Sample Category Title

US: Payrolls Slow in January, But California Wildfires and Cold Weather Likely a Factor

Non-farm payrolls rose 143k in January, slightly below the consensus forecast calling for a gain of 170k.

- This morning's report also included more comprehensive benchmark revisions, which are done annually to better align the establishment survey figures to observed employment counts reported in tax filing data. The revisions showed the level of employment as of March 2024 was lower by 589k.

- The Bureau of Labor Statistics also revised its seasonal adjustment factors (dating back to 2020) as well as the birth/death factors used to scale payroll changes up or down depending on the estimated rate of firm formation. These revisions showed that payroll growth between April 2024 – December 2024 was revised slightly lower by a total of 21k jobs. However, revisions through the fourth quarter were notably higher (adding an additional 101k jobs to the previously reported figures), suggesting more hiring momentum heading into 2025.

Private payrolls rose 111k – notably lower than the 273k reported in December – with the largest gains seen in health care & social assistance (+66k) and retail trade (+34.3k). Government hiring rose 32k.

In the household survey, new population controls were introduced last month (as is the case every January), to reflect new population estimates from the Census Bureau. Unlike the establishment survey, the historical household data is not revised, distorting the month-to-month changes for civilian employment, unemployment, and the labor force. However, the ratios in the survey (i.e., the unemployment and participation rates) remain largely unaffected.

- Civilian population was revised higher by 2.9 million in January, as prior population estimates have significantly undercounted immigration flows in recent years.

- The unemployment rate ticked lower by 0.1 percentage points to 4.0%, while the labor force participation rate edged up to 62.6%.

Average hourly earnings rose 0.5% month-on-month (m/m) in January – an acceleration from December's more modest gain of 0.3%. On a twelve-month basis, wage growth was up 4.1% (unchanged from the month prior), while the three-month annualized edged up to 4.5% (from 4.3% in December).

Key Implications

There was a lot to digest in this report. But perhaps the biggest takeaway was that hiring momentum was even stronger than previously expected at the end of last year – averaging 204k jobs per-month in the fourth quarter. And even though the January figures showed some deceleration in payrolls, it was likely due to wildfires in California and cold weather across much of the U.S. – suggesting we could see some bounce back in February.

While it was previously thought that that labor market had fallen into a sweet spot, this morning's release suggests things are still running a bit hotter than previously expected. The unemployment rate dipped to an eight-month low, while wage growth has shown more staying power. With inflation progress having stalled in recent months and heightened uncertainties on how far the new administration will go on tariffs, the Fed is likely to remain more cautious on rate cuts and hold the policy rate steady until sometime this summer.

Another Positive Surprise for Canada’s Job Market in January

The Canadian labour market's solid job gains carried over into 2025, with 76k new jobs beating expectations. Job gains were split between full (+42.3k) and part-time (+38.6k) positions.

The healthy job gain pushed the unemployment rate down another 0.1 percentage point to 6.6%.

Following a period where labour force growth was outpacing job creation, the proportion of the population aged 15+ with a job has now risen for three consecutive months. And this has occurred across age cohorts: youth (15-24 years), core age (25-54 years) and older people (55-64) have all seen their employment rates rise.

Employment gains across industries were mixed. Gains were led by manufacturing (+33k), professional, scientific and technical services (+21.7k), construction (+19.3k) and accommodation and food services (+14.9k). Meanwhile, other services (-13.9k), educational services (-7.9k) and business building and other support services (-7.4k) led the declines.

Given the threat of tariffs in the spotlight, Statistics Canada included a feature on manufacturing employment, which accounts for 8.9% of total employment in Canada. Specifically, 39.4% of manufacturing jobs depend on U.S. demand for Canadian exports, or roughly 641k jobs.

Lastly, total hours worked jumped a massive 0.9% month-on-month, pointing to solid economic growth on the month. Meanwhile wage inflation continued to cool. Average hourly wages were up 3.5% year-on-year in January (from 4.0% in December).

Key Implications

Three consecutive months of solid job growth suggests the cyclical boost to Canada's economy from lower interest rates is clearly taking effect. Unfortunately, the imminent threat of tariffs hanging over the Canadian economy, is likely to temper business confidence and could weigh on hiring in some sectors in the coming months.

The Bank of Canada continued to lower interest rates in January, such that interest rates are no longer a drag on the economy. Now it is over to Canadian governments to do what they can (see commentary) to improve the competitiveness of the economy in the face of the tariff threat.

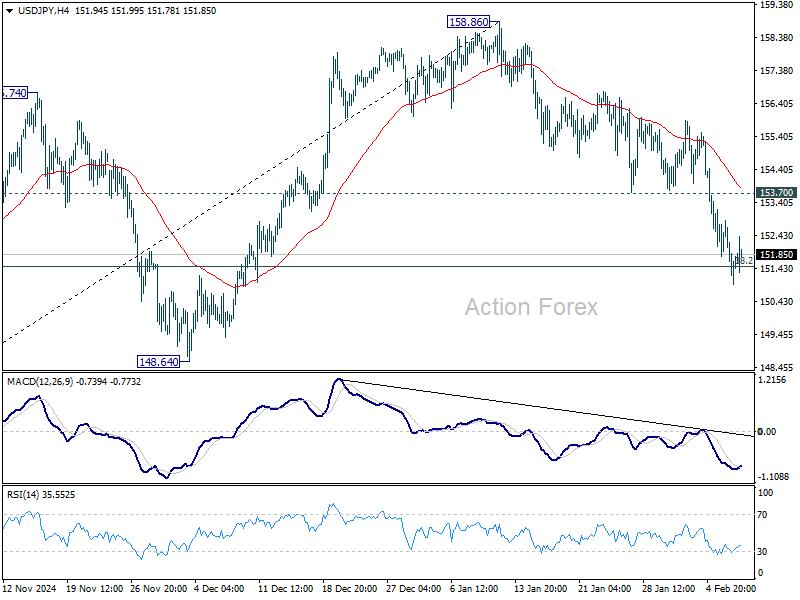

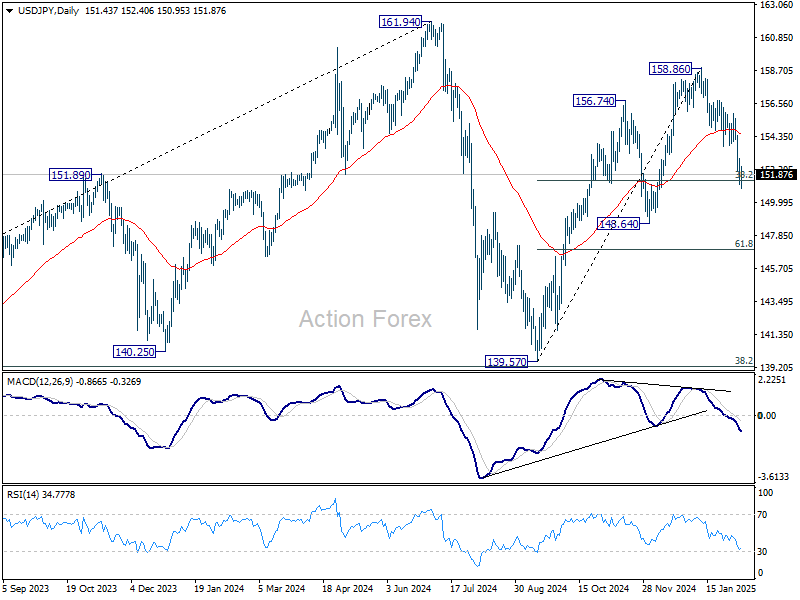

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 150.83; (P) 151.86; (R1) 152.48; More...

Intraday bias in USD/JPY is turned neutral with 4H MACD crossed above signal line. Focus stays on 38.2% retracement of 139.57 to 158.86 at 151.49. Strong bounce from current level will keep decline from 158.86 as a correction, and retain near term bullishness. Firm break of 153.70 support turned resistance will turn bias back to the upside for stronger rebound. However, sustained break of 151.49 will raise the chance of bearish reversal, and target 61.8% retracement at 146.32 next.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

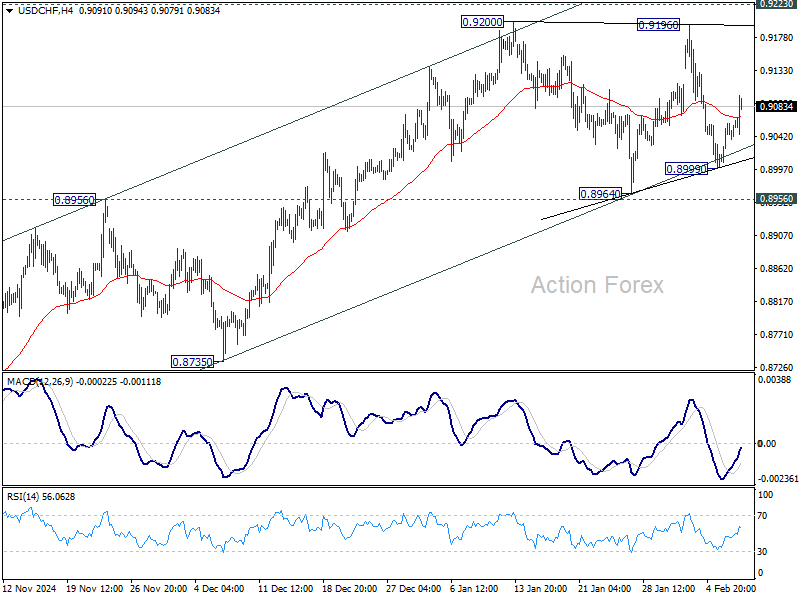

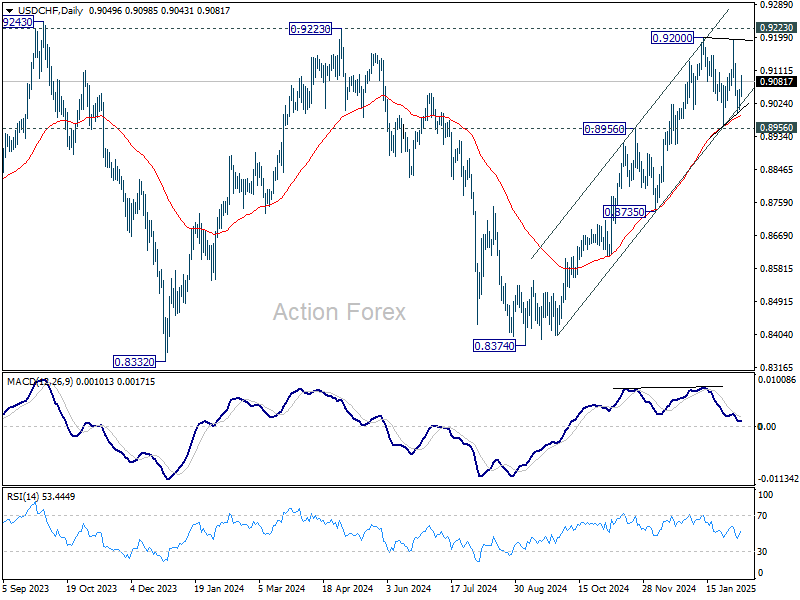

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9015; (P) 0.9038; (R1) 0.9074; More…

Intraday bias in USD/CHF stays neutral at this point. Consolidation from 0.9200 could extend further. Outlook will remain bullish as long as 0.8956/64 support holds. Firm break of 0.9200/9223 will resume the whole rally from 0.8374 and carry larger bullish implication. However, sustained break of 0.8964 will complete a double top reversal pattern, and turn bias to the downside for deeper decline.

In the bigger picture, decisive break of 0.9223 resistance will argue that whole down trend from 1.0342 (2017 high) has completed with three waves down to 0.8332 (2023 low). Outlook will be turned bullish for 1.0146 resistance next. Nevertheless, rejection by 0.9223 will retain medium term bearishness for another decline through 0.8332 at a later stage.

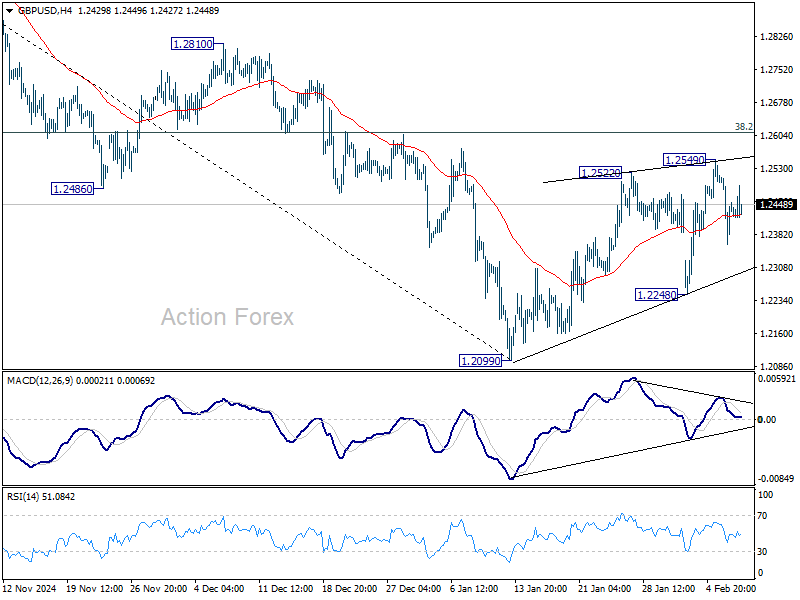

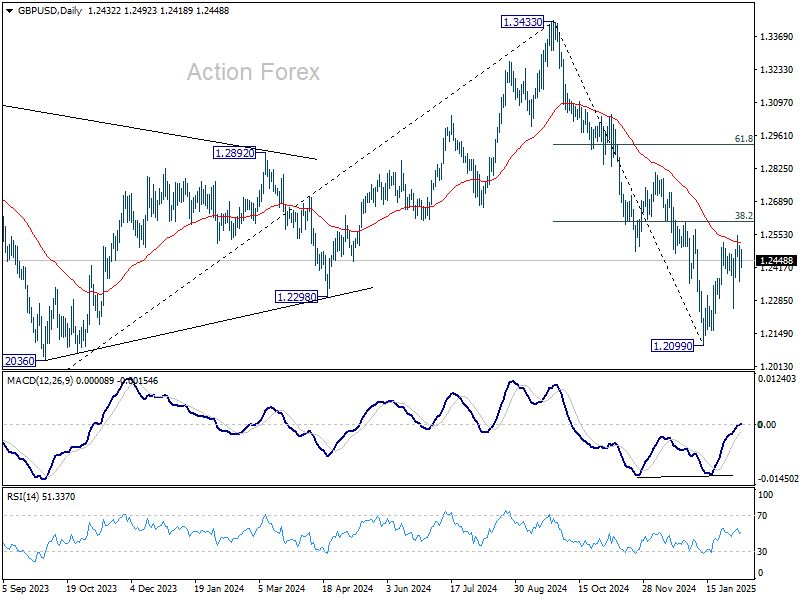

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2360; (P) 1.2437; (R1) 1.2511; More...

Intraday bias in GBP/USD stays neutral for the moment. While corrective rebound from 1.2099 could still extend, upside should be limited by 38.2% retracement of 1.3433 to 1.2099 at 1.2609. On the downside, break of 1.2248 support will bring retest of 1.2099 first. Firm break there will resume whole decline from 1.3433. However, decisive break of 1.2609 will raise the chance of near term reversal, and target 61.8% retracement at 1.2923.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433 (2024 high), and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move. However, firm break of 1.2810 will dampen this bearish view and bring retest of 1.3433 high instead.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0355; (P) 1.0381; (R1) 1.0410; More...

EUR/USD dips mildly but stays well inside range of 1.0176/0531. Intraday bias remains neutral and more consolidations could be seen. Strong resistance is expected from 1.0531 to limit upside. On the downside, break of 1.0176 will resume whole fall from 1.1213. However, sustained break of 1.0531 will rise the chance of bullish reversal and turn bias back to the upside for stronger rally.

In the bigger picture, immediate focus is back on 61.8 retracement of 0.9534 (2022 low) to 1.1274 (2024 high) at 1.0199. Sustained break there will solidify the case of medium term bearish trend reversal, and pave the way back to 0.9534. However, strong support from 1.0199 will argue that price actions from 1.1274 are merely a corrective pattern, and has already completed.

Dollar Gains Modestly on NFP, But Lacks Momentum

Dollar edged higher in early US session following the non-farm payrolls (NFP) report, but the overall momentum remains lackluster. Stock futures are flat, while 10-year Treasury yield is staging a slight recovery, suggesting a measured market response as traders hold back from aggressive positioning ahead of next week's key economic events including US CPI and Fed Chair Jerome Powell's testimony.

While headline NFP figure of 143k fell short of expectations, the dip in the unemployment rate to 4.0% and strong wage growth at 0.5% mom have reinforced the Fed’s cautious stance towards further policy easing. Markets now see over 90% chance that Fed will keep rates unchanged in March, while expectations for another hold in May stands at 70%.

Overall, despite today's recovery, Dollar is still trading as the worst performer for the week, followed by Euro, and then Swiss Franc. Yen continues to sit at the top of the ladder, followed by Canadian, and then Aussie. Kiwi and Sterling are mixed in the middle.

In Europe, at the time of writing, FTSE is down -0.18%. DAX is down -0.06%. CAC is down -0.02%. UK 10-year yield is down -0.0014 at 4.489. Germany 10-year yield s up 0.0149 at 2.395. Earlier in Asia, Nikkei fell -0.72%. Hong Kong HSI rose 1.16%. China Shanghai SSE rose 1.01%. Singapore Strait Times rose 0.81%. Japan 10-year JGB yield rose 0.0357 to 1.303.

US NFP grows 143k, wages growth strong

US non-farm payroll job growth fell short of expectations but wage growth exceeding forecasts. Employers added 143k jobs, missing the 169k estimate and coming in below the 2024 monthly average of 166k. However, the downward surprise was offset by a significant upward revision to December’s number, which was adjusted from 256k to 307k.

Unemployment rate unexpectedly dropped from 4.1% to 4.0%. At the same time, the labor force participation rate ticked slightly higher to 62.6%, reinforcing signs of a still-active workforce. While the decline in headline job creation might signal a cooling labor market, the improvement in unemployment suggests that the slowdown is not yet severe.

The standout data point in the report was wage growth, with average hourly earnings surging 0.5% mom, surpassing the expected 0.3% mom increase. On an annual basis, wages rose 4.1% yoy, a sign that businesses are still competing for workers despite moderation in hiring.

Canada's employment grows 76k, unemployment rate down to 6.6%

Canada’s labor market significantly outperformed expectations in January, with employment rising by 76.0k, far exceeding 26.5k forecast. The biggest job gains were seen in manufacturing (+33k, +1.8%) and professional, scientific, and technical services (+22k, +1.1%).

The unexpected strength in employment was further reinforced by decline in the unemployment rate from 6.7% to 6.6%, beating market expectations of a slight uptick to 6.8%.

Despite the surge in hiring, wage growth showed signs of moderation, with average hourly earnings rising 3.5% yoy, down from 4.0% yoy in December. Total actual hours worked rose 0.9% mom, with a 2.2% annual increase.

IMF backs BoJ’s gradual rate hikes, sees policy rate moving toward neutral by 2027

Nada Choueiri, deputy director of IMF’s Asia-Pacific Department and mission chief for Japan, stated that IMF remains “supportive” of BoJ’s current monetary policy course. She emphasized that rate hikes should be implemented in a gradual and flexible manner to ensure that domestic demand continues to recover.

Choueiri projected that BoJ’s policy rate could rise “beyond 0.5%” by the end of this year, with a longer-term path toward the “neutral level” by the end of 2027.

IMF estimates Japan’s neutral rate to be within a band of 1% to 2%, with a midpoint of 1.5%.

Also, IMF maintains an optimistic outlook for Japan’s economy, forecasting 1.1% GDP growth in 2025, supported by increasing wages and stronger consumer spending.

Given these projections, IMF expects BoJ to continue its tightening cycle in a controlled manner.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0355; (P) 1.0381; (R1) 1.0410; More...

EUR/USD dips mildly but stays well inside range of 1.0176/0531. Intraday bias remains neutral and more consolidations could be seen. Strong resistance is expected from 1.0531 to limit upside. On the downside, break of 1.0176 will resume whole fall from 1.1213. However, sustained break of 1.0531 will rise the chance of bullish reversal and turn bias back to the upside for stronger rally.

In the bigger picture, immediate focus is back on 61.8 retracement of 0.9534 (2022 low) to 1.1274 (2024 high) at 1.0199. Sustained break there will solidify the case of medium term bearish trend reversal, and pave the way back to 0.9534. However, strong support from 1.0199 will argue that price actions from 1.1274 are merely a corrective pattern, and has already completed.

Canada’s employment grows 76k, unemployment rate down to 6.6%

Canada’s labor market significantly outperformed expectations in January, with employment rising by 76.0k, far exceeding 26.5k forecast. The biggest job gains were seen in manufacturing (+33k, +1.8%) and professional, scientific, and technical services (+22k, +1.1%).

The unexpected strength in employment was further reinforced by decline in the unemployment rate from 6.7% to 6.6%, beating market expectations of a slight uptick to 6.8%.

Despite the surge in hiring, wage growth showed signs of moderation, with average hourly earnings rising 3.5% yoy, down from 4.0% yoy in December. Total actual hours worked rose 0.9% mom, with a 2.2% annual increase.

US NFP grows 143k, wages growth strong

US non-farm payroll job growth fell short of expectations but wage growth exceeding forecasts. Employers added 143k jobs, missing the 169k estimate and coming in below the 2024 monthly average of 166k. However, the downward surprise was offset by a significant upward revision to December’s number, which was adjusted from 256k to 307k.

Unemployment rate unexpectedly dropped from 4.1% to 4.0%. At the same time, the labor force participation rate ticked slightly higher to 62.6%, reinforcing signs of a still-active workforce. While the decline in headline job creation might signal a cooling labor market, the improvement in unemployment suggests that the slowdown is not yet severe.

The standout data point in the report was wage growth, with average hourly earnings surging 0.5% mom, surpassing the expected 0.3% mom increase. On an annual basis, wages rose 4.1% yoy, a sign that businesses are still competing for workers despite moderation in hiring.

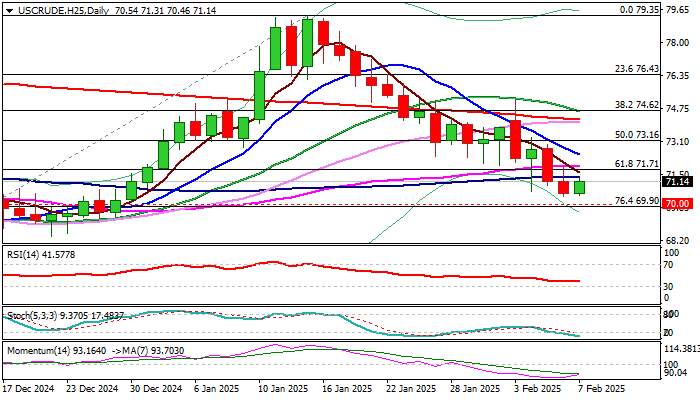

WTI Oil: Larger Bears Taking a Breather Ahead of Key $70.00 Support Zone

WTI oil price edged higher on Friday as larger bears are taking a breather after this week’s strong fall.

Fresh gains were sparked by new US sanctions on Iran’s crude exports, which partially countered strong pressure on oil price from growing fears about US-China trade war and its consequences on global economy.

Recovery was underpinned by rising thin daily cloud, but upticks were so far limited by broken 100DMA ($71.36).

Firmly bearish technical picture on daily chart contributes potential scenario of limited bounce rather to offer better selling opportunities than to mark a more significant correction.

The WTI contract is on track for the third consecutive strong weekly loss that weighs on near-term outlook.

Weekly close below broken Fibo support at $71.71 (61.8% of $66.98/$79.35 rally) to confirm that bears remain firmly in play for attack at next key supports at $70 zone (psychological / Fibo 76.4%), guarding $68.44 (Dec 20 low) and $66.98 (Dec 6 low).

Above 100DMA, significant barriers lay at $71.93 (55DMA) and $72.53 (falling 10DMA).

Res: 73.16; 73.63; 74.29; 74.52.

Sup: 72.01; 71.71; 71.18; 70.00.