Sample Category Title

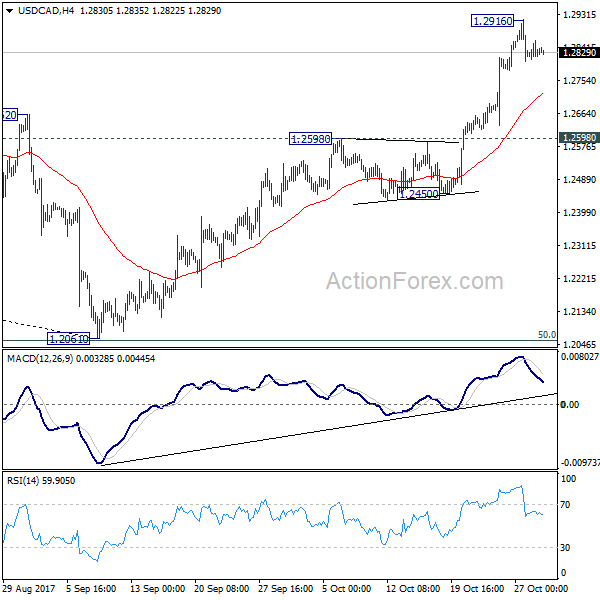

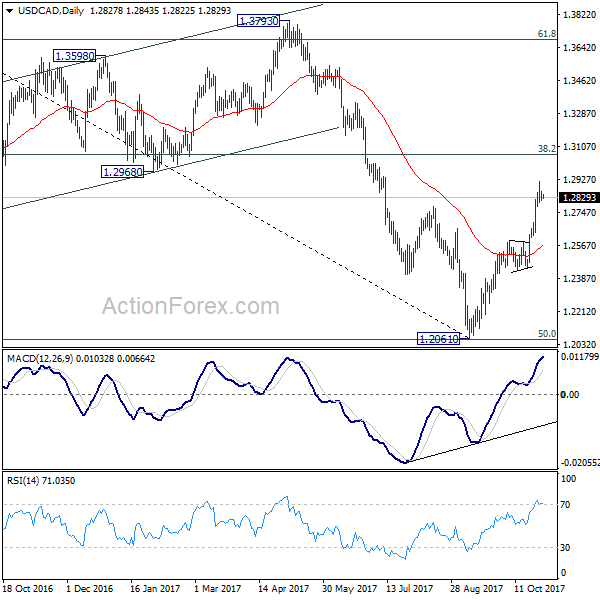

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2809; (P) 1.2835; (R1) 1.2858; More....

USD/CAD is staying in consolidation below 1.2916 temporary top and intraday bias remains neutral at this point. Downside of retreat should be contained above 1.2598 resistance turned support and bring rally resumption. Medium term trend in USD/CAD should have reversed. Break of 1.2916 will extend the rise from 1.2061 to 38.2% retracement of 1.4689 to 1.2061 at 1.3065.

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4689 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Rise from 1.2061 medium term bottom should now target 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Firm break there will target 1.3793 key resistance next (61.8% retracement at 1.3685). We'll now hold on to this bullish view as long as 1.2450 support holds.

Forex: Another Political Headache For Trump

USD gave up some of its recent gains on news that investigators had charged President Trump's former campaign manager regarding the investigation of Russian interference in last year's US Presidential Campaign. Trump's former campaign manager Paul Manafort and another aide, Rick Gates, were both charged with money laundering on Monday. It was also announced on Monday that Former Trump advisor, George Papadopoulos, pleaded guilty in early October to lying to the FBI. The indictment of Manafort & Gates includes accusations of conspiracy against the United States, failure to report foreign bank accounts to the US government and conspiracy to launder money, a count that carries a 20-year maximum prison sentence. U.S. Justice Department Special Counsel Robert Mueller's 5-month investigation into alleged Russian efforts to tilt the election in Trump's favor and into potential collusion by Trump aides has Trump claiming the probe 'a witch hunt' and, as we have come to expect from Trump, he also commented on Twitter: 'Sorry, but this is years ago, before Paul Manafort was part of the Trump campaign. But why aren't Crooked Hillary & the Dems the focus?????'. Once again political turmoil is haunting Trump at a critical time for his administration, as they look to pass a tax reform bill and await Trump's selection of the next Fed Chair.

It appears that Federal Reserve Governor Jerome Powell is the first choice of President Trump to be the next Chair of the Federal Reserve, according to an unnamed senior official. Powell is a Republican centrist who is likely to continue the Fed's strategy of gradual interest rate hikes but may also be open to easing some regulations on banks. Powell, 64, has consistently backed Janet Yellen's plan to hike rates slowly to head off a potential surge in inflation without disrupting an economic recovery that remains in a fragile state. An unnamed senior administration commented that 'Trump hasn't made a final decision and could change his mind' and also commented that 'an announcement is scheduled for Thursday'.

EURUSD is trading around 1.1635 in early Tuesday trading.

USDJPY is relatively flat, trading around 113.12.

GBPUSD currently trades around 1.3210.

Gold is little changed in early trading at around $1,276.50.

WTI is 0.15 lower at around $54.12 in early trading.

Major data releases for today:

At 06:30 GMT, Bank of Japan Governor Kuroda will give a press conference to the markets regarding monetary policy. He will comment on the factors that affected the most recent interest rate decision, the overall economic outlook, inflation, and clues regarding future monetary policy in Japan.

At 10:00 GMT, Eurostat will release a host of Eurozone Data: GDP (YoY & QoQ) for Q3, CPI & CPI Core (YoY) for October and the Unemployment Rate for September. Unemployment is forecast to have dropped to 9.0% from August's 9.1%. CPI-Core is expected to come in at 1.2% slightly lower than the previous release of 1.3% with CPI forecast at 1.4% from 1.5%. Annualized GDP is forecast to come in slightly higher at 2.4% from the previous release of 2.3%. The quarterly GDP is expected to come in at 0.5%, slightly lower than the previous release of 0.6%. The markets will be looking for any significant deviation from the forecasts which will likely cause EUR volatility.

At 19:30 GMT, Bank of Canada Governor Poloz is scheduled to appear before the House of Commons Standing Committee on Finance in Ottawa. He will be accompanied by Senior Deputy Governor Carolyn A. Wilkins.

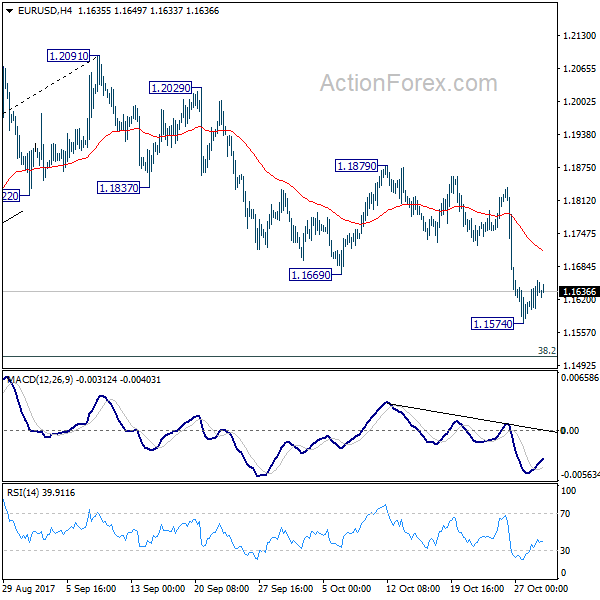

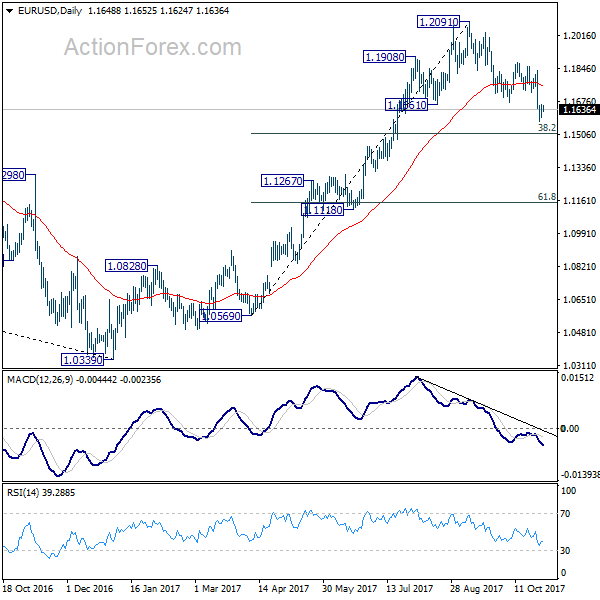

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1610; (P) 1.1634 (R1) 1.1675; More...

A temporary low is in place at 1.1574 and intraday bias in EUR/USD is turned neutral first. Some consolidations could be seen. But still, break of 1.1879 resistance is needed to confirm completion of the decline from 1.2091. Otherwise, near term outlook will stay bearish. Below 1.1574 will target 38.2% retracement of 1.0569 to 1.2091 at 1.1510.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be cautious on 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

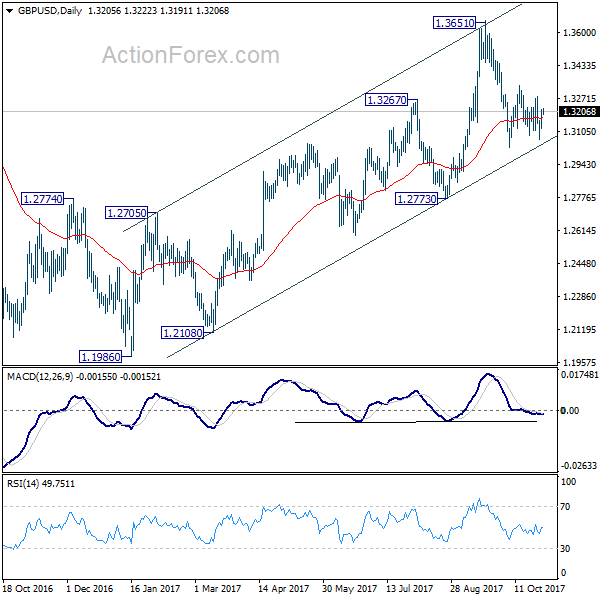

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3140; (P) 1.3177; (R1) 1.3243; More....

No change in GBP/USD's outlook as it's still bounded in range of 1.3026/3337. Intraday bias remains neutral for the moment. On the downside, firm break of 1.3026 support will resume the decline from 1.3651 and target 1.2773 key support level. This will also revive the case of medium term reversal. On the upside, in case of another rally, upside should be limited by 61.8% retracement of 1.3651 to 1.3026 at 1.3412 to bring fall resumption finally.

In the bigger picture, while the medium term rebound from 1.1946 was strong, GBP/USD hit strong resistance from the long term falling trend line. Outlook is turned a bit mixed and we'll stay neutral first. On the downside, decisive break of 1.2773 key support will argue that rebound from 1.1946 has completed. The corrective structure of rise from 1.1946 to 1.3651 will in turn suggest that long term down trend is now completed. Break of 1.1946 low should then be seen. On the upside, break of 1.3835 support turned resistance will revive the case of trend reversal and target 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466 .

Daily Wave Analysis: EUR/USD Builds Bear Flag Within Wave 4 Correction

Currency pair EUR/USD

The EUR/USD has retraced to the 38.2% Fibonacci level of wave 4 (blue) which could be a resistance zone. A break below the bear flag (green) could indicate the continuation of the wave 5 (blue) within a larger wave C (purple).

The EUR/USD is showing strong bearish momentum and has most likely completed a wave 3 (blue). An ABC (green) seems to have been completed within the wave 4 (blue) if price breaks below the channel (green).

Currency pair GBP/USD

The GBP/USD break below the support line (blue) would confirm a bearish continuation. For the moment price remains choppy but a wave 5 could occur if price does not break above resistance (red).

The GBP/USD is showing strong bullish momentum but the wave structure could change when a clear higher low is visible or when price breaks above resistance (red).

Currency pair USD/JPY

The USD/JPY has broken below the support trend lines (dotted) after reaching the main target zone at 114.50-115. This bearish break could start a wave 2 or B (light purple).

The USD/JPY has retraced to the 38.2% Fibonacci level of wave 4 (green) and is building a bearish channel lower.

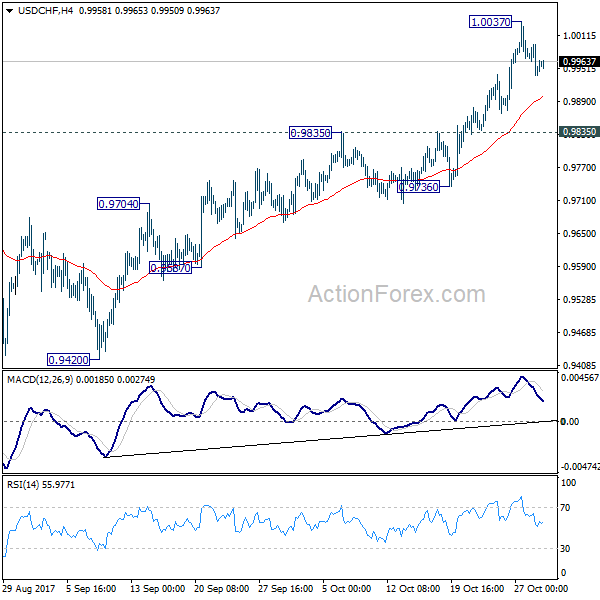

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9922; (P) 0.9959; (R1) 0.9980; More....

Intraday bias in USD/CHF remains neutral as consolidation from 1.0037 temporary top is still unfolding. Deeper retreat could be seen. But downside should be contained above 0.9835 resistance turned support and bring rally resumption. Since 61.8% retracement of 1.0342 to 0.9420 at 0.9990 is already met, break of 1.0037 will turn bias to the upside for 1.0342 key resistance next.

In the bigger picture, current development suggests that USD/CHF has defended 0.9443 (2016 low) key support level again. Rise from 0.9420 could is a medium term up move and should target a test on 1.0342 high. This represents the upper end of a long term range that started back in 2015. On the downside, break of 0.9736 support is now needed to indicate completion of the rise from 0.9420. Otherwise, further rally will remain in favor in medium term.

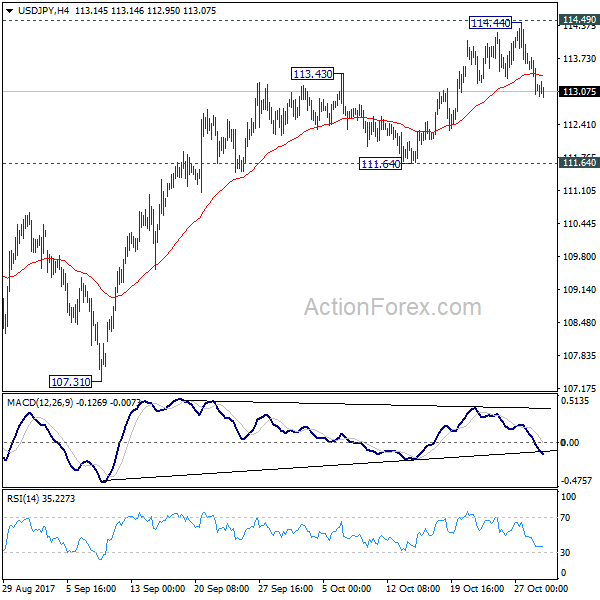

USD/JPY Daily Outlook

Daily Pivots: (S1) 113.39; (P) 113.91; (R1) 114.20; More...

USD/JPY's pull back from 114.44 is still in progress and could dip further lower. But still, outlook will stays cautiously bullish as long as 111.64 support holds. Decisive break of 114.49 key resistance will confirm that correction pattern from 118.65 has completed at 107.31 already. And USD/JPY should then target a test on 118.65. However, sustained break of 111.64 will argue that rebound from 107.31 has completed and bring retest of this low.

In the bigger picture, medium term rise from 98.97 (2016 low) is not completed yet. It should resume after corrective fall from 118.65 completes. Break of 114.49 resistance will likely resume the rise to 61.8% projection of 98.97 to 118.65 from 107.31 at 119.47 first. Firm break there will pave the way to 100% projection at 126.99. This will be the key level to decide whether long term up trend is resuming.

Yen Firm after BoJ Stands Pat, Lowers Inflation Projections

The Japanese Yen traders mildly firmer this week and maintains gains after BoJ stands pat and lowers inflation forecast. Risk appetite recedes as traders are preparing for big events like BoE and NFP later in the week. Also, markets could be a bit disappointed by news that US will adopt a phased approach in the tax cuts. Meanwhile, disappointing Germany inflation is weighing down global yield slightly, and bond traders turned a bit more cautious ahead of Eurozone CPI today. Meanwhile, Sterling remains firm as markets await BoE rate hike. Aussie, Kiwi, Euro ad Swiss Franc are the softer ones.

BoJ stands left, lowers inflation forecast

BoJ left monetary policy unchanged today as widely expected. Short term interest rate was held at -0.1%. The target for 10 year JGB yield was also kept at 0%. The decision was made by 8-1 vote. New comer Goushi Kataoka dissented and urged that "if there were a delay in the timing of achieving the price target due to domestic factors, the BOJ should take additional easing measures." Kataoka also proposed that BoJ should also target to keep 15 year yield at "less than 0.2%", comparing to market pricing at 0.307%.

Meanwhile, BOJ lowered inflation forecast but slightly raised growth forecast:

- For fiscal 2017, core inflation is projected to be at 0.8%, down from prior forecast at 1.1%

- For fiscal 2018, core inflation is projected to be at 1.4%, down from prior forecast at 1.5%

- For fiscal 2019, core inflation is projected to be at 1.8%, unchanged.

- For fiscal 2017, GDP is projected to be at 1.9%, down from prior forecast at 1.8%

- For fiscal 2018, GDP is projected to be at 1.4%, unchanged

- For fiscal 2019, GDP is projected to be at 0.7%, unchanged.

Also released from Japan, household spending dropped -0.3% yoy in September versus expectation of 0.7% yoy. Industrial production dropped -1.1% mom versus expectation of -1.6% mom. Housing starts dropped -2.9% yoy versus expectation of -2.9% yoy.

Trump to nominate Powell on Thursday

It's reported that US President Donald Trump will announce, on Thursday, to nominate current Fed Governor Jerome Powell to succeed Janet Yellen as Fed chair after next February. Comparing to another front runner Stanford economist John Taylor, Powell is generally seen as a safer pick for his experience with monetary policies and Fed. Besides, he is seen as some as a diplomat with good relationship with others. Also, it's well known that Treasury Secretary Steven Mnuchin supports Powell. While Powell shared Yellen's concern on slowdown in inflation this year, he is generally seen as a less dovish one and could speed up Fed's tightening pace.

US tax cuts could be gradual and phased in

Staying in the US, ahead of the released of a drafted tax bill on Wednesday, there are reports suggesting that the Ways and Means Panel is considering a phased approach to cut the corporate tax rate from 35% in 2018 to 20% by 2022. Treasury Secretary Steven Mnuchin suggested that "the objective is not to have that phase in". Yet he did not deny any possibility. While the bill is not finalized, the market is already disappointed by the possibility of the "gradual" approach of the corporate tax cut. The sentiment was also weighed down by the formal charging of former Trump campaign manager Paul Manafort, together with two others, of accepting payments from Ukrainian political leaders and parties. The money was then laundered back into the US. This has raised concerns that the scandal would not delay the tax reform debate in the Congress.

China PMIs disappoint

The official China manufacturing PMI dropped to 51.6 in October, down from 52.4 and missed expectation of 52.1. Non-manufacturing PMI dropped to 54.3, down from 55.4. Overall, the data suggests that China's growth is on track to meet the government's target of 6.5% this year. Mild slowdown in manufacturing activity is seen as partly due to tighter environmental supervision, in particular in the north-eastern regions. While the stricter regulations will dampen growth in manufacturing sector, the overall impact should be negligible in the near term.

Elsewhere, New Zealand building permits dropped -2.3% mom in September. UK Gfk consumer confidence dropped to -10 in October.

Looking ahead

Eurozone data will be the key to focus in European session. Q3 GDP is expected to grow 0.5% qoq. The closely watched CPI is expected to be unchanged at 1.50% yoy in October. Core CPI is expected to be unchanged at 1.1% yoy. There is some risk for a downside surprise in consumer inflation data. And Euro could be weighed down by a miss there. Eurozone unemployment rate is expected to drop 0.1% to 9.0% in September.

Later in the data, Canada GDP, IPPI and RPMI are featured. US will release employment cost index, S&P Case-Shiller house price, Chicago PMI and Conference Board consumer confidence.

USD/JPY Daily Outlook

Daily Pivots: (S1) 113.39; (P) 113.91; (R1) 114.20; More...

USD/JPY's pull back from 114.44 is still in progress and could dip further lower. But still, outlook will stays cautiously bullish as long as 111.64 support holds. Decisive break of 114.49 key resistance will confirm that correction pattern from 118.65 has completed at 107.31 already. And USD/JPY should then target a test on 118.65. However, sustained break of 111.64 will argue that rebound from 107.31 has completed and bring retest of this low.

In the bigger picture, medium term rise from 98.97 (2016 low) is not completed yet. It should resume after corrective fall from 118.65 completes. Break of 114.49 resistance will likely resume the rise to 61.8% projection of 98.97 to 118.65 from 107.31 at 119.47 first. Firm break there will pave the way to 100% projection at 126.99. This will be the key level to decide whether long term up trend is resuming.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Building Permits M/M Sep | -2.30% | 10.20% | 5.90% | |

| 23:30 | JPY | Unemployment Rate Sep | 2.80% | 2.80% | 2.80% | |

| 23:30 | JPY | Household Spending Y/Y Sep | -0.30% | 0.70% | 0.60% | |

| 23:50 | JPY | Industrial Production M/M Sep P | -1.10% | -1.60% | 2.00% | |

| 0:01 | GBP | GfK Consumer Confidence Oct | -10 | -10 | -9 | |

| 1:00 | CNY | Manufacturing PMI Oct | 51.6 | 52.1 | 52.4 | |

| 1:00 | CNY | Non-manufacturing PMI Oct | 54.3 | 55.4 | ||

| 3:05 | JPY | BoJ Policy Balance Rate | -0.10% | -0.10% | -0.10% | |

| 5:00 | JPY | Housing Starts Y/Y Sep | -2.90% | -3.20% | -2.00% | |

| 6:30 | EUR | French GDP Q/Q Q3 A | 0.5% | 0.50% | 0.50% | |

| 6:30 | EUR | French GDP Y/Y Q3 A | 2.2% | 2.10% | 1.80% | |

| 10:00 | EUR | Eurozone Unemployment Rate Sep | 9.00% | 9.10% | ||

| 10:00 | EUR | Eurozone GDP Q/Q Q3 A | 0.50% | 0.60% | ||

| 10:00 | EUR | Eurozone CPI Estimate Y/Y Oct | 1.50% | 1.50% | ||

| 10:00 | EUR | Eurozone CPI Core Y/Y Oct A | 1.10% | 1.10% | ||

| 12:30 | CAD | GDP M/M Aug | 0.10% | 0.00% | ||

| 12:30 | CAD | Industrial Product Price M/M Sep | 0.50% | 0.30% | ||

| 12:30 | CAD | Raw Materials Price Index M/M Sep | 0.40% | 1.00% | ||

| 12:30 | USD | Employment Cost Index Q3 | 0.70% | 0.50% | ||

| 13:00 | USD | S&P/CS Composite-20 Y/Y Aug | 5.90% | 5.80% | ||

| 13:45 | USD | Chicago PMI Oct | 60 | 65.2 | ||

| 14:00 | USD | Consumer Confidence Oct | 121 | 119.8 |

Australia’s New Home Sales Declined In September

For the 24 hours to 23:00 GMT, the AUD rose 0.20% against the USD and closed at 0.7689.

LME Copper prices declined 0.1% or $8.5/MT to $6823.0/MT. Aluminium prices rose 1.1% or $24.0/MT to $2143.0/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7676, with the AUD trading 0.17% lower from yesterday's close.

Data revealed that Australia's HIA new home sales plunged 6.1% in September, due to a large decline in apartment purchases. In the previous month, the HIA new home sales had recorded a 9.1% jump. Additionally, Australian private sector credit growth slowed in September, after it rose 0.3% MoM from a rise of 0.5% in August.

Earlier today, in China, Australia's largest trading partner, the NBS manufacturing PMI dropped to 51.6 in October, compared to market expectations of a fall to 52.0. The manufacturing PMI had recorded a level of 52.4 in the previous month. Moreover, the nation's non-manufacturing PMI eased to a level of 54.3 in October from a reading of 55.4 in the last month.

The pair is expected to find support at 0.7655, and a fall through could take it to the next support level of 0.7634. The pair is expected to find its first resistance at 0.7698, and a rise through could take it to the next resistance level of 0.7720.

Investors will now look forward to Australia's AiG performance of manufacturing index for October, scheduled to be released overnight.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Eurozone Economic Confidence Soared To Almost 17-Year High Level In October

For the 24 hours to 23:00 GMT, the EUR rose 0.30% against the USD and closed at 1.1644, following better than expected Eurozone data.

On the macro front, economic confidence across the Eurozone climbed to its highest level since January 2001 in October, as it rose to 114.0 from a revised level of 113.1 reported in the previous month, suggesting that the region has shown some solid economic recovery following a decade-long economic and financial crisis. Markets had envisaged the economic confidence index to advance to 113.3. Moreover, the region’s business climate index rose more than expected to 1.44 in October, from 1.34 in September, registering its highest level since March 2011. Meanwhile, Eurozone’s final consumer confidence index advanced to -1.0 in October, in line with market expectations. In the previous month, the consumer confidence index had recorded a level of -1.2. The preliminary figures had also indicated an advance to -1.0.

In Germany, the powerhouse economy of the Eurozone, retail sales rebounded by 0.5% on a monthly basis in September, matching the forecast. Retail sales had fallen by a revised 0.2% in the previous month. Separately, Germany’s inflation eased more than expected to 1.6% YoY in October, following a rate of 1.8% in September.

In the US, consumer spending recorded a rise of 1.0% in September, more than market expectations for an advance of 0.9%. In the prior month, personal spending had risen 0.1%. Also, US personal income rose 0.4% in September, in line with market estimates. Additionally, the Dallas Fed manufacturing business index unexpectedly climbed to a level of 27.6, compared to a level of 21.3 in the prior month. Markets were anticipating the Dallas Fed manufacturing business index to ease to 21.0.

Meanwhile, a report stated that US President, Donald Trump, is likely to pick Federal Reserve (Fed) Governor, Jerome Powell, as the next Chair of the US Fed and an announcement about the same would be made by Trump on Thursday.

In the Asian session, at GMT0400, the pair is trading at 1.1635, with the EUR trading 0.08% lower from yesterday’s close.

The pair is expected to find support at 1.1605, and a fall through could take it to the next support level of 1.1576. The pair is expected to find its first resistance at 1.1661, and a rise through could take it to the next resistance level of 1.1688.

Moving ahead, traders will closely asses the Eurozone GDP data for the third quarter along with the region’s consumer prices for October, both due to release today. Additionally, in the US, the consumer confidence index and Chicago PMI data, both for October, along with the home price index for August, will be on investors’ radar.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.