Sample Category Title

USDJPY Bullish Above 113.72 Level

The U.S Dollar has recovered losses against the Japanese Yen during the European session, hitting 113.75, as the U.S dollar index moves higher across the board, recovering steep trading losses from Wednesday. Price-action currently trades around the 113.73 level on the USDJPY pair, as traders test intraday supply and demand around the key 113.70 technical region.

The USDJPY pair remains bullish while trading above the 113.72 level, further upside can be expected while above the 113.72 level, with buyers likely pushing price action towards the 113.89 and 114.13 technical levels.

Should USDJPY buyers fail to hold price-action above the 113.72 level, a continuation of yesterday's bearish move can be expected towards the 113.40 and 113.23 levels.

(ECB) Monetary Policy Decisions

At today's meeting the Governing Council of the ECB took the following monetary policy decisions:

(1) The interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility will remain unchanged at 0.00%, 0.25% and -0.40% respectively. The Governing Council continues to expect the key ECB interest rates to remain at their present levels for an extended period of time, and well past the horizon of the net asset purchases.

(2) As regards non-standard monetary policy measures, purchases under the asset purchase programme (APP) will continue at the current monthly pace of €60 billion until the end of December 2017. From January 2018 the net asset purchases are intended to continue at a monthly pace of €30 billion until the end of September 2018, or beyond, if necessary, and in any case until the Governing Council sees a sustained adjustment in the path of inflation consistent with its inflation aim. If the outlook becomes less favourable, or if financial conditions become inconsistent with further progress towards a sustained adjustment in the path of inflation, the Governing Council stands ready to increase the APP in terms of size and/or duration.

(3) The Eurosystem will reinvest the principal payments from maturing securities purchased under the APP for an extended period of time after the end of its net asset purchases, and in any case for as long as necessary. This will contribute both to favourable liquidity conditions and to an appropriate monetary policy stance.

(4) The main refinancing operations and the three-month longer-term refinancing operations will continue to be conducted as fixed rate tender procedures with full allotment for as long as necessary, and at least until the end of the last reserve maintenance period of 2019.

The President of the ECB will comment on the considerations underlying these decisions at a press conference starting at 14:30 CET today.

Market Update – European Session: Awaiting ECB On Its QE Policy

Notes/Observations

ECB seen implementing a slower but longer” QE extension designed to reinforce the low-for-long rates guidance

Sweden Riksbank keeps policy steady (as expected) and awaits the ECB move before deciding its own QE outlook

Spain Q3 Unemployment Rate hits its lowest level since Q4 2008 (16.4% v 16.6%e)

Overnight

Asia:

South Korea Q3 Preliminary GDP Q/Q: 1.4% v 0.8%e; Y/Y: 3.6% v 3.0%e (fastest quarterly pace since Q2 2010)

China Communist Party Seniorr Official Yang Weimin: China will no longer set a target to double GDP from 2021, emphases on quality of growth

North Korea official warns that hydrogen bomb threat should be taken literally

Europe:

EU govts reportedly have agreed to begin preparations for scenario where Brexit talks fail

EU officials said to put any Brexit transition period limited to 20 months citing the end of the EU budget timeline and potentially lining up better with certain annual quotas

Ireland Fin Min Donohoe: insufficient progress on tracker mortgages could lead to targeted action. Tax law for bank may be amended

British Retail Consortium (BRC) retailers are cutting production at the fastest rate since 2008. Q3 employment -3% y/y; total hours worked -4.2% y/y (**Note: both figures are the steepest falls since BRC started collecting records in 2008)

Catalan Parliament to meet late Thursday. Reports circulating that Catalan President Puigedemont seemed inclined to prepare independence declaration in regional parliamentary session

Americas:

President Trump has reportedly removed Gary Cohn from shortlist for Fed Chairman. Cohn reportedly likely to leave administration after tax reform passes

Brazil Central Bank (BCB) cuts Selic Target Rate by 75bps to 7.50% (as expected) for its 9th straight rate cut

Brazil Chamber of Deputies votes against proceeding with Temer corruption charges (as expected); against votes totaled 251 vs 233

Economic Data

(DE) Germany Nov GfK Consumer Confidence: 10.7 v 10.8e

(NO) Norway Aug AKU Unemployment Rate: 4.1% v 4.2%e

(HU) Hungary Sept Unemployment Rate: 4.1% v 4.1%e

(ES) Spain Q3 Unemployment Rate: 16.4% v 16.6%e (lowest level since Q4 2008)

(SE) Sweden Central Bank (Riksbank) left its Repo Rate unchanged at -0.50% (as expected); maintained Repo Rate path and current QE bond buying program

(EU) Euro Zone Sept M3 Money Supply Y/Y: 5.1% v 5.0%e

(IT) Italy Oct Consumer Confidence: 116.1 v 114.9e; Manufacturing Confidence: 111.0 v 110.0e

(NO) Norway Central Bank (NORGES) left its Deposit Rates unchanged at 0.50% (as expected)

Fixed Income Issuance:

(SE) Sweden sold SEK 750M vs. SEK750M indicated in I/L Jun 2025 bond; Avg yield: -1.4397% v -1.4079% prior; Bid-to-cover: 1.67x v 2.80x prior

(IT) Italy Debt Agency (Tesoro) sold €1.25B vs. €0.75-1.25B indicated in I/L 2028 Bonds (BTPei); Avg Yield: 0.97%; Bid-to-cover: 1.85x

(IT) Italy Debt Agency (Tesoro) sold €3.0B vs. €2.5-3.0B indicated range in new zero coupon Oct 2019 CTZ Bonds; Avg yield: -0.167% v -0.22% prior; Bid-to-cover: 2.02x v 2.0x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 flat at 387.20, FTSE +0.3% at 7465, DAX +0.1% at 12973, CAC-40 +0.2% at 5385, IBEX-35 -0.2% at 10137, FTSE MIB +0.1% at 22476, SMI +0.4% at 9117, S&P 500 Futures -0.1%]

Market Focal Points/Key Themes:

European Indices trade mostly higher ahead of the ECB rate meeting later today. Mixed earnings have capped the move with German heavyweight Bayer down over 3%, while Deutsche Bank also weighs. UK Banking giant Barclays trades sharply lower after weak investment banking results, whilst Nokia trades over 10% lower after weak 2018 guidance. STMicro outperforms on strong results and guidance, with other notable risers including Wirecard, Orange and ABB.

Looking ahead Ford, Southwest, Twitter and American Airlines are some of the notable earners expected this morning.

Equities

Consumer discretionary [AB Inbev [ABI.BE] -2.3% (Earnings)]

Industrials: [ABB [ABBN.CH] +3.1% (Earnings), Ferrovial [FER.ES] +1.5% (Heathrow earnings)]

Financials: [Deutsche Bank [DBK.DE] -1.9% (Earnings), Barclays [BARC.UK] -7.0% (Earnings)]

Technology: [STMicro [STM.FR] +6.4% (Earnings), Fingerprint Cards [FINGB.SE] -15% (Earnings), Wirecard [WDI.DE] +3.7% (Earnings)]

Telecom: [Orange [ORA.FR] +1.4% (Earnings), Telefonica [TEF.ES] -1.5% (Earnings)]

Healthcare: [Bayern [BAYN.DE] -3.3% (Earnings)]

Energy: [Statoil [STL.NO] -3.9% (Earnings)]

Speakers

Sweden Central Bank (Riksbank) policy statement reiterated that its monetary policy needed to remain expansionary for inflation to continue to be close to 2% target. International recovery was continuing, but global inflationary pressures were subdued. Purchases of government bonds (QE program) to continue during the second half of 2017; Awaited further info that could affect a decision in December to possibly extend purchases. Extended the mandate for FX intervention (members Ohlsson and Floden had reservations)

Sweden Central Bank (Riksbank) Gov Ingves post Rate Decision press conference reiterated that policy needed to be expansionary. Inflation was near the 2% target again but too early to make policy less expansionary. Reiterated that SEK currency (Krona) should not appreciate too quickly

Spain Econ Min de Guindos: Economic indicators are good but political crisis could have an impact. Central govt could not accept or allow Catalan secession scenario; such a move would lead to a debacle for the region

Spain govt spokesperson: Received written response from Catalan leader Puigdemont on Article 155 presenting his case against the implementation of Article 155 (just before deadline expired)

Poland Labor Min Rafalska: End-2017 Unemployment Rate seen between 6.8-7.0% area (**Note: Sept Unemployment was 6.8%)

RBA's Debelle: Subdued wage pressure at full employment could happen. Saw sizable spare capacity in labor market

Japan PM Abe: Hopeful of 3% wage hikes in negotiations next spring

Russia Energy Min Novak reiterated his view that is too early to decide on any extension of current production cut agreement

Saudi Arabia Crown Prince Mohammed Bin Salman: Committed to work will all oil producers to balance oil market supply and demand. Backed extending OPEC production cuts into 2018. Reiterated govt view that Saudi Aramco IPO was on track for 2018; noted that the valuation could be over $2T

Currencies

EUR/USD was little changed ahead of the ECB rate decision where the central bank was expected to lay out plans to scale back monetary easing

GBP/USD was softer by 0.3% to probe the lower end of 1.32 after ONS Stats Agency noted that full-time worker weekly earnings (inflation adjusted) was -0.4% in the eyar period ending in April for its 1st drop since 2014.

EUR/SEK cross was initially lower after the Rikebank decision to keep it policy steady. The central bank awaited the ECB outcome before deciding on its oqn QE bond buying extension. EUR/SEK tested 9.68 following the decision but later reversed the move. Dealers noted that real fireworks in volatility could emerge if ECB hinted at the expected timing of any interest rates hike (doubtful that would come at today’s meeting)

Fixed Income

Bund futures trade at 161.26 up 18 ticks, after 10-year yield on US Treasuries tentatively broke below the 2.42%. The focus remains on the ECB rate decision where the consensus is for the ECB to halve bond purchases to €30 billion a month and that asset purchase period will be extended to September 2018. Support lies at 161.00, followed by 160.38. Resistance stands initially at 162.75, followed by 163.51.

Gilt futures trade at 123.59 little changed after initially opening higher. Continued downside eyeing 123.26. Upside targets 124.90 then 125.24.

Thursday’s liquidity report showed Wednesday’s excess liquidity rose to €1.825T from €1.791T and use of the marginal lending facility fell to €133M from €417M

Corporate issuance saw $2.4B come to market via 4 issuers, headlined by AT&T $1.1B senior note offering

Looking Ahead

(GR) ESM to discuss €800M tranche disbursement to Greece

(ES) Catalonia Parliament meets

(AR) Argentina Oct Consumer Confidence: No est v 51.0 prior

(BR) Brazil Sept Central Govt Budget Balance (BRL): -22.8Be v -9.6B prior

05:30 (ZA) South Africa Sept PPI M/M: 0.4%e v 0.4% prior; Y/Y: 4.9%e v 4.2% prior

05:30 (HU) Hungary Central Bank (AKK) to sell combined HUF50B in 2020, 2022 and 2027 Bonds

06:00 (UK) Oct CBI Retailing Reported Sales: 14e v 42 prior

06:00 (BR) Brazil Oct FGV Construction Costs M/M: 0.1%e v 0.1% prior

06:00 (IL) Israel Sept Trade Balance: No est v -$1.2B prior

06:45 (US) Daily Libor Fixing

07:00 (TR) Turkey Central Bank (CBRT) Interest Rate Decision: Expected to leave all key rates unchanged

07:00 (UR) Ukraine Central Bank Interest Decision: Expected to leave Key Rate unchanged at 12.50%

07:00 (BR) Brazil Sept PPI Manufacturing M/M: No est v 0.1% prior; Y/Y: No est v 1.3% prior

07:45 (EU) ECB Interest Rate Decision: ECB expected to keep key rates unchanged; Leave Main Refinance Rate unchanged at 0.00%; Leave Marginal Lending rate unchanged at 0.25%; Leave Deposit Rate unchanged at -0.40%

08:00 (PL) Poland Central Bank (NBP) Oct Minutes

08:05 (UK) Baltic Dry Bulk Index

08:30 (US) Sept Advance Goods Trade Balance: -$64.0Be v -$63.3 prior (revised from -$62.9B)

08:30 (US) Sept Preliminary Wholesale Inventories M/M: 0.4%e v 0.9% prior, Retail Inventories M/M: No est v 0.7% prior

08:30 (US) Initial Jobless Claims: 235Ke v 222K prior; Continuing Claims: 1.89Me v 1.888M prior

08:30 (US) Weekly USDA Net Export Sales

08:30 (BR) Brazil Sept Current Account: -$0.3Be v -$0.3B prior; Foreign Direct Investment (FDI): $6.0Be v $5.1B prior

08:30 (EU) ECB chief Draghi post rate decision press conference

09:00 (RU) Russia Gold and Forex Reserve w/e Oct 20th: No est v $427.0B prior

09:00 (MX) Mexico Sept Trade Balance: -$1.3Be v -$2.7B prior

10:00 (US) Sept Pending Home Sales M/M: +0.4%e v -2.6% prior; Y/Y: -4.2%e v -3.1% prior

10:00 (BR) Brazil to sell Fixed Rate 2023 and 2027 Bonds

10:00 (BR) Brazil to sell 2018, 2019 and 2021 LTN Bills

10:30 (US) Weekly EIA Natural Gas Inventories

11:00 (US) Oct Kansas City Fed Manufacturing Activity: 17e v 17 prior

12:00 (CE) Canada to sell 10-Year Bonds

13:00 (US) Treasury to sell 7-Year Notes

Pending ECB Decision Primes Investors

Anticipation is mounting across the financial markets today, ahead of what many consider as one of the European Central Bank's most significant policy meetings this year.

Markets are widely expecting the ECB to finally announce a reduction of its monthly bond buying at October's policy meeting – something that is seen as a big step towards the end of easy money. The million-dollar question is; by how much will the monthly purchase be reduced, and how long will tapering last. This has investor expectations running rampant, and we could see some fireworks today.

The gossip in the markets is that the ECB may reduce monthly purchases, to around 30/40 billion euros per month from the current 60 billion, starting from January. With regards to the duration, markets are expecting the bond-buying program to be extended by roughly six to nine months, after the current program ends at the end of 2017. Investors should keep in mind that although the macroeconomic landscape in Europe remains encouraging, inflation is still below the golden 2% target and as such, is likely to impact today's ECB meeting.

Let's not forget about Mario Draghi, who will be closely scrutinized by investors on his tone and thoughts about the Euro. With ECB policy makers still expressing concerns over the Euro's strength, Draghi could seize this opportunity to keep Euro bulls at bay, by adopting a dovish tone. With there being many potential outcomes to the pending ECB meeting, the Euro could turn volatile against its counterparts.

Taking a look at the technical picture, the EURUSD remains in a wide range on the daily charts, with 1.1850 acting as a key level of interest. A breakout above this level may encourage a further incline higher towards 1.1920. In an alternative scenario, sustained weakness below 1.1850 could trigger a decline back towards 1.1730.

DAX Edges Higher Ahead Of ECB Stimulus Decision

The DAX has posted slight gains in the Thursday session, as the index remains close to the symbolic 13,000 level. Currently, the DAX is at 12,998.00, up 0.26%. On the release front, German GfK Consumer Climate edged lower to 10.7, close to the forecast of 10.8 points. The ECB will release its rate statement, and is expected to taper its asset purchase program. On Friday, Germany will publish Import Prices, while the US releases Advance GDP.

The ECB holds a crucial policy meeting on Thursday. The Bank is expected to maintain interest rates at a flat 0.00%, but could significantly trim the ECB’s asset purchase program (QE). Currently, the ECB is purchasing EUR 60 billion/mth, and there is a strong likelihood that this amount will drop to EUR 30 billion/mth. The stronger eurozone economy is the catalyst behind a taper, but with inflation persistently at low levels, the ECB is expected to announce to extend the program well into 2018 or even later. Eurozone members remain divided as to whether the ECB should signal that it plans to wind up QE. Germany and the Netherlands are in favor of a quick exit, but other members want the scheme to remain open-ended, so that the ECB can continue with extensions, if needed. ECB policymakers will need to perform a balancing act between these views as it shifts its monetary policy.

German Ifo Business Climate jumped to 116.7, an all-time high. The business sector is very optimistic about the robust economy, and does seems unfazed by German coalition talks and the deadlock in the Brexit talks. The strong reading suggests that the German economy will enjoy a strong fourth quarter. German policymakers insist that the ECB’s interest rate policy is too loose for Germany, but the economy is still expected to thrive. Earlier in the week, German Manufacturing PMI posted a strong reading of 60.5, beating expectations. The manufacturing sector continues to expand, buoyed by strong domestic demand and the global appetite for German exports.

CRUDE OIL Pushing Towards Key Resistance

Crude oil is consolidating within range defined by support at 50.43 and the strong resistance lies at 52.86 (28/09/2017). Expected to show continued increase within this range.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. For the time being the pair lies in an upside momentum. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).

SILVER Riding Lower

Silver is again grinding lower. Hourly support can be founds at 16.88. Hourly resistance is given at 17.46 (13/10/2017 high). Additional support can be found at 16.13 (06/10/2017 low).

In the long-term, the trend is rater negative. Further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

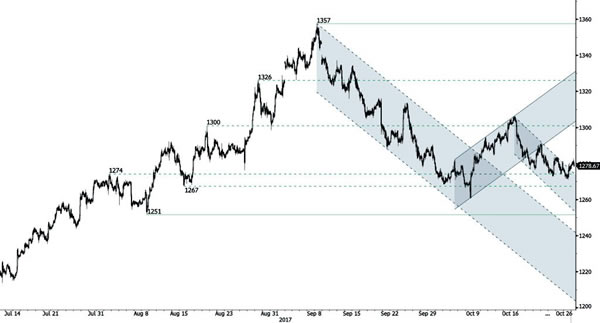

GOLD Exiting Downtrend Channel

Gold remains weak. The precious metal has exited downtrend channel. The technical structure confirms an underlying bearish trend. Strong support lies at a distance at 1267 then 1204 (10/07/2017 high). Resistance is now located at 1288 (20/10/2017).

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

BITCOIN Bouncing Higher Within Uptrend Channel

Bitcoin remains weak as long as prices remains below the key resistance at 6063. Strong support stands very far at 2975 (22/08/2017 low). However with rising trend unbroken road is wide open for further bullish momentum. Support can be located at 5325 (rising trendline). In the shortterm, the digital currency should monitor $6000.

In the long-term, the digital currency has had an exponential growth. There are decent likelihood that the asset will reach $10'000.

EUR/CHF Breaking Uptrend Channel

EUR/CHF has broken uptrend channel indicating strong bullish pressures. Support is given at 1.1640 (25/10/2017 low). Rising channel suggests further bullish momentum.

In the longer term, the technical structure has reversed. Strong resistance is given at 1.20 (level before the unpeg). Yet, the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).