nothing to do with the President or his –campaign

White House: President Trump to make announcement on Fed Chair decision on Thursday (Nov 2). Most recnt speculation that Trump was likely to name Jerome Powell as Fed Chair

Treasury Sec Mnuchin: Treasury was not seeing a lot of demand for ultra long bonds; to continue to monitor market for interest

Economic Data

(FR) France Q3 Advance GDP Q/Q: 0.5% v 0.5%e; Y/Y: 2.2% v 2.1%e

(TR) Turkey Sept Trade Balance: -$8.1B v -$8.1Be

(FR) France Oct Preliminary CPI M/M: 0.1% v 0.1%e; Y/Y: 1.1% v 1.0%e

(FR) France Oct Preliminary CPI EU Harmonized M/M: 0.1% v 0.1%e; Y/Y: 1.2% v 1.2%e

(FR) France Sept Consumer Spending M/M: 0.9% v 0.6%e; Y/Y: 2.8% v 1.9%e

(FR) France Sept PPI M/M: 0.5% v 0.4% prior; Y/Y: 2.1% v 1.9% prior

(TW) Taiwan Q3 Preliminary GDP Y/Y: 3.1% v 2.2%e

(AT) Austria Q3 Preliminary GDP Q/Q: 0.6% v 0.7% prior; Y/Y: 2.6% v 2.8% prior

(IT) Italy Sept Preliminary Unemployment Rate: 11.1% v 11.1%e (matched lowest level since 2012)

(ZA) South Africa Q3 Unemployment Rate: 27.7% v 27.7% prior (matched highest level since 2003)

Fixed Income Issuance:

(ID) Indonesia sold total IDR22.5T vs. IDR15T target in 3-month and 9-month Bills; 5-year, 10-year 15-year Bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 +0.2% at 394.7, FTSE 0.4% at 7515, DAX +0.1% at 13229, CAC-40 +0.2% at 5502, IBEX-35 +0.4% at 10484 , FTSE MIB flat at 22758, SMI +0.4% at 9214, S&P 500 Futures +0.2%]

Market Focal Points/Key Themes:

European Indices trade higher across the board, continuing the upward momentum with good earnings from Oil Giant BP, Airbus and Ryanair underpinning the rise. Advertising giant WPP trades higher despite cutting their full year outlook, while Gerberit and BNP Paribas trade lower after missing estimates.

Looking notable earners include Pfizer, Under Armour, Lumber Liquidators and Kellogg.

Equities

Consumer discretionary [ Just Eat [JE.UK] +3.9% (Q3 update, raises outlook), RyanAir [RYA.UK] +4.9% (Earnings)]

Industrials: [Airbus [AIR.FR] +2.3% (Earnings), Geberit [GEBN.CH] -4.6% (Earnings), Weir Group [WEIR.UK] -6.2% (Trading update, cuts outlook), SCA [SCAB.SE] +4% (Earnings), - Oerlikon [OERL.CH] +2.8% (Earnings)]

Financials: [BNP Paribas [BNP.FR] -3.3% (Earnings)]

Energy: [BP [BP.UK] +3.5% (Earnings), Siemens Gamesa [SGRE.ES] +5.8% (Contract)]

Speakers

Russia Central Bank 1st Dep Gov Yudaeva reiterated that govt opposed to capital controls. Had the tools to maintain stability under current sanctions

Russia Central Bank Oct 12-month Inflation Expectation Survey: Households see CPI at 9.9% v 9.6% prior survey

BOJ Gov Kuroda post rate decision press conference reiterated that domestic economy was expanding moderately while downside risks to prices were larger. To continue with easing to hit 2% inflation target asap. BOJ was far from price target and no need to change Yield Control (YCC). He added that BOJ saw no need to adjust all easing package at once at some point in the future. Upward pressure on wages was growing steadily. Important for govt to maintain faith on fiscal reform; have not given up on primary budget surplus discipline

Bank of Korea (BOK) Gov Lee Ju-yeol: To check if the solid growth trend continues and also check price movements before any change in policy

Currencies

FX markets were subdued at month end with German markets closed for public holiday.

The GBP/USD little changed with focus on the upcoming BOE rate decision on Thursday. For the month of October the GBP was weaker as dealers noted that the 1st interest-rate increase in a decade would not enough to offset their concerns over Brexit negotiations

USD/CHF was just below parity but the recent weakening of the CHF franc currency helped the SNB report a record 9-month net profit of CHF 33.7B.

Fixed Income

Bund futures trade at 162.75 up 3 ticks poised to end October at month’s high. Support lies at 161.00, followed by 160.38. Resistance stands initially at 163.51, followed by 164.25.

Gilt futures trade at 124.51 up 18 ticks, with the focus remaining on the BOE meeting on Thursday. Continued downside eyeing 123.26. Upside targets 124.90 then 125.24.

Tuesday’s liquidity report showed Monday’s excess liquidity rose to €1.833T from €1.828T and use of the marginal lending facility rose to €431M from €328M

Corporate issuance shows primary sees busiest October on record.

Looking Ahead

(ES) Spain Sept YTD Budget Balance: No est v -€21.5B prior

(AT) Austria Debt Agency (AFFA) announcement on upcoming RAGB bond auction on Wed, Nov 7th

06:00 (EU) Euro Zone Oct Advance CPI Estimate Y/Y: 1.5%e v 1.5% prior; CPI Core Y/Y: 1.1%e v 1.1% prior

06:00 (EU) Euro Zone Q3 Advance GDP Q/Q: 0.5%e v 0.6% prior; Y/Y: 2.3%e v 2.3% prior

06:00 (EU) Euro Zone Sept Unemployment Rate: 9.0%e v 9.1% prior

06:00 (IT) Italy Oct Preliminary CPI (NIC incl. tobacco) M/M: +0.1%e v -0.3% prior; Y/Y: 1.3%e v 1.1% prior

06:00 (IT) Italy Oct Preliminary CPI EU Harmonized M/M: 0.2%e v 1.8% prior; Y/Y: 1.3%e v 1.3% prior

06:00 (GR) Greece Aug Retail Sales Value Y/Y: No est v 2.3% prior; Retail Sales Volume Y/Y: No est v 1.6% prior

06:00 (EU) Daily Euribor Fixing

06:00 (ZA) South Africa to sell combined ZAR2.65B in 2032, 2040 and 2048 bonds

06:15 (CH) Switzerland to sell 3-month Bills

06:30 (UK) Weekly John Lewis LFL sales data

06:30 (EU) ECB allotment in 7-day Main Financing Tender (MRO) tender

06:30 (HU) Hungary Debt Agency (AKK) to sell in 3-month Bills

06:30 (BE) Belgium Debt Agency (BDA) to sell 3-month and 6-month bills

07:00 (IT) Italy Sept PPI M/M: No est v 0.5% prior; Y/Y: No est v 1.6% prior

07:00 (BR) Brazil Sept National Unemployment Rate: 12.4%e v 12.6% prior

07:00 (IL) Israel Sept Unemployment Rate: No est v 4.1% prior

07:45 (US) Weekly Goldman Economist Chain Store Sales

07:45 (US) Daily Libor Fixing

08:00 (CL) Chile Sept Unemployment Rate: 6.5%e v 6.6% prior

08:00 (ZA) South Africa Sept Trade Balance (ZAR): 10.0Be v 5.9B prior

08:00 (IN) India Sept Eight Infrastructure (Key) Industries: No est v 4.9% prior

08:30 (US) Q3 Employment Cost Index (ECI): 0.7%e v 0.5% prior

08:30 (CA) Canada Aug GDP M/M: 0.1%e v 0.0% prior; Y/Y: 3.5%e v 3.8% prior

08:30 (CA) Canada Sept Industrial Product Price M/M: 0.5%e v 0.3% prior; Raw Materials Price Index M/M: 0.4%e v 1.0% prior

08:55 (US) Weekly Redbook Retail Sales

09:00 (US) Aug S&P/Case-Shiller 20-City M/M: 0.40%e v 0.35% prior; Y/Y: 5.90%e v 5.81% prior; House Price Index (HPI): No est v 201.99 prior

09:00 (US) Aug S&P/Case-Shiller (overall) HPI Y/Y: No est v 5.94% prior, House Price Index (HPI): No est v 194.1 prior

09:00 (BR) Brazil Oct PMI Manufacturing: No est v 50.9 prior

09:00 (PL) Poland Oct Preliminary CPI M/M: 0.4%e v 0.4% prior; Y/Y: 2.1%e v 2.2% prior

09:00 (US) The FOMC begins its 2-day policy meeting (Decision on Wed)

09:05 (UK) Baltic Dry Bulk Index

09:45 (US) Oct Chicago Purchasing Manager: 60.0e v 65.2 prior

10:00 (US) Oct Consumer Confidence: 121.0e v 119.8 prior

10:00 (EU) Weekly ECB Forex Reserves:

10:00 (MX) Mexico Q3 Preliminary GDP Q/Q: 0.0%e v 0.6% prior; Y/Y: 1.6%e v 1.8% prior

10:00 (RU) Russia announces weekly OFZ bond auction

10:00 (BR) Brazil to sell I/L 2022, 2026, 2035 and 2055 Bonds

11:00 (CO) Colombia Sept National Unemployment Rate: No est v 9.1% prior; Urban Unemployment Rate: No est v 9.9% prior

11:00 (MX) Mexico Sept Net Outstanding Loans (MXN): No est 3.869T prior

11:30 (US) Treasury to sell4-Week Bills

15:00 (AR) Argentina Sept Industrial Production Y/Y: 4.8%e v 5.1% prior; Construction Activity Y/Y: No est v 13.0% prior

15:30 (CA) Bank of Canada (BOC) Gov Poloz in Parliament

16:30 Weekly API Petroleum Inventories

CRUDE OIL Approaching Long-Term Resistance

Crude oil has surged. Strong resistance given at 52.86 (28/09/2017) has been broken. The commodity is monitoring 1-year high. Expected to show continued increase.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. For the time being the pair lies in an upside momentum. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).

SILVER Continued Decline Within Downtrend Channel

Silver is again grinding lower. Hourly support can be found at 16.60 927/10/2017 low). Hourly resistance is given at 17.46 (13/10/2017 high). Additional support can be found at 16.13 (06/10/2017 low).

In the long-term, the trend is rater negative. Further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

GOLD Riding Lower

Gold remains weak. The technical structure confirms an underlying bearish trend. Strong support lies at a distance at 1204 (10/07/2017 high). Resistance is now located at 1288 (20/10/2017).

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

BITCOIN Consolidating Around All-Time High

Bitcoin has broken key resistance at 6063. Strong support stands very far at 2975 (22/08/2017 low). The technical structure shows a very positive short-term momentum. Support can be located at 5325 (rising trendline). In the short-term, the digital currency should continue rising.

In the long-term, the digital currency has had an exponential growth. There are decent likelihood that the asset will reach $10'000.

EUR/CHF Back Within Former Uptrend Channel

EUR/CHF is back within former uptrend channel. Support is given at 1.1610 (27/10/2017 low). Rising channel suggests further bullish momentum.

In the longer term, the technical structure has reversed. Strong resistance is given at 1.20 (level before the unpeg). Yet, the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).

EUR/GBP Heading Lower

EUR/GBP is showing downside pressures. However, as long as prices are below the resistance at 0.9046 (05/09/2017 high), the shortterm technical structure is biased to the downside Hourly support is given at a distance at 0.8746 (27/09/2017 low).

In the long-term, the pair has largely recovered from recent lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading above from its 200 DMA. Strong resistance can be found at 0.9500 (psychological level).

AUD/USD Short-Term Bounce

AUD/USD continues to bounce back but downside pressures are still lively. Hourly resistance is given at 0.7897 (13/10/2017 high). Further. Expected to show continued decline towards key support at 0.7571 (05/07/2017 low).

In the long-term, the trend is turning positive. Key supports stands at 0.6009 (31/10/2008 low) . A break of the key resistance at 0.8164 (14/05/2015 high) is needed to invalidate our long-term bearish view.

USD/CAD Ready For Another Leg Higher

USD/CAD is holding above former resistance at 1.2778 (15/08/2017 high). This suggests an extension of bullish momentum. Hourly support lies at 1.2331 (26/09/2017 high). Expected to show continued short-term bullish pressures.

In the longer term, the pair has broken longterm support that can be found at 1.2461 (16/03/2015 low). Strong resistance is given at 1.4690 (22/01/2016 high). The pair is likely to head further lower.