Sample Category Title

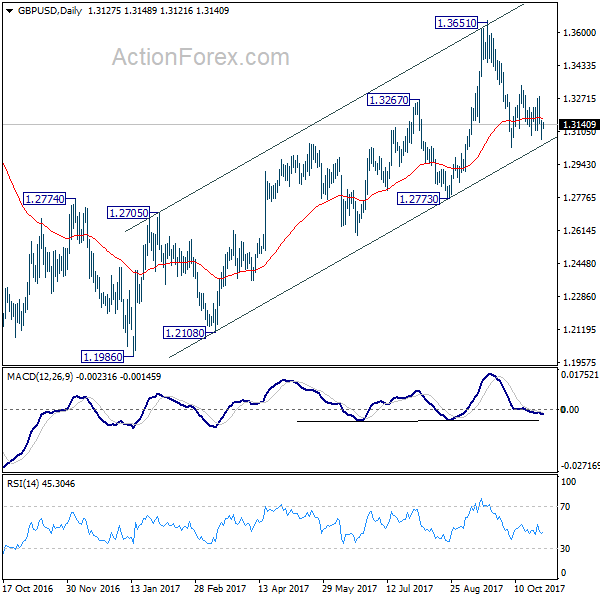

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3072; (P) 1.3116; (R1) 1.3164; More....

Intraday bias in GBP/USD remains neutral at this point. On the downside, firm break of 1.3026 support will resume the decline from 1.3651 and target 1.2773 key support level. This will also revive the case of medium term reversal. On the upside, in case of another rally, upside should be limited by 61.8% retracement of 1.3651 to 1.3026 at 1.3412 to bring fall resumption finally.

In the bigger picture, while the medium term rebound from 1.1946 was strong, GBP/USD hit strong resistance from the long term falling trend line. Outlook is turned a bit mixed and we'll stay neutral first. On the downside, decisive break of 1.2773 key support will argue that rebound from 1.1946 has completed. The corrective structure of rise from 1.1946 to 1.3651 will in turn suggest that long term down trend is now completed. Break of 1.1946 low should then be seen. On the upside, break of 1.3835 support turned resistance will revive the case of trend reversal and target 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466 .

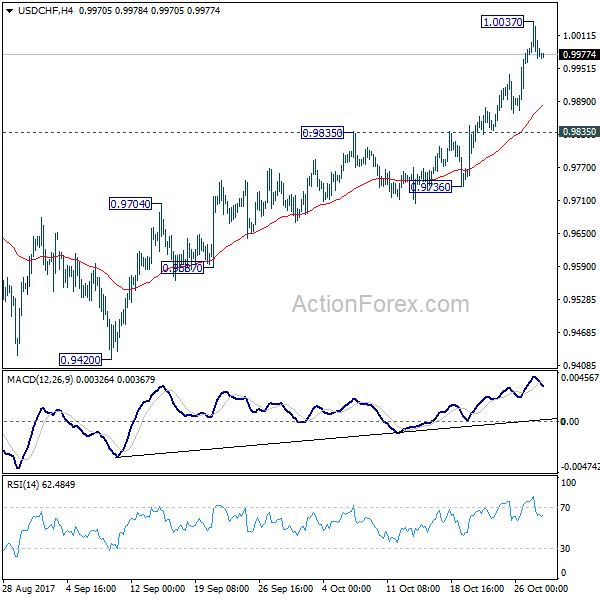

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9942; (P) 0.9989; (R1) 1.0019; More....

Intraday bias in USD/CHF remains neutral for consolidation below 1.0037 temporary top. Downside of retreat should be contained above 0.9835 resistance turned support and bring rally resumption . Since 61.8% retracement of 1.0342 to 0.9420 at 0.9990 is already met, break of 1.0037 will turn bias to the upside for 1.0342 key resistance next.

In the bigger picture, current development suggests that USD/CHF has defended 0.9443 (2016 low) key support level again. Rise from 0.9420 could is a medium term up move and should target a test on 1.0342 high. This represents the upper end of a long term range that started back in 2015. On the downside, break of 0.9736 support is now needed to indicate completion of the rise from 0.9420. Otherwise, further rally will remain in favor in medium term.

Market Update – Asian Session: Regional Bond Yields Gain

Asia Summary

Asian equity markets have opened generally higher, following Friday's gains seen on the Nasdaq.

In the tech sector, Sharp has gained over 2%, as the company raised its FY operating profit guidance. Shares of Softbank and Hitachi have traded higher by over 1%, while Nintendo is currently flat ahead of its later today earnings report. Samsung Electronics has gained over 1.5% ahead of its earnings presentation due on Oct 31st. Nasdaq Futures are trading at around flat levels. According to a press report out of Taiwan, Apple is said to have asked suppliers for the iPhone X to double their capacities amid stronger than expected demand.

Nippon Steel has declined by over 1%, as Q2 profits missed market expectations. Kobe Steel, which is expected to release its earnings report later today, has gained over 1.5%. In China Baoshan Iron & Steel has declined by over 0.4% amid the release of its earnings report.

Japanese industrial name Komatsu has traded higher by over 3% after the company reported better than expected Q2 profits and raised its FY guidance. Chinese rail equipment firm CRRC Corp has gained over 1% after reporting an increase in Q3 profits. Hong Kong listed cement producer Anhui Conch has gained over 2% following its earnings report.

PetroChina's shares are trading higher ahead of its later today earnings report. Energy producers in Australia are trading generally higher, following the over 2% rise seen in oil prices on Friday's US session.

As of the time of writing, markets have traded off of their best levels. Japanese mega banks are trading generally lower on the session, following the recent gains that have been seen since Japan's general election results.

In China, Bank of Communications and China Merchants Bank have traded lower following their respective earnings reports. BYD is also lower by over 3%, after releasing its financial results. The overall Shanghai Composite has declined by over 1%.

China's 5 and 10-year government bond yields have added on to the gains seen during the prior week and are currently at the highest levels since late 2014. In South Korea, bond yields are trading lower. Earlier during the session, the Bank of Korea announced that it was planning to repurchase government bonds later this week. Looking ahead on Wednesday's session, South Korea is due to release its Oct CPI data.

On tomorrow's session, China's October manufacturing and non-manufacturing PMI data is due to be released, along with the Bank of Japan's policy statement and forecasts. Other notable macro-economic releases for this week include, New Zealand Q3 employment change (Wed), US Fed decision (Wed), Australia Sept Trade Balance (Thursday), Bank of England decision (Thursday), Australia Sept retail sales (Friday) and US Oct Nonfarm payrolls (Friday).

Japanese companies due to report earnings later today include Alps Electric, Casio, ibiden, Kao Corp, Konica Minota, Kyocera, Nippon Carbon, Nippon Electric Glass, Nomura, ORIX Corp, Seikisui Chemicals, Stanley Electric, Sumitomo Dainippon Pharma, TDK and West Japan Railway.

US companies seen reporting on Monday include Mondelez International. HSBC reported Q3 results which exceeded analyst expectations.

Key economic data

(JP) JAPAN SEPT RETAIL SALES M/M: 0.8% V 0.8%E; RETAIL TRADE Y/Y: 2.2% V 2.3%E; Department Store, Supermarket Sales y/y: 1.9% v 1.5%e

(NZ) Statistics NZ: Corrects Q2 retail sales q/q to 1.7% from 2.0%; delays Q3 release on new methodology

Speakers and Press

Japan

(JP) BOJ Gov Kuroda likely to stay for another 5 year term after his current term ends on April 2018 – Nikkei

(JP) Japan FSA said to set capital requirement rules for high frequency trading (HFT) firms - Japanese Press

Korea

(KR) Bank of Korea (BOK) Official: Planning to repurchase bonds this week to stabilize the market

China/Hong Kong

(CN) CICC Research sees 2018 real GDP at 6.9% v 6.7% prior

Australia/New Zealand

(AU) Australia Treasurer Morrison: Businesses are seeing best conditions since 2008

(AU) Australia Queensland calls snap election after the ruling center-left Labor Party lost its legislative majority

(NZ) New Zealand PM Ardern: want to legislate to ban foreign buyers of existing NZ homes before TPP-11 is ratified

Asian Equity Indices/Futures (00:00ET)

Nikkei -0.2%, Hang Seng +0.0%; Shanghai Composite -0.7%; ASX200 +0.4%, Kospi +0.3%

Equity Futures: S&P500 -0.2%; Nasdaq100 -0.1%, Dax -0.1%; FTSE100 -0.3%

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.1615-1.1594; JPY 113.83-113.52; AUD 0.7682-0.7664;NZD 0.6887-0.6840

Dec Gold +0.1% at $1,272/oz; Dec Crude Oil +0.1% at $53.94/brl; Dec Copper -0.2% at $3.09/lb

(AU) Australia MoF buys back A$500M in Oct 2018 and Mar 2019 bonds

(AU) Australia MoF sells A$500M in 2029 bonds, avg yield 2.8110%, bid to cover 6.5x

(CN) PBoC OMO: Injects CNY150B combined CNY140B in 7-day, 14-day and 63-day reverse repos v CNY140B prior; Net injection CNY40B

USD/CNY *(CN) PBOC SETS YUAN REFERENCE RATE AT 6.6487 V 6.6473 PRIOR

(CN) CHina MoF sells 5-yr special treasury bonds at 3.9206%

Equities notable movers

Australia/New Zealand

NAB.AU Agreed to a A$30M settlement with the Australian Securities and Investments Commission (ASIC) of the Bank Bill Swap Rate (BBSW) legal action – filing; +0.1%

COE.AU Reports Q1 production 0.43 MBOE v 0.09M BOE y/y; Rev A$14.4M v A$4.9M y/y; +6.7%

TNG.AU Reports FY17 (A$) Net loss 4.4M v loss 7.1M y/y; Total income 504K v 6K y/y - Annual reports; -6%

Japan

8411.JP Said to be considering cutting up to a third of its global workforce over the next 10 years – FT; -0.1%

7731.JP Reports prelim H1 Net ¥14B v ¥13B guided; Op ¥23B v ¥17B guded;to discontinue China unit of imaging business; +0.8%

Korea

004990.KR Shares resume trading after restructuring into holding company; +17.5%

009150.KR Reports Q3 (KRW) Net profit 74.5B v 3.85B y/y, Op profit 103.2B v 12.8B y/y, Rev 1.84T v 1.47T y/y; +5%

042660.KR Resumes trading after more than 1-yr halt; -30%

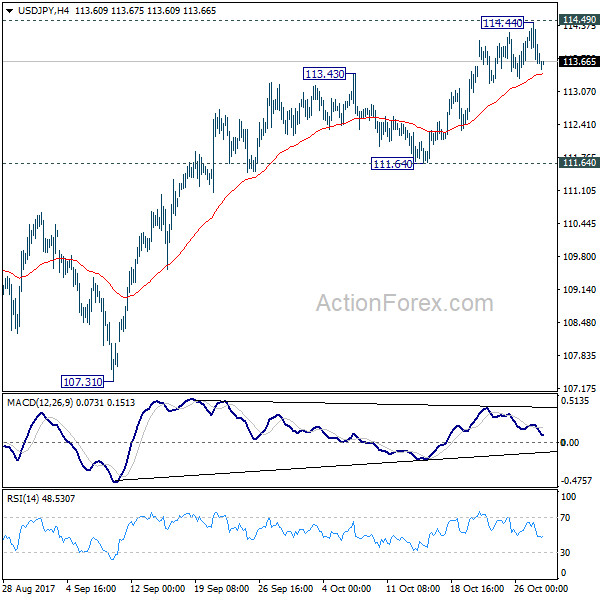

USD/JPY Daily Outlook

Daily Pivots: (S1) 113.39; (P) 113.91; (R1) 114.20; More...

Intraday bias in USD/JPY remains neutral for the moment. Pull back from 114.44 could extend lower. But after all, outlook will stays cautiously bullish as long as 111.64 support holds. Decisive break of 114.49 key resistance will confirm that correction pattern from 118.65 has completed at 107.31 already. And USD/JPY should then target a test on 118.65.

In the bigger picture, medium term rise from 98.97 (2016 low) is not completed yet. It should resume after corrective fall from 118.65 completes. Break of 114.49 resistance will likely resume the rise to 61.8% projection of 98.97 to 118.65 from 107.31 at 119.47 first. Firm break there will pave the way to 100% projection at 126.99. This will be the key level to decide whether long term up trend is resuming.

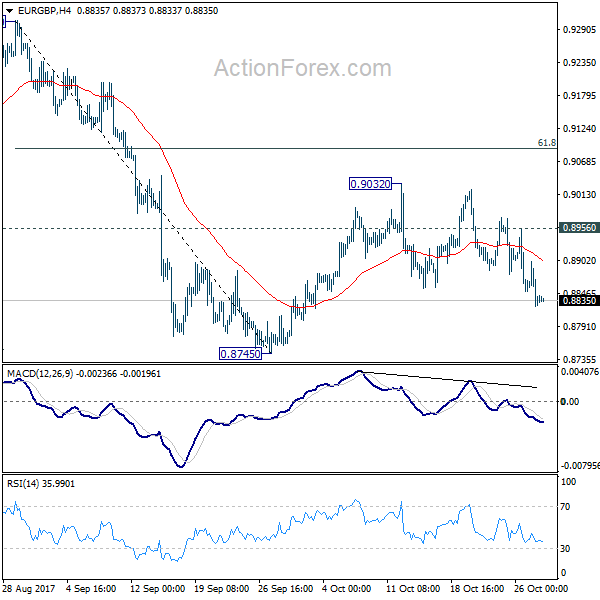

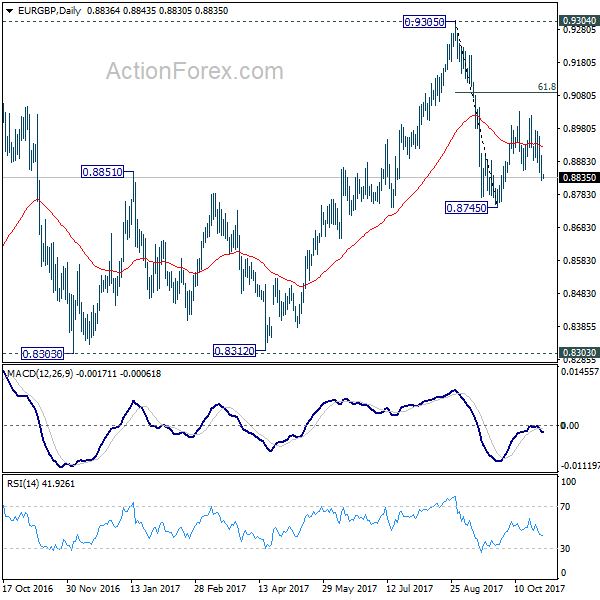

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8809; (P) 0.8855; (R1) 0.8885; More...

Intraday bias in EUR/GBP remains mildly on the downside for 0.8745 support. Break will will resume whole fall from 0.9305 and target 0.8303 key support level. On the upside, above 0.8956 minor resistance will extend the corrective rise from 0.8745 with another rise. But upside should be limited by 61.8% retracement of 0.9305 to 0.8745 at 0.9091 to bring fall resumption eventually.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of another fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

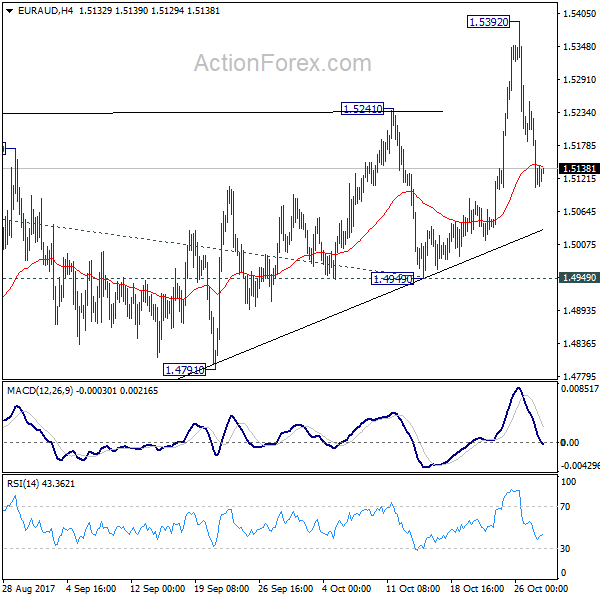

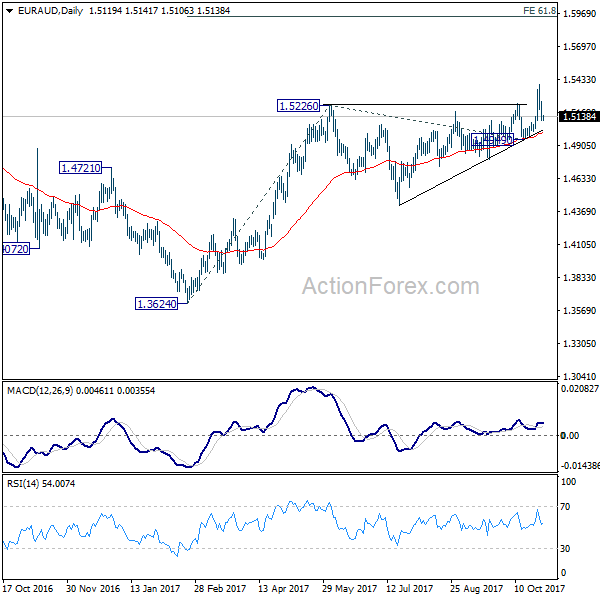

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5060; (P) 1.5157; (R1) 1.5208; More....

Intraday bias in EUR/AUD remains neutral first. While the pull back from 1.5392 was steep, it's holding well above 1.4949 support. Thus, medium term rally is still in favor to resume. On the upside, break of 1.5392 will resume medium term rise from 1.3624 and target 61.8% projection of 1.3624 to 1.5226 from 1.4949 at 1.5939 first. However, decisive break of 1.4949 will carry larger bearish implication and turn bias to the downside.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term top has completed at 1.3624. Rise from 1.3624 is expected to extend to retest 1.6587. However, break of 1.4949 support will dampen our view and argue that rise from 1.3624 has completed. In that case, EUR/AUD would turn southward for retesting 1.3624 low.

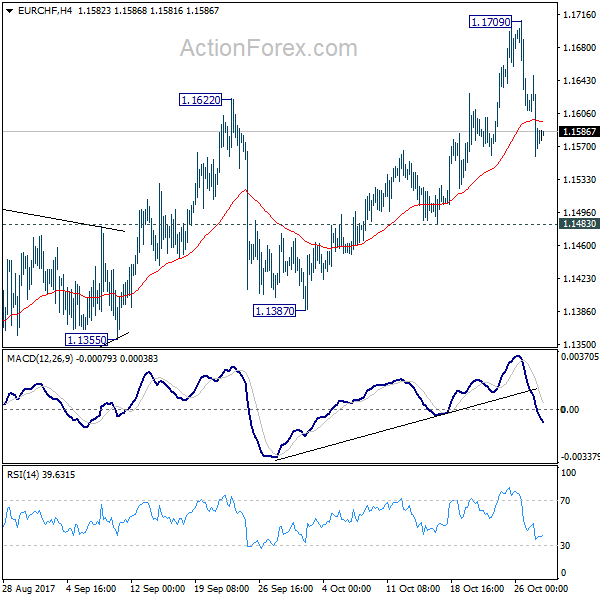

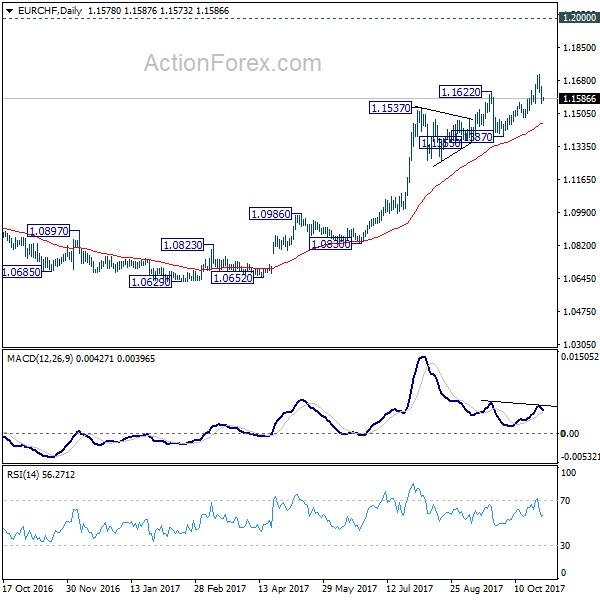

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1541; (P) 1.1595; (R1) 1.1630; More...

Intraday bias in EUR/CHF remains neutral for the moment. Pull back from 1.1709 might extend lower. But still, as long as 1.1483 minor support holds, we'd expect further rally ahead. Break of 1.1709 will target 1.2 key level. However, break of 1.1483 will be an early sign of reversal. In that case, deeper decline should be seen back to 1.1355 support.

In the bigger picture, long term rise from SNB spike low back in 2015 is still in progress. EUR/CHF should now be heading back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.1355 support holds. However, break of 1.1355 will indicate medium term topping. In that case, EUR/CHF should head back to 55 week EMA (now at 1.1067) and possibly below.

Aussie Dollar Trading Higher This Morning

For the 24 hours to 23:00 GMT, the AUD rose 0.22% against the USD and closed at 0.7670 on Friday.

LME Copper prices declined 1.9% or $132.5/MT to $6831.5/MT. Aluminium prices declined 2.5% or $55.0/MT to $2119.0/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7676, with the AUD trading 0.08% higher from Friday’s close.

The pair is expected to find support at 0.7640, and a fall through could take it to the next support level of 0.7604. The pair is expected to find its first resistance at 0.7697, and a rise through could take it to the next resistance level of 0.7718.

Investors will now closely assess Australia’s HIA new homes sales and private sector credit data, both for September, due overnight.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 148.62; (P) 149.32; (R1) 149.83; More

Intraday bias in GBP/JPY is mildly on the downside for 149.82 support. Break there will resume the correction from 152.82 and target 61.8% retracement of 139.29 to 152.82 at 144.45. Such decline is seen as a correction and we'd look for strong support from 144.45 to bring rebound. On the upside, above 151.38 will target a test on 152.82 high instead.

In the bigger picture, medium term rebound from 122.36 is still expected to resume after corrective pull back from 152.82 completes. Firm break of 38.2% retracement of 196.85 to 122.36 at 150.43 will carry long term bullish implications. In that case, GBP/JPY could target 61.8% retracement at 167.78. However, break of 139.29 will indicate rejection from 150.43 key fibonacci level. And the three wave corrective structure of rebound from 122.36 will argue that larger down trend is resuming for a new low below 122.26.

Catalonia Declares Independence From Spain, ECB Survey Expects Higher Eurozone Inflation In 2022

For the 24 hours to 23:00 GMT, the EUR declined 0.31% against the USD and closed at 1.1600 on Friday, after the Catalan Parliament declared its independence from Spain.

The European Central Bank’s (ECB) survey of professional forecasters showed that the Eurozone consumer price index could be higher than earlier expected in five years’ time, thus supporting the ECB’s recent decision to trim its monetary stimulus. Inflation growth is expected to rise to 1.9% by 2022, in line with the central bank’s target and above the 1.8% projected three months ago. Moreover, the Eurozone economy is also expected to grow at a faster rate than previously expected for both 2018 and 2019. The survey now anticipates growth at 1.9% and 1.7% in 2018 and 2019, respectively.

On the macro front, German import price index advanced more than expected on a yearly basis in September as it registered a rise of 3.0%, compared to a rise of 2.1% in the previous month. Market anticipation was for the import price index to climb 2.6%.

The US Dollar gained ground against its major counterparts after macroeconomic data showed that the world’s largest economy expanded at an annual rate of 3.0% on a QoQ basis in the third quarter of 2017, compared to a rise of 3.1% in the prior quarter. Market had anticipated the annualised GDP growth to ease to 2.6% due to devastation caused by Hurricanes Harvey and Irma. Additionally, the final Reuters/Michigan consumer sentiment index in the US rose to 100.7 in October, at par with market expectations. In the prior month, the consumer sentiment index had recorded a reading of 95.1. The preliminary figures had indicated an advance to 98.0. However, gains in the US dollar were pared following news that US President, Donald Trump, was leaning toward Federal Reserve Governor, Jerome Powell, as the next US central bank Chairman.

In the Asian session, at GMT0400, the pair is trading at 1.1614, with the EUR trading 0.12% higher from Friday’s close.

The pair is expected to find support at 1.1578, and a fall through could take it to the next support level of 1.1542. The pair is expected to find its first resistance at 1.1647, and a rise through could take it to the next resistance level of 1.1680.

Moving ahead, all eyes will be on the Eurozone economic confidence and business climate indicator, along with the region’s final consumer confidence index, all for October, due to release today. Moreover, Germany’s inflation numbers for October and the nation’s retail sales data for September, scheduled for today, will be on investors’ radar. In the US, personal spending as well as income figures for September, set to release later in the day, will also garner significant market attention.

The currency pair is trading between its 20 Hr and 50 Hr moving averages.