Sample Category Title

EUR/USD Mid-Day Outlook

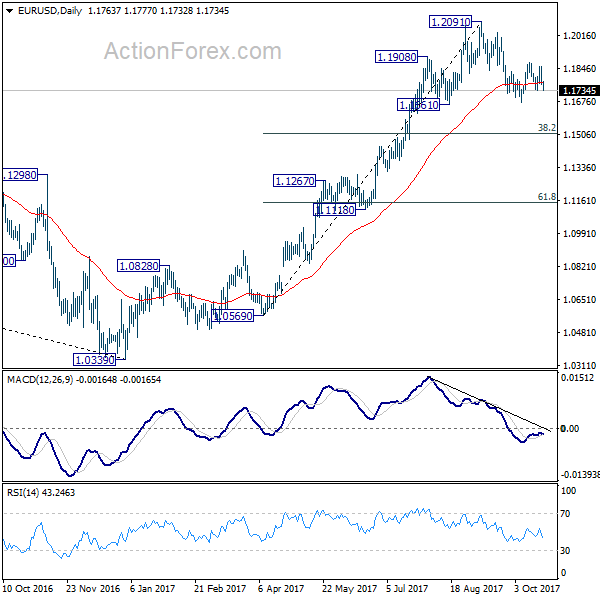

Daily Pivots: (S1) 1.1740; (P) 1.1799 (R1) 1.1835; More...

Euro drops to as low as 1.1732 so far today but stays above 1.1729 support. Intraday bias remains neutral first. On the downside, break of 1.1669 will resume the corrective fall from 1.2091 to 38.2% retracement of 1.0569 to 1.2091 at 1.1510. We'd expect strong support from there to complete the correction. On the upside, break of 1.1879 will revive the case that pull back from 1.2091 has already completed at 1.1669. In such case, intraday bias will be turned back to the upside for retesting 1.2091 high.

In the bigger picture, rise from medium term bottom at 1.0339 is not finished yet. It's expected to continue after pull back from 1.2091 completes. And, next target will be 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. However, it should be noted that there is no confirmation of trend reversal yet. That is, such rebound from 1.0399 could be a correction. And the long term fall from 1.6039 (2008 high) could resume. Hence, we'd be cautious on strong resistance from 1.2516 to limit upside.

Euro Broadly Lower as Traders Await ECB, Yen Stays Soft

Euro is trading broadly lower today as markets are awaiting the highly anticipated ECB meeting later in the week. The common currency is even weaker than the Japanese Yen, which gapped down after Japanese election. Prime Minister Shinzo Abe's coalition retained absolute majority in the parliament, paving him the way to push for strong fiscal and monetary stimulus. Meanwhile, Dollar is generally firmer today with support from hope on tax cut/reform in the US. New Zealand Dollar and Sterling are also among the strongest ones.

Trump wants to pass the tax plan by Thanksgiving

US President Donald Trump warned House Republicans yesterday that 2018 mid term elections would be "really bad" if they failed to pass the tax plan. Meanwhile, Trump intentionally called the plan "tax cuts" and said "it will be the biggest cuts ever in the history of this country. I think that there's tremendous appetite. There's tremendous spirit for it." Trump also noted that he hoped the plan will be done "before the end of the year, but maybe much sooner than that". There are talks that Trump is driving to have the plan passing through the Congress and be on his desk by Thanksgiving.

CBI report showed drastic deterioration in optimism

In UK, a report from the Confederation of British Industry shows that 12% of businesses said they were more optimistic on the general business situation than three months ago. But 24% were less optimistic. That made the Business Optimism index at -11, sharp deterioration from 5 recorded in the three months to July. CBI trends total orders also dropped to -2 in October.

CBI Chief Economist Rain Newton-Smith noted that there is a "general softening in manufacturing activity over the past three months, with the outlook for investment becoming more subdued." And he urged the government to use the Budget to provide a fillip for factories through business rate reforms, including exempting new plant and machinery from rates altogether, and switching to the more recognized CPI inflation measure rather RPI when calculating upratings."

Bundesbank said industry drives German economy

In Germany, Bundesbank said in its monthly reported that "industry, supported by buoyant export demand, is likely to retain its role as a main pillar of a strong economy." And, "the order situation of industrial firms is excellent." Meanwhile, "against the backdrop of very good consumer sentiment and favorable labor market and income prospects, no lasting deterioration in consumption is to be expected."

There the political turmoil in Catalonia continues, Euro traders' minds are clearly on ECB meeting later this week. The market has already fully priced in an announcement of tapering of the asset purchase program from the current pace of EUR 60B per month until December 2017 "or beyond, if necessary". To what extend the ECB would taper is the question. Some suggest a reduction of monthly purchases to EUR 40B beginning in January 2018 for 6 months, while others expect a cut to EUR 30B for 9 months.

Abe to continue with Abenomics after winning election

After having a landslide victory in Sunday's snap election, Japanese Prime Minister Shinzo Abe said "the key to Japan's sustainable growth is how we respond to ageing of the population, which is the biggest challenge for Abenomics." And, he and his cabinet aimed to "exit deflation by accelerating wage growth through innovation on productivity.". Abe also said he will "promote human resources, proceed with free pre-school education in one spell and we are going to offer free higher education for the children who truly need it."

The ruling Liberal Democratic Party and coalition partner Komeito party won 313 of the 465 seats in the lower house. That gives the coalition over 1/3 absolute majority. With renewing strong mandate, Abe continue to push his three arrows in the Abenomics. One of which is aggressive monetary easing. There are talks that BoJ governor Haruhiko Kuroda will have a high chance to have his term renewed if Abe has a landslide victory. But after all, whether Kuroda would stay should not alter the ultra-accommodative policy stance.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1740; (P) 1.1799 (R1) 1.1835; More...

Euro drops to as low as 1.1732 so far today but stays above 1.1729 support. Intraday bias remains neutral first. On the downside, break of 1.1669 will resume the corrective fall from 1.2091 to 38.2% retracement of 1.0569 to 1.2091 at 1.1510. We'd expect strong support from there to complete the correction. On the upside, break of 1.1879 will revive the case that pull back from 1.2091 has already completed at 1.1669. In such case, intraday bias will be turned back to the upside for retesting 1.2091 high.

In the bigger picture, rise from medium term bottom at 1.0339 is not finished yet. It's expected to continue after pull back from 1.2091 completes. And, next target will be 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. However, it should be noted that there is no confirmation of trend reversal yet. That is, such rebound from 1.0399 could be a correction. And the long term fall from 1.6039 (2008 high) could resume. Hence, we'd be cautious on strong resistance from 1.2516 to limit upside.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 10:00 | EUR | Bundesbank Releases Monthly Report | ||||

| 10:00 | GBP | CBI Trends Total Orders Oct | -2 | 9 | 7 | 1.70% |

| 12:30 | CAD | Wholesale Sales M/M Aug | 0.50% | 1.10% | 1.50% | |

| 14:00 | EUR | Eurozone Consumer Confidence Oct A | -1.1 | -1.2 |

CAC Higher, Investors Eye French Manufacturing PMIs

The CAC index has started the week with gains. Currently, the CAC is trading at 5,390.55, up 0.34% on the day. On the release front, the sole event on the schedule is Eurozone Consumer Confidence, which is expected to remain at -1 point. On Tuesday, France and the eurozone release Services and Manufacturing PMIs, with the indicators expected to show expansion.

Will Catalonia declare independence this week? The constitutional crisis has now entered its third week. On Saturday, the central government said it was imposing direct rule, invoking Article 155 of the Spanish Constitution. The Spanish Senate is expected to approve the measure on Friday, so all eyes are on the Catalan parliament, which could be dissolved. Madrid is expected to strip Catalan President Carles Puigdemont of his title and powers and take over Catalonia's local police force. Unsurprisingly, the Catalan government has condemned Madrid and said it will not accept direct rule. The crisis has led to many companies in Catalonia moving their legal headquarters to Madrid, and investors are nervously watching as developments unfold in Spain, which is the eurozone's fourth largest economy.

With the French economy enjoying the economic rebound seen across the eurozone this year, French stock markets have responded with gains. Currently the CAC is trading at its highest level since May, and the index has gained an impressive 5.3% since September 1. President Macron's plans to reform the economy have been well-received by investors, and the government seems intent on overhauling labor laws and making France much more competitive, which should continue to boost French stock markets. Recent French indicators have generally looked good, and the markets are expecting strong readings from the services and manufacturing PMIs on Tuesday.

USD/CHF Strongly Bullish

Price rallies and extends the bullish momentum as the USDX is trading in the green. The USD has taken full control and drives the pair higher, remains to see what will really happen in the upcoming period and if the USDX will have enough energy to make a valid breakout above the 93.81 static resistance.

The rate edges higher and is almost to reach a very strong dynamic resistance. I've said in the previous days that technically it is expected to climb much higher in the upcoming period.

The USD appreciates versus its rivals as the United States data have come in better in the last days, the dollar index reached the 94.00 psychological level earlier and could finally make a valid breakout above the 93.81 static resistance.

The rate increased sharply and is almost to reach the median line (ml) of the minor ascending pitchfork, where he may find resistance again. Most likely will be attracted by the confluence area formed at the intersection between the median line (ml) with the first warning line (WL2) of the descending pitchfork. Resistance can be found at the 250% Fibonacci line (ascending dotted line) as well if will take out the near term obstacles.

We'll see if will have enough energy to climb above the mentioned resistance levels, a rejection from the median line of from the WL1 will send the rate towards the WL2 again. We have a bullish bias as long as the rate is trading within the ascending pitchfork's body.

USD/CAD Will Make New Highs

The currency pair increased and resumed the Friday's impressive rally, should approach and reach the 1.2678 horizontal resistance if the USDX will climb much higher. Is expected to be attracted by the median line (ML) of the major red descending pitchfork. Technically, it should climb towards the upper median line (uml) of the blue ascending pitchfork after the failure to retest the median line (ml).

NZD/USD Erased The Morning Losses

The NZD/USD dropped further in the morning resuming the bearish momentum, but the bulls have struck back and have forced the rate to jump higher and to close the morning gap. The pair was almost to reach the sixth warning line (wl6), but now it could come back to retest the median line. Could reach also the 0.7000 psychological level, while a valid breakout above the median line will signal a further rebound.

Loonie Swoons to 7-Week Low After Dismal Canadian Retail Sales

After a rough week, the Canadian dollar is almost unchanged in the Monday session. Currently, USD/CAD is trading at 1.2634, up 0.04% on the day. On the release front, it's a quiet start to the week, with no major US events until Wednesday. Later in the day, Canada releases Wholesale Sales, which is expected to slow to 1.1 percent.

The Canadian dollar lost 1.3% last week against the greenback, and is currently at its lowest level since August 31. USD/CAD gained ground on Friday, as Core Retail Sales slumped with a decline of 0.7% in August. This marked the indicator's steepest decline since June 2016. Inflation remains weak, as CPI inched up to 0.2%, shy of the estimate of 0.3%. These numbers have bolstered the likelihood that the Bank of Canada will sit on its hands at its policy meeting next week. The odds that interest rates will stay the same have increased to 81%, up from 73% prior to the core retail sales and CPI data. Canada's economy has slowed down after an excellent first half of 2017. Strong economic growth and and an increase in exports prompted the BoC to respond with a rate hike in September.

The markets are keeping a close eye on the Federal Reserve, as President Trump has said he will nominate a new Fed head shortly. The front runners are economist John Taylor and Federal Reserve Governor Jerome Powell. Taylor advocates a rule in which rates which be as high as 3 percent, given current economic conditions. Powell is more closely aligned to Fed Chair Janet Yellen's monetary stance which advocates an incremental increase in rates. With the two candidates representing sharply differing views on interest rate levels, Trump's choice for the new Fed chair could have a significant effect on monetary policy and the strength of the US dollar.

EURUSD Strongly Bearish Below 1.1750

The euro has slipped lower against the U.S dollar during the European trading session, hitting 1.1734, as investors remain concerned about the political risks coming from Catalonia and new political risks coming from the Lombardy region of Italy. The EURUSD pair currently trades close to the 1.1740 region, as the U.S dollar Index continues to push towards the trading highs of October.

The EURUSD pair is strongly bearish while trading below the 1.1750 level, further intraday declines can be expected for the euro while below this level, with sellers targeting the 1.1733 and 1.1713 levels.

Should the EURUSD pair move back above the 1.1750 level, euro buyers will likely try to push price towards the 1.1770 and 1.1800 resistance areas.

GBPUSD Bearish Below 1.3190

The British pound has slipped lower against the U.S dollar, hitting 1.3163, with broad strength in the U.S dollar index behind the current decline. The GBPUSD pair currently trades around the 1.3170 level, with the economic calendar remaining fairly light heading into today's U.S session. Pound traders will likely be cautious, ahead of the release of third fiscal quarter GDP figures from the UK economy on Tuesday.

The GBPUSD pair remains bearish while trading below the pivotal 1.3189 level. Further declines can be expected while trading below the 1.3189 level, with sellers targeting the 1.3146 and 1.3116 levels. Extended intraday resistance is seen at 1.3087.

Should price-action move above the 1.3189 level, buyers will look to target the 1.3200 level, and the key 1.3227 price-high.

Market Update – European Session: Quiet Start To Trading Week, Focus On ECB QE Taper

Notes/Observations

ECB poised to indicate its QE policy later this week

Abenonics continues with decisive victory for PM Abe in Japan

Overnight

Asia:

Japan PM Abe’s ruling LDP/Komeito coalition won a supermajority in elections with 312 seats* or ~67.1% compared to 290 under prior Parliament (as speculated)

Europe:

Spain PM Rajoy invoked Article 155 of the Constitution: plans to dissolve the Catalonia govt and curb its powers, and call elections within 6 months. Powers of Catalan administration to be transferred to the central govt

Catalan Leader Puigdemont: People of Catalonia cannot accept measures decided by Spanish Govt; Spanish govt steps on Catalonia worst attacks since Franco dictatorship; requests Catalan parliament meet to debate Spain govt measures

Catalan parliament speaker Forcadell: Measures taken by Spanish govt are a "coup"; committed to defending the sovereignty of the Catalan parliament

Northern regions of Veneto and Lombardy claimed victory in autonomy referendums that seek to grab additional powers and tax revenue from Rome. leaders of the neighboring regions hope to leverage strong turnout in talks with Italy's center-left government

Czech Election Results: Centrist and populist ANO party wins ~30% (78 of 200 Seats in Chamber of Deputies) Billionaire Babis expected to become PM

Fitch affirmed Italy sovereign rating at BBB; outlook Stable

S&P affirmed Norway sovereign rating at AAA; outlook Stable

Fitch raised Cyprus sovereign rating one notch to BB from BB-; outlook Positive

Americas:

Fed Chair Yellen: must keep our unconventional policy tools ready to be deployed due to "uncomfortably high" risk of short term rates dropping to lower bound again in the future

President Trump: Confident about tax reform plan, should be approved by the end of the year or maybe "much sooner than that"

President Trump: Both Fed chair possibilities John Taylor and Jerome Powell are very talented; likes Janet Yellen 'a lot'; will make decision on Fed chair shortly

Economic Data

(CH) Swiss Sept M3 Money Supply Y/Y: 4.4 v 4.1% prior

(DK) Denmark Oct Consumer Confidence: 7.1 v 7.5e

(TR) Turkey Oct Consumer Confidence: 67.3 v 67.7e

(TW) Taiwan Sept Industrial Production Y/Y: 5.2% v 5.4%e

(TW) Taiwan Sept Unemployment Rate: 3.7% v 3.8%e

(HK) Hong Kong Sept CPI Composite Y/Y: 1.4% v 2.0%e

Fixed Income Issuance:

None seen

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 +0.2% at 390.9, FTSE +0.1% at 7532, DAX +0.3% at 13035, CAC-40 +0.3% at 5389, IBEX-35 -0.4% at 10184, FTSE MIB flat at 22353, SMI +0.2% at 9255, S&P 500 Futures flat]

Market Focal Points/Key Themes:

European Indices trade mostly higher across the board with the exception of the Spanish Ibex which trades lower on continuing worries over Catalonia as Spanish Banks weigh on the Index.

In the UK Dialight and Pendragon trade sharply lower after profit warnings, while in the Netherlands Philips trade higher after Q3 results. In the healthcare space DBV Tech trades lower by over 40% after its Phase III trial failed to meet primary endpoint.

Looking ahead to the US morning notable earners include T-Mobile, Halliburton and Kimberly Clark, in whats expected to be a busy week for earnings.

Equities

Consumer discretionary [ Air France [AF.FR] +1% (New pension scheme agreements reached by KLM with its pilot and cabin staff unions), Pendragon [PDG.UK] -17% (Cuts outlook)]

Industrials: [GKN [GKN.UK] +3% (Considering splitting aerospace and automotive businesses), Dialight [DIA.UK] -15.6% (Profit warnings)]

Healthcare:[Cosmo Pharma [COPN.CH] +1% (FDA approves QIDP and Fast Track designations forAemcolo), Philips [PHIA.NL] -0.4% (Earnings), DBV Tech [DBV.FR] -44% (Topline results of Phase III clinical trial in Peanut-Allergies failed to meet primary endpoint), Spire Healthcare [SPI.UK] +13% (Takeover approach by Mediclinic)]

Speakers

Spain Dep PM Saenz; Catalan govt will not disappear; May choose a single representative to govern the region temporarily. To apply Article 155 in a gradual manner and noted that the Catalan leader would lose all powers once Senate approved direct intervention

Bank of Korea (BOK) Gov Lee: 2018 GDP growth forecast of 2.9% excludes any potential rate hike

Japan PM Abe: Signed coalition agreement with Komeito. Would implement policies as promised during campaign and think about new Cabinet. To reach cross-party consensus on constitution

Currencies

USD was slightly firmer against the major pairs as the week began.

EUR/USD was trading in the mid-1.17 area ahead of Thursday’s ECB meeting where the central bank is expected to take action in tapering its bond buying program.

USD/JPY pair hit a 3-month high just above the 114 level following PM Abe super-majority win in the lower house over the weekend. The political victory removed uncertainty for the course of Abenomics. Dealers noted that the dovish policy from the BOJ seen continuing even in the context of BOJ Gov Kuroda's term coming to an end in April of next year

Fixed Income

Bund futures trade at 161.63 up 12 ticks as German government bonds looks more balanced going into the European Central Bank meeting Thursday. Support lies at 161.24, followed by 160.38. Resistance stands initially at 162.75, followed by 163.51.

Gilt futures trade at 124.30 down 7 ticks and below a strong horizontal resistance at 124.75 and remains under pressure. Continued downside eyeing 123.26. Upside targets 124.90 then 125.24.

Monday’s liquidity report showed Friday’s excess liquidity fell to €1.791T from €1.792T and use of the marginal lending facility dropped to €315M from €338M.

Corporate issuance saw primary market finish week with over $20B priced

Looking Ahead

(UR) Ukraine Sept Industrial Production M/M: No est v 3.0% prior; Y/Y: 0.6%e v 1.2% prior

(BR) Brazil Oct CNI Industrial Confidence: No est v 55.7 prior

(BR) Brazil Sept Total Federal Debt (BRL): No est v 3.404T prior

05:30 (BE) Belgium Debt Agency (BDA) to sell €2.3-2.8B in 2023, 2026 and 2043 OLO bonds

06:00 (UK) Oct Industrial Trends Total Orders: 9e v 7 prior, Selling Prices: No est v 18 prior, Business Optimism: No est v 5 prior

06:00 (TR) Turkey to sell 2018, 2022 and 2027 bonds (3 tranches)

06:00 (IL) Israel to sell 2022, 2026, 2027 and 2047 bonds

06:00 (DE) German Bundesbank Monthly Report

06:25 (BR) Brazil Central Bank Weekly Economists Survey

06:45 (US) Daily Libor fixing

07:00 (IN) India announces details of upcoming bond sale (held on Fridays)

08:00 (PL) Poland Sept M3 Money Supply M/M: 0.6%e v 0.4% prior; Y/Y: 5.6%e v 5.5% prior

08:05 (UK) Baltic Dry Bulk Index

08:30 (US) Sept Chicago Fed National Activity Index: -0.10e v -0.31 prior

08:30 (CA) Canada Aug Wholesale Trade Sales M/M: 0.5%e v 1.5% prior

08:50 (FR) France Debt Agency (AFT) to sell combined €4.3-5.5B in 3-month, 6-month and 12-month Bills

09:30 (EU) ECB announces Covered-Bond Purchases

09:35 (EU) ECB calls for bids in 7-Day Main Refinancing Tender

10:00 (EU) Euro Zone Oct Advance Consumer Confidence: -1.1e v -1.2 prior

11:30 (US) Treasuries to sell 3-Month and 6-Month

(IT) Italy Debt Agency (Tesoro) announcement for upcoming CTZ and BTPei auction for Thurs., Oct 26th

13:30 (EU) ECB’s Nouy (SSM chief) in London

15:00 (CO) Colombia Aug Economic Activity Index (Monthly GDP) Y/Y: 1.4%e v 3.0% prior

16:00 (US) Weekly Crop Progress Report