Sample Category Title

ECB Begins Trimming Asset Purchase in 2018, Pledges to Expand/ Extend if Necessary

ECB announced the plan to reduce asset purchase next year. In line with the majority of market participants had anticipated, the central bank would trim the size of buying by half, to 30B euro per month, in the first nine months of 2018, "or beyond, if necessary". It added that stimulus measures would be implemented "in any case until the Governing Council sees a sustained adjustment in the path of inflation consistent with its inflation aim". The single currency dropped after the announcement, on profit-taking. The policy rates stayed unchanged, with the main refinancing rate, the marginal lending rate and the deposit rate at 0%, 0.25% and -0.40% respectively.

Satisfactory Economic Recovery

At the press conference, President Mario Draghi appeared confident over the Eurozone's economic recovery, suggesting growth has continued "unabated". He supported his judgment citing the upswing in business investment, improvement in construction investment has also improved, as well as robust exports. While attributing these developments to the accommodative monetary policy and QE, Draghi again called for "more growth-friendly" fiscal policies in "all Eurozone countries"..

Dovish Tapering

Despite tapering, ECB intentionally maintain a dovish tone. Draghi used "recalibration" of the asset purchase program, instead of the word "tapering". He admitted that the decision was not an unanimous one. Yet, the members were generally positive towards reducing the size of purchase, thanks to the increase in employment across the Eurozone and rising wages. The composition in the assets to be bought would be largely unchanged. Meanwhile, ECB would reinvest the principal payments from maturing securities "for an extended period of time after the end of its net asset purchases, and in any case for as long as necessary". The central bank remained flexible and noted that "if the outlook becomes less favourable, or if financial conditions become inconsistent with further progress towards a sustained adjustment in the path of inflation, the Governing Council stands ready to increase the APP in terms of size and/or duration". At the press conference, Draghi maintained a flexible tone and reiterated that the stimulus measures after September 2018 is "open-ended.

ECB is not Fed

When asked about why ECB continues to buy assets while the Fed has begun balance sheet reduction, Draghi suggested that the US recovery is "way more advanced" than in the Eurozone, and the region's inflation outlook is "way behind". He dismissed comparison between ECB and the Fed, refusing to promise that ECB would follow the suit of the Fed in raising interest rates 15 months after ending the bond-purchase program.

Yen Ticks Lower as Japanese Inflation Report Meets Expectations

USD/JPY has inched higher in Thursday trade. In the North American session, USD/JPY is trading at 113.64, down 0.09% on the day. On the release front, Japanese Services Producer Price Index gained 0.9%, above the forecast of 0.8%. In the US, unemployment claims climbed to 233 thousand, just below the forecast of 235 thousand. Later in the day, Japan releases Tokyo Core CPI, which is expected to remain unchanged at 0.5 percent. On Friday, the US releases two key indicators – Advance GDP and the UoM Consumer Sentiment.

The Bank of Japan is expected to hold course with its ultra-accommodative monetary policy, following Prime Minister Shinzo Abe's convincing election victory this week. The BoJ holds a policy meeting next week, and policymakers are expected to maintain its inflation forecasts. At the September meeting, the BoJ stated that it did not expect inflation to reach the Bank's 2 percent target until fiscal year 2020. BoJ Governor Haruhiko Kuroda has long insisted that the bank will not taper its stimulus program until inflation moves higher. Despite weak inflation and wage growth, there has not been much pressure on the Bank to change policy, as the Japanese economy has performed well in 2017. GDP expanded at an annualized 2.5 percent in the second quarter, buoyed by solid numbers from the manufacturing and export sectors.

The US releases Advance GDP on Friday, and this key indicator should be treated as a market mover. The markets are forecasting a gain of 2.5%, after Preliminary GDP posted a sharp gain of 3.0%. US economic numbers remain strong, and the labor market is close to capacity. At the same time, inflation has not moved higher, and wage growth has been weaker than expected. Despite the lack of inflation, the odds of a December rate hike have soared in recent weeks, with the odds of a rate raise at 96%, according to CME FedWatch.

EURGBP: Vulnerable, Eyes Move Towards The 0.8855 Zone

EURGBP- The cross remains biased to downside and looks to extend that weakness with eyes on 0.8855 level. Support lies at the 0.8850 Level where a violation will turn focus to the 0.8800 level. A break will expose the 0.8750 level. Its daily RSI is bearish and pointing lower suggesting further decline. Resistance resides at the 0.8950 level where a violation if seen will turn risk towards the 0.9000 level. Further up, resistance resides at 0.9050 level followed by the 0.9100 level. All in all, EURGBP remains biased to the downside on further weakness.

(ECB) Introductory Statement to the Press Conference

Mario Draghi, President of the ECB,

Vítor Constâncio, Vice-President of the ECB,

Frankfurt am Main, 26 October 2017

Ladies and gentlemen, the Vice-President and I are very pleased to welcome you to our press conference. We will now report on the outcome of today's meeting of the Governing Council, which was also attended by the Commission Vice-President, Mr Dombrovskis.

Based on our regular economic and monetary analyses, today we conducted a thorough assessment of the outlook for inflation, the risks surrounding this outlook and our monetary policy stance. As a result, the Governing Council took the following decisions in pursuit of its price stability objective.

First, the key ECB interest rates were kept unchanged and we continue to expect them to remain at their present levels for an extended period of time, and well past the horizon of our net asset purchases.

Second, as regards non-standard monetary policy measures, we will continue to make purchases under the asset purchase programme (APP) at the current monthly pace of €60 billion until the end of December 2017. From January 2018 our net asset purchases are intended to continue at a monthly pace of €30 billion until the end of September 2018, or beyond, if necessary, and in any case until the Governing Council sees a sustained adjustment in the path of inflation consistent with its inflation aim. If the outlook becomes less favourable, or if financial conditions become inconsistent with further progress towards a sustained adjustment in the path of inflation, we stand ready to increase the APP in terms of size and/or duration.

Third, the Eurosystem will reinvest the principal payments from maturing securities purchased under the APP for an extended period of time after the end of its net asset purchases, and in any case for as long as necessary. This will contribute both to favourable liquidity conditions and to an appropriate monetary policy stance.

And fourth, we also decided to continue to conduct the main refinancing operations and three-month longer-term refinancing operations as fixed rate tender procedures with full allotment for as long as necessary, and at least until the end of the last reserve maintenance period of 2019.

Today's monetary policy decisions were taken to preserve the very favourable financing conditions that are still needed for a sustained return of inflation rates towards levels that are below, but close to, 2%. The recalibration of our asset purchases reflects growing confidence in the gradual convergence of inflation rates towards our inflation aim, on account of the increasingly robust and broad-based economic expansion, an uptick in measures of underlying inflation and the continued effective pass-through of our policy measures to the financing conditions of the real economy. At the same time, domestic price pressures are still muted overall and the economic outlook and the path of inflation remain conditional on continued support from monetary policy. Therefore, an ample degree of monetary stimulus remains necessary for underlying inflation pressures to continue to build up and support headline inflation developments over the medium term. This continued monetary support is provided by the additional net asset purchases, by the sizeable stock of acquired assets and the forthcoming reinvestments, and by our forward guidance on interest rates.

Let me now explain our assessment in greater detail, starting with the economic analysis. The economic expansion in the euro area continues to be solid and broad-based. Real GDP increased by 0.7%, quarter on quarter, in the second quarter of 2017, after 0.6% in the first quarter. The latest data and survey results point to unabated growth momentum in the second half of this year. Our monetary policy measures have facilitated the deleveraging process and continue to support domestic demand. Private consumption is underpinned by rising employment, which is also benefiting from past labour market reforms, and by increasing household wealth. The upswing in business investment continues to benefit from very favourable financing conditions and improvements in corporate profitability. Construction investment has also strengthened. In addition, the broad-based global recovery is supporting euro area exports.

Risks surrounding the euro area growth outlook remain broadly balanced. On the one hand, the strong cyclical momentum, as evidenced in recent developments in sentiment indicators, could lead to further positive growth surprises. On the other hand, downside risks continue to relate primarily to global factors and developments in foreign exchange markets.

Euro area annual HICP inflation remained unchanged at 1.5% in September. Looking ahead, on the basis of current futures prices for oil, annual rates of headline inflation are likely to temporarily decline towards the turn of the year, mainly reflecting base effects in energy prices. At the same time, measures of underlying inflation have ticked up moderately since early 2017, but have yet to show more convincing signs of a sustained upward trend. Wage growth has increased somewhat, but domestic cost pressures still remain subdued overall. Underlying inflation in the euro area is expected to continue to rise gradually over the medium term, supported by our monetary policy measures, the continuing economic expansion, the corresponding gradual absorption of economic slack and rising wage growth.

Turning to the monetary analysis, broad money (M3) continues to expand at a robust pace, with an annual rate of growth of 5.1% in September 2017, after 5.0% in August. As in previous months, annual growth in M3 was mainly supported by its most liquid components, with the narrow monetary aggregate M1 expanding at an annual rate of 9.7% in September 2017, up from 9.5% in August.

The recovery in the growth of loans to the private sector observed since the beginning of 2014 is proceeding. The annual growth rate of loans to non-financial corporations increased to 2.5% in September 2017, after 2.4% in August, while the annual growth rate of loans to households remained stable at 2.7%. The euro area bank lending survey for the third quarter of 2017 indicates that net loan demand has continued to increase for all loan categories. Credit standards have further eased for loans to households, while they remained broadly unchanged for loans to enterprises. Banks' overall terms and conditions on new loans have continued to ease for all categories of loans.

The pass-through of the monetary policy measures put in place since June 2014 continues to significantly support borrowing conditions for firms and households, access to financing ‒ notably for small and medium-sized enterprises ‒ and credit flows across the euro area.

To sum up, a cross-check of the outcome of the economic analysis with the signals coming from the monetary analysis confirmed the need to recalibrate the policy instruments to ensure the degree of monetary accommodation necessary to secure a sustained return of inflation rates towards levels that are below, but close to, 2%.

In order to reap the full benefits from our monetary policy measures, other policy areas must contribute decisively to strengthening the longer-term growth potential and reducing vulnerabilities. The implementation of structural reforms in all euro area countries needs to be substantially stepped up to increase resilience, reduce structural unemployment and boost euro area productivity and growth potential. Regarding fiscal policies, all countries would benefit from intensifying efforts towards achieving a more growth-friendly composition of public finances. A full, transparent and consistent implementation of the Stability and Growth Pact and of the macroeconomic imbalance procedure over time and across countries remains essential to increase the resilience of the euro area economy. Strengthening Economic and Monetary Union remains a priority. The Governing Council welcomes the ongoing discussions on further enhancing the institutional architecture of our Economic and Monetary Union.

We are now at your disposal for questions.

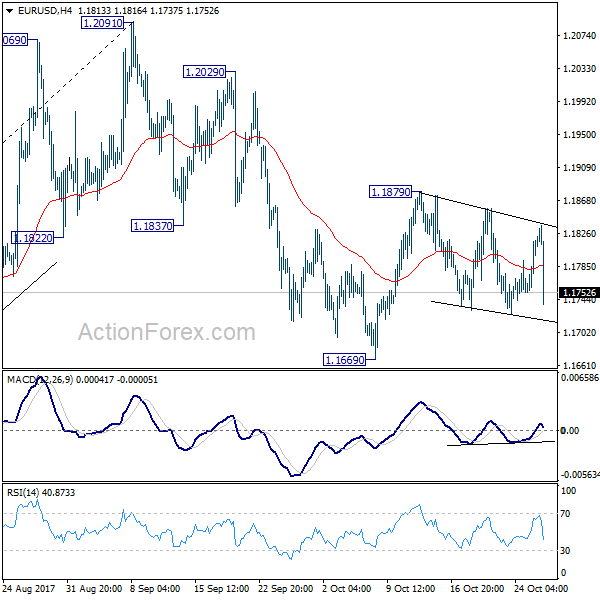

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1770; (P) 1.1794 (R1) 1.1835; More...

EUR/USD drops sharply after ECB announcement. But it's staying in range of 1.1669/1879 and intraday bias remains neutral at this point. On the downside, break of 1.1669 will resume the corrective fall from 1.2091 to 38.2% retracement of 1.0569 to 1.2091 at 1.1510. We'd expect strong support from there to complete the correction. On the upside, break of 1.1879 will revive the case that pull back from 1.2091 has already completed at 1.1669. In such case, intraday bias will be turned back to the upside for retesting 1.2091 high.

In the bigger picture, rise from medium term bottom at 1.0339 is not finished yet. It's expected to continue after pull back from 1.2091 completes. And, next target will be 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. However, it should be noted that there is no confirmation of trend reversal yet. That is, such rebound from 1.0399 could be a correction. And the long term fall from 1.6039 (2008 high) could resume. Hence, we'd be cautious on strong resistance from 1.2516 to limit upside.

Euro Drops Sharply after ECB Announces to Half Asset Purchases, Extends by 9 Months

Euro drops sharply after ECB announced the tapering plan as the markets expected. But traders seem to be unhappy with the cautious tone in the statement. Meanwhile, Dollar remains generally firm, as supported by solid job data. Also, markets are getting more convinced that either Powell or Taylor will be taken as the next Fed chair. Elsewhere, Canadian and Australian Dollar are both trying to recovery yesterday's losses. But not much strength is seen against Dollar yet.

ECB halves asset purchase, extends 9 months

ECB left main refinancing rate unchanged at 0.00% as widely expected. The marginal lending facility rate and deposit facility rate are held at 0.25% and -0.40% respectively. The key in the announcement is that starting January 2018, the next asset purchases will be halved to EUR 30B a month, down from current EUR 60B a month. The asset purchase program will be extended by nine months until end of September 2018, or beyond.

ECB left the options open for itself and noted that "if the outlook becomes less favorable, or if financial conditions become inconsistent with further progress towards a sustained adjustment in the path of inflation, the Governing Council stands ready to increase the APP in terms of size and/or duration."

Euro dives after the release. While the halving of the size and 9 months of extensions are in line with expectation, traders seem to be unhappy with the cautious tone in the accompanying statement.

House to vote on budget plan

In US, the House is set to vote on the Senate's version of budget plan today, to pave way for finishing the tax plan by year end. This will be closely watched as some House Republicans vowed to vote against it. They believe that the plan that eliminate state and local income taxes deduction would hit middle-class votes in regions like New York, New Jersey and California.

Regarding US President Donald Trump's decisions on who to succeed Janet Yellen as Fed chair, it's reported that decisions will be made very soon. White House advisor Gary Cohn was out of the race as he's central to the tax plan. Former Fed Governor Kevin Warsh was also eliminated. Latest news say that Yellen is finally out. That leaves current Fed Governor Jerome Powell and Stanford University economist John Taylor as front runners. And a regularly cited option is for both of them to take the chair and vice place.

Jobless claims rose to 233k, continuing claims hit lowest since 1973

Initial jobless claims rose 10K to 233K in the week ended October 21, slightly below expectation of 236K. The four week moving average dropped to 239.5K, down from 248.5K. Continuing claims dropped -3K to 1.89M in the week ended October 14, lowest since December 1973. Also from US, trade deficit widened slightly to USD -64.1B in September, versus consensus of USD -63.8B.

Release earlier today

Eurozone M3 rose 5.1% yoy in September, above expectation of 4.0% yoy. German Gfk consumer sentiment dropped 0.1 to 10.7 in November. UK CBI reported sales dropped to -36 in October. New Zealand trade deficit narrowed slightly to NZD 1143M in September. Australia import price index dropped -1.6% qoq in Q3. Japan corporate service price index rose 0.9% yoy in September.

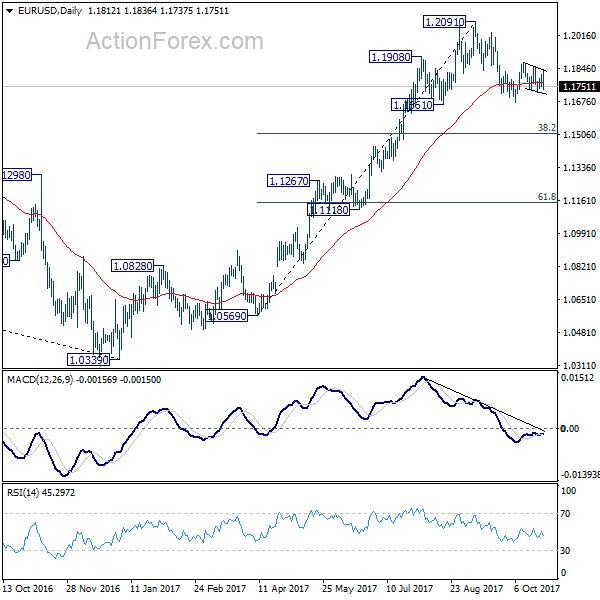

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1770; (P) 1.1794 (R1) 1.1835; More...

EUR/USD drops sharply after ECB announcement. But it's staying in range of 1.1669/1879 and intraday bias remains neutral at this point. On the downside, break of 1.1669 will resume the corrective fall from 1.2091 to 38.2% retracement of 1.0569 to 1.2091 at 1.1510. We'd expect strong support from there to complete the correction. On the upside, break of 1.1879 will revive the case that pull back from 1.2091 has already completed at 1.1669. In such case, intraday bias will be turned back to the upside for retesting 1.2091 high.

In the bigger picture, rise from medium term bottom at 1.0339 is not finished yet. It's expected to continue after pull back from 1.2091 completes. And, next target will be 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. However, it should be noted that there is no confirmation of trend reversal yet. That is, such rebound from 1.0399 could be a correction. And the long term fall from 1.6039 (2008 high) could resume. Hence, we'd be cautious on strong resistance from 1.2516 to limit upside.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Trade Balance (NZD) Sep | -1143M | -900M | -1235M | -1179M |

| 23:50 | JPY | Corporate Service Price Y/Y Sep | 0.90% | 0.80% | 0.80% | |

| 00:30 | AUD | Import Price Index Q/Q Q3 | -1.60% | -1.50% | -0.10% | |

| 06:00 | EUR | German GfK Consumer Confidence Nov | 10.7 | 10.8 | 10.8 | |

| 08:00 | EUR | Eurozone M3 Y/Y Sep | 5.10% | 5.00% | 5.00% | |

| 10:00 | GBP | CBI Realized Sales Oct | -36 | 14 | 42 | |

| 11:45 | EUR | ECB Rate Decision | 0.00% | 0.00% | 0.00% | |

| 12:30 | EUR | ECB Press Conference | ||||

| 12:30 | USD | Wholesale Inventories Sep P | 0.30% | 0.40% | 0.90% | 0.80% |

| 12:30 | USD | Initial Jobless Claims (OCT 21) | 233K | 236K | 222K | 223K |

| 12:30 | USD | Advance Goods Trade Balance (USD) Sep | -64.1B | -63.8B | -62.9B | -63.3B |

| 14:00 | USD | Pending Home Sales M/M Sep | 0.60% | -2.60% | ||

| 14:30 | USD | Natural Gas Storage | 51B |

GBP/JPY Continuation Triangle Formed at 50.0 Fib Level

The GBP/JPY has formed a continuation triangle. The entry that was made on LIVE webinar provided more than 50 pips and the price is consolidating above the POC zone now. The POC 149.70-95 could spike the price up again but 149.15 needs to stay firm. In the case of deeper retracement 149.40 should provide support and short term buying opportunities too. Above 150.28 we might see a continuation towards 150.83, 151.07 and 151.43. Only if the price breaks above 151.43 we could see 151.78 and 152.00 in upcoming days. Below 149.15 the price might break out to 148.72 and 148.57 that will put the pair in neutral mode again.

- H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

- W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

- D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

- D L3 - Daily Camarilla Pivot (Daily Support)

- D L4 - Daily H4 Camarilla (Very Strong Daily Support)

- PPR - Progressive Polynomial Channel

- POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

Summary of the 19th Communist Party of China National Congress

There were a few key takeaways from the 2017 edition of China's twice-a-decade National Congress. Largely a political event, there were appointments of party members to more senior positions in the Communist Party of China's (CPC) inner circle. Most interesting was President Xi's vision for China, including a list of policy initiatives aimed at making China's economy more open, innovative, equitable, and sustainable.

Political developments

President Xi Jinping saw his leadership solidified and status elevated as the CPC incorporated his self-titled doctrine "Xi Jinping Thought on Socialism with Chinese Characteristics for a New Era" into its constitution. Other leaders to have their names enshrined in the constitution in this manner include Mao Zedong and Deng Xiaoping.

Breaking with convention, the CPC chose not to make a strong statement on a potential successor to President Xi by failing to appoint more youthful party members to its inner circle. The CPC maintains a retirement age of 68 for its top leaders.

A refusal to map out a clear successor has opened up speculation that President Xi may remain in a position of influence even after his customary two five-year terms end in 2022. Although the Chinese constitution limits him to two consecutive terms as president, he may seek another high-level role in the CPC and serve as a guide to the newly appointed President.

Economic Policies

President Xi's opening speech last Wednesday referred to a number of initiatives to improve upon China's prosperity and his vision to make China a global power by 2050. To achieve this, he outlined some broad goals. Near term goals include achieving a thriving middle class by 2020, while medium term goals targeting improvements to the quality of life for the average Chinese citizen. This includes efforts to promote a clean environment, and an expansion in public services. Longer-term goals involve the promotion of a patriotic culture and strengthening national security by achieving a first-class military by 2050.

The adoption of these tenants in the CPC constitution suggest a gradual shift away from one of growth at any cost to a more balanced approach that places gains in material wealth at an almost equal footing as achieving social prosperity. This change has largely been interpreted as acceptance by the CPC of lower economic growth in the future in order to maintain social harmony.

President Xi's vision also affirms China's outward expansion, including investments in projects such as the Belt and Road initiative that focus on expanding trade routes, and consequently Chinese influence, throughout Asia and westward into Europe. In addition, the longer-term focus on strengthening national security implies more defense spending aimed at building its air and naval capabilities in order to deter territorial challenges from neighbouring nations.

The affirmation of policies focused on open and innovative economic development suggests an emphasis on increasing research and development expenditures to continue efforts to move up the value chain and follow the evolution of neighbouring South Korea and Japan toward advanced economy status. President Xi has set 2035 as a target for China in joining the ranks of the most innovative nations.

China's repeated its commitment to adopting market-oriented reforms. This includes greater efforts to allowing market forces to determine resource allocation, with the implication that domestic prices from now on should be more representative of market conditions. Moreover, this commitment remains consistent with China's determination to eventually allow global markets to determine China's exchange rate as it strives to open itself to more foreign investment in the years ahead.

Lastly, China remains committed to supply-side structural reforms, including reducing industrial overcapacity and restructuring bad debts in its corporate and banking sectors. China's explosive debt growth over the past decade has raised concerns that a China-driven deleveraging episode may be the event that triggers the next economic downturn globally. Debt restructuring will remain a key strategy that China employs to reduce its financial fragility implied by its elevated debt levels across all sectors.

Canadian Dollar Slips as BoC Holds Off

The Canadian dollar has paused in the Thursday session, after sharp losses on Wednesday. Currently, USD/CAD is trading at 1.2793, down 0.03% on the day. On the release front, there are no Canadian releases on Thursday. The US releases two key indicators – unemployment claims and Pending Home Sales. On Friday, the US releases Advance GDP and the UoM Consumer Sentiment.

There were no surprises from the Bank of Canada, which maintained the benchmark rate at 1.00 percent. In its rate statement, the Bank noted that wage growth levels remain weak, as there is slack in the labor market. Inflation pressure from wage growth remains muted, but the Bank did not provide a reason why inflation levels are so low. This problem is apparent south of the border as well, where a robust US economy and red-hot labor market has not translated into higher inflation. The cautious tone of the BoC did not impress investors, and the Canadian dollar shed close to 1.0 percent on Wednesday after the rate announcement.

Who will win the race to take over at the Federal Reserve? Janet Yellen's 3-year term concludes in February 2018, and President Trump has said he will nominate a new Fed in the next few days. The front runners are economist John Taylor and Federal Reserve Governor Jerome Powell. Taylor advocates a rule in which rates which be as high as 3 percent, given current economic conditions. Powell is more closely aligned to Fed Chair Janet Yellen's monetary stance which advocates an incremental increase in rates. With the two candidates representing sharply differing views on interest rate levels, Trump's choice for the new Fed chair could have a significant effect on monetary policy and the strength of the US dollar. If Taylor gets the nod, the US dollar could respond with gains of 3 percent or more.

EURUSD Bullish above 1.1800 Level

The euro continues to advance against the U.S dollar in Thursday trading, with price-action moving towards the top-end of the euros recent 1.1724-1.1879 trading range. The EURUSD currently trades around the 1.1825 level, as financial markets await the European Central Bank's monetary policy decision later today, in Frankfurt, Germany.

The EURUSD pair remains bullish on an intraday basis while trading above the 1.1800 level. Further upside can be expected while above 1.1800, with buyers likely to target the 1.1879 and 1.1910 levels. Extended intraday resistance for the euro is located at 1.1980 and 1.2040.

If EURUSD sellers push price-action below the 1.1800 level, further declines towards 1.1770 and 1.1724 can be expected. Extended intraday support for the euro is found at the 1.1664 and 1.1580 levels.