Sample Category Title

Markets Weekly Outlook – Inflation Fears Rise with Tariffs Ahead of US CPI Release

- Inflation expectations are rising, driven by tariff concerns and impacting consumer sentiment.

- US job growth was lower than expected, adding to market concerns.

- Key events for the week ahead include the US CPI release and testimony from Fed Chair Jerome Powell.

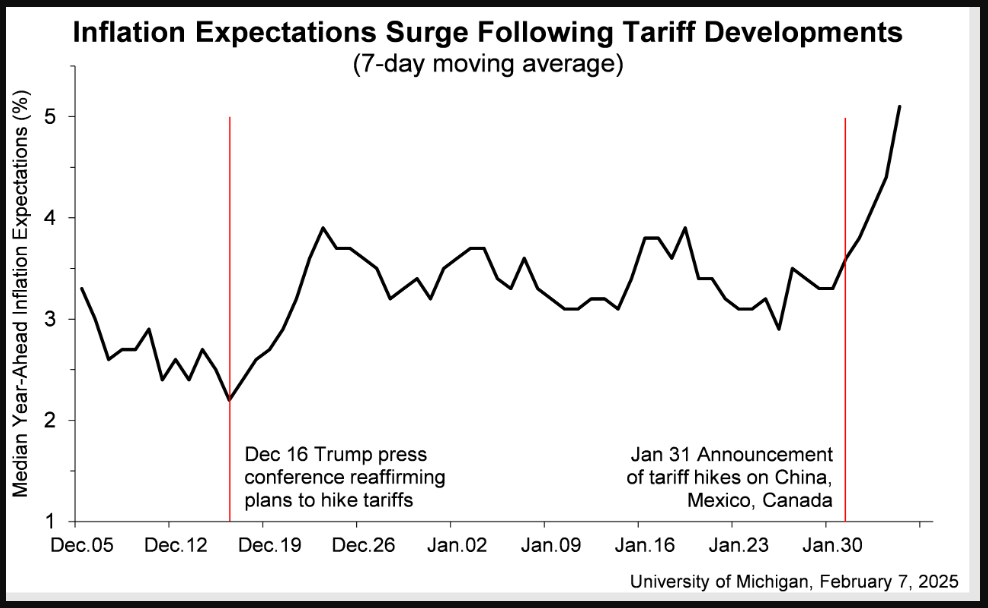

Week in Review: Tariff Fears Sees Inflation Expectations Rise

Markets had an interesting end to the week with a mixed bag of jobs data leaving a lot to be desired. However, in 2025 Fridays have proven anything but disappointing thus far, and this week did not disappoint.

A significant uptick in inflation expectations was seen with the release of the preliminary Michigan consumer sentiment data. Inflation expectations for the next year jumped to 4.3%, the highest since November 2023, up from 3.3%. This is only the fifth time in 14 years that year-ahead inflation expectations have risen by one percentage point or more in a single month.

Many people are worried that high inflation could make a comeback within the next year. Meanwhile, long-term inflation expectations also increased slightly to 3.3%, the highest since June 2008, up from 3.2%.

Source: University of Michigan

There was also an impact on the overall sentiment, with the report showing sentiment in the US dropped to 67.8 in February 2025 from 71.1 in January. This was below expectations of 71.1. It marks the second month of declines, with sentiment hitting its lowest level since July 2024.

The current economic conditions index fell to 68.7 from 74, while the expectations index also dropped to 67.3 from 69.3. Additionally, views on buying durable goods fell by 12%, partly because many believe it’s too late to avoid the negative effects of tariff policies.

This news actually had a bigger impact on the markets than the actual NFP and jobs report which was highly anticipated.

The Labor Department reported that the U.S. economy added 143,000 jobs in January, which was less than the 170,000 jobs economists had predicted. The unemployment rate was 4%, slightly better than the expected 4.1%. However, the data also showed that the economy created 598,000 fewer jobs in the year up to March than previously estimated.

In the aftermath of the data releases we saw the US indices surrender the initial gains made to trade lower on the day. The S&P 500 was down around 0.83% while the Nasdaq was trading down around 1.15%.

My take on the data is that there is just enough in the data to stoke some concern in the minds of market participants.

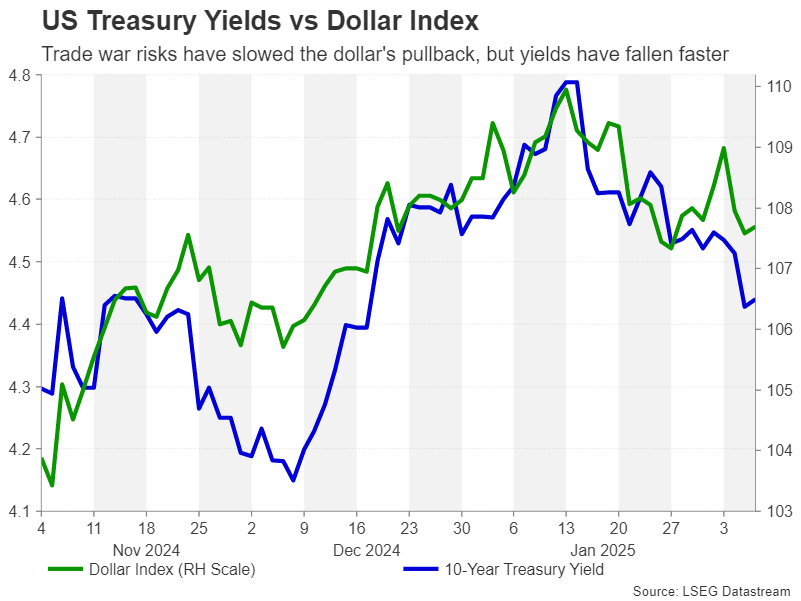

On the FX Front, there was a solid end to the week for the US Dollar Index (DXY) after the rise in inflation expectations. The Dollar looked on course to end the week with a whimper before finishing the week strong and dragging all dollar denominated majors lower.

EUR/USD and GBP/USD both struggled on Friday with cable in particular surrendering some of its weekly gains.

Gold rose to print fresh all time highs once more before falling hard following the Michigan data release as well. Gold surrendered its all time high at 2886 before trading at 2858 at the time of writing.

Oil on the other hand enjoyed a rather mixed week but is set to conclude its third consecutive week of losses with Brent trading at 75.00 at the time of writing. Fear around Iranian sanctions were overcome by tariffs and how they may impact growth and thus global demand.

Weakening Oil demand remains an even greater concern following the arrival of the Trump administration and a period of tariff uncertainty.

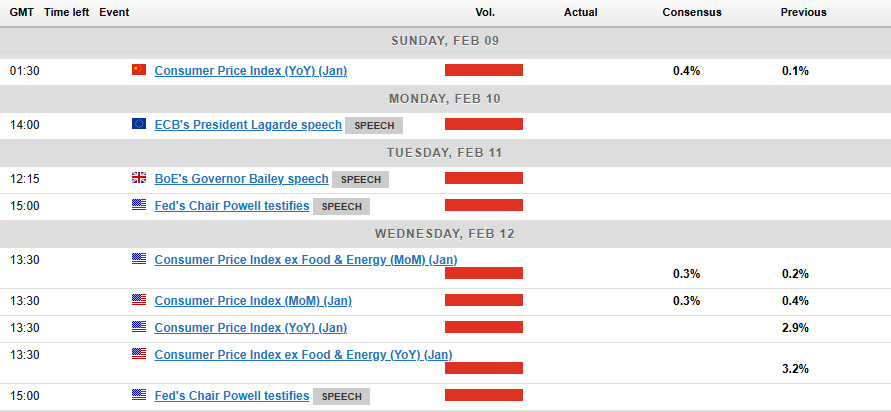

The Week Ahead: US CPI and Powell Testimony to Dominate

Asia Pacific Markets

The main focus this week in the Asia Pacific region is tariff developments and inflation data from China.

From China, the key event to watch is whether China and the US hold high-level talks soon. Currently, the US has added 10% tariffs on Chinese goods, though exemptions for items in transit mean the impact may take time.

China plans to impose its own tariffs on February 10, leaving a short window for potential negotiations to ease tensions. President Trump did say on Friday that he will probably meet Xi Jinping soon but no date has been given as yet.

On the data side, China will release January’s CPI inflation on Sunday. A slight increase to 0.4% YoY is expected, driven by higher food prices from the Lunar New Year, while non-food inflation is likely to stay low. The People’s Bank of China will also report January’s credit activity data next week.

Europe + UK + US

In developed markets, the US CPI release and testimony from Fed Chair Jerome Powell will dominate proceedings. We will also get a glimpse into the growth picture for both the UK and EU this week. GDP growth continues to plague the Euro Area, with Eurozone GDP Preliminary data being released on Friday.

US inflation data is expected to show a 0.3% monthly rise in both headline and core measures. Food and energy costs, housing prices, and rising vehicle prices are driving this increase. While tariffs have been paused for now, there’s a chance they could return later this year, keeping inflation high. This makes it unlikely the Fed will cut rates before June.

Fed Chair Jerome Powell will testify to Congress as the Fed releases its semi-annual monetary policy report. I expect the report to touch on the uncertainty caused by Trump’s policies but confirm that further rate cuts depend on economic data. Despite Trump’s initial rhetoric of pressure on the Fed, recent suggestions by his administration is that such a move is unlikely.

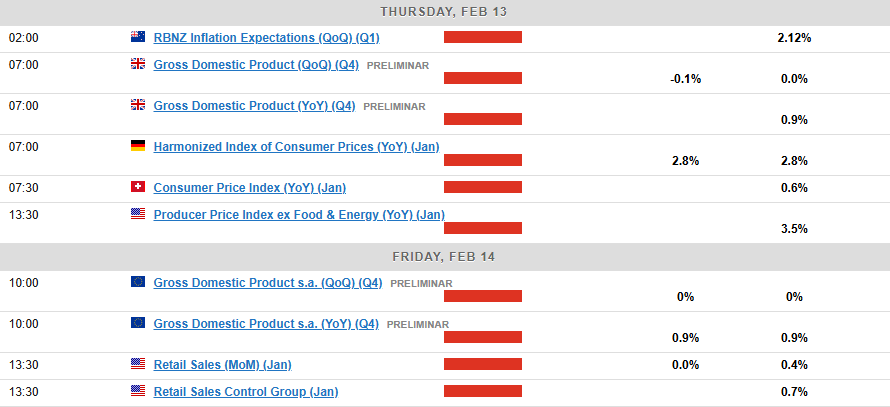

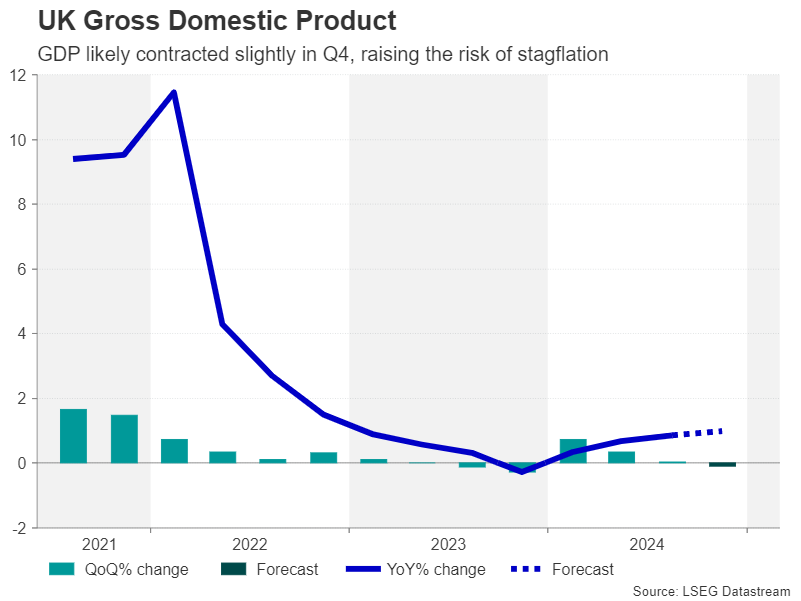

UK GDP data is due on Thursday with growth likely to have slowed in the second half of last year, and fourth-quarter GDP likely flat. Growth may improve in 2025 due to higher government spending, but it’s expected to fall short of the 2% forecast by the Office for Budget Responsibility. This, along with potential data revisions, adds pressure to the Treasury’s March Spring Statement, especially as rising debt costs have reduced fiscal flexibility.

Chart of the Week – US Dollar Index (DXY)

This week’s focus is on the US Dollar Index (DXY) after it recovered late on Friday and is looking like it is ready to print a fresh high.

The rising inflationary expectations may get a nod if US CPI comes in higher than expected, while any new tariff announcements will likely add to the USDs appeal.

Looking at the technical picture, the DXY has printed a higher low on the daily timeframe hinting at the possibility of a change in structure. The daily candle on Friday is struggling to close above the key 108.00 resistance level however, with a close above likely to give bulls confidence that further gains may materialize.

Failure to do so could see the DXY retest the 107.00 handle in the early part of next week which may add a further dimension to the US CPI release.

US Dollar Index Daily Chart – February 7, 2025

Source:TradingView.Com (click to enlarge)

Key Levels to Consider:

Support

- 107.00

- 106.13

- 105.63

Resistance

- 108.49

- 109.52

- 110.00

The Weekly Bottom Line: Tariffs On, Tariff Off, Tariffs On?

Canadian Highlights

- President Trump kept most Canadians glued to their TVs/socials this week, announcing tariffs to take effect February 1st, before quickly delaying them for 30 days following a big market selloff and further measures at the border from Canada.

- Canadian trade data came in quite positive in December as firms appear to be frontrunning potential tariffs. Exports for the fourth quarter of 2024 are now tracking double digit growth.

- The job market continues to hum along, with a gain of 76k net new jobs in January. That marks three straight months of above-trend job growth.

U.S. Highlights

- Tariffs on Canada and Mexico have been put on hold for one month, but a 10% tariff was imposed on imports from China.

- Companies have ramped up inventories ahead of tariffs, leading to a sharp increase in the trade deficit in December. Activity has eased off in the services sector, but continued to reaccelerate in manufacturing.

- Hiring has slowed in January, however, the labor market remains solid overall. Significant upward revisions to the fourth quarter figures suggest that job growth was stronger at the end of last year than previously thought.

Canada – Tariffs On, Tariff Off, Tariffs On?

It feels like the longest week ever for Canadians. Many of us with sleepy eyes last weekend were sorting out the impact of Trump’s tariffs and what they would mean for an economy that has been on weak footing for the last two years. Then the reprieve of a 30-day delay came on Monday, creating a whipsaw effect in Canadian financial markets. Economic data this week was also headline grabbing. Trade data showed that Canada’s export dependence on the U.S. increased through the end of last year (Chart 1), while employment growth gave a glimpse of what could have been/may still be a solid growth trajectory for 2025 (Chart 2).

President Trump kept most Canadians glued to their TVs/socials on Saturday, announcing a 25% tariff on Canadian exports (10% on energy) to take effect Tuesday, February 1st. With Canadian retaliation announced, financial markets went into panic on Monday. Government of Canada yields collapsed by nearly 20 bps and the Loonie reached a low of 67.5 U.S. cents. Although the President postponed tariffs, Monday’s reaction gave everyone a view into what could be in store for Canadian markets should a trade war come to pass. In the meantime, yields have recovered their lost ground, while the Canadian dollar is hovering close to 70 U.S. cents.

Canadian trade data came in quite positive in December as firms appear to be front running tariffs. Exports for the fourth quarter of 2024 are tracking double digit growth, a big rebound from the negative growth seen over much of last year. High demand for energy and metals from the U.S. led the gain, as the trade surplus with the U.S. clocked in at over $100 billion for the year. This overall figure could be used as fodder for President Trump to validate his claims that trade with Canada is ‘unfair’, even though the trade surplus would become a deficit when energy is excluded.

In any other week, Friday’s labour market report would have been the focus. But trade risks have bumped it to runner up. Yet, the jobs market continues to hum along. Today’s gain of 76k net new jobs in January marks three straight months of above trend job growth. Importantly, the unemployment rate dipped to 6.6%, as population growth ebbs. While the labour market has been a pillar of strength for the Canadian economy, the outlook has become precarious. We have been expecting the unemployment rate to decline over this year, but our tariff scenario analysis shows that it could quickly rise to 7%, if not higher, should tensions persist.

Canada has entered a period of great uncertainty. Tariff threats have cast a shadow over the economic outlook. Market pricing for the Bank of Canada has started to move towards a greater likelihood of another cut come March. The Bank has highlighted the growing downside risks, perhaps signaling a greater willingness to take out more insurance should risks become reality.

U.S. – Canada-Mexico Tariffs on Hold

This week was anything but boring. On Monday, an 11th-hour deal was reached to delay tariffs on Canada and Mexico for a month. However, while Canada and Mexico were spared, China was not, as an additional 10% tariff was imposed on all imports from the country.

The prospect of tariffs being imposed on North America in a month, or in April when the review of current trade policies is completed, looms large. Financial markets have largely recovered from their initial knee-jerk reaction to the tariff announcement, with the S&P 500 paring back losses by the end of the week. However, inflation expectations over the next two years have risen (Chart 1) while bond yields have declined. This points to investors’ concerns that tariffs will accelerate inflation and slow economic growth.

.

Businesses’ uncertainty about the looming tariffs were reflected in the trade data. The U.S. trade deficit widened sharply in December – the largest one-month increase since the early 1990s. Imports surged as companies rushed to ramp up inventories ahead of potential tariffs. Last month’s sharp increase in the trade deficit is likely temporary, but trade policy uncertainty will continue to affect trade flows throughout the year. Uncertainty about tariffs also clouds the outlook in the manufacturing sector, particularly in industries such as auto manufacturing. Even though the ISM manufacturing index has continued to improve in January, rising for the third consecutive month and finally moving into expansionary territory, supply chain disruptions could dent the sector’s nascent progress.

Activity in the services sector continued to expand robustly in January, although it dialed back a notch. The services sector is less exposed to trade than manufacturing, but it is not immune. The prices paid subcomponent remains elevated, and any supply chain disruptions and higher input prices could reignite inflationary pressure.

Additional inflationary impetus could also come from the labor market. Today’s employment report showed that the U.S. economy added 143k jobs in January. This is considerably less than December’s tally (+305k), but still a solid outturn, particularly when combined with a slight decline in the unemployment rate and an uptick in wage growth. Moreover, wildfires in Los Angeles and a cold weather spell nationwide could have also weighed on employment, suggesting a bounce-back next month could be in the cards. Lastly, revisions through the fourth quarter were notably higher, adding an extra 101k jobs to the previously reported figures and suggesting that hiring momentum was even stronger at the end of last year than previously thought (Chart 2).

With inflation progress having stalled in recent months, wage growth showing staying power and heightened uncertainties on how far the new administration will go on its policies, the Fed is likely to remain more cautious. Next week’s inflation report will likely show that the Fed’s patience is justified, as inflation remains persistently above the Fed’s 2% target.

Weekly Economic & Financial Commentary: The Tariff Man Cometh

Summary

United States: It Felt Like Much Longer than a Week

- It was a week of contradiction, where just when things looked like they were going badly, some mitigating factor offset a prior concern. By Friday, it felt more like survival than victory. The takeaways include an improving backdrop for manufacturing and construction, a little less heat in the service sector and a jobs market that refuses to fit into a tidy label.

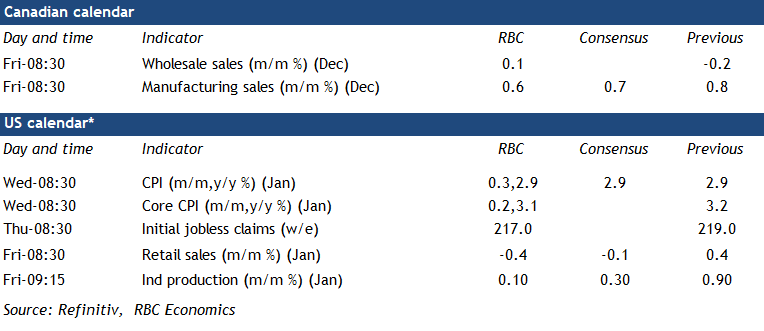

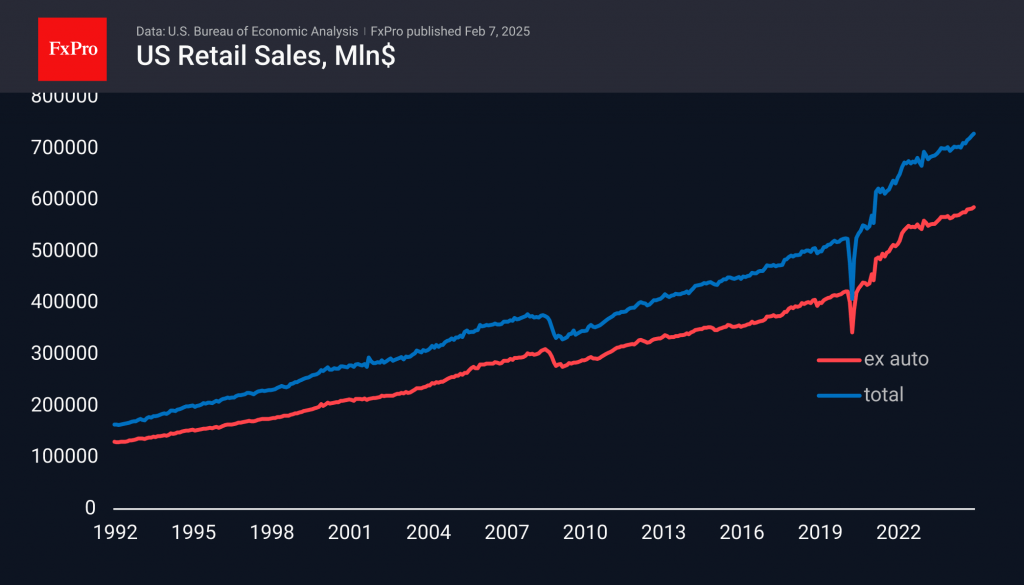

- Next week: CPI (Wed.), Retail Sales (Fri.), Industrial Production (Fri.)

International: Foreign Central Banks Lower Rates

- This week saw rate reductions from central banks across emerging and advanced economies. In Mexico, Banxico lowered its policy rate by 50 bps to 9.50% and issued commentary that we view as consistent with another same-sized move in March. Elsewhere, the Reserve Bank of India delivered its first rate cut since 2020, lowering its policy rate by 25 bps, and the Bank of England also cut its policy rate by 25 bps.

- Next week: Norway CPI (Mon.), Brazil Inflation (Tue.), U.K. GDP (Thu.)

Credit Market Insights: The Wave of Credit Tightening Is Quickly Receding

- Banks appear to be changing their risk calculus. The Q4 Senior Loan Officer Opinion Survey revealed that banks are still tightening lending standards on net, but the prevalence of restriction is quickly fading.

Topic of the Week: The Tariff Man Cometh

- The week started off with a bang when the Trump administration announced plans on Saturday to place tariffs of 25% on goods imports from Canada and Mexico and a tariff of 10% on goods imports from China, effective Feb. 4. Though the Canada and Mexico tariffs were postponed for 30 days, the domestic upshot of the policies, if they are eventually realized, is higher inflation in the near term and slower growth in the outlook.

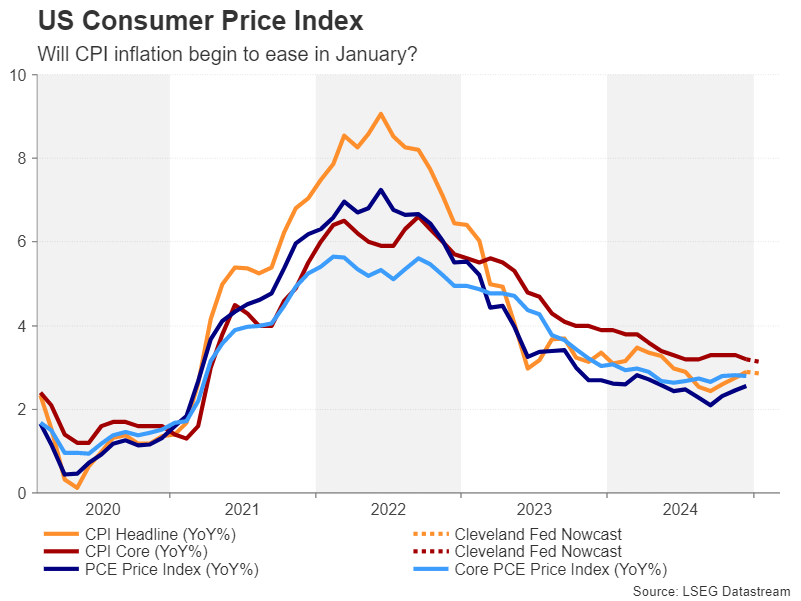

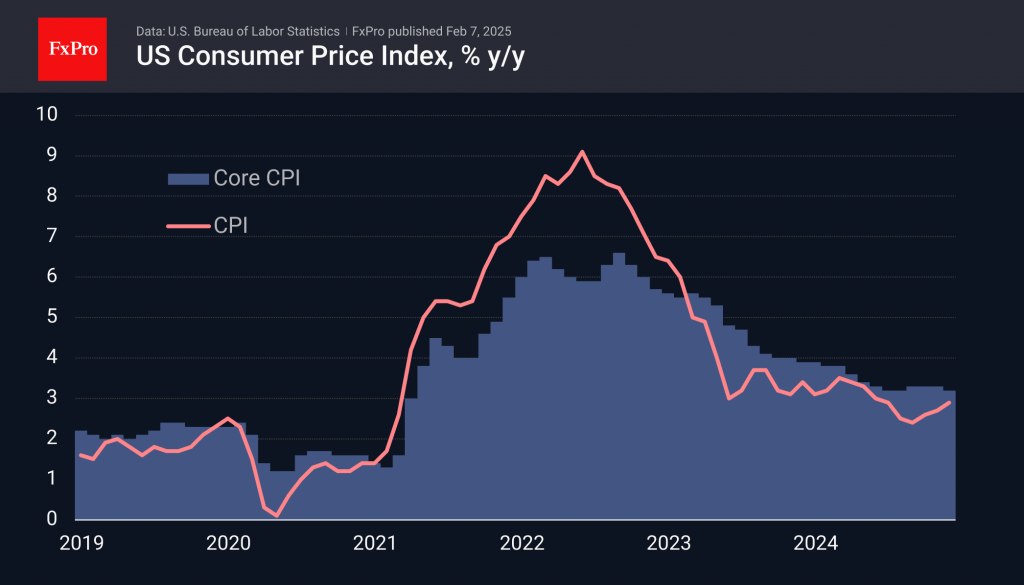

U.S. January Inflation to Show Limited Easing in Price Pressures

The U.S. Federal Reserve will be closely watching January inflation data on Wednesday after foregoing an interest rate cut last month for the first time in the last four meetings.

A resilient U.S. economy isn’t signalling an urgency to cut interest rates further. Retail sales likely ticked lower in January, given a pullback in auto sales after a string of upside surprises. That leaves any additional interest rate reductions in the near term more contingent on price growth continuing to slow towards a 2% rate.

We expect some signs of gradual easing in core price growth in January, but with the total consumer price index growth holding at 2.9% year-over-year, and the risk of a round of tariff hikes on imports from China threatening to stall further progress later this year.

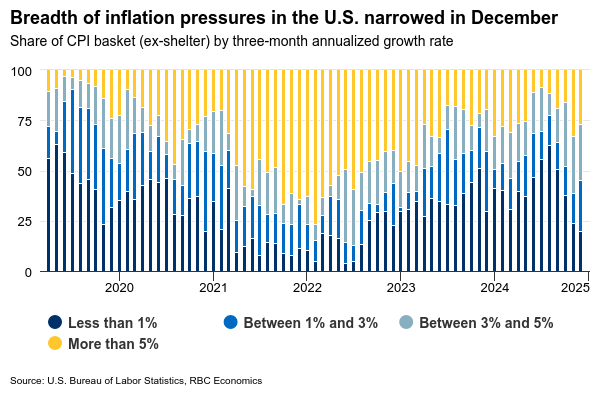

We expect core prices edged up by 0.2% for a second straight month, excluding volatile food and energy components. Growth in home rent prices has continued to slow as expected from an earlier slowdown in market rent costs filtering gradually through to lease renewals. Growth in core goods prices slowed in December after a larger rise in November. By our count, the breadth of inflationary pressures narrowed in December, and we will watch our diffusion measure closely for further signs of broader easing in price pressures.

We don’t expect that progress on inflation will be enough to prompt additional interest rate cuts from the Fed this year.

Week ahead data watch

We expect manufacturing sales to edge 0.6% higher in December, in line with Statistics Canada’s preliminary estimate. Most of the increases were driven by higher sales in petroleum and coal products, and food subsectors.

Canadian wholesale trade likely grew 0.1% in December, according to StatsCan’s early indicator, given sales were up in the motor vehicles, parts and accessories subsector.

We look for 0.4% growth in January U.S. retail sales, slowing from the 0.5% increase in December. Auto sales dropped sharply during the month. Sales at gas stations saw price increases, but not enough to offset the pullback from the auto sector.

U.S. industrial production likely slowed from 0.9% to 0.1% in January, given hours worked in mining and manufacturing sectors both declined during that month.

Week Ahead – Will US CPI be a Positive Distraction Amid Trump’s Dramas?

- US consumer and producer prices to be main focal point.

- UK economic output data to be watched too.

- But Trump and tariff headlines might be a bigger market driver.

Trump rattles markets with tariff games

With the initial central bank decisions of 2025 out of the way, it will be somewhat of a quieter week. However, there’s still plenty for investors to look forward to as the all-important CPI report out of the United States is on the agenda.

Of course, that’s not to say that President Trump won’t find himself at the centre of the markets’ attention again. The tariff war is only just getting started and an escalation is more likely than a de-escalation, while Congressional Republicans have started work on how to finance an extension of the 2017 tax cuts that are due to expire at the end of 2025 amid worries about rising debt.

There’s been some relief, however, for the Treasury Department from the recent drop in Treasury yields. A slight slowdown in economic growth and signs that the uptick in inflation is peaking, alongside Trump’s conciliatory tone on tariffs, have contributed to the pullback in long-term borrowing costs.

Subsequently, the US dollar has retreated from more than two-year highs against a basket of currencies. There could be more losses in store for the greenback in the coming week if the consumer price index begins to ease on a yearly basis.

US CPI might test Dollar bulls’ resolve

The headline rate of CPI edged up to 2.9% y/y in December, while the core rate softened to 3.2%. According to the Cleveland Fed’s Inflation Nowcasting model, headline CPI is anticipated to have moderated to 2.85% in January and the core rate to have ticked lower to 3.13%.

If the actual numbers meet these estimates, investors will likely read them as an indication that the disinflation process is back on track and yields could slide further.

The CPI figures are out on Wednesday and producer prices will follow on Thursday. US factory gate prices have also been trending north in recent months so a decline in the PPI data will be key for a sustained pullback in the dollar. Furthermore, retail sales for January will be an additional guide for Fed policy expectations as strong retail spending could partially offset any increase in rate cut bets.

Markets seem reluctant to fully price in two rate reductions for 2025, likely due to the active threat of higher tariffs. But should the incoming data significantly boost expectations of more aggressive easing, risk appetite could improve further, lifting Wall Street.

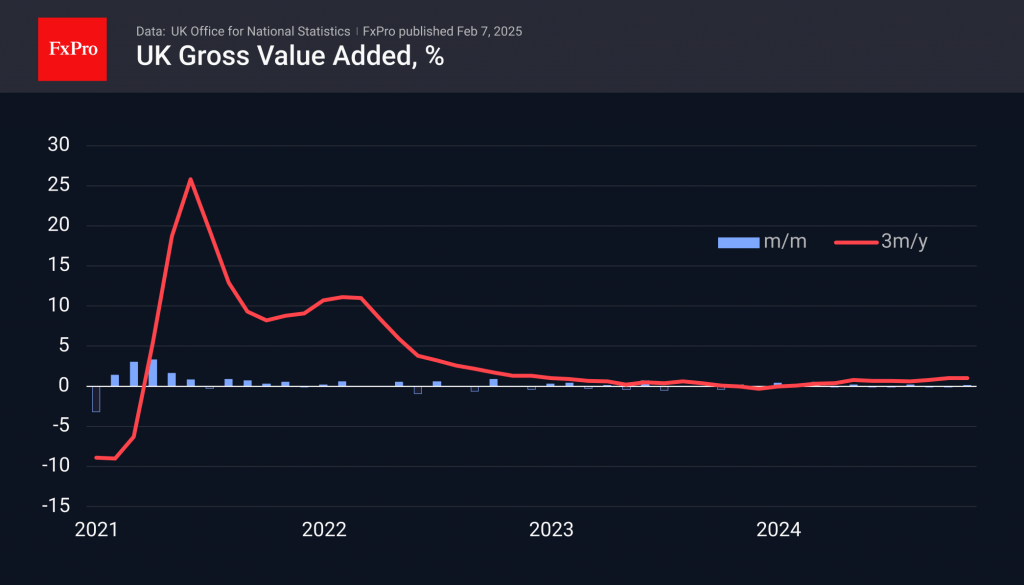

Pound eyes UK GDP update after BoE cut

The Bank of England lowered its benchmark lending rate by 25 basis points at its February meeting but maintained a cautious stance on the pace of future cuts. Worries about elevated wage growth and the inflationary impact of the Labour government’s budget measures continue to weigh on policymakers’ minds.

However, the BoE is also concerned about the anaemic growth that the economy has been eking out since last summer. GDP barely grew in the third quarter of 2024 so investors will be hoping that there was some improvement in Q4, although the forecasts show a small contraction.

The first estimate of Q4 growth is out on Thursday and will be accompanied by the monthly readings on services, industrial and manufacturing output. Stronger-than-expected data could aid the pound’s rebound from January’s more than one-year low of $1.2097.

The pound took a lesser hit from the tariff-led market turmoil than its counterparts as Trump hinted that he is not as of yet thinking about imposing any import levies on the UK. Any change in that rhetoric could hurt sterling, while political developments could also spur some volatility amid rumours that Prime Minister Keir Starmer is thinking of reshuffling his cabinet as a means of replacing his finance minister, Rachel Reeves.

On inflation watch

Elsewhere, CPI numbers are also due out of Switzerland and China. The latter will publish its stats for January on Sunday. The yearly CPI rate is expected to have stayed quickened from 0.1% to 0.4% and the decline in producer prices is forecast to have slowed to -2.1%, which would suggest a slight improvement in domestic demand.

In Switzerland, inflation has been subdued since the middle of 2023 and stood at just 0.6% y/y in December. The Swiss National Bank doesn’t meet until March 20, and although another 25-bps cut is highly likely, whether policymakers maintain an easing bias or turn more neutral will depend on what the next two CPI reports will point to, the first of which is out on Thursday.

In the meantime, the safe-haven Swiss franc has made modest gains versus its major peers during the past week on the back of the Trump-induced uncertainty.

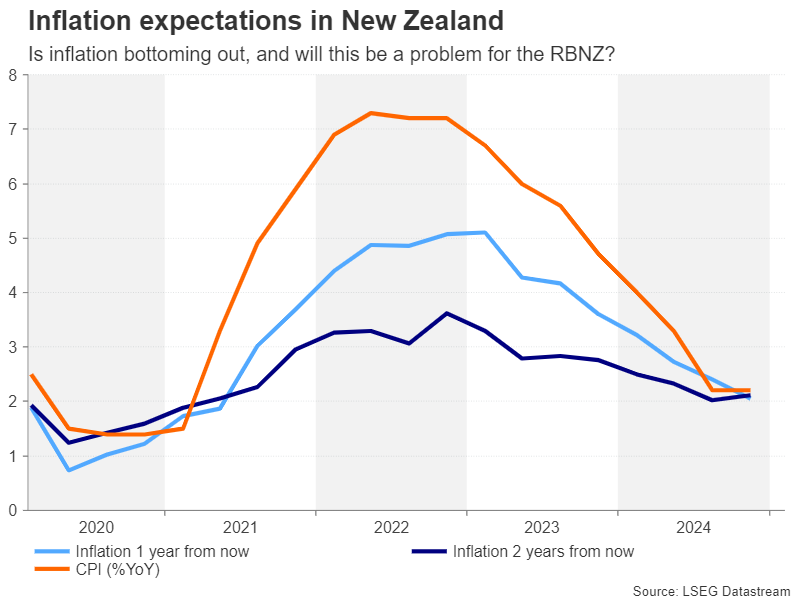

Inflation

Another central bank that’s yet to meet this year is the Reserve Bank of New Zealand. Ahead of the February 19 decision, the central bank’s own survey of inflation expectations might sway rate cut bets on Thursday. In the previous quarter’s survey, two-year expectations edged up slightly to 2.1%. If there’s another uptick in the Q1 report, investors might scale back their bets of a 50-bps reduction at the February meeting, lifting the kiwi.

January CPI Preview: A Strong, But Less Jarring Start to 2025

Summary

Inflation's early strength in 2024 was a jarring reminder that restoring price stability would not be a quick affair. The January CPI report is likely to show that inflation remained stubbornly strong at the start of 2025. We estimate the headline index rose a "high" 0.3%, which would leave the year-over-year rate unchanged at 2.9%. The core index also looks set for a 0.3% advance that we expect to be driven by the ongoing rebound in goods prices and a pickup in non-housing services.

We expect some lingering issues around residual seasonality to buoy January's core reading, but we think this dynamic will be less pronounced than last year. Seasonal adjustment factors will be updated with the upcoming release to reflect the most recent year's price movements. The incorporation of 2024 figures should lead the seasonal factors to "expect" more strength in January and February. Meantime, the somewhat calmer price environment of the past year should lessen the need for businesses to push through big price increases at the start of the calendar year.

If realized, more moderate price increases at the start of this year would unlock favorable base effects and lead to a slowing in the year-over-year rate of inflation in Q1. Yet, we expect the 12-month rate of inflation to move sideways through the remainder of the year, as further services disinflation is offset by higher goods inflation now that additional tariffs are in the works.

January Brings a Change in the Calendar, but Not the Inflation Picture

The first CPI prints of 2024 ended the notion that normalizing supply conditions would be enough to return inflation to the Fed's 2% target in short order. An upside surprise in January was followed by further strength in the first quarter, and while the 12-month rate of consumer price inflation still managed to slow over the course of 2024, it ended the year little better than where it started (Figure 1). A similar story played out across the PCE price index, with the core up 2.8% year-over-year in the fourth quarter—half a point higher than where the January 2024 Bloomberg consensus estimated it would end the year.

The first major inflation reading for 2025 is likely to show that inflation remains stubbornly strong. We estimate the consumer price index rose a "high" 0.3% in January (0.34% before rounding), which would leave the year-over-year rate unchanged at 2.9%. Energy prices should provide less of a lift to the headline than in December. Although energy services should see another sizable rise following higher natural gas prices (Figure 2), energy goods are poised for a smaller advance based on gasoline prices. The rebound in food inflation since the summer, however, is likely to continue amid the recent months’ rise in food-related commodity prices generally and egg prices particularly.

Excluding food and energy, we estimate consumer price growth picked up relative to December’s 0.2% gain with an increase in January of 0.3% (0.32% before rounding) (Figure 3). The disinflationary impulse from the goods sector continues to fade, and we estimate prices for core goods rose another 0.1% last month. Within core goods, we look for the drivers to be roughly balanced between vehicle prices (+0.2%) and other core goods (+0.1%). Meantime, core services inflation likely picked up a tenth in January (+0.4%), fueled by strength in non-housing services like medical care and travel. We look for primary shelter to rise 0.3% in January, matching December’s gain.

Could Residual Seasonality Fuel Another Upside Surprise this January?

Last January, the core CPI came out of the gate strong, rising a full tenth more than consensus expectations. Some—but not all—of this looked due to residual seasonality, i.e., the inability of seasonal adjustment factors to fully capture regular calendar patterns. Typically, January and February see the largest price increases of the year as businesses update their pricing at the start of the calendar year. However, the need to update pricing more quickly in the pandemic period scrambled the recent historical patterns, leading seasonal factors to not “expect” such outsized strength at the start of the year (Figure 4).

We expect some lingering residual seasonality to buoy January’s core reading, but for this dynamic to be less pronounced than last year. New seasonal factors will be published with the release of the January CPI on February 12, and these will incorporate the monthly (not-seasonally adjusted) price changes observed in 2024. The non-seasonally adjusted increase in the January core CPI was particularly strong last year (the January gain exceeded the calendar year average by 28 bps compared to an average of 16 bps the prior five years). The incorporation of 2024 figures and the rolling off of the 2019 price data should lead the seasonal factors to "expect" more strength this January. In addition, as the overall inflation environment quiets down, the degree to which firms need to raise prices at the start of the year to cover their own costs diminishes. These developments should also help tamp down February’s seasonally adjusted change in the core CPI.

Notably, the more moderate pop in prices that we expect at the start of the year will help unlock favorable base effects when it comes to the 12-month rate of core inflation. If our estimate of a 0.3% monthly increase in the core CPI is realized, the year-over-year rate would still likely manage to round to 3.2% in January, but the read-through to the core PCE deflator would push the 12-month change down from 2.8% to 2.6%.

Yet, the path back to 2% remains bumpy, with risks of roadblocks rising. Higher tariffs promised by President Trump on the campaign trail are now a reality with an additional 10% import duty levied against products from China. Although the 25% tariffs threatened against Mexico and Canada have been delayed a month, the down-to-the-wire decision has nevertheless forced businesses to reckon with the potential for higher input and product costs, and leaves little reason for firms to “give” on pricing now. We expect the year-over-year rate of inflation to tick down in Q1 due to favorable base effects, but for price growth to trend sideways through the remainder of 2025 at a pace still above the Fed's target (Table). Some further slowing in services inflation remains in train due to the lag in shelter and ongoing moderation in labor costs, but we expect that to be offset by stronger goods inflation as businesses prepare for, and soon face, higher tariffs.

Xi-Trump Call Cancelled, 10% Tariff Just ‘Opening Salvo’, Chinese Stocks Rallying

Geopolitics:

First shots have been fired in trade war: While it took more than a year before the trade war starting in the first term of US President Donald Trump’s, it only took 10 days this time. A 10% tariff rate was put on China related to Fentanyl coming to the US via Mexico. China was quick to retaliate with tariffs on energy, export controls on metals and targeting several US companies (see box).

It is interesting that China throws export controls into the mix in its retaliation as it has normally only been used in the ‘tech war’ in response to US export controls on microchips. Several commentators have interpreted China’s retaliation as moderate as the tariffs only cover a small part of imports coming from the US. However, I would argue the export controls on key metals are more painful for the US and the same goes for measures towards single US companies. PVH Corp dropped 15% since the retaliation was announced. China sends a clear signal it could hurt other major US companies and thus US stock market performance in case of a further escalation. PVH Corp may not move the overall market but if China goes after big US tech companies, and potentially Tesla, it could have a wider impact. Nvidia is already under an anti-trust investigation and China looks into a similar move on Intel. China likely knows that Trump may be more sensitive to how US stocks perform than tariffs on US trade.

Xi-Trump call cancelled, tariffs just an ‘opening salvo’: A call between Xi and Trump was apparently planned to take place on Tuesday this week but cancelled after China retaliated. On Tuesday afternoon, Trump said he was in no hurry to speak to Xi and that the tariffs was only an ‘opening salvo’. He added that "If we can't make a deal with China, then the tariffs would be very, very substantial". As I wrote last week the ‘real’ trade war will probably not start until the US trade study looking into China’s unfair practices etc. is done by 1 April. Our baseline scenario is still that US average tariffs on China will ultimately end up of around 40% over the next 1-2 years from currently just below 25% (including the latest 10% increase).

Panama leaves Belt and Road Initiative, US claims victory: Panama is officially leaving the Chinese Belt and Road Initiative following US pressure. The news came few days after US Secretary of State Marc Rubio visited the country and Rubio called the decision a “victory”. China’s ambassador to UN Fu Cong called the decision “regrettable” and said that “The smear campaign that is launched by the US and some of the other Western countries on the Belt and Road Initiative is totally groundless”. An audit by Panama of the Hong Kong company that operates two of the five ports in the Panama Canal has been launched and a law suit has also been filed against the Hong Kong company. It seems likely the company will end up having to end the port operations.

Panel warns US risk losing next industrial revolution: At a hearing held by the US-China Economic and Security Review Commission, a panel of China experts warned that the US is at risk of falling behind China as the country is making significant strides in the realms of artificial intelligence (AI) and humanoid robotics. One panellist stated, “China’s AI and robotics ecosystem has seen significant growth, with major companies driving innovation in humanoid robotics and embodied intelligence…these firms are pioneering advancements in robotic hardware, AI integration, and industrial automation, positioning China as a leader in next-generation intelligent robotics.” China’s decades long focus on tech and industrial policy programs continue to put China at the frontier in a rising number of manufacturing areas, such as within EVs, batteries and drones. AI and robotics are also advancing fast.

Markets:

Chinese stocks on a roll: Despite Trump firing the first tariff shots last week, Chinese stocks have performed strongly. This week offshore stocks were up 6% and they have outperformed US stocks lately. The DeepSeek breakthrough two weeks ago has provided optimism back to tech stocks that have led the gains. With more stimulus, positive tech stories and Chinese long-term funds pushed to invest in the market, equities are getting a better foundation. The upside may be capped once the trade war really takes off. In the medium to long term, I still see value, though, as current levels are still low in a historical perspective.

CNY weakening pressure eased lately: Despite the rise in US tariffs, the pressure on the yuan has eased somewhat over the past weeks (chart). It reflects a slight weakening of the overall USD as US yields have moved lower and the removal of tariffs on Canada and Mexico for now. We continue to see USD/CNY moving higher on a 12-month horizon towards 7.60 as we look for the trade war to get tougher during the year. EUR/CNH has stabilized somewhat around the 7.56 level mirroring the stabilisation seen in EUR/USD (chart).

Chinese bond yield back at lows: The Chinese 10-year yield is back at the recent low of 1.60% as the soft PMI data and threat of tariffs has added to the expectations of low(er) for long. Next week CPI data are likely to show another weak print for January.

Economy:

PMI’s for January warning of need for continued stimulus: Chinese PMI’s from both NBS and Caixin pointed to some weakening in January, especially in the service sector (see charts below). The first months of the year should always be treated with some caution due to the effects from Chinese New Year, but still the numbers give rise to some caution and underlines the need for continued stimulus.

Strong China New Year travel spending: Providing some light was reports of strong holiday spending over the New Year break last week. The number of trips hit 501 million, a 5.9% increase from last year. The number of foreign travellers also reached a level similar to the one prior to the pandemic suggesting that China’s visa-free travel has had a clear positive effect on inbound tourism.

Weekly Focus – Tariff Announcements Gave Markets a Roller Coaster Ride

Donald Trump caused a significant market reaction this week by announcing steep tariffs on Canada, Mexico, and China starting from 4 February, which pushed the broad USD higher and sent equities lower. However, after he quickly put the tariffs on Mexico and Canada on hold for a month, the market reaction reversed, and overall equity indexes ended the week higher due to positive earnings reports. Although the outcome remains unclear, we anticipate more tariffs on China later this year, with the EU and possibly other countries being affected soon after. The new tariffs are linked to border security and could be removed or reduced following negotiations, though there is a risk of a tit-for-tat escalation in the short term. China's package of retaliation measures includes 10-15% tariffs on US energy imports and export controls on five metals used in defence, clean energy, and other industries, showing its readiness to engage in conflict if Trump is inclined to do so. On 13 February, we are hosting a webinar to shed light on this situation, see invitation: US Tariff Update - Deal or No Deal?.

On the data front, HICP inflation in the euro area increased to 2.5% y/y in January, slightly above expectations for an unchanged print at 2.4% y/y. The increase was entirely due to energy inflation while food inflation declined, and core inflation was unchanged at 2.7%. Despite the elevated yearly growth rates, the most recent monthly price increases on core inflation rhymes well with 2% annualised inflation. On the political front, French prime minister Bayrou managed to pass the 2025 budget and survive a no-confidence vote.

In the US, the ISM manufacturing index rose more than expected to 50.9 from 49.3, reaching its highest level since September. This increase aligns with the PMI surveys and indicates positive momentum for the US manufacturing sector. In contrast, both the services PMI and ISM fell in January, with the ISM index dropping to 52.8 from 54.0. Data on US productivity in Q4 showed that productivity growth weakened. Although the data is volatile, the current pace is now close to the pre-pandemic trend of around 1%, down from over 3% seen in the second half of 2023. This indicates that structural growth is slowing, meaning firms will either need to pass a larger share of nominal wage costs onto their selling prices or absorb them into their margins.

The Bank of England lowered the policy rate by 25bp to 4.50% as widely expected. At the same time, the BoE delivered a dovish twist to its guidance as two members voted for a larger 50bp cut and they lowered their growth projections, see BoE Review, 6 February.

Next week, the key data release will be the US January CPI, while US politics will also remain in focus. We forecast US headline inflation at 2.9% y/y and core inflation at 3.1% y/y. Attention in the US will also be on Fed Chair Powell's congressional testimony on Wednesday and US retail sales on Friday. In China, CPI and PPI data will be released on Monday, with focus on whether a call between Xi Jinping and Trump, cancelled this week due to China's retaliation to Trump's 10% tariffs, will take place. In the euro area, data releases are limited, but Q4 employment data on Friday will be a highlight. Additionally, the US is set to unveil Trump's plan to end the war in Ukraine at the Munich Peace Conference starting on Friday.

What Next: US CPI and Powell Testifies

In the new week, Fed Chairman Jerome Powell will address Congress on Tuesday and the House of Representatives on Wednesday. The prepared speech will be the same in both cases, but all attention will be focused on his answers to lawmakers’ questions and the outlook for monetary policy.

The key economic news will be the release of US consumer inflation data on Wednesday, 12 February. It has been accelerating since September and reached 2.9% in December. Further acceleration is a strong positive for the Dollar as it pushes back the timing of a rate cut.

Don’t miss the UK’s monthly and quarterly GDP estimates on Thursday, 13 February. The Bank of England has just lowered its growth forecast for this year to 0.75%, which is expected to be weak and negative for the Pound.

On Friday, 14th February, US retail sales are due to be released. Sales excluding autos have been rising every month since last May. The big question is whether this trend will be broken.

Sunset Market Commentary

Markets

The long-awaited re-evaluation of the neutral rate in the euro area turned out to be much ado about nothing. Estimates varied widely depending on the measurement technique. What mattered most in the end was whether or not the bottom of the pre-pandemic 1.75-2.5% range had risen in this new era. The ECB is guessing that it didn’t. The practical implication is that the central bank could lower rates as low as 1.75% before adopting a supportive stance. The latter is not warranted given the lingering inflationary risks, especially in the services sector and ahead of an expected economic recovery. Two things stand out though. One is that the variability at the lower bound estimates decreased sharply compared to pre-2020, which does reveal some upward pressure on the neutral rate. Second is that the staff paper goes at length trying to downplay the usefulness of this theoretical, unobservable neutral rate for actual policymaking. ECB chief economist Lane did the same earlier this week as part of an unusually hawkish speech. It suggests, if anything, that the ECB wants to at least contain (too dovish) market expectations. Money markets already almost fully price in four additional moves (to 1.75%).

Moving on to the next potential market moving candidate for today: US payrolls. Job growth remains solid. The January outcome of 143k was slightly below expectations (175k). But November and December saw a combined 100k upward revision. The household survey, just as in December, tells a similar story with 223k employment growth. That was more than enough to offset the increase in labour participation (rate rose to 62.6%), leading to an unexpected decline in the unemployment rate to 4%. To top it off, wages grew an above-consensus 0.5% m/m to 4.1% y/y. Yearly wage growth now appears to be stabilizing around 4%, significantly above the levels seen prior to the pandemic. US yields dropped up to 7 bps in a kneejerk reaction to what a small headline miss to begin with anyway. It reveals market sensitivity is currently skewed to downside surprises. US rates erased losses and more as the strong details began to sink in. They currently trade 4-5.4 bps higher across the curve. We’re now spotting the first signs of a bottoming out process. US yields pull European rates a few bps higher as well. The Fed’s extended rate pause (at least through June) gets firm market backing now. The next first full rate cut isn’t priced in before September. Dallas Fed president Logan during yesterday’s BIS event even openly pondered whether more cuts are necessary this year at all. The dollar is trading extremely stoic with a tiny strengthening bias. EUR/USD trades around 1.036, DXY just south of 108 and USD/JPY at 152. Both European and US stock markets trade little changed.

News & Views

Canadian employment rose by 76k in December, building on the solid 91k pace from December and beating consensus (25k) by a wide margin. Details showed an increase in both full-time (+35.2k) and part-time (+40.9k) occupations. Employment gains in January were led by manufacturing (+33k; +1.8%) and professional, scientific and technical services (+22k; +1.1%). The unemployment rate avoided the feared uptick from 6.7% to 6.8% and even declined to 6.6%. This occurred even against the background of a higher participation rate (65.5% from 65.4%). Average hourly wages rose by 3.5% Y/Y (down from 4% in December). The Canadian dollar holds the balance with a strong USD today as the numbers reduce the likelihood that the BoC will implement more rate cuts even as the lingering tariffs pose significant downside risks to the Canadian economy. USD/CAD is testing first support in the 1.43-area. A break lower would make the technical picture in the pair more neutral. CAD swap rates add 7 to 9 bps across the curve.

The Turkish central bank published its updated inflation outlook. The CBRT raised the end of year forecast to 24% from 21% with a projection band of 19%-29%. It added that it was mostly a mechanical revision driven by factors beyond the control of monetary policy. It doesn’t suggest any easing of the monetary policy stance. The end-2026 forecast was unchanged at 12% while a first prognosis for end-2027 came in at 8%. The CBRT sets the policy rate in a way to ensure the tightness required by the projected disinflation path. In December and January, they conducted back-to-back 250 bps rate cuts to bring the policy rate at 45% currently. EUR/TRY trades sideways (36-38.50) near record highs since last summer.