Sample Category Title

Daily Technical Analysis: EURUSD, GBPUSD, USDJPY, USDCHF

EURUSD

The EURUSD was indecisive yesterday. The bias is neutral in nearest term probably with a little bullish bias after price bounced-off the lower line of the bearish channel testing the upper line as you can see on my H1 chart below, located around 1.1800/50 area. Immediate support is seen around 1.1725. A clear break below that area could trigger further bearish pressure testing 1.1670 key support which is the “neckline” of the “head and shoulders” formation on daily chart. A clear break below 1.1670 would confirm the bearish reversal scenario with nearest target seen at 1.1450. On the upside, key resistance remains at 1.1900 which need to be clearly broken to the upside to potentially nullify the “head and shoulders” bearish reversal scenario and resume the major bullish trend testing 1.2000 – 1.2090.

GBPUSD

The GBPUSD was indecisive yesterday. The bias is neutral in nearest term probably with a little bullish bias testing 1.3300/30 resistance area. Immediate support is seen around 1.3150. A clear break and daily close below that area could trigger further bearish pressure testing 1.3087/00 region. Overall I remain bullish but need a clear break above 1.3330 key resistance to reactivate my bullish mode targeting 1.3615 region.

USDJPY

The USDJPY closed lower yesterday at 113.43 after gapped higher at 113.86 but still able to stay above 113.20 key support so far. The bias is neutral in nearest term. Immediate resistance is seen around 113.75. A clear break above that area could trigger further bullish pressure testing 114.50 region which is a good place to sell with a tight stop loss as a clear break above that area would expose 115.50 region. On the downside, a clear break back below 1113.20 would expose 112.85 or lower. Overall I remain neutral.

USDCHF

The USDCHF printed a bearish pin bar formation yesterday as you can see on my daily chart below. The bias is neutral in nearest term. I still prefer a bullish scenario at this phase but need a clear break above 0.9881 to nullify the bearish pin bar scenario targeting 0.9950 area. Immediate support is seen around 0.9830. A clear break below that area could trigger further bearish pressure testing 0.9765 area.

Market Morning Briefing: The Aussie Has Medium Term Support At 0.7785

STOCKS

Dow (23273.96, -0.23%) saw its first dip of about 95 points since its rally from levels near 22288 seen on 28th Sep’17. In case the correction continues, we could see the current dip extend towards 23200-23000 in the near term.

Dax (13003.14, +0.09%) continues to remain in the 1310-12900 region and is expected to trade in the said region for a few more sessions.

Shanghai (3383.52, +0.08%) could face a small rejection from 3385 and could come off towards 3360 in the near term before bouncing back again towards 3400. Range-bound movement expected in the coming sessions.

Nikkei (21733.10, +0.17%) has tried to move up slightly. Immediate target of 21800-21900 remains intact on the upside for now. A small dip from 21800/900 is possible before the index tries to move higher in the medium term.

Nifty (10184.85, +0.38%) is almost stable within 10250-10100 region and could remain so for some more days. Near term could see some sideways consolidation before deciding on further direction.

COMMODITIES

Gold (1282.52) is trading near immediate support on the daily candles and while that holds, the price could bounce back towards 1300-1310 in the near term. Only a break below 1275, if seen could take it lower to 1260.

Silver (17.11) has some scope of coming down towards 16.80-16.50 in the coming sessions, before bouncing back towards 17.00 and higher. While some room is visible on the downside, near term could be bearish.

Brent (57.49) has immediate support near 57.00-56.65 levels which is likely to hold in the medium term, taking the index to higher levels of 59.00 or even 60.00 in the coming sessions. Note that on a longer term, 61 is a crucial resistance and could eventually push the index to lower levels in the longer term. For now, we prefer a bounce from 56.65 to levels near 59-60.

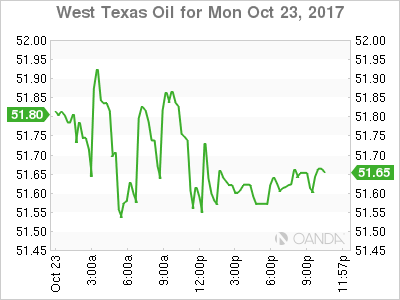

WTI (52.00) could trade in the 51-53 region in the coming sessions. While immediate support near 51 holds, a rise above 53 is a possible situation for the medium term.

Copper (3.2245) has risen again today and is trading fairly on the upside. Resistance on the 3-day candles look strong just now and while that holds, medium term looks bearish towards 3.10-3.05.

FOREX

The crucial Support at 1.1730-00 on the Euro (1.1760) is holding well enough so far even though the German-US 10Yr Spread (-1.94%) trades a little lower than yesterday's -1.93%.

Looking at the medium term (see Interest Rates below), there should be decent chances of an upmove in the German-US 10Yr Spread and therefore in the Euro.

Dollar-Yen (113.35) rose to 114.07, but has come off from there, perhaps endorsing strength of long-term Resistance at 114.50. The Euro-Yen (133.37) has come off a bit alongwith Dollar-Yen and the dip in the Euro, but has good Support near 132.75-50 now.

The Pound (1.3220) trades stronger than yesterday, but still has another important Resistance overhead at 1.3250, which could still push it down.

The Aussie (0.7823) has medium term Support at 0.7785 and may try to mount a rally towards 0.79+ while the Support holds. The overall shape of the Aussie chart resembles the Euro chart.

Dollar-Yuan trades near 6.6298. Dollar-Rupee (65.0225) may test important Support in the 64.95-90 region today.

INTEREST RATES

The German 10Yr (0.43%) trades 1bp lower than yesterday's 0.44%, but should have Support at 0.40%, with upside open up to 0.70%.

On the other hand, the US 10Yr (2.37%) has immediate Resistance at 2.40% and further Resistance at 2.50%. Similarly, long-term Resistance is seen near 0.08-09% on the 10Yr JGB. Even the UK 10Yr Gilt (1.31%) has Resistance just overhead.

The US Yield Curve (30-10 Spread 0.52%, 30-5 Spread 0.89%) has steepened a wee bit more than yesterday. Some more upside towards 0,54% and 0.92% seems possible.

The Indo-US 10Yr Spread (4.4186%) is trading below important Resistance at 4.45%.

USD/JPY Gap Fill Line

Yesterday we saw USD/JPY approach the top of its range, gap up, and then spend the rest of the day dropping.

A beautiful gap fill if you were looking to short rallies in the pair as we spoke about in yesterday’s blog. Just take a look at the intraday chart here:

USD/JPY 15 Minute:

The gap fill is pretty self explanatory, but look at the way that price has retested the gap fill line and continued lower. There’s definitely a bit of bearish momentum to start the week and when you see these little pullbacks into previous short term support being sold, you know there’s often more to come.

Political Malaise

Political Malaise

While the USD dollar remains tentatively poised for a breakout, lingering political uncertainty still hangs heavy in the air which has left G10 FX rangebound for the most part on Monday.

Despite taking a knock in late US trade after an afternoon US equity market swoon, JPY is expected to weaken over time as an extension of Abenomics should mean further stimulus for Japan. But in the early stages of any currency move, there’s seldom a ” take-it-to-the-bank-trade ” more so in this current scenario given the extending long USD positions, very frothy equity markets and the omnipresent level of uncertainty when it comes to The House passing any substantive US administration policy. Even if Abe served up weaker JPY on a silver platter, there are many hurdles on the way to an eventual payday.

US equities finally came up for air after the Dow snapped a six days winning streak as investors get set to dissect the deluge of corporate earnings this week. In general, earings should remain a significant boost to equity prices, but markets were spooked when GE shares cratered 6.3 percent causing analysts to hit the panic button warning of possible dividend cuts.

On the Fed chair watch, the highlight of the day was stale reports that President Trump is “very, very close” to deciding on the next US Federal Reserve chief. Jerome Powell and John Taylor are getting markets nod while Janet Yellen is relegated to the sidelines.

The Euro

While political concerns are likely weighing on the common currency, the central focus is the ECB meeting on Thursday where the master of central bank voodoo, Mario Draghi, will take centre stage. Caught between a hawk and a dove nest, Draghi will have to be at his more eloquent self to not only satisfy both sides of the council but to ensure markets are not spooked. But given the Euro markets have been trending sideways in a happy place for the past month it would be improbable the ECB announces anything other than what was leaked to the markets, an apparent ECB consensus of buying €20-€40 billion in monthly asset purchasing with the program running for another 9-12 months.

Even approaching some significant technical levels trade remains exceptionally lacklustre perhaps due to reduced EUR positioning as any constructive bias has likely evaporated in a sea of frustration the past month.

Japanese Yen

With the election in the rearview mirror and no challenges to Abenomics, the markets are free to focus on other wave makers. The disconnect with the Nikkei remains a key focus and should this correlation move back towards historical levels it will underpin USDJPY. But in the meantime, the markets have their hands full with reactant price movements from developments around tax reform while gauging USD concerted momentum over the FED chair appointment.

Mind you, New York traders were not dazzled with the USDJPY’s 113.95 NY open and went into hit the bid mode from the get-go. But at the start of APAC trade, there is sizable support at 113.30-113levels, but on a break of the psychological 113, things will get messy quick given the market is generally long USD in this space.

Australian Dollar

The main event this week is AUS CPI on Wednesday, and RBA Debelle will speak on Uncertainty on Thursday.

AUD does feel like the intransigent of G-10 trade unable to break out on the bottom or the top of current ranges. AUD lower story will be a US rates higher storyline, full stop.

Other than that, for traders looking to get short, Wednesdays CPI could present such an opportunity. In this positive USD environment fading the Aussie remains the name of the game.

The New Zealand Dollar

Is Patience a virtue? Not sure about that one with regards to the Kiwi trade.But so far this week the political landscape has shown signs of stabilising, and the onslaught has abated. Political risk usually has a way of evaporating quickly, and with little pressure from the greenback this week we could see a relief rally which would provide an opportunity to unwind some nervous nellie long Kiwi positions.

The long NZD trade remains fraught with peril given the absolute political uncertainties. Be nimble

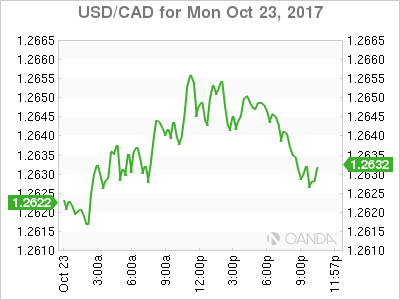

USD/CAD Canadian Dollar Drops After Wholesale Sales Miss And Dollar Resurgence

The Canadian dollar is softer on Monday after last week’s events boosted the USD against the loonie. Tax reform optimism and a message from the Trump administration that a Fed Chair candidate will be announced shortly put US yields higher. The three people short-list includes: Federal Reserve Governor Jerome Powell, economist John Taylor and current Fed Chair Janet Yellen

The Canadian economy is showing further signs of a slowdown from the impressive growth pace of the first half of the year. Wholesale sales were 0.5 percent. Last month the leading indicator of consumer spending had risen by 1.5 percent (revised today to 1.7 percent). The disappointing data echoed the retail sales data released on Friday which caused the CAD to break through the 1.25 price level.

The Bank of Canada (BoC) will announce its benchmark short term interest on Wednesday, October 25 at 10:00 am EDT. The central bank is anticipated to keep rates unchanged after an earlier unexpected rate hike in September that put the benchmark rate at 1.00 percent. A press conference by Governor Stephen Poloz will take place at 11:15 am EDT.

Meetings between Canada, Mexico and the United States continue as legislators from the three nations will meet in Mexico and Washington. JPMorgan is advising its clients to short Mexican stocks as the chances of a no deal scenario have increased. Mexico and the US were pushing initially for the renegotiation of the trade deal to be done before 2018 to avoid the political cycle ahead of Presidential elections in Mexico and the primaries in the US. The demands by the Trump administration have derailed that timeline and now the deal is in jeopardy as it appears the deal will be negotiated with a highly politicized background in 2018 making its future even more uncertain.

The USD/CAD rose 0.18 percent on Monday. The currency pair is trading at 1.2645 after the USD got an early boost against the loonie with the release of Canadian wholesale sales. Total sales at the wholesale level came in lower than expected at 0.5 percent putting more downside pressure to the Canadian currency as more signs of an economic slowdown accumulate.

On Friday retail sales fell –0.3%. Market expectations were looking for a strong +0.5% gain. The miss in retail sales was a big blow to the loonie. After the surprise rate hike in September by the Bank of Canada (BoC) and various calls for a GDP slowdown the currency is more sensitive to underperforming indicators.

Stronger headline numbers would have improved the odds of the Bank of Canada (BoC) raising rates before the end of 2017. Retail and wholesale sales data could take the BoC out of the rate hike equation for the time being. The BoC meet next Wednesday, October 25 at 10:00 am EDT.

The price of West Texas Intermediate is trading near 5.162 in the last 24 hours. Crude price levels have been stable as threats for disruption of supplies in Iraq and a drop in US drilling. Iraq is the largest producer in the Organization of the Petroleum Exporting Countries (OPEC), but an independence referendum by the oil producing Kurdish region prompted the central government to dispatch the military to intervene. Exports from the Kirkuk fields are starting to pick up and are now in 288,000 barrels per day in the Turkish pipeline, this is down from 600,000 before the conflict.

Market events to watch this week:

Tuesday, October 24

8:30pm AUD CPI q/q

Wednesday, October 25

4:30am GBP Prelim GDP q/q

8:30am USD Core Durable Goods Orders m/m

10:00am CAD BOC Monetary Policy Report

10:00am CAD BOC Rate Statement

10:00am CAD Overnight Rate

10:30am USD Crude Oil Inventories

11:15am CAD BOC Press Conference

Thursday, October 26

7:45am EUR Minimum Bid Rate

8:30am EUR ECB Press Conference

8:30am USD Unemployment Claims

Friday, October 27

8:30am USD Advance GDP q/q

Gold Starts Week With A Whimper

Gold is showing little movement in the Monday session. In the North American session, the spot price for an ounce of gold is $1279.12, down 0.10% on the day. On the release front, there are no US events on the schedule.

The Federal Reserve is in the spotlight, as Janet Yellen’s term as head of the powerful central bank expires in February 2018. President Trump has said he will nominate a new Fed head shortly, and the front runners are economist John Taylor and Federal Reserve Governor Jerome Powell. Taylor advocates a rule in which rates which be as high as 3 percent, given current economic conditions. Powell is more closely aligned to Fed Chair Janet Yellen’s monetary stance which advocates an incremental increase in rates. With the two candidates representing sharply differing views on interest rate levels, Trump’s choice for the new Fed chair could have a significant effect on monetary policy and the strength of the US dollar.

Some rare good news for President Trump translated into losses for gold on Friday. On Thursday, the US Senate passed a $4 trillion budget measure. The bill barely squeaked through, as the vote was 51-49. Still, this is represents a crucial victory for President Trump, who was desperately in need of a legislative victory. The budget measure clears the way for an overhaul reform to the tax code, one of Trump’s key campaign promises. The Republicans are hopeful of passing a new tax code by the New Year, but that could prove overly optimistic, as the Democrats are expected to resist Trump’s tax proposal.

Elliott Wave Trade Ideas Performance Update

4 positions were entered last week with total profit of 135 points and the positions are listed below.

13 Oct : GBP/USD - Short at 1.3315, exited at 1.3115 (+ 200 points)

16 Oct : AUD/USD - Short at 0.7875,

18 Oct : USD/CAD - Long at 1.2515, exited at 1.2490 (- 25 points)

19 Oct : EUR/GBP - Short at 0.8975, exited at 0.9015 (- 40 points)

| AUD EUR/JPY EUR/GBP CAD GBP GBPJPY

Jan - 15 -275 - 35 -120

Feb + 140 -17 - 40 +11

Mar - 20 +115 +132 - 19

Apr + 30 - 40 +120 + 45

May - 55 +100 - 6 -65 -60

Jun + 81 +150 - 10 +185 -120 +205

Jul - 40 - 60

Aug +155 +200 + 100 + 195 -45 - 50

Sep -50 + 165 + 5

Oct - 60 - 80 - 25 +20 +200

Nov

Dec

Y-T-D + 371 + 8 + 87 +798 - 30 +285

Candlesticks and Ichimoku Trade Ideas Performance Update

6 positions were entered among all 4 currency pairs with total loss of 93 points and the positions are listed below:

12 Oct : USD/CHF - Short at 0.9755, exited at 0.9775 (- 20 points)

13 Oct : USD/JPY - Short at 112.25, exited at 112.25 ( 0 point)

13 Oct : GBP/USD - Long at 1.3250, exited at 1.3245 (- 5 points)

19 Oct : USD/CHF - Long at 0.9790, exited at 0.9755 (- 35 points)

19 Oct : USD/JPY - Long at 112.70, exited at 112.35 (- 35 points)

19 Oct : EUR/USD - Short at 1.1850, exited at 1.1848 (+ 2 points)

| JPY EUR CHF GBP

Jan + 167 - 85 - 10 + 50

Feb + 200 +150 +93 - 59

Mar -23 -70 -23 - 35

Apr + 65 + 93 + 50 - 40

May - 65 - 35 + 100 -175

Jun -100 -10 - 10 +175

Jul + 85 - 35 - 8

Aug + 35 +210 + 35 +65

Sep +129 +210 +200 - 70

Oct - 35 +2 - 90 - 30

Nov

Dec

Y-T-D + 457 +425 +337 -109

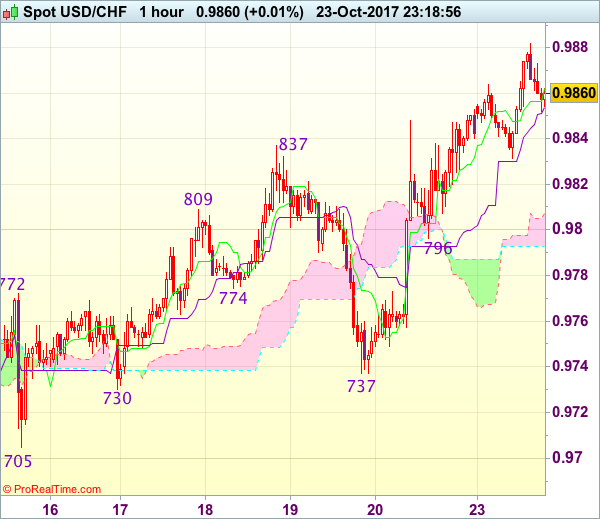

Trade Idea Wrap-up: USD/CHF – Buy at 0.9795

USD/CHF - 0.9865

Most recent candlesticks pattern : N/A

Trend : Up

Tenkan-Sen level : 0.9862

Kijun-Sen level : 0.9854

Ichimoku cloud top : 0.9807

Ichimoku cloud bottom : 0.9793

Original strategy :

Buy at 0.9795, Target: 0.9895, Stop: 0.9760

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9795, Target: 0.9895, Stop: 0.9760

Position : -

Target : -

Stop : -

As the greenback rallied after finding renewed buying interest at 0.9737 late last week, adding credence to our view that recent upmove has resumed and bullishness remains for the rise from 0.9421 low to extend headway to 0.9870 and possibly towards 0.9900, however, near term overbought condition should limit upside and price should falter below 0.9940-50, bring retreat later.

In view of this, we are looking to buy dollar again on pullback as support at 0.9796 should limit downside and bring another rise. Below 0.9765-70 would defer and suggest top is possibly formed, risk test of indicated support at 0.9730-37, however, break there is needed to provide confirmation, then further fall to previous support at 0.9705 would follow.

Trade Idea Wrap-up: GBP/USD – Sell at 1.3285

GBP/USD - 1.3183

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.3183

Kijun-Sen level : 1.3193

Ichimoku cloud top : 1.3160

Ichimoku cloud bottom : 1.3150

Original strategy :

Sell at 1.3285, Target: 1.3155, Stop: 1.3320

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.3285, Target: 1.3155, Stop: 1.3320

Position : -

Target : -

Stop : -

As cable found good support at 1.3088 late last week and has staged a strong rebound, suggesting consolidation with initial upside bias would be seen for recovery to 1.3240-45 (61.8% Fibonacci retracement of 1.3338-1.3088), however, price should falter below indicated resistance at 1.3287 and bring retreat later, below 1.3130-35 would bring test of said support at 1.3088 but break there is needed to extend the fall from 1.3338 to 1.3050, then towards recent low at 1.3027.

In view of this, wee are looking to sell cable on further subsequent recovery as resistance at 1.3287 should limit upside and bring another decline later. Only above 1.3312 resistance would abort and extend further gain to said recent high at 1.3338 which is likely to hold from here.