Sample Category Title

BOJ Left Stimulus Unchanged, Downgraded Inflation Forecasts

BOJ again voted 8-1 to leave the monetary policies unchanged in October. The targets for short- and long-term interest rates stay at -0.1% and around 0%, respectively while the guideline for JGB purchases remains at an annual pace of about 80 trillion yen. Again, BOJ revised lower its inflation forecasts for FY 2017 and FY 2018 but maintained that for FY 2019. The central bank upgraded the GDP growth outlook for FY 2017 while leaving others unadjusted. The new member was the lone dissent as he voted against the yield curve control measure for two meetings in a row. He judged that 'monetary easing effects gained from the current yield curve were not enough for 2% inflation to be achieved around fiscal 2019'. At the press conference, Governor Kuroda defended the yield curve control policy and the +2% target. As he suggested, the 'main objective is to achieve 2% inflation and stably maintain price growth at that level. There's no change to our view that monetary policy must be guided to achieve this objective' and there is no need to change the yield targets'.

Economic Forecasts

BOJ downgraded its core CPI forecast to +0.8% for FY 2017, from +1.1% previously, and to +1.4% fro FY 2018m from +1.5% previously. The forecast for FY 2019, however, stayed unchanged +1.8%. We expect policymakers to continue revising lower the forecasts in upcoming meetings as it appears to have become a monthly ritual due to stubbornly weak inflation. The nationwide core inflation has improved for nine months in a row, rising to +0.7% y/y in September. However, this has stayed far below the central bank target of +2%. BOJ expects the target could be reached sometime in FY 2019. Meanwhile, BOJ upgraded the GDP growth outlook to +1.9% y/y for FY 2017, from +1.8% previously. Growth for FY 2018 and FY 2019 stayed unchanged at +1.4% and +0.7%.

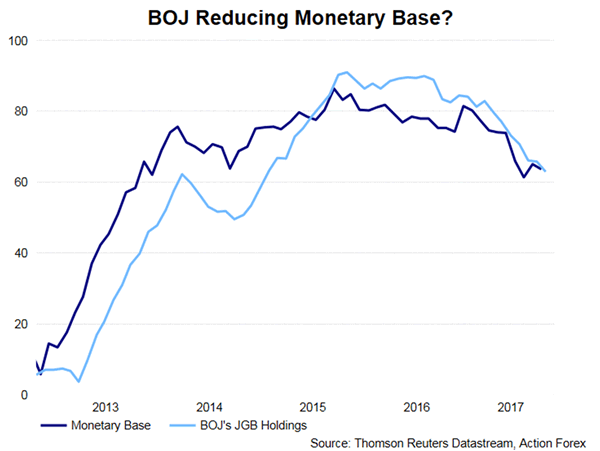

Shifting Policy Focus from Monetary Base

Since the Fed has started balance sheet reduction this month and the ECB announced last week to reduced asset purchases in 2018, Kuroda has encountered this question at the press conference. Unsurprisingly, he immediately shrugged off any intention to taper anytime soon. At he noted, 'it would be misleading for markets for the BOJ to debate an exit strategy now'. He added that 'it's wrong to assume an exit from monetary easing would be difficult just because central banks are embarking on non-conventional monetary policies. Even under conventional monetary policies, central banks can face difficulty exiting if monetary easing or tightening steps are excessive'.

Interestingly, we notice that the monetary base has been shrinking. The chart below shows that the central bank has steadily diminished its monthly JGBs purchase in the first nine months of this year. The annual increase in JGB buying has fallen to 60-ishh trillion yen in September, from about 79 trillion yen in December 2016. This might be evidence that the central bank has gradually move away from targeting monetary base growth, to yield curve control, as a policy instrument. If so, the sustainability of yield curve control should be closely watched.

New BOJ Governor

Regarding the next governor, Kuroda indicated that it is important for him/her to 'have the ability to grasp what is happening in the real economy and the ability to theoretically analyze the impact of policy moves. He or she also needs to have a global human network'. Following Abe's victory in the snap election earlier this month, it is likely that he would reappoint Kuroda for another term. Yet, no matter the next governor is Kuroda or not, we expect the person would have to continue dovish stance under Abe's regime.

(BOJ) Statement on Monetary Policy – October 31, 2017

At the Monetary Policy Meeting held today, the Policy Board of the Bank of Japan decided upon the following. [Note 1]

(1) Yield curve control

The Bank decided, by an 8-1 majority vote, to set the following guideline for market operations for the intermeeting period. [Note 2]

The short-term policy interest rate:

The Bank will apply a negative interest rate of minus 0.1 percent to the Policy-Rate Balances in current accounts held by financial institutions at the Bank.

The long-term interest rate:

The Bank will purchase Japanese government bonds (JGBs) so that 10-year JGB yields will remain at around zero percent. With regard to the amount of JGBs to be purchased, the Bank will conduct purchases at more or less the current pace -- an annual pace of increase in the amount outstanding of its JGB holdings of about 80 trillion yen -- aiming to achieve the target level of the long-term interest rate specified by the guideline.

(2) Guidelines for asset purchases

With regard to asset purchases other than JGB purchases, the Bank decided, by a unanimous vote, to set the following guidelines.

a) The Bank will purchase exchange-traded funds (ETFs) and Japan real estate investment trusts (J-REITs) so that their amounts outstanding will increase at annual paces of about 6 trillion yen and about 90 billion yen, respectively.

b) As for CP and corporate bonds, the Bank will maintain their amounts outstanding at about 2.2 trillion yen and about 3.2 trillion yen, respectively.

[Note 1] With a view to reinforcing the inflation-overshooting commitment, Mr. G. Kataoka dissented from the decision, considering that, if there was a delay in the timing of achieving the price stability target due to domestic factors, the Bank should take additional easing measures and that it was necessary to include that in the text.

[Note 2] Voting for the action: Mr. H. Kuroda, Mr. K. Iwata, Mr. H. Nakaso, Mr. Y. Harada, Mr. Y. Funo, Mr. M. Sakurai, Ms. T. Masai, and Mr. H. Suzuki. Voting against the action: Mr. G. Kataoka. Mr. G. Kataoka dissented, considering that, with a view to lowering the interest rates with longer maturities of the yield curve, it was appropriate for the Bank to purchase JGBs so that 15-year JGB yields would remain at less than 0.2 percent.

The Oil is Updating Its Highs and Getting Ready for a New Attack

The oil is still getting more expensive. Last Friday, the Brent futures contract price for December broke $60 per barrel and continues rising at the beginning of this week. The "bulls" clearly had enough time to "rest" during the weekend and right now are ready for new highs. The oil hasn't been so expensive for more than two years – the current levels were last reached in July 2015. In early November, market conditions remain in favor of the oil buyers. It means that there might be more records in the future.

However, the "commodity bulls" really have reasons to be active. Last week, Mohammad bin Salman, the Crown Prince of Saudi Arabia, confirmed that he was in favor of extending the OPEC+ agreement after its expiration in March 2018. The document, which establishes strict borders and limits for the oil extracting countries, will expire in the first quarter of the next year. The organization has no plan B, but now Saudis joined Russia, the country that promoted the agreement for extension. Later, these countries might as well draw over other members of the organization, which are doubtful or undecided.

It's quite clear that the borders of the agreement can't last forever. But there are no alternatives right now, given that the document really proves to be effective and provides the slowdown of the oil demand. If the agreement is extended for another 6-9 months, the OPEC will have enough time to develop a new strategy how to exit the period of low extraction.

Additional support to the oil "bulls" is provided by political and geopolitical tensions in Libya and Iraq respectively. In this light, investors showed no interest in Baker Hughes reports, which indicated the decline in the number of the rigs in the USA (-4 units). The indicator has been falling for the fourth consecutive week and that's another "bullish factor" for the market.

From the technical point of view, Brent is trading inside the uptrend. The short-term upside target may be at 61.35, which is close to the upside border of the mid-term channel. Also, we can't exclude a possibility that the price may break the border and reach the upside target of the short-term channel at 63.50. But the most probable scenario suggests that the instrument may rebound from 61.35 and then resume falling towards 58.86, which provided significant resistance earlier and was located near the retracement of 50.0%.

US Dollar Cautious Ahead Of Fed, FBI Probe Russian Links Weighs, BoJ Stands Pat

Foreign exchange markets and specifically the US dollar were cautious to break fresh ground during Tuesday's Asian trading as a combination of bearish and bullish factors left traders waiting for more clues.

The probe of links between the Trump campaign and Russia led to house arrests and criminal indictments the previous day, such as that of Trump's former campaign manager Paul Manafort. So far the market hasn't really paid much attention to the news as accusations against Trump's campaign officials have been around for a long time but this is an issue that could hurt the administration's agenda if further negative developments materialize.

One development that might have hurt the US dollar further was a report that any cut in the US corporate tax rate would be a gradual affair over time rather than a one-off measure. This would obviously slow down the benefits of the proposed tax reform and this led to modest profit-taking on Wall Street overnight. In US data released during Monday, September personal spending was stronger-than-expected, while inflation as measured by the Personal Consumption Expenditure remained relatively subdued with the core PCE index posting a 1.3% year-on-year increase as expected.

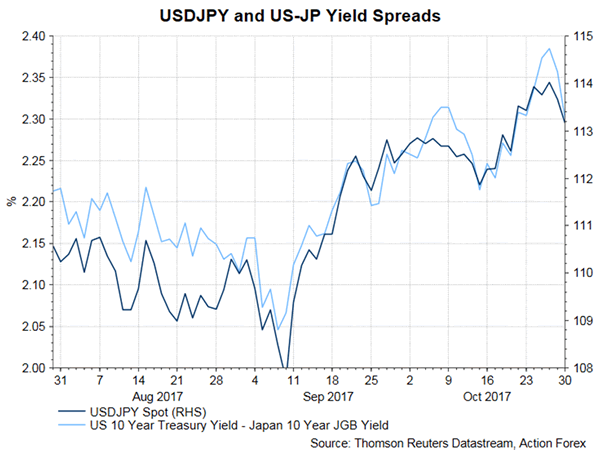

Today also marks the beginning of the Fed's two-day meeting for deciding interest rates. The Fed is not expected to change rates tomorrow, but a statement pointing to a strong possibility of a December hike is to be expected. This could provide support for the dollar, which was being tested against the yen as dollar/yen managed to break below 113 before rebounding slightly above that level.

The Bank of Japan left its policy unchanged during its latest meeting which ended on Tuesday, which was in line with market expectations. There was still one dissenter in the 8-1 vote who advocated more stimulus.

There was also a minor setback concerning China as the country's manufacturing PMI dipped to 51.6 in October from the previous month's 52.4 reading. The reading did hold well above the 50 expansion/contraction limit and services' PMI, although lower than the previous month, was relatively high at 54.3.

The euro was managing to hold the 1.16 level against the dollar after sharp losses the previous week on indications that Catalonian secessionists would be unable to make progress on their goal. A latest poll showed a pro-unity majority in the region, which meant that the parties backing an independent Catalonia would lose their parliamentary majority if elections were held now.

Later today, GDP releases out of the Eurozone (third quarter, preliminary) and Canada (monthly, August) will attract some attention, while later in the day the Conference Board's consumer confidence will be released out of the United States. A speech by the Bank of Canada Governor will take place close to the end of New York trading.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 149.00; (P) 149.50; (R1) 149.95; More

Intraday bias in GBP/JPY remains mildly on the downside for 149.82 support. Break there will resume the correction from 152.82 and target 61.8% retracement of 139.29 to 152.82 at 144.45. Such decline is seen as a correction and we'd look for strong support from 144.45 to bring rebound. On the upside, above 151.38 will target a test on 152.82 high instead.

In the bigger picture, medium term rebound from 122.36 is still expected to resume after corrective pull back from 152.82 completes. Firm break of 38.2% retracement of 196.85 to 122.36 at 150.43 will carry long term bullish implications. In that case, GBP/JPY could target 61.8% retracement at 167.78. However, break of 139.29 will indicate rejection from 150.43 key fibonacci level. And the three wave corrective structure of rebound from 122.36 will argue that larger down trend is resuming for a new low below 122.26.

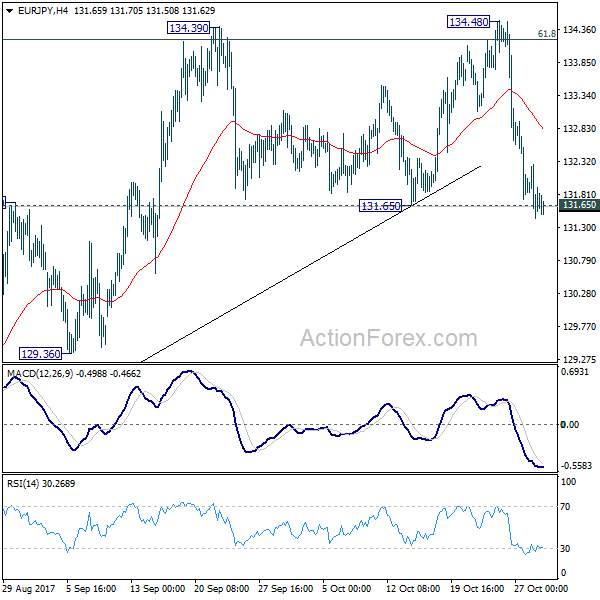

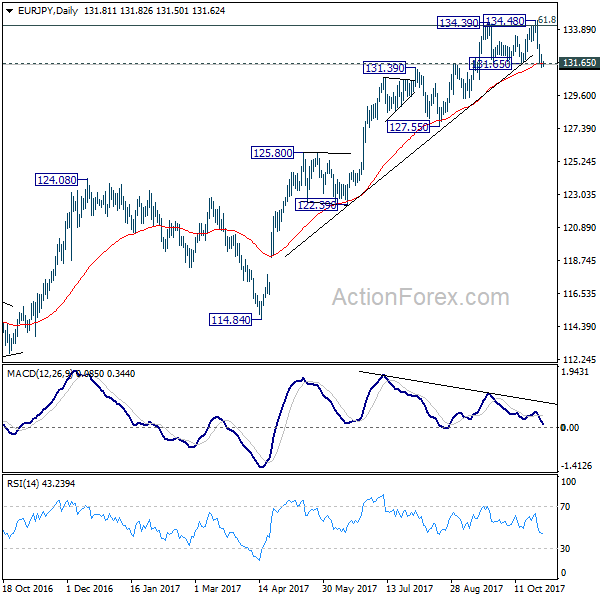

EUR/JPY Daily Outlook

Daily Pivots: (S1) 131.45; (P) 131.86; (R1) 132.28; More....

Focus remains on 131.65 key support in EUR/JPY Decisive break there will confirm rejection from 134.20 fibonacci level. That will also complete and double top pattern (134.39, 134.48) and confirms near term reversal. 55 day EMA will also be firmly taken out. In that case, deeper decline should be seen back to 127.55 key support. On the upside, decisive break of 134.39/48 resistance zone is needed to confirm up trend resumption. Otherwise, even in case of rebound, near term outlook is neutral at best.

In the bigger picture, medium term rise from 109.03 (2016 low) is seen as at the same degree as the down trend from 149.76 (2014 high) to 109.03 (2016 low). 61.8% retracement of 149.76 to 109.03 at 134.20 is already met. Sustained break there will pave the way to key long term resistance zone at 141.04/149.76. However, break of 127.55 support will argue that the medium term trend has reversed and will turn outlook bearish for deeper fall back to 114.84/124.08 support zone at least.

XAUUSD Intraday Analysis

XAUUSD (1275.48): Gold prices managed to post a modest rally as price cleared the minor support/resistance level of 1272. Having cleared this level, we could expect to see further gains that could push price towards the 1285 handle. However, in the medium term, the outlook for gold prices remains flat. A close above 1285 will be required in order to push prices higher towards the 1320 - 1324 region. To the downside, if price continues to consolidate near the 1272 level, we could expect to see a short term decline towards 1262.

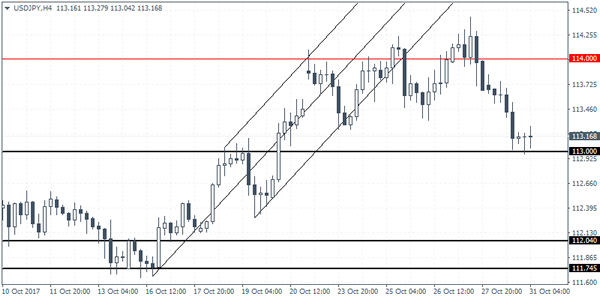

USDJPY Intraday Analysis

USDJPY (113.16): The USDJPY is showing sign of weakness as price action is currently seen hovering near the lower trend line of the rising wedge pattern. This pattern formed on the daily chart signals a possible downside price action. Support is seen at 110.70 which could be the likely target. On the 4-hour chart, USDJPY touched down to the support level at 113.00 briefly. We expect to see a modest rebound off this level as USDJPY remains flat within 114.00 and 113.00 price levels. A breakout to the downside below 113.00 will signal a move to the next support at 112.00 ahead of further declines that can be expected towards 110.70.

EURUSD Intraday Analysis

EURUSD (1.1636): EURUSD managed to close on a bullish note yesterday following two consecutive days of declines. Price action was however muted as the euro approaches the previously breached support level. If resistance is formed here, the EURUSD could be seen reversing the modest gains. Further downside could be expected as the currency pair is likely to follow through to the downside. The initial target level of 1.1552 is likely to be tested followed by further declines towards 1.5500 level of support. This will mark the minimum price objective to the downside, following the descending triangle pattern that was formed.

USD Pauses Ahead Of Trump’s Announcement On Fed Chair Nominee

The US dollar was seen pausing on its tracks on Monday. Lack of economic data saw the markets looking to the broader themes. President Trump is expected to announce his nomination for the next Federal Reserve Chair as Yellen's term ends in February next year. Political developments on the day also saw the former campaign manager, Paul Manafort facing charges in the Russia scandal.

On the economic front, the Bank of Japan held its benchmark interest rates steady at today's meeting. The central bank also retained its QE purchases steady signaling no change. The Japanese yen was seen trading stronger since Monday.

Looking ahead, the economic calendar today will see the Canadian GDP numbers. Economists estimate a 0.1% increase on the month in GDP. Later in the day, the BoC Governor Poloz is also expected to speak which brings some downside risks to the Canadian dollar. Later in the evening, New Zealand's unemployment figures will be coming out. The unemployment rate is forecast to fall to 4.7% from 4.8% previously.