Sample Category Title

Bank Of England Preview: Taking Back Emergency Cut From 2016

- We expect the Bank of England (BoE) to hike the Bank Rate by 25bp to 0.50% from 0.25% with a vote count of 7-2.

- We think this is more about taking back the emergency cut from August 2016, just after the Brexit vote, and not the beginning of a new hiking cycle for now.

- We expect the BoE to repeat that it will hike at only 'a gradual pace and to a limited extent'.

- The direction for EUR/GBP from here will crucially depend on whether the BoE signals that the November hike is a one-off or not

Not the beginning of a new hiking cycle for now

After the surprisingly hawkish shift in tone at the latest Bank of England (BoE) meeting in September, we think the BoE is going to hike the Bank Rate by 25bp from 0.25% to 0.50% at its meeting on Thursday (in line with consensus and market pricing). The shift is due to a combination of low unemployment rate and high inflation. We think the vote count is likely to be 7-2, as Sir David Ramsden and Sir Jonathan Cunliffe have indicated that they think it is too early to hike. However, even Gertjan Vlieghe, who was previously considered very dovish, now seems to support a hike and we think most BoE members are inclined to vote with the majority.

As we believe the hike is relatively certain, the bigger question is whether this is the beginning of a new hiking cycle or not. We are in the camp believing this is more about taking back the emergency cut from August last year just after the Brexit vote and do not forecast another rate hike in 2018. In this regard, it is worth noting what the BoE says about the current market pricing of BoE, as the BoE has a tendency to compare the current market pricing to the consensus view among BoE members. This is going to be very important for whether or not this is just a 'one and done hike', as markets have priced in a second hike by autumn 2018, which we think is too hawkish. If we are right, the BoE may say that markets are overestimating the number of rate hikes, although the BoE may try to keep its flexibility here. Regardless, we expect the BoE to repeat that it will hike at only 'a gradual pace and to a limited extent'.

There are multiple reasons why we do not believe this is the beginning of a new cycle despite the current situation with low unemployment and high inflation: we still believe the BoE is too optimistic on the growth outlook, as it projects a pickup in private consumption growth due to higher wage growth, which we are having a hard time seeing in the current situation. The still subdued wage growth also means that domestically generated inflation is not as high as actual inflation, which is pushed higher temporarily by the big fall in GBP, which again passes through to consumer prices only slowly. By the end of the day, it is the underlying inflation pressure that is important for the BoE. Finally, but not least, the ECB is not expected to hike before 2019 and has just extended QE by nine months (although slowing the buying pace) and we do not believe the BoE wants to tighten monetary policy too much relative to the ECB

This is one of the big meetings, so we will also get updated projections and a press conference. We expect inflation to be revised higher in the short-term but to be unchanged further out on the forecast horizon. Although GDP growth is weaker now than previously, we think the BoE will continue signalling a pickup in GDP growth due to higher wage growth. The unemployment rate has continued to turn out lower than expected and hence we expect another downward revision of the projections.

EUR/GBP: downside risks if BoE hesitant that hike is a one-off

The direction for EUR/GBP from here will crucially depend on whether BoE signals that the November hike is a one-off. With the market priced some 90% for the hike, this should in itself deliver only limited GBP strength but a knee-jerk reaction in EUR/GBP to test the 0.88 level could be on the cards. If the BoE manages to convince the market that the hike is a one-off, then the cross should stick to the 0.87- 0.90 range but we emphasise that there is a significant risk the BoE will fail to conjure up speculation on further nearterm tightening. Coupled with negative EUR momentum post the ECB's dovish tapering, this heightens the risk of a move below 0.88 on the announcement. However, we still target this level (0.88) in 1-3M, as we think the BoE will be keen to stress its data and Brexit dependence, which we deem limits the scope for further policy tightening on a 12M horizon. We still expect EUR/GBP to edge only a little lower on a six to 12M horizon

Russia’s Central Bank Cut Its Key Rate By 25Bp To 8.25%

Market movers today

Globally, we do not have many important data releases due today but the week is going to be interest ing. US PCE inflat ion data may at tract some at tention today but note that we implicitly got t he dat a in connect ion wit h Friday's first estimat e of Q3 GDP . Assuming no revisions to previous months, both CPI and GDP figures indicate PCE core rose 0.1% m/m in September (unchanged at 1.3% y/y).

In Europe, confidence indicators for consumers and businesses is due out .

In the Scandies, Norwegian retail sales and Swedish wage growth data are due out this morning.

After last week's ECB meet ing (see ECB review: ECB opts for ‘lower-for-longer’ QE extension, 26 October 2017), focus turns to the Fed on Wednesday and Bank of England on Thursday. We do not expect Fed to send any new signals (see FOMC preview: No new signals, while Trump is set to announce new Fed chair soon, 25 October 2017) but the bank of England will most likely hike the Bank rate by 25bp from 0.25% to 0.50%. See Bank of England Preview: Taking back emergency cut from 2016, 30 October 2017.

Selected market news

The Spanish political crisis continues to develop as a test of strength looms today. On Sunday, hundreds of thousands of Catalans marched in the st reet s of Barcelona, calling for the region to remain part of Spain in the biggest show of force so far for a united Spain since the crisis began. T he demonst rat ion followed t he regional parliament 's declarat ion of independence on Friday, which led Madrid to act ivate Art icle 155, dissolving the Catalan government and calling for new elect ions in the region for 21 December. Today, Catalan regional minist ries will reopen under direct cont rol by Madrid, which could be a real test of st rength for both sides. Former Catalan leader Carles Puigdemont is calling for peaceful opposit ion and some Catalan ministers have refused to accept the direct ives from the central government removing them from power. Hence, there is a risk that Madrid could st ruggle to enforce its rule.

Decision on Fed Chair imminent. According to a video President Trump has posted on Instagram, he is set to announce the next Fed Chair this week. Our base case scenario is that Trump will nominate Jerome H. Powell (current Fed Board Governor nominated by President Bush) as Janet Yellen's successor. Republicans can support Powell while he at t he same t ime is a guarantor of the status quo (i.e. to cont inue the gradual hiking cycle and quant itat ive t ightening programme). The other favourite is John B. Taylor, who would be the hawkish choice.

Russia's central bank cut its key rate by 25bp to 8.25% on Friday, following a decline in inflat ion to 2.7% y/y.

Equity markets ended the week on a positive note. In the US, S&P500 closed 0.8% up at a new record high, while most European bourses also closed in the green. In Spain, however, the IBEX index closed 1.5% lower, reflecting the polit ical turmoil in the country. This morning, Asian stocks are trading higher, boosted by solid earnings from US tech companies.

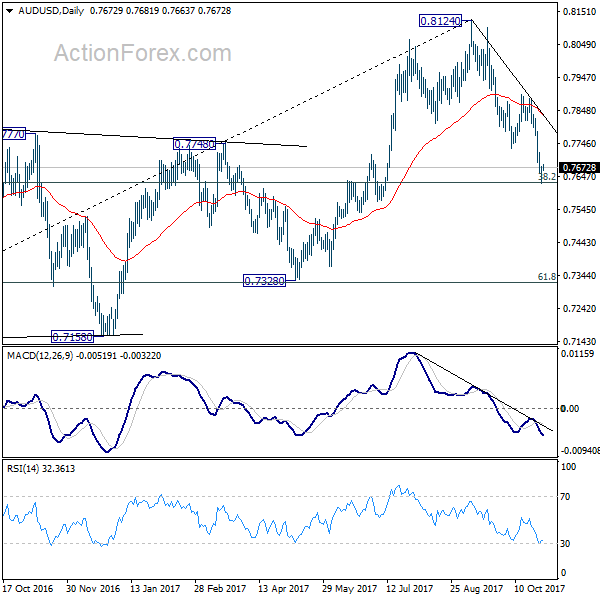

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7641; (P) 0.7659; (R1) 0.7693; More...

Intraday bias in AUD/USD remains neutral for consoldiation above 0.7624 temporary low. Upside of recovery should be limited well below 0.7896 resistance to bring decline resumption. Firm break of 0.7624 will resume whole decline from 0.8124 and target next key cluster level at 0.7322/8.

In the bigger picture, corrective rise from 0.6826 medium term bottom is likely completed at 0.8124, after hitting 55 month EMA (now at 0.8067). Decisive break of 0.7328 key cluster support (61.8% retracement 0.6826 to 0.8124 at 0.7322) will confirm. And in that case, long term down trend from 1.1079 (2011 high) will likely be resuming. Break of 0.6826 will target 61.8% projection of 1.1079 to 0.6826 from 0.8124 at 0.5496. This will now be the favored case as long as 0.7896 near term resistance holds.

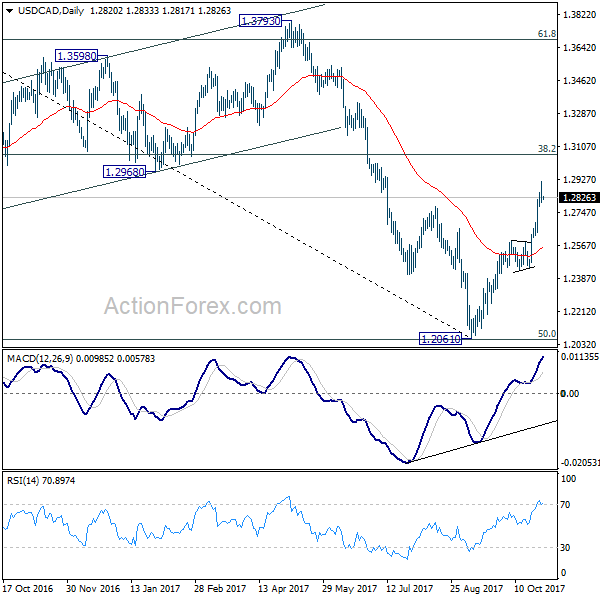

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2766; (P) 1.2841; (R1) 1.2881; More....

Intraday bias in USD/CAD remains neutral for consolidation below 1.2916 temporary top. Downside of retreat should be contained above 1.2598 resistance turned support and bring rally resumption. Medium term trend in USD/CAD should have reversed. Break of 1.2916 will extend the rise from 1.2061 to 38.2% retracement of 1.4689 to 1.2061 at 1.3065.

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4689 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Rise from 1.2061 medium term bottom should now target 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Firm break there will target 1.3793 key resistance next (61.8% retracement at 1.3685). We'll now hold on to this bullish view as long as 1.2450 support holds.

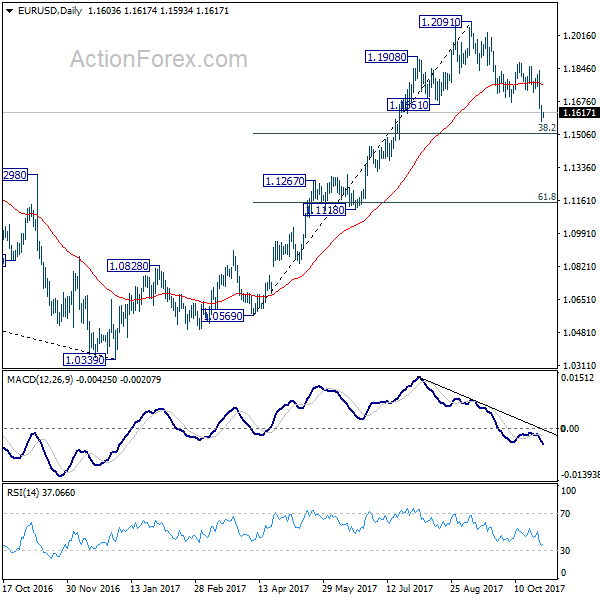

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1568; (P) 1.1612 (R1) 1.1651; More...

Intraday bias in EUR/USD remains on the downside for the moment. Current fall from 1.20191 would target 38.2% retracement of 1.0569 to 1.2091 at 1.1510. We'd expect strong support from there, at least on first attempt, to bring rebound. Above 1.1643 minor resistance will turn bias neutral first. But break of 1.1879 is needed to confirm completion of the decline. Otherwise, near term outlook remains bearish. Meanwhile, sustained break will of 1.1510 will carry larger bearish implication and target 55 week EMA (now at 1.1346).

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be cautious on 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

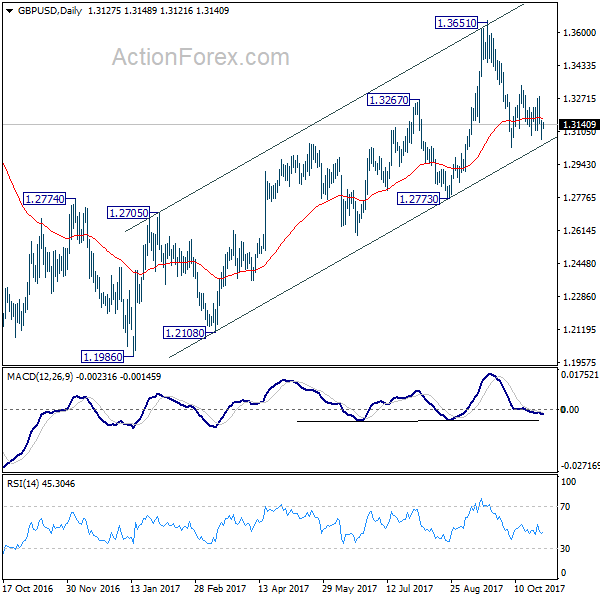

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3072; (P) 1.3116; (R1) 1.3164; More....

Intraday bias in GBP/USD remains neutral at this point. On the downside, firm break of 1.3026 support will resume the decline from 1.3651 and target 1.2773 key support level. This will also revive the case of medium term reversal. On the upside, in case of another rally, upside should be limited by 61.8% retracement of 1.3651 to 1.3026 at 1.3412 to bring fall resumption finally.

In the bigger picture, while the medium term rebound from 1.1946 was strong, GBP/USD hit strong resistance from the long term falling trend line. Outlook is turned a bit mixed and we'll stay neutral first. On the downside, decisive break of 1.2773 key support will argue that rebound from 1.1946 has completed. The corrective structure of rise from 1.1946 to 1.3651 will in turn suggest that long term down trend is now completed. Break of 1.1946 low should then be seen. On the upside, break of 1.3835 support turned resistance will revive the case of trend reversal and target 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466 .

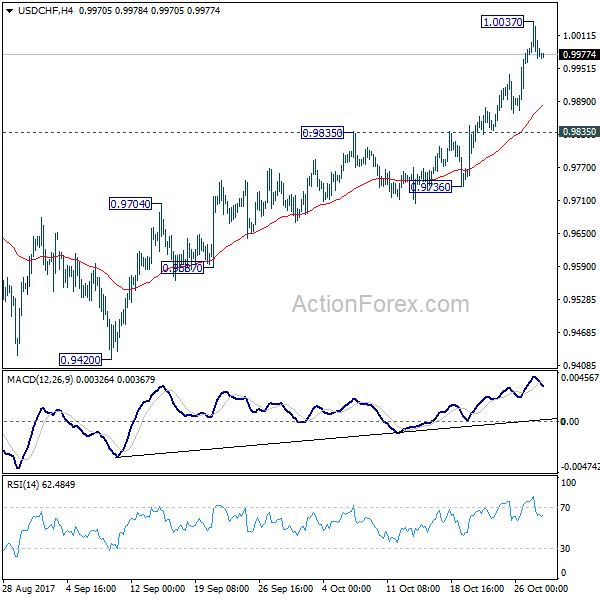

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9942; (P) 0.9989; (R1) 1.0019; More....

Intraday bias in USD/CHF remains neutral for consolidation below 1.0037 temporary top. Downside of retreat should be contained above 0.9835 resistance turned support and bring rally resumption . Since 61.8% retracement of 1.0342 to 0.9420 at 0.9990 is already met, break of 1.0037 will turn bias to the upside for 1.0342 key resistance next.

In the bigger picture, current development suggests that USD/CHF has defended 0.9443 (2016 low) key support level again. Rise from 0.9420 could is a medium term up move and should target a test on 1.0342 high. This represents the upper end of a long term range that started back in 2015. On the downside, break of 0.9736 support is now needed to indicate completion of the rise from 0.9420. Otherwise, further rally will remain in favor in medium term.

Market Update – Asian Session: Regional Bond Yields Gain

Asia Summary

Asian equity markets have opened generally higher, following Friday's gains seen on the Nasdaq.

In the tech sector, Sharp has gained over 2%, as the company raised its FY operating profit guidance. Shares of Softbank and Hitachi have traded higher by over 1%, while Nintendo is currently flat ahead of its later today earnings report. Samsung Electronics has gained over 1.5% ahead of its earnings presentation due on Oct 31st. Nasdaq Futures are trading at around flat levels. According to a press report out of Taiwan, Apple is said to have asked suppliers for the iPhone X to double their capacities amid stronger than expected demand.

Nippon Steel has declined by over 1%, as Q2 profits missed market expectations. Kobe Steel, which is expected to release its earnings report later today, has gained over 1.5%. In China Baoshan Iron & Steel has declined by over 0.4% amid the release of its earnings report.

Japanese industrial name Komatsu has traded higher by over 3% after the company reported better than expected Q2 profits and raised its FY guidance. Chinese rail equipment firm CRRC Corp has gained over 1% after reporting an increase in Q3 profits. Hong Kong listed cement producer Anhui Conch has gained over 2% following its earnings report.

PetroChina's shares are trading higher ahead of its later today earnings report. Energy producers in Australia are trading generally higher, following the over 2% rise seen in oil prices on Friday's US session.

As of the time of writing, markets have traded off of their best levels. Japanese mega banks are trading generally lower on the session, following the recent gains that have been seen since Japan's general election results.

In China, Bank of Communications and China Merchants Bank have traded lower following their respective earnings reports. BYD is also lower by over 3%, after releasing its financial results. The overall Shanghai Composite has declined by over 1%.

China's 5 and 10-year government bond yields have added on to the gains seen during the prior week and are currently at the highest levels since late 2014. In South Korea, bond yields are trading lower. Earlier during the session, the Bank of Korea announced that it was planning to repurchase government bonds later this week. Looking ahead on Wednesday's session, South Korea is due to release its Oct CPI data.

On tomorrow's session, China's October manufacturing and non-manufacturing PMI data is due to be released, along with the Bank of Japan's policy statement and forecasts. Other notable macro-economic releases for this week include, New Zealand Q3 employment change (Wed), US Fed decision (Wed), Australia Sept Trade Balance (Thursday), Bank of England decision (Thursday), Australia Sept retail sales (Friday) and US Oct Nonfarm payrolls (Friday).

Japanese companies due to report earnings later today include Alps Electric, Casio, ibiden, Kao Corp, Konica Minota, Kyocera, Nippon Carbon, Nippon Electric Glass, Nomura, ORIX Corp, Seikisui Chemicals, Stanley Electric, Sumitomo Dainippon Pharma, TDK and West Japan Railway.

US companies seen reporting on Monday include Mondelez International. HSBC reported Q3 results which exceeded analyst expectations.

Key economic data

(JP) JAPAN SEPT RETAIL SALES M/M: 0.8% V 0.8%E; RETAIL TRADE Y/Y: 2.2% V 2.3%E; Department Store, Supermarket Sales y/y: 1.9% v 1.5%e

(NZ) Statistics NZ: Corrects Q2 retail sales q/q to 1.7% from 2.0%; delays Q3 release on new methodology

Speakers and Press

Japan

(JP) BOJ Gov Kuroda likely to stay for another 5 year term after his current term ends on April 2018 – Nikkei

(JP) Japan FSA said to set capital requirement rules for high frequency trading (HFT) firms - Japanese Press

Korea

(KR) Bank of Korea (BOK) Official: Planning to repurchase bonds this week to stabilize the market

China/Hong Kong

(CN) CICC Research sees 2018 real GDP at 6.9% v 6.7% prior

Australia/New Zealand

(AU) Australia Treasurer Morrison: Businesses are seeing best conditions since 2008

(AU) Australia Queensland calls snap election after the ruling center-left Labor Party lost its legislative majority

(NZ) New Zealand PM Ardern: want to legislate to ban foreign buyers of existing NZ homes before TPP-11 is ratified

Asian Equity Indices/Futures (00:00ET)

Nikkei -0.2%, Hang Seng +0.0%; Shanghai Composite -0.7%; ASX200 +0.4%, Kospi +0.3%

Equity Futures: S&P500 -0.2%; Nasdaq100 -0.1%, Dax -0.1%; FTSE100 -0.3%

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.1615-1.1594; JPY 113.83-113.52; AUD 0.7682-0.7664;NZD 0.6887-0.6840

Dec Gold +0.1% at $1,272/oz; Dec Crude Oil +0.1% at $53.94/brl; Dec Copper -0.2% at $3.09/lb

(AU) Australia MoF buys back A$500M in Oct 2018 and Mar 2019 bonds

(AU) Australia MoF sells A$500M in 2029 bonds, avg yield 2.8110%, bid to cover 6.5x

(CN) PBoC OMO: Injects CNY150B combined CNY140B in 7-day, 14-day and 63-day reverse repos v CNY140B prior; Net injection CNY40B

USD/CNY *(CN) PBOC SETS YUAN REFERENCE RATE AT 6.6487 V 6.6473 PRIOR

(CN) CHina MoF sells 5-yr special treasury bonds at 3.9206%

Equities notable movers

Australia/New Zealand

NAB.AU Agreed to a A$30M settlement with the Australian Securities and Investments Commission (ASIC) of the Bank Bill Swap Rate (BBSW) legal action – filing; +0.1%

COE.AU Reports Q1 production 0.43 MBOE v 0.09M BOE y/y; Rev A$14.4M v A$4.9M y/y; +6.7%

TNG.AU Reports FY17 (A$) Net loss 4.4M v loss 7.1M y/y; Total income 504K v 6K y/y - Annual reports; -6%

Japan

8411.JP Said to be considering cutting up to a third of its global workforce over the next 10 years – FT; -0.1%

7731.JP Reports prelim H1 Net ¥14B v ¥13B guided; Op ¥23B v ¥17B guded;to discontinue China unit of imaging business; +0.8%

Korea

004990.KR Shares resume trading after restructuring into holding company; +17.5%

009150.KR Reports Q3 (KRW) Net profit 74.5B v 3.85B y/y, Op profit 103.2B v 12.8B y/y, Rev 1.84T v 1.47T y/y; +5%

042660.KR Resumes trading after more than 1-yr halt; -30%

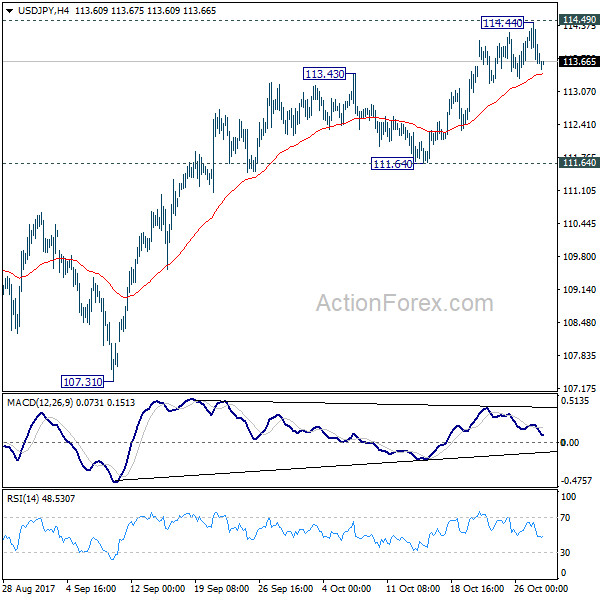

USD/JPY Daily Outlook

Daily Pivots: (S1) 113.39; (P) 113.91; (R1) 114.20; More...

Intraday bias in USD/JPY remains neutral for the moment. Pull back from 114.44 could extend lower. But after all, outlook will stays cautiously bullish as long as 111.64 support holds. Decisive break of 114.49 key resistance will confirm that correction pattern from 118.65 has completed at 107.31 already. And USD/JPY should then target a test on 118.65.

In the bigger picture, medium term rise from 98.97 (2016 low) is not completed yet. It should resume after corrective fall from 118.65 completes. Break of 114.49 resistance will likely resume the rise to 61.8% projection of 98.97 to 118.65 from 107.31 at 119.47 first. Firm break there will pave the way to 100% projection at 126.99. This will be the key level to decide whether long term up trend is resuming.

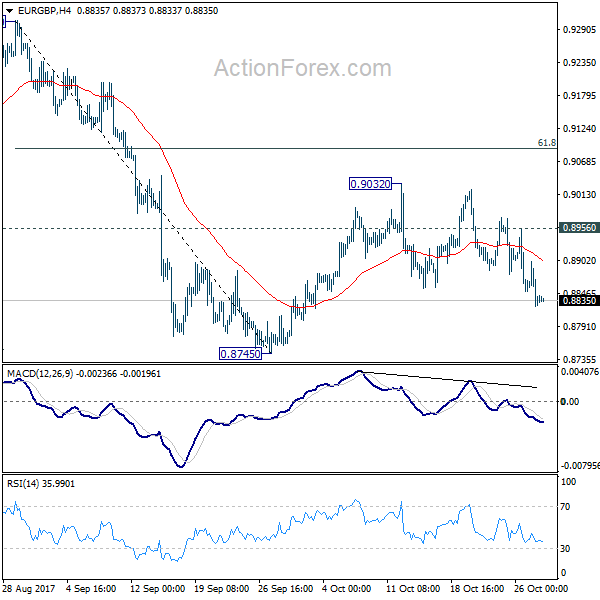

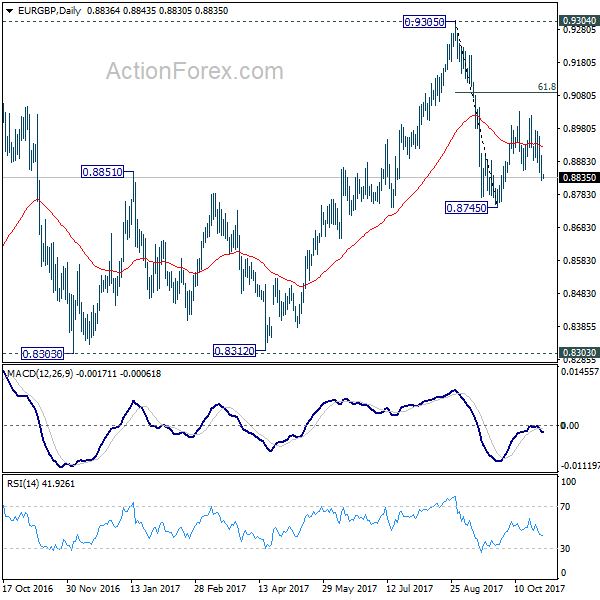

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8809; (P) 0.8855; (R1) 0.8885; More...

Intraday bias in EUR/GBP remains mildly on the downside for 0.8745 support. Break will will resume whole fall from 0.9305 and target 0.8303 key support level. On the upside, above 0.8956 minor resistance will extend the corrective rise from 0.8745 with another rise. But upside should be limited by 61.8% retracement of 0.9305 to 0.8745 at 0.9091 to bring fall resumption eventually.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of another fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.