Sample Category Title

Volatility Levels Set to Rise During Week Ahead

The EUR/USD price keeps falling on the background of US dollar strengthening. Data published today in the US on personal spending showed a 1% growth for September against the 0.8% forecast has strengthened the likelihood of more monetary policy tightening in the US. Investors are waiting for the FOMC statement due to be published this Wednesday. Also this week, US President Donald Trump is expected to announce the name of the next Fed chairman. Gerome Powell who is known for his hawkish views on monetary policy is one of the most favoured candidates to become the next governor of the central bank. At the same time, it is still possible that Janet Yellen will remain in her chair. Tomorrow the focus of investors will be on the unemployment rate, consumer price index and preliminary report on GDP growth in the Eurozone.

The USD/JPY is falling despite the strong positions of the greenback. There was little impact on the markets from the news on retail sales in Japan which grew by only 2.2% in September against the 2.3% expected. Traders are likely to be influenced by the data on household spending and unemployment change in Japan due at 23:30 GMT and preliminary industrial production at 23:50 GMT.

The British pound is rising on the background of an expected interest rate increase by the Bank of England on Thursday by 0.25% to 0.50%. Strong housing market data is also supporting the sterling as mortgage approvals came in at 66,000 thousand in September hitting analysts forecast on the mark. Volatility levels are likely to remain high during the week due to the large number of important economic events.

EUR/USD

The EUR/USD price is consolidating near the 1.1620 level. The RSI approached the oversold zone which points to a possible price rebound with potential targets at 1.1650 and 1.1700. In case of the fall continuation, the target levels will be at 1.1550 and 1.1500. The MACD signal line on the 15-minute chart just crossed the zero level and that may stimulate the bears to push the price down further.

GBP/USD

The GBP/USD price is correcting upwards within the limits of the descending channel. Soon the quotes may return to the important 1.3250 level and the upper limit of the channel. The RSI on the 15-minute chart hints at the current rising impulse exhaustion. The volatility is likely to remain high and the next objective in case of a fall will be at 1.3050.

USD/JPY

The USD/JPY price has recently broken the inclined support line. In case of the price breaking through the closest low near 113.30, the fall may accelerate and the closest targets will in this case be at 113.00 and 111.70. Upward correction today is likely to be restrained by the resistance at 114.00. The amplitude of price fluctuations is likely to increase during the week.

Pound Starts Week With Gains, Markets Eye BoE Decision

The British pound has posted gains in the Monday session. In North American trade, GBP/USD is trading at 1.3179, up 0.39% on the day. On the release front, British Net Lending to Individuals came in at GBP 5.5 billion, matching the estimate. In the US, Personal Spending gained 1.0%, above the forecast of 0.8%. On Tuesday, the US will publish CB Consumer Confidence.

British consumer spending took a hit in October, according to last week's British CBI Realized Sales report. The soft reading, which was the sharpest drop since March 2009, was all the more surprising because the September reading showed a strong gain of 42 points. High inflation is likely having a chilling effect on consumer spending, a key driver of economic growth. The BoE will be taking note of the sharp drop in retail sales, as the Bank must decide at its policy meeting on Thursday whether to raise rates for the first time in a decade. Policymakers remain divided over a rate hike, which would be the first in a decade. Proponents of a rate increase point to inflation running at 3.0%, above the Bank's target of 2.0%, but opponents argue that the economy is showing signs of weakness and a rate hike could hamper economic growth.

The week ended on a positive note in the US, as Advance GDP in third quarter jumped 3.0%, well above the estimate of 2.5%. The economy was boosted by strong consumer spending and business investment, as well as a strong export sector. The economy could have done even better in Q3, but hurricanes which hit Texas, Florida and Puerto Rico caused widespread damage. Consumer confidence remains strong, as Revised UoM Consumer Sentiment soared to 100.7 points in September, compared to 95.1 a month earlier. On Tuesday, CB Consumer Confidence is expected at 121.1 points.

NZDUSD Looking Bearish in the Short- and Medium-Term

NZDUSD has declined considerably in recent weeks, falling to a five-and-a-half-month low of 0.6817 during Friday's trading.

The Tenkan-sen line being below the Kijun-sen line is a negative alignment pointing to bearish momentum in the short-term. Adding to this, both lines maintain a fairly steep negative slope.

Should the pair continue declining, the area around Friday's low of 0.6817 could act as support. Notice that the area around this level also encapsulates the May 11 seventeen-month low (which is only marginally below last week's low).

If NZDUSD reverses course and heads higher, the range around 0.69 might provide resistance – 0.69 being a potential psychological level.

The medium-term picture based on movement over the last five months is looking bearish with the overall trend throughout this period being negative. In addition, the pair has been recording lower lows and lower highs ever since reaching a twenty-nine-and-a-half-month high of 0.7558 on July 27. Furthermore, NZDUSD is trading below the Ichimoku cloud as well as below the 50- and 100-day SMAs (simple moving averages) with the two recording a bearish cross earlier in October when the 50-day SMA moved below the 100-day one.

Overall, the pair is looking bearish in both the short- and medium-term.

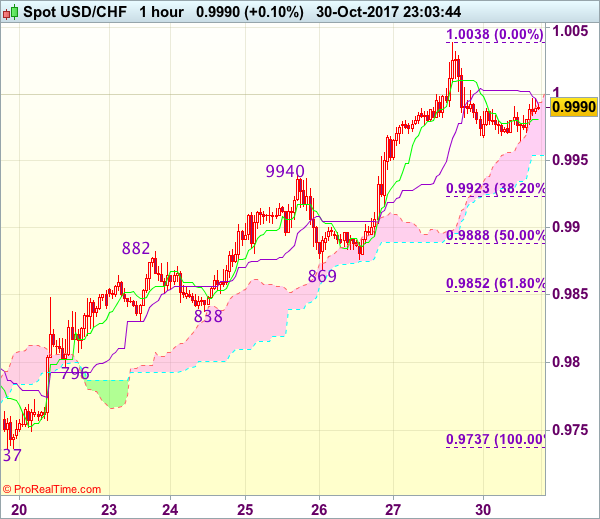

Trade Idea Wrap-up: USD/CHF – Buy at 0.9920

USD/CHF - 0.9972

Most recent candlesticks pattern : N/A

Trend : Up

Tenkan-Sen level : 0.9981

Kijun-Sen level : 0.9992

Ichimoku cloud top : 0.9994

Ichimoku cloud bottom : 0.9954

Original strategy :

Buy at 0.9920, Target: 1.0030, Stop: 0.9885

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9920, Target: 1.0030, Stop: 0.9885

Position : -

Target : -

Stop : -

Dollar’s retreat after rising to 1.0038 on Friday has retained our view that minor consolidation below this level would be seen and pullback to previous resistance at 0.9940 cannot be ruled out, however, reckon 0.9920-25 (38.2% Fibonacci retracement of 0.9737-1.0038) would limit downside and bring another rise, above said resistance at 1.0038 would extend recent rise from 0.9421 low to 1.0050-55, having said that, overbought condition should limit upside to 1.0075-80 and price should falter below 1.0100 resistance and bring retreat later.

In view of this, we are looking to buy dollar again on pullback as 0.9920-25 should limit downside, bring another rise later. Below 0.9885-90 (50% Fibonacci retracement of 0.9737-1.0038) would defer and suggest top is possibly formed, risk test of support at 0.9869.

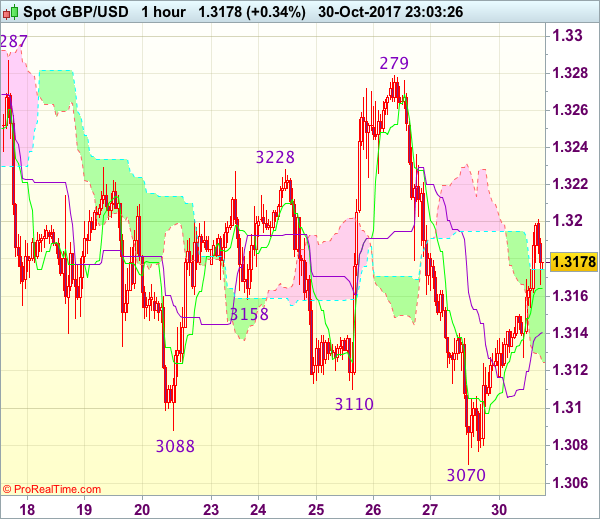

Trade Idea Wrap-up: GBP/USD – Sell at 1.3255

GBP/USD - 1.3189

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.3164

Kijun-Sen level : 1.3141

Ichimoku cloud top : 1.3175

Ichimoku cloud bottom : 1.3125

Original strategy :

Sell at 1.3225, Target: 1.3125, Stop: 1.3260

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.3255, Target: 1.3135, Stop: 1.3290

Position : -

Target : -

Stop : -

As cable found support at 1.3070 on Friday and has rebounded, suggesting consolidation above this level would be seen and corrective bounce to 1.3200, then 1.3220-25 cannot be ruled out, however, still reckon upside would be limited to 1.3255-60 and bring another decline later, below 1.3100 would bring test of said support at 1.3070, break there would extend the erratic decline from 1.3338 to 1.3050, then towards recent low at 1.3027.

In view of this, we are looking to sell cable on further subsequent recovery as 1.3255-60 should limit upside. Only above indicated strong resistance at 1.3279-87 would abort and shift risk to the upside for the erratic rise from 1.3027 low is still in progress for further gain to 1.3300-10, then towards 1.3340-50.

Trade Idea Wrap-up: EUR/USD – Sell at 1.1700

EUR/USD - 1.1625

Most recent candlesticks pattern : N/A

Trend : Down

Tenkan-Sen level : 1.1622

Kijun-Sen level : 1.1608

Ichimoku cloud top : 1.1708

Ichimoku cloud bottom : 1.1647

Original strategy :

Sell at 1.1685, Target: 1.1585, Stop: 1.1720

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.1685, Target: 1.1585, Stop: 1.1720

Position : -

Target : -

Stop : -

As the single currency recovered after falling to 1.1574 on Friday, suggesting consolidation above this level would be seen and corrective bounce to 1.1645-50 cannot be ruled out, however, reckon upside would be limited to the upper Kumo (now at 1.1708) and bring another decline later, below said support at 1.1574 would extend recent decline from 1.2093 top to 1.1550-55 but loss of downward momentum should prevent sharp fall below 1.1520-25 and reckon 1.1500 would hold from here.

In view of this, we are looking to sell euro on subsequent recovery as the upper Kumo (now at 1.1700) should limit upside and bring another decline. Only above previous support at 1.1725 (now resistance) would signal low is formed instead, bring retracement of recent decline to 1.1750-55 first.

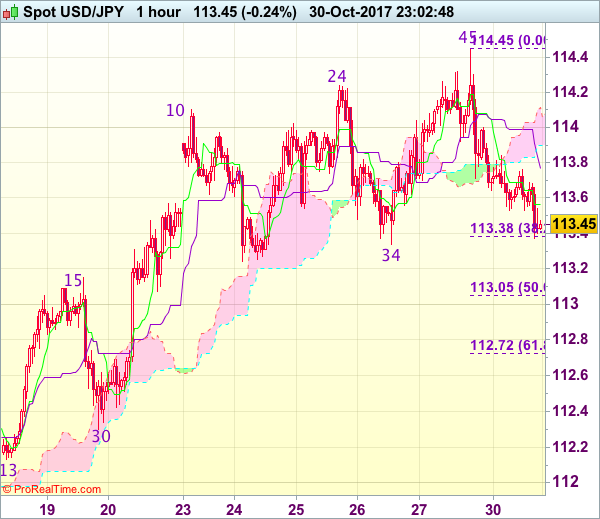

Trade Idea Wrap-up: USD/JPY – Sell at 114.20

USD/JPY - 113.44

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 113.57

Kijun-Sen level : 113.77

Ichimoku cloud top : 114.11

Ichimoku cloud bottom : 113.90

Original strategy :

Sell at 114.20, Target: 113.20, Stop: 114.55

Position : -

Target : -

Stop : -

New strategy :

Sell at 114.20, Target: 113.20, Stop: 114.55

Position : -

Target : -

Stop : -

Dollar’s retreat after Friday’s brief rise to 114.45 suggests consolidation below this level would be seen and weakness to 113.34-38 (previous support and 38.2% Fibonacci retracement of 111.65-114.45), break there would add credence to our view that top has possibly been formed, bring correction of recent rise to 113.05-15 (50% Fibonacci retracement and previous resistance), however, reckon 112.70-75 (61.8% Fibonacci retracement) would remain intact, bring another rise later.

In view of this, we are looking to sell dollar on recovery as 114.20-25 should limit upside, bring another retreat. Above indicated resistance at 114.45-50 would extend recent rise from 107.32 low for further gain to 114.75-80 (61.8% projection of 111.65-114.10 measuring from 113.24), however, overbought condition should limit upside to 115.00 and risk from there is seen for a retreat later.

Yen Edges Higher on Strong Japanese Retail Sales, BOJ Decision Next

USD/JPY has edged higher in Monday trade. In the North American session, USD/JPY is trading at 113.43, down 0.22% on the day. On the release front, Japanese Retail Sales posted a strong gain of 2.2%, just shy of the estimate of 2.3%. In the US, Personal Spending gained 1.0%, above the forecast of 0.8%. On Tuesday, the Bank of Japan releases its monetary statement. The US will publish CB Consumer Confidence.

All eyes are on the BoJ, which will release a rate statement on Tuesday. The Bank is expected to hold course with its ultra-accommodative monetary policy, and also maintain its inflation forecasts. Policymakers appear resigned to persistently weak inflation – at the September meeting, the BoJ stated that it did not expect inflation to reach the Bank's 2 percent target until fiscal year 2020. BoJ Governor Haruhiko Kuroda has long insisted that the bank will not taper its stimulus program until inflation moves higher. Despite weak inflation and wage growth, there has not been much pressure on the Bank to change policy, as the Japanese economy has performed well in 2017. GDP expanded at an annualized 2.5 percent in the second quarter, buoyed by solid numbers from the manufacturing and export sectors. Consumer spending has improved, and retail sales in September improved 2.3%, compared to 1.7% a month earlier. Retail sales have risen for 11 consecutive months, as consumers appear more confident in the economy and have opened their purse strings.

The week ended on a positive note in the US, as Advance GDP in third quarter jumped 3.0%, well above the estimate of 2.5%. The economy was boosted by strong consumer spending and business investment, as well as a strong export sector. The economy could have done even better in Q3, but hurricanes which hit Texas, Florida and Puerto Rico caused widespread damage. Consumer confidence remains strong, as Revised UoM Consumer Sentiment soared to 100.7 points in September, compared to 95.1 a month earlier. On Tuesday, CB Consumer Confidence is expected at 121.1 points.

EUR/USD Stabilizes after Weak German Inflation

- European equities and US equities trade little changed on the day. The Spanish IBEX35 and NASDAQ are outperformers. The former on a poll showing the pro-independent Catalan parties would lose their majority; the latter in follow-through gains after stellar earnings reports of tech bellwethers.

- Spain's public prosecutor has accused the entire Catalan government of rebellion, sedition and misuse of public funds as Madrid moved swiftly to re-impose its authority on the breakaway region. He calls for charges to be brought against the Catalan rulers that could lead to trials, which may prevent them from running in regional elections.

- Economic confidence in the eurozone surged to its highest level since 2001 this month, to extend the bloc's surprisingly robust recovery this year. The uptick was driven by strength across the economy driven by industry, retail and construction and was the 14th consecutive monthly rise.

- UK consumer lending rose at a rapid pace last month, underlining concerns that lenders could face losses in the event the British economy deteriorates. The latest lending data showed UK consumer lending rose 9.9% Y/Y in September, hovering around the 10% level it has maintained since June.

- Autumn is welcoming the Swiss economy with a tailwind, according to the Kof's economic barometer. It hit its highest level in more than seven years to reach 109.1 points in October. Consensus stood much lower at 105.5.

- The eurozone-wide recovery outweighed any impact from domestic political uncertainty on Spain's economy in Q3, with growth continuing at a healthy pace. GDP increased 0.8% Q/Q (3.1% Y/Y), down slightly from 0.9% Q/Q in Q2. Belgian GDP grew by 0.3% Q/Q following 0.5% Q/Q in Q2.

- Paul Manafort, a former campaign manager for Donald Trump and a business partner were charged with conspiracy against the US, the first people charged in the broad investigation into Russian meddling with the U.S. election

- German HICP inflation fell unexpectedly by 0.1% M/M to be up 1.5% Y/Y in October, down from 1.8% Y/Y in September and defying expectations for a more modest decline to 1.7% Y/Y. It suggests that the EMU inflation, to be reported tomorrow, will surprise on the downside too.

Rates

Catalan pro-independence bloc loses in poll

Global core bonds traded with a very small upward bias in this week's opening session. The eco calendar was unusually busy for a Monday, but didn't leave traces on bond trading. EMU eco data printed mixed with a multiyear high for the EC's confidence indicator, but a big disappointment in German inflation readings (1.5% Y/Y from 1.8% Y/Y). US eco data (personal income/spending and PCE) were very close to consensus, but that shouldn't surprise as Q3 GDP numbers were already released last Friday.

At the time of writing, the German yield curve flattens with yield changes ranging between +1.4 bps (2-yr) and -1.7 bps (30-yr). The belly of the US yield curve (-1.5 bps) slightly outperforms the wings (flat). From a technical point of view, the US 10-yr (2.42%) and US 30-yr (2.95%) yields are back below key resistance levels following last week's intense, but failed, test. On intra-EMU bond markets, 10-yr yield spread changes versus Germany are narrowly mixed with a significant outperformance of Portugal (-10 bps), Spain (-7 bps) and Italy (-9 bps after S&P upgrade). The Spanish outperformance is related to an El Mundo poll whish showed that the pro-independence bloc would lose its majority in new Catalan elections.

The Italian debt agency tapped the on the run 5-yr BTP (€2.5 bn 0.9% Aug2022) and 10-yr BTP (€2.5 bn 2.05% Aug2027). The combined amount sold was the maximum of the €4-5 bn on offer with a 1.48 auction bid cover which is in line with average. S&P's rating upgrade on Friday night (to BBB) couldn't give an additional boost. Apart from the regular BTP's, the Italian debt agency also launched a new floating rate bond (€3.5 bn Apr2025).

Currencies

EUR/USD stabilizes after weak German inflation

EUR/USD tried to fight back after an uneventful sideways oriented overnight session and a shy attempt of the dollar to extend its rally for a third day in a row. The dip lower in EUR/USD met renewed euro buying in albeit thin market conditions. EUR/USD recouped opening levels around 1.1610 and powered ahead to the 1.1640 area where resistance kicked in and a pause materialised. The start of the up-move had no distinct trigger, but stronger German retail sales and 17-yr high euro area economic sentiment were of course underlying euro positives. Lower-than-expected German states' inflation was less positive, but ignored. After US traders joined the fray, the euro's going got tougher. The 1.1644 high remained too tough to break and the pair gradually slid lower. When the overall German inflation was reported much lower than expected, EUR/USD dropped instantaneously to 1.1610 opening levels. There was no follow through euro selling though, allowing the pair to stabilize. US personal spending was, as expected, very strong, while PCE deflators were in line with expectations. It had little impact. Similarly, the indictment of president Trump's former campaign chair, Mr. Manfort, didn't weigh on the dollar.

USD/JPY had an uneventful session today, after failing to take out major resistance at 114.45 on Friday. There was no attempt to give it another try. The pair traded listless in the 113.50/80 range. In early US dealings the pair briefly moved to 113.40, maybe a shy reaction to the FBI indictment of Paul Manafort,. However, the dollar decline never went far and the pair trades currently at 113.50, a minor 23 tick daily loss. Equity trading was also mostly sideways and in any case showed insufficient firm direction to affect the cross. Neither did yields.

Sterling makes further headway ahead of BoE meeting

Sterling is already for some days in a positive flow and that continued today. After an uneventful morning session, sterling caught a bid. We signaled that technicals improved and a modest double top formation in EUR/GBP could send the pair towards the key supports at 0.8743/0.8652. We didn't see any trigger that caused today's sterling buying, but suspect that rate expectations ahead of Thursday's BOE meeting and the technical picture played a role. Once the ball got rolling, lower than expected German inflation weakened the euro overall. EUR/GBP slid from 0.8840 at noon (CET) to an intraday low at 0.8790 after the German inflation release and is at the moment of writing quoted around 0.8807. Cable moved already higher in the morning session in sympathy with a temporary EUR/USD up-move. It made some more headway in the afternoon session despite a dip in EUR/USD. Cable trades now at 1.3190, up from opening levels around 1.3130.

BoJ Expected to Stand Pat; Weaker Inflation Outlook Could Hurt the Yen

The Bank of Japan will be tomorrow completing its two-day meeting on monetary policy. With inflation remaining well below the central bank's 2% target - headline and core inflation grew by 0.7% y/y in September - the BoJ is not expected to reverse course from its ultra-easy monetary policy stance.

Market participants anticipate the BoJ to maintain the 0.1% fee charged on a portion of commercial banks' reserves held with the central bank as well as keep its target for the 10-year Japanese government bond yield around 0%. It is also likely to maintain its purchases of exchange-traded funds and real estate investment trusts at current levels.

The base case scenario is that there won't be much market reaction to the BoJ's decision, given of course that the outcome does not significantly deviate from expectations. There is speculation however that the central bank could cut this year's inflation forecast of 1.1%. The BoJ has also numerous times in the past pushed forward its time frame for achieving its 2% inflation target - it currently aims to accomplish that "around fiscal 2019." Should the bank indeed project a weaker outlook for inflation, then dollar/yen could head higher. The pair touched a three-and-a-half-month peak of 114.44 at its highest on Friday following the release of stronger-than-expected third quarter GDP figures out of the US. The area around this level, which also encapsulates a couple of peaks from the recent past, could act as a barrier to the upside, with the range around the 114 handle - a potential psychological level - also having the capacity to act as resistance.

A hawkish take by the BoJ that would push dollar/yen lower is unlikely, especially in light of the fact that dovish-perceived members have recently joined the bank's board; in the previous meeting new board member Goushi Kataoka dissented, favoring additional stimulus. If dollar/yen moves lower, then that's more likely to do with figures for household spending, employment and industrial production for the month of September all due tomorrow out of Japan (with US-related developments pushing the pair lower also not to be ruled out). A decline could see the pair finding support around the 113 mark, this being an area of congestion recently.

In the bigger picture, the BoJ is likely to stick to its broader outlook of a gradual rise in inflation and moderate growth.

BoJ Governor Haruhiko Kuroda's term ends in April. Prime Minister Shinzo Abe coming strong out of elections earlier this month is seen as increasing the chances of Kuroda being reappointed as BoJ chief for a second five-year term, something which would likely translate into massive stimulus remaining in place further ahead. Given the different path monetary policy is taking in Japan versus elsewhere in the world - and perhaps most notably in the US - this is supportive of a weaker yen relative to other currencies in the medium- to longer-term.

The recent rally in equities in the world's third largest economy is also noteworthy - the Topix and Nikkei 225 currently stand at their highest levels since 2007 and 1996 respectively.

Later in the week, the forex markets' focus would turn to the Fed meeting (November 1) and the Bank of England meeting (November 2) with the latter one being the one that is seen as having the highest odds of reflecting a shift in monetary policy.