Sample Category Title

Market Morning Briefing: Keep On Eye On Possible Big Movement In Dollar-Yen

STOCKS

Global stock indices are all strong and the bulls do not seem to leave the ground just now except Shanghai and Nikkei. Nikkei could be vulnerable to a fall in the coming sessions while Shanghai remains range-bound.

Dow (23348.74, -0.36%) has been stable near current levels for the last 3-4 sessions. 23250-23500 region holds for now with a possible break on the upside towards 23750 in the medium term.

Dax (13229.57, +0.09%) was almost stable yesterday and there is scope of a rise towards 13300-13500 in the coming sessions. Near to medium term looks bullish.

21700 is the immediate support on the Nikkei (21991.16, -0.08%) but the index is likely to come below 21700-21600 levels in the medium term. The fall in Dollar Yen has from 114.50 levels could be indicative of a fall in Nikkei going forward. In that case a test of 22666 on the upside for Nikkei is doubtful.

Shanghai (3380.51, -0.29%) is trading well within the 3360-3425 region and this range could hold for some sessions in the near term. A re-test of 3350 looks likely.

Nifty (10363.65, +0.39%) is trying to reach towards 10400, attempting a break above current resistance for the last 3-sessions. A break above 10400, if seen could open up chances of 10500-10600 in the near term; else a sharp correction from 10400 could be expected towards 10250.

COMMODITIES

Gold (1275.74) has immediate support zone of 1260-1240 which is likely to hold in the near term. Some stable movement with a possible downside extension is possible in early November followed by a bounce back towards 1300 levels. A break below 1240, if seen could turn very bearish for the coming weeks.

Silver (16.81) is almost stable and could trade within 16.50-17.00 region for the next few sessions.

Brent (60.83) has almost moved up to our initial target of 61 and it would be crucial to see if the price comes off from there or breaks higher to make fresh highs in the current rally, heading towards 63. A rejection is expected either from 61 just now or from higher levels near 63. Near term looks bullish.

WTI (54.07) is also quiet and could possibly attempt a rise towards 55-56 levels in the near to medium term before coming off from there.

Copper (3.1035) could come off to test immediate support near 3.05 which is likely to hold in the first testing, producing a bounce to 3.15/20 again.

FOREX

Keep on eye on possible big movement in Dollar-Yen.

As warned, Dollar-Yen (113.08) has come down to a low of 112.97, dragging the Euro-Yen (131.59) lower with it even as the Euro (1.1636) recovered a bit.

The dip in Dollar-Yen possibly confirms the strength of the 114.50-115.00 Resistance and opens up chances of further fall towards 112. A Day Close below 113.00 is needed to confirm. The Euro-Yen too looks like it can dip further to 130 at least.

This suggests the Euro will be subdued around 1.16. We have a Bear SHS target near 1.15.

As expected, the Pound (1.3203) is trading sideways between 1.3040-3300 and can move to the upper end of the range. The Aussie (0.7675) rose to almost 0.7700 yesterday. It has Support at 0.7630-20 and might try to move up further while that holds.

Dollar-Yuan (6.6317) has dipped a bit from yesterday's 6.6438. Dollar-Rupee (64.8550) has dipped to 64.80 yesterday. Need to see if it continues to hold above 64.70 today or not.

INTEREST RATES

There's been a sharp dip in US yields (5Yr 1.99%, 10Yr 2.36% and 30Yr 2.87%) compared to 2.04%, 2.43% and 2.94% respectively. This is a bit of a surprise ahead of tomorrow's FOMC meeting even as the US PCE moved up to +1.14% (y/y) yesterday.

As expected, however, the US yield curve has flattened again a bit, with the 30-5 (0.88%) coming down from 0.91%.

The US-Japan 10Yr Spread (2.30%) has seen dip from levels near 2.38% last week. A break below 2.30%, if seen, could be bearish for Dollar-Yen. This is to be kept an eye on.

Trade Idea: GBP/JPY – Hold short entered at 150.00

GBP/JPY - 149.40

Original strategy:

Sold at 150.00, Target: 148.00, Stop: 150.60

Position: - Short at 150.00

Target: - 148.00

Stop: - 150.60

New strategy :

Hold short entered at 150.00, Target: 148.00, Stop: 150.60

Position: - Short at 150.00

Target: - 148.00

Stop:- 150.60

Although sterling rebounded yesterday to 150.00, the British pound did meet renewed selling interest there and has retreated, adding credence to our bearish view (we recommended to sell at 150.00 and a short position was entered) that the rebound from 146.95 has ended at 151.40 last week, hence consolidation with downside bias remains for weakness to 148.50, then 148.00, however, break of support at 147.80 is needed to retain bearishness and signal another leg of decline from 152.85 top is underway for further fall towards said support at 146.95.

In view of this, we are holding on to our short position entered at 150.00. Above 150.50-60 would prolong consolidation and bring rebound to 151.00 but said resistance at 151.40 should hold. Only a break of this resistance would revive bullishness and extend the rebound from 146.95 towards 151.90-00 first.

Our preferred count is that larger degree wave V with circle is unfolding from 251.12 with wave (I) 219.34, (II): 241.38 and wave (III) is subdivided into 1: 192.60, 2: 215.89 (23 Jul 2008) and wave 3 ended at 118.87 earlier in 2009. The correction from there to 162.60 is wave 4 which itself is a double three and is labeled as first a-b-c ended at 151.53, followed by wave x at 139.03, 2nd a ended at 162.60, 2nd b at 146.75 and 2nd c leg of wave 4 ended at 163.00. Therefore, the decline from 163.00 to 116.85 is now treated as wave 5 which also marked the end of larger degree wave (III), hence wave (IV) major correction has commenced for retracement of the wave (III) from 241.38 and upside target at 183.95-00 (50% Fibonacci retracement of the wave (II) from 241.38) had been met, a drop below 160.00 would suggest wave (IV) has ended at 195.85, bring decline in wave (V) for initial weakness to 130 (already met) and 120.

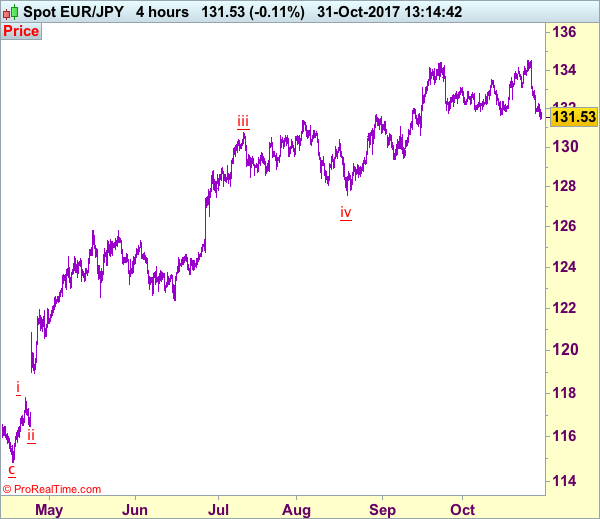

Trade Idea: EUR/JPY – Sell at 132.70

EUR/JPY - 131.55

Original strategy:

Sell at 132.70, Target: 130.70, Stop: 133.30

Position: -

Target: -

Stop: -

New strategy :

Sell at 132.70, Target: 130.70, Stop: 133.30

Position: -

Target: -

Stop:-

As the single currency has remained under pressure after dropping sharply from 134.50 and the breach of previous support at 131.66 adds credence to our view that top has been formed there, hence consolidation with downside bias remains for a correction of early upmove to 131.00, then towards 130.50-60, however, near term oversold condition should limit downside to psychological level at 130.00, bring rebound later.

In view of this, we are still looking to sell euro on recovery as 132.70-80 should limit upside and bring another decline later. Above 133.10 would defer and suggest first leg of corrective decline from 134.50 top has ended, risk a stronger rebound to 133.50-60 but still reckon upside would be limited to 133.95-00, price should falter well below said last week’s high at 134.50, bring another selloff later.

Our latest preferred count is that wave (ii) is ABC-X-ABC which ended at 123.33 and wave (iii) is unfolding with wave iii ended at 100.77, followed by wave iv at 111.57 and wave v as well as the wave (iii) has ended at 97.04, followed by wave (iv) at 111.43 and wave (v) has ended at 94.12 which is also the end of the larger degree v, this also implied the major wave (C) has also ended there, hence major correction has commenced from there with (A) leg unfolding in its lower degree wave c which has possibly ended at 145.69. Under this count, A-B-C wave (B) has commenced with A leg ended at 136.23, wave B at 143.79 and wave C has possibly ended at 149.79.

Our larger degree count is that the decline from 139.26 is wave (C) and is sub-divided into a diagonal triangle i-ii-iii-iv-v with wave i - 105.44, wave ii- 123.33, wave iii - 97.03, wave iv - 111.43, followed by the final wave v as well as the end of wave (C) at 94.12, this also mark the bottom of larger degree wave B. Under this count, major rise in wave C has commenced as an impulsive wave with minor wave III ended at 145.69, wave V is still in progress for further gain to 150.00. Having said that, this so-called wave V could well be the first leg of larger degree 5-waver wave C and this wave C should bring at least a retest of wave A top at 169.97 (July 2008).

Trade Idea: AUD/USD – Sell at 0.7720

AUD/USD – 0.7675

Original strategy:

Sell at 0.7720, Target: 0.7550, Stop: 0.7780

Position: -

Target: -

Stop:-

New strategy :

Sell at 0.7720, Target: 0.7550, Stop: 0.7780

Position: -

Target: -

Stop:-

Aussie’s recovery after finding support at 0.7625 late last week suggests consolidation above this level would be seen and corrective bounce to 0.7700 cannot be ruled out, however, reckon 0.7720-25 would limit upside and bring another decline later, below said support would add credence to our view that recent decline from 0.8125 top is still in progress and may extend further weakness to 0.7600, having said that, loss of downward momentum should prevent sharp fall below 0.7550 and reckon 0.7500 would hold from here, bring rebound later.

In view of this, we are looking to reinstate short on recovery as 0.7720-25 should limit upside and bring another decline. Above previous support at 0.7770 would defer and suggest a temporary low is possibly formed, bring rebound to 0.7800 and then towards 0.7825-35 later.

On the 4-hour chart, recent upmove from 0.7329 is unfolding as an impulsive rise with wave 3 as well as smaller degree wave (iii) extending, only minor wave v of (iii) has ended at 0.8125, hence bullishness remains for this move to extend headway to 0.8200, then towards 0.8300, however, reckon upside would be limited to 0.8400 and the final wave 5 should falter below 0.8500, bring correction later.

Elliott Wave View: DAX Short-Term

DAX shows a 5 swing Elliott Wave bullish sequence from 8/29 low, suggesting further upside is likely. The rally from 8/29 low is unfolding as a double three Elliott Wave structure where Intermediate wave (W) ended at 13089 and Intermediate wave (X) ended at 12903. The rally from 12903 low appears to be unfolding as an impulse where Minute wave ((i)) ended at 13066, Minute wave ((ii)) ended at 12906.5, and Minute wave ((iii)) ended at 13249.5. Near term, while pullbacks stay above 12903 low, expect Index to extend higher. We don’t like selling the Index.

DAX 1 Hour Elliott Wave Analysis

Double three ( 7 swings) is the most important pattern in Elliott wave’s new theory. It is also probably the most common pattern in the market these days. Double three is also known as a 7-swing structure. It is a very reliable pattern that gives traders a good opportunity to trade with a well-defined level of risk and target areas. The image below shows what Elliott Wave Double Three looks like. It has labels (W), (X), (Y) and an internal structure of 3-3-3. This means that all 3 legs has corrective sequences. Each (W) and (Y) is formed by 3 wave oscillations and has a structure of A, B, C or W, X, Y of smaller degrees.

OIL Drives Into Resistance

I don't know about where you are, but the cheap petrol cycles seem to be getting shorter here in Sydney. Taking a look at the price of oil pushing up against higher time frame resistance, it's not hard to see why.

Take a look at the weekly chart for an overview on why this level is so important:

OIL Weekly:

As you can see, price has had multiple touches in the past and has now come back up to test the level again.

Stepping down one more level, but staying higher time frame with a look at the daily, you can see where price is at more clearly:

OIL Daily:

Something else to start to take notice of is the fact that the latest daily candle is an indecision candle which could be signalling a pending reversal in the near term.

As always, if higher time frame resistance holds, then we'll zoom into the intraday charts and look for any short term rallies to short into.

Uncertainty And Anxiety

Uncertainty and Anxiety

No coronation for the US dollar just yet as investors spent a significant part of Monday analysing the latest edition of Fear and Loathing in Washington. To say that confusion reigned would be an understatement as waves of jittery headlines more than sullied investor sentiment. Special Prosecutor Mueller’s recent arrests reminded us that some stories just never go away while the journey down the yellow brick road to tax reform is still fraught with peril. And rounding out the headlines, Jerome Powell remains the odds-on favourite. The mash-up of all three headlines sent equities, yields, and USDJPY lower.

The Greenback was always the first player this week given the massive US economic data diary.But even without getting sideswiped by risk-averse headline there was an increasing air of reluctance to chase the dollar higher given that long dollar positions were a bit overextended. But even traders who like the USD story were playing the patience game given the plethora of economic data releases this week and are looking to buy the dollars at better levels.

The scope of Special Prosecutor Mueller’s investigation will likely widen. But at this stage, we have no idea if there’s a smoking gun or its all a tempest in a teapot.Regardless, look for this inquisition to remain in the headlines for the foreseeable future.

Tax reform took another detour after Bloomberg reported that “the House is said to be discussing phase-in of the corporate tax cut” implying no one-off haircut but instead it’s to adjust gradually.

Powell is 75-80 % priced in so we should only expect a more significant USD knee-jerk if Trump pulls a rabbit out of the hat.

The Japanese Yen

The markets spent the more significant part of last week buying USDJPY. But when it struggled to gain momentum after the buoyant 3 Q GDP and then fell victim to the Jerome Powell headlines; it has spent most of its time in recoil since. There remains a lot of events to get through this week including the BoJ, FOMC and of course Friday NFP, and while there remains is a valid argument to move higher, it’s challenging to trade USDJPY continually look over one’s shoulder for headline risk. At the moment the market is still tentatively buying the dip, but a break below 112.75 could lead to a cascade of stop-loss triggers and pricing could get very messy.

One can sense the level of angst and frustration brewing as dollar bulls like it higher, but given the Yen headline risk sensitivity, USDJPY will continue to march to its beat.

The Euro

A willfully dovish ECB suggests the EURO should remain under pressure. The single currency received something of a reprieve from last weeks onslaught as the push for independence in Catalonia has taken several severe blows over the weekend. But the market momentum continues to lean lower

The Australian Dollar

Let’s see what the Aussie bears have to say about the China ban on Australia beef lifted. I suspect they’ll be hungry as the market approaches the .7700 level. But all eyes should remain on the USD side of the calculus with the deluge of economic data, FOMC and new FED chair announcement

In the meantime, the Aussie received a get out of jail card as US bond yields fell and US dollar bull’s retreated at the prospect of Trump Tax cuts getting phased in as opposed to an on-off haircut.

Yen Rises Ahead Of Bank Of Japan

US dollar struggles at start of a busy week

The US dollar is lower against most majors after scoring huge gains last week. Political uncertainty as the FBI investigation on Russian collusion in the Presidential elections as well as Fed Governor Jerome Powell as a lead candidate for the U.S. Federal Reserve Chair position have put downward pressure on the currency ahead of a week that features various central banks, included the Fed and will end with the release of the U.S. non farm payrolls (NFP) on Friday.

The Bank of Japan (BOJ) will release its monetary policy statement near midnight Monday, October 30 EDT to be followed by the central bank's outlook report and a press conference Tuesday, October 31 at 2:30 am EDT. Investors are not expecting a change in rates and the stimulus program, but see room in the economic outlook to introduce downgraded inflation expectations.

The majority win in the Japanese snap elections positions Shinzo Abe's party to continue pushing a loose monetary policy. The Bank of Japan (BOJ) Governor Haruhiko Kuroda was one of the most influential recruits five years ago, and with the electoral win he is thought to have another five year term at the head of the central bank.

The USD/JPY lost 0.43 percent on Monday. The currency pair is trading at 113.15 ahead of the Bank of Japan (BOJ) statement and the press conference hosted by Governor Kuroda. Political stability has been achieved with the victory of the LDP securing another five years in which to fulfill Prime Minister Abe's lofty inflation ambitions.

Earlier today MarketPulse analyst Kenny Fisher pointed out the release of a strong economic indicator in Japan:

On the release front, Japanese Retail Sales posted a strong gain of 2.2%, just shy of the estimate of 2.3%. In the US, Personal Spending gained 1.0%, above the forecast of 0.8%. On Tuesday, the Bank of Japan releases its monetary statement. The US will publish CB Consumer Confidence.

All eyes are on the BoJ, which will release a rate statement on Tuesday. The Bank is expected to hold course with its ultra-accommodative monetary policy, and also maintain its inflation forecasts. Policymakers appear resigned to persistently weak inflation – at the September meeting, the BoJ stated that it did not expect inflation to reach the Bank's 2 percent target until fiscal year 2020. BoJ Governor Haruhiko Kuroda has long insisted that the bank will not taper its stimulus program until inflation moves higher.

Despite weak inflation and wage growth, there has not been much pressure on the Bank to change policy, as the Japanese economy has performed well in 2017. GDP expanded at an annualized 2.5 percent in the second quarter, buoyed by solid numbers from the manufacturing and export sectors. Consumer spending has improved, and retail sales in September improved 2.3%, compared to 1.7% a month earlier. Retail sales have risen for 11 consecutive months, as consumers appear more confident in the economy and have opened their purse strings.

The U.S. Federal Reserve will begin its two day meeting just as the Bank of Japan (BOJ) will have finished theirs. The Fed is also not expected to change the benchmark rate in November, with the market pricing in a almost 99 percent in December. With little data to start the trading the week the USD could not mount a defence against more political uncertainty in Washington. Employment is expected to rebound after the impact of the hurricane season, which could focus the attention of the market back to fundamentals.

Market events to watch this week:

Monday, October 30

Midnight JPY Monetary Policy Statement

Tuesday, October 31

Tentative JPY BOJ Outlook Report

Tentative JPY BOJ Policy Rate

2:30 am JPY BOJ Press Conference

8:30 am CAD GDP m/m

10:00 am USD CB Consumer Confidence

5:45pm NZD Employment Change q/q

Wednesday, November 1

5:30 am GBP Manufacturing PMI

8:15 am USD ADP Non-Farm Employment Change

10:00 am USD ISM Manufacturing PMI

10:30 am USD Crude Oil Inventories

2:00 pm USD FOMC Statement

2:00 pm USD Federal Funds Rate

8:30 pm AUD Trade Balance

Thursday, November 2

5:30 am GBP Construction PMI

8:00 am GBP BOE Inflation Report

8:00 am GBP MPC Official Bank Rate Votes

8:00 am GBP Monetary Policy Summary

8:00 am GBP Official Bank Rate

8:30 am GBP BOE Gov Carney Speaks

8:30 am USD Unemployment Claims

8:30pm AUD Retail Sales m/m

Friday, November 3

5:30 am GBP Services PMI

8:30 am CAD Employment Change

8:30 am CAD Trade Balance

8:30 am CAD Unemployment Rate

8:30 am USD Average Hourly Earnings m/m

8:30 am USD Non-Farm Employment Change

8:30 am USD Unemployment Rate

10:00 am USD ISM Non-Manufacturing PMI

Gold Starts Week With Gains, US Consumer Spending Improves

Gold has ticked higher in the Monday session. In North American trade, the spot price for an ounce of gold is $1275.72, up 0.28% on the day. On the release front, Personal Spending jumped 1.0%, beating the estimate of 0.8%. On Tuesday, the US releases CB Consumer Confidence.

The US consumer is optimistic about the economy, and that confidence has translated into stronger spending. Personal Spending gained 1.0% in September, its sharpest gain since April 2016. The strong reading comes on the heels of Friday’s UoM Consumer Sentiment Report, which hit an all-time high of 100.7 points in September. Another key consumer confidence will be reported on Tuesday, and the markets are expecting more good news. CB Consumer Confidence is forecast to climb to 121.1, up from 119.8 in the previous release. Consumer spending is a key driver of the economy, accounting for two-thirds of economic growth.

The US economy received a high grade on Friday, as Advance GDP for the third quarter posted a gain of 3.0%. This easily beat the forecast of 2.5%, and kept close pace with Final GDP in Q2, which gained 3.1%. The strong reading is welcome news for the Federal Reserve, which is widely expected to raise rates at the December meeting. Employment and consumer data has been strong, with weak inflation the only real fly in the ointment. Fed Chair Janet Yellen and other policymakers have downplayed the significance of low inflation, and the markets have responded by pricing in at December hike at 96%.

Russia Redux But Focus Elsewhere

The front-page news this week might be the Trump-Russia drama but the US dollar will move on the FOMC, Fed chair and tax reform news. The pound was the top performer while the Canadian dollar lagged. Japanese jobless numbers are due later. A new Premium trade has been posted and sent, supported by 3 charts and 4 technical reasons. It will be explained in detail in Tuesday's Premium video.

The indictment of Trump's campaign manager Paul Manafort and another top aide along with a guilty plea from a foreign policy advisor will breathe fresh life into the election story but traders may be wise to ignore it. The playbook earlier this year was to fade any moves on the investigation, especially in stocks markets. That won't change unless the scandal reaches the President or his family. In the meantime, the market has far more direct and near-term news to drive trading.

One story is the Fed chair decision, which will is expected on Thursday. A further leak Monday suggested that Powell is the likely pick and that's probably 70% priced in now. It's part of the reason that 10-year yields fell back below 2.40% to 2.36%.

Another part of the reason is that the corporate tax cut might take years. A report indicated that the plan – which will be released Wednesday – may phase in the drop to a 20% corporate rate over four years. That's still good for corporate USA but not as quick and powerful as hoped.

In turn, the US dollar fell through most of the session. Sterling, in particularly, took advantage in an 80 pip rally. That may also reflect a sense in the GBP market that it can focus on the BOE rather than the endless bad Brexit news.

In the near-term, Asia-Pacific traders will look to Japanese data on jobs at 2330 GMT and industrial production 20 minutes later.