Sample Category Title

Trade Idea: GBP/USD – Sell at 1.3195

GBP/USD – 1.3144

Original strategy :

Sell at 1.3170, Target: 1.3000, Stop: 1.3230

Position: -

Target: -

Stop: -

New strategy :

Sell at 1.3195, Target: 1.3030, Stop: 1.3255

Position: -

Target: -

Stop:-

As sterling has recovered after falling to 1.3070 on Friday, suggesting minor consolidation above this level would be seen, however, reckon upside would be limited to 1.3200 and bring another decline later, below said support would add credence to our view that the rebound from 1.3027 has ended at 1.3338, then a retest of 1.3027 would follow, having said that, break there is needed to confirm early decline from 1.3658 top has resumed for further fall to psychological support at 1.3000 first.

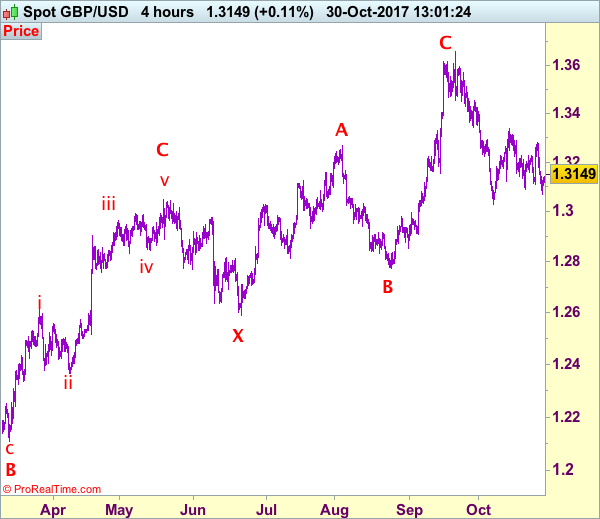

In view of this, we are looking to sell cable on recovery as 1.3200 should limit upside and bring another decline later. Above 1.3240 would defer and prolong choppy consolidation, risk rebound to indicated resistance area at 1.3279-87 which is likely to hold from here. Our preferred count is that (pls see the attached chart) the wave IV is unfolding as a complex double three (ABC-X-ABC) correction with 2nd wave B ended at 1.2774, hence 2nd wave C could have ended at 1.3658.

Our preferred count on the daily chart is that cable's rebound from 1.3500 (wave (A) trough) is unfolding as a wave (B) with A ended at 1.7043, followed by triangle wave B and wave C as well as wave (B) has ended at 1.7192, the subsequent selloff is the larger degree wave (C) which is still unfolding with minor wave (III) of larger degree wave 3 ended at 1.1986, hence wave (IV) correction is in progress which could either be a triangle wave (IV) of a complex formation but upside should be limited to 1.3500 and price should falter well below 1.4000, bring another decline in wave (V) of 3 for weakness to 1.1500, then 1.1200.

Trade Idea: GBP/JPY – Sell at 150.00

GBP/JPY - 149.35

Original strategy:

Sell at 150.00, Target: 148.00, Stop: 150.60

Position: -

Target: -

Stop: -

New strategy :

Sell at 150.00, Target: 148.00, Stop: 150.60

Position: -

Target: -

Stop:-

Last week’s sharp retreat from 151.40 together with the breach of previous support at 149.15 add credence to our view that the rebound from 146.95 has ended there and consolidation with downside bias is seen for weakness to 148.50, then 148.00, however, break of support at 147.80 is needed to retain bearishness and signal another leg of decline from 152.85 top is underway for further fall towards said support at 146.95.

In view of this, we are looking to sell sterling on recovery as 150.00-10 should limit upside and bring another decline later. Above 150.50-60 would prolong consolidation and bring rebound to 151.00 but said resistance at 151.40 should hold. Only a break of this resistance would revive bullishness and extend the rebound from 146.95 towards 151.90-00 first.

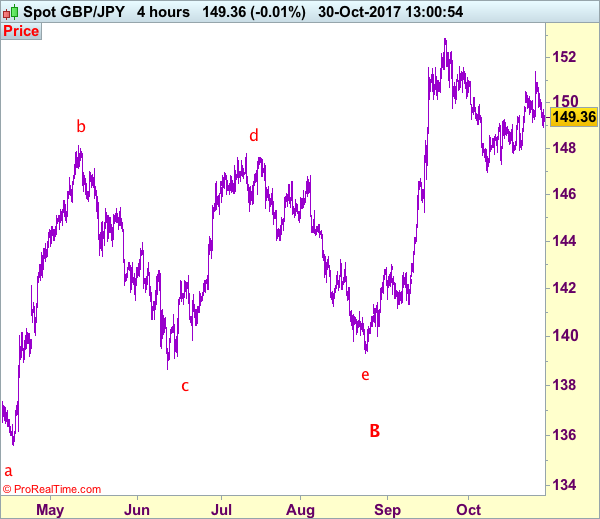

Our preferred count is that larger degree wave V with circle is unfolding from 251.12 with wave (I) 219.34, (II): 241.38 and wave (III) is subdivided into 1: 192.60, 2: 215.89 (23 Jul 2008) and wave 3 ended at 118.87 earlier in 2009. The correction from there to 162.60 is wave 4 which itself is a double three and is labeled as first a-b-c ended at 151.53, followed by wave x at 139.03, 2nd a ended at 162.60, 2nd b at 146.75 and 2nd c leg of wave 4 ended at 163.00. Therefore, the decline from 163.00 to 116.85 is now treated as wave 5 which also marked the end of larger degree wave (III), hence wave (IV) major correction has commenced for retracement of the wave (III) from 241.38 and upside target at 183.95-00 (50% Fibonacci retracement of the wave (II) from 241.38) had been met, a drop below 160.00 would suggest wave (IV) has ended at 195.85, bring decline in wave (V) for initial weakness to 130 (already met) and 120.

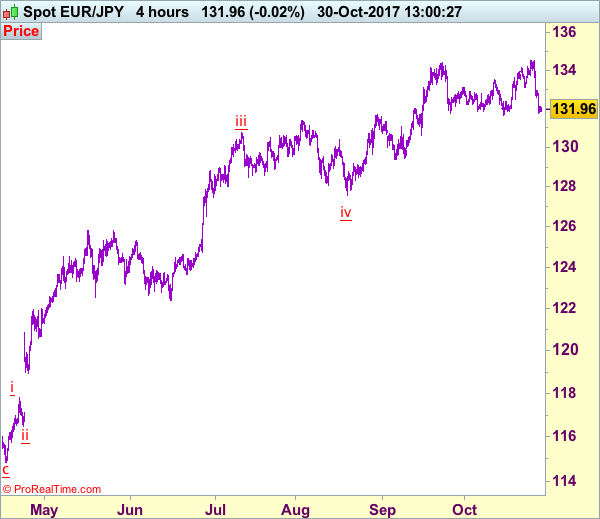

Trade Idea: EUR/JPY – Sell at 132.70

EUR/JPY - 131.97

Original strategy:

Sell at 133.50, Target: 131.50, Stop: 134.10

Position: -

Target: -

Stop: -

New strategy :

Sell at 132.70, Target: 130.70, Stop: 133.30

Position: -

Target: -

Stop:-

The single currency tumbled last week after marginal rise to 134.50, adding credence to our view that top has been formed there and consolidation with downside bias remains for test of previous support at 131.66, break there would provide confirmation and signal correction of early upmove has commenced, hence further fall to 131.00, then towards 130.50-60 would follow but near term oversold condition should limit downside to psychological level at 130.00, bring rebound later.

In view of this, we are still looking to sell euro on recovery but at a lower level as 132.70-80 should limit upside and bring another decline later. Above 133.10 would defer and suggest first leg of corrective decline from 134.50 top has ended, risk a stronger rebound to 133.50-60 but still reckon upside would be limited to 133.95-00, price should falter well below said last week’s high at 134.50, bring another selloff later.

Our latest preferred count is that wave (ii) is ABC-X-ABC which ended at 123.33 and wave (iii) is unfolding with wave iii ended at 100.77, followed by wave iv at 111.57 and wave v as well as the wave (iii) has ended at 97.04, followed by wave (iv) at 111.43 and wave (v) has ended at 94.12 which is also the end of the larger degree v, this also implied the major wave (C) has also ended there, hence major correction has commenced from there with (A) leg unfolding in its lower degree wave c which has possibly ended at 145.69. Under this count, A-B-C wave (B) has commenced with A leg ended at 136.23, wave B at 143.79 and wave C has possibly ended at 149.79.

Our larger degree count is that the decline from 139.26 is wave (C) and is sub-divided into a diagonal triangle i-ii-iii-iv-v with wave i - 105.44, wave ii- 123.33, wave iii - 97.03, wave iv - 111.43, followed by the final wave v as well as the end of wave (C) at 94.12, this also mark the bottom of larger degree wave B. Under this count, major rise in wave C has commenced as an impulsive wave with minor wave III ended at 145.69, wave V is still in progress for further gain to 150.00. Having said that, this so-called wave V could well be the first leg of larger degree 5-waver wave C and this wave C should bring at least a retest of wave A top at 169.97 (July 2008).

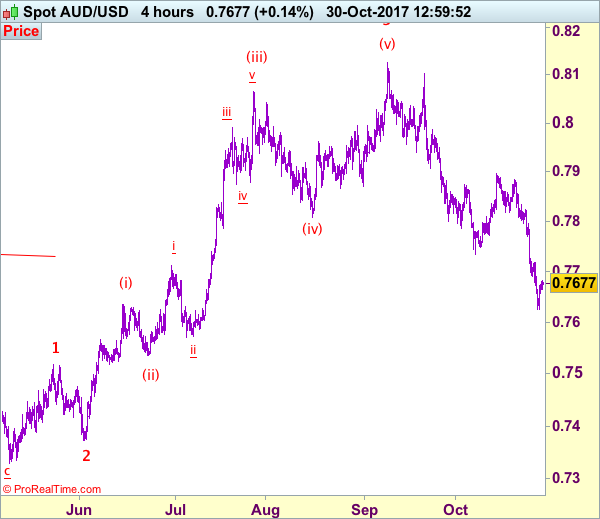

Trade Idea: AUD/USD – Sell at 0.7720

AUD/USD – 0.7676

Original strategy:

Sell at 0.7720, Target: 0.7550, Stop: 0.7780

Position: -

Target: -

Stop:-

New strategy :

Sell at 0.7720, Target: 0.7550, Stop: 0.7780

Position: -

Target: -

Stop:-

As aussie found support at 0.7625 late last week and has rebounded, suggesting consolidation above this level would be seen and corrective bounce to 0.7700 cannot be ruled out, however, reckon 0.7720-25 would limit upside and bring another decline later, below said support would add credence to our view that recent decline from 0.8125 top is still in progress and may extend further weakness to 0.7600, having said that, loss of downward momentum should prevent sharp fall below 0.7550 and reckon 0.7500 would hold from here, bring rebound later.

In view of this, we are looking to reinstate short on recovery as 0.7720-25 should limit upside and bring another decline. Above previous support at 0.7770 would defer and suggest a temporary low is possibly formed, bring rebound to 0.7800 and then towards 0.7825-35 later.

On the 4-hour chart, recent upmove from 0.7329 is unfolding as an impulsive rise with wave 3 as well as smaller degree wave (iii) extending, only minor wave v of (iii) has ended at 0.8125, hence bullishness remains for this move to extend headway to 0.8200, then towards 0.8300, however, reckon upside would be limited to 0.8400 and the final wave 5 should falter below 0.8500, bring correction later.

Market Morning Briefing: The Euro-Yen Fell Further On Friday

STOCKS

Dow (23434.19, +0.14%) is almost stable in the 23250-23500 region but could eventually attempt a rise to 23750. Near term looks range bound with chances of moving up further in the medium term.

Dax (13217.54, +0.64%) looks strong just now and could move up in the coming sessions towards 13500. Bulls are dominant and could take the index higher in the coming weeks.

22666 is the next important resistance on Nikkei (21991.16, -0.08%) and the index could be eventually heading towards it. Before that the interim target of 22250 remains intact for the coming sessions.

Shanghai (3377.92, -1.14%) fell sharply in early trade today losing all the gains seen last week. Now the broad 3350-3430 region is likely to hold in the near term bringing in a bounce in the index within the next couple of sessions.

Nifty (10323.05, -0.20%) has resistance near 10365 on the daily charts. While that holds, the index could come off towards 10250 or lower in the near term before again resuming the upward rally. Near term looks bearish while below 10365.

COMMODITIES

Gold (1271.52) is trading above important support region of 1250-1260 and while that holds could possibly bounce back towards 1290-1300 levels in the near term. That could well go with the resistance on the US Dollar Index which has a decent resistance near 95.00-95.20 which is likely to hold for now.

Brent (60.34) has moved up as expected. Resistance near 61 is likely to hold pushing the crude price to lower levels of 58.

WTI (53.91) is trading just below immediate resistance and if that holds, the price can come down in the next few sessions towards 53.00 or even lower.

Copper (3.0975) has broken below 3.10 much faster than expected maybe due to the fall In the Chinese stock index. Near to medium term looks bearish.

FOREX

Maybe the markets will be a little quiet for a couple of days after last week's volatility. Also, the FOMC is coming up on Wednesday.

The Euro (1.1610), which saw of a low of 1.1573 on Friday, is likely to have Support at 1.1510 while the Dollar Index (94.82) has immediate Resistance at 95.00-20. Both these Support and Resistance could turn out to be relatively strong.

Dollar-Yen (113.65) has come off from Friday's high of 114.45, just below the stated Resistance at 114.50. A break below 113.50 (possible) can lead to test of 113.10-00. Overall upside might be limited to 115.00 in the medium term.

The Euro-Yen (131.92) fell further on Friday and the market might try to explore prospects of fall towards 130 in the next few weeks. However, immediate Support is seen in the 131.50-35 region.

The Pound (1.3138) dipped to 1.3068 on Friday. It has medium term Support at 1.3070-40 now and may trade sideways between 1.3040-3300 for some days. The Aussie (0.7678)is finding some Support in the 0.7630-20 region. Below this, there is a jumble of Supports down to 0.7520-00. Expect messy trade between 0.77-76 for a couple of days. The earlier anticipated fall towards 0.7520 might not be easy.

Dollar-Yuan (6.6438) seems to be on a slow rise towards 6.67. Dollar-Rupee (65.045) might be quiet between 64.90-65.20 for a couple of days, deciding the future course of action.

INTEREST RATES

US FOMC on Wednesday. Will the Fed surprise with an earlier than expected rate hike? By the presence of immediate Resistances at 3.00% on the 30Yr (2.94%), at 2.50% on the 10Yr (2.43%) and near 2.20% on the 5Yr (2.04%), it might seem that they will not try to surprise the market.

The US Yield Curve (30-10 Spread 0.51% and 30-5 Spread 0.90%) could flatten a bit again, with the Near end moving up a little more than the Middle and Far end sections.

A rate hike, if it happens on Wednesday, can lead to volatility because it is not expected.

USDCHF – Looks To Strengthen Further But With Caution

USDCHF - With the pair closing higher the past week, risk remains to the upside. But with price rejection seen on Friday (daily chart), corrective pullback is likely. On the downside, support lies at the 0.9950 level. A turn below here will open the door for more weakness towards the 0.9900 level and then the 0.9850 level. On the upside, resistance resides at the 1.0000 level where a break will clear the way for more strength to occur towards the 1.0050 level. Further out, resistance comes in at the 1.0100 level. Above here if seen will turn attention to 1.0150. All in all, USDCHF faces further upside pressure.

EURUSD – Bearish, Vulnerable But With Caution

EURUSD - With the pair selling off the past week, more weakness is likely. Resistance comes in at 1.1650 level with a cut through here opening the door for more upside towards the 1.1700 level. Further up, resistance lies at the 1.1750 level where a break will expose the 1.1800 level. Conversely, support lies at the 1.1550 level where a violation will aim at the 1.1500 level. A break of here will aim at the 1.1450 level. Below here will open the door for more weakness towards the 1.1400. Its weekly RSI is bearish and pointing lower suggesting further weakness. All in all, EURUSD continues to face downside threats but with caution of a recovery.

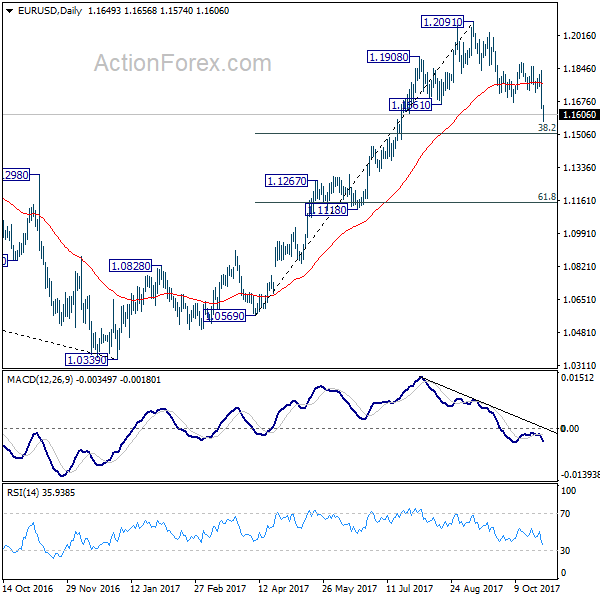

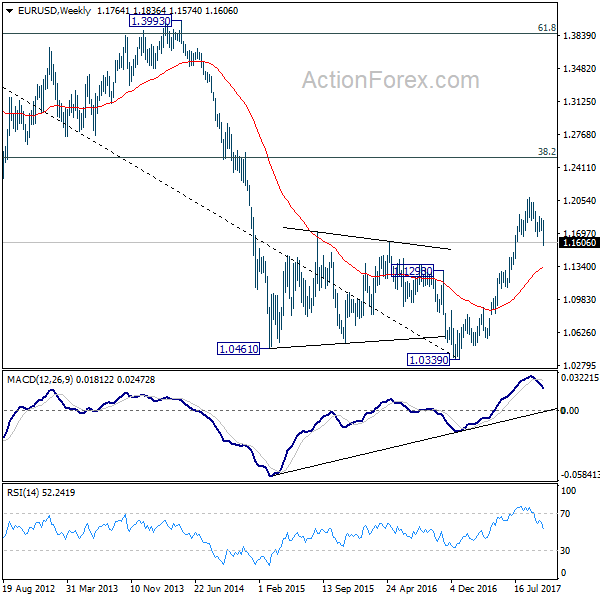

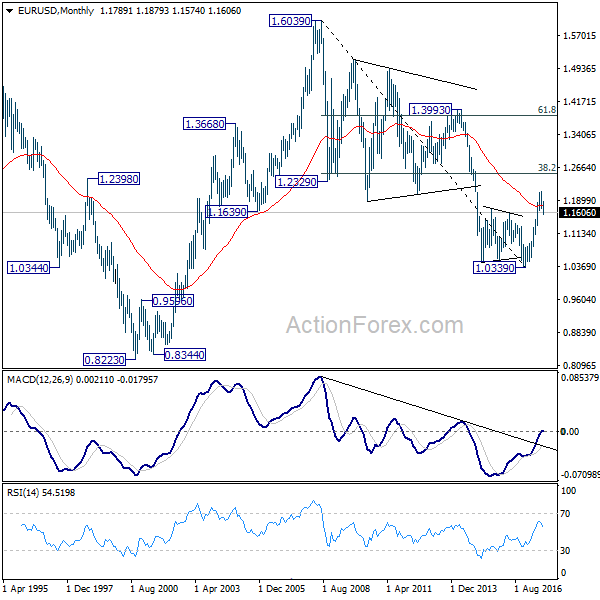

EUR/USD Weekly Outlook

EUR/USD's fall from 1.2091 resumed last week but taking out 1.1669 support decisively and reached as low as 1.1574. Initial bias remains on the downside this week for 38.2% retracement of 1.0569 to 1.2091 at 1.1510. We'd expect strong support from there, at least on first attempt, to bring rebound. Above 1.1643 minor resistance will turn bias neutral first. But break of 1.1879 is needed to confirm completion of the decline. Otherwise, near term outlook remains bearish. Meanwhile, sustained break will of 1.1510 will carry larger bearish implication and target 55 week EMA (now at 1.1327).

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be cautious on 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

In the long term picture, 1.0339 is now seen as an important bottom as the down trend from 1.6039 (2008 high) could have completed. It's still early to decide whether price action form 1.0339 is developing into a corrective or impulsive move. On the upside, strong resistance could be seen from 38.2% retracement of 1.6039 to 1.0339 at 1.2516. On the downside, we're not anticipating a break of 1.0339 in near to medium term.

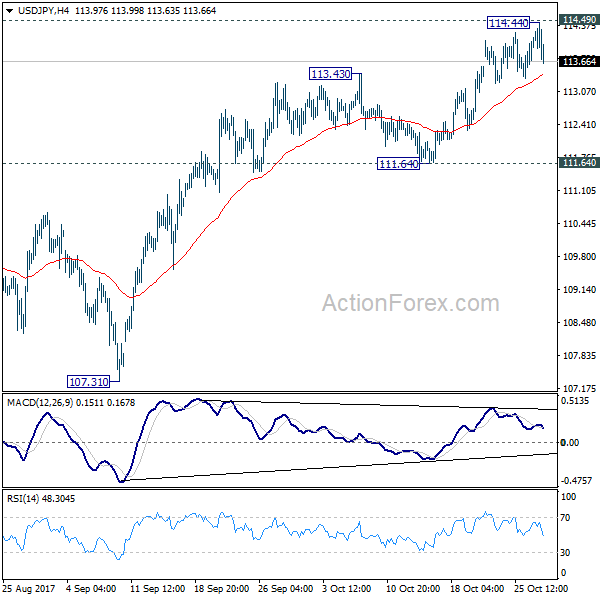

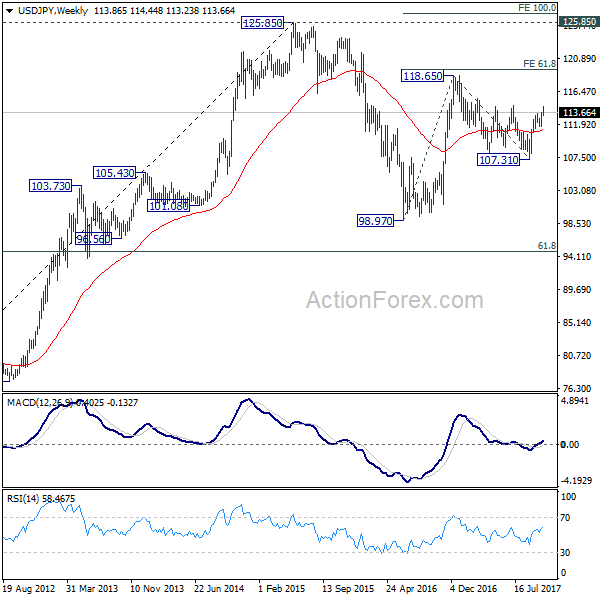

USD/JPY Weekly Outlook

USD/JPY crawled higher to 114.44 with weak momentum last week. But it lacked sustainable buying to push through 114.49 key resistance. Initial bias remains neutral this week first. On the upside, decisive break of 114.49 will confirm that correction pattern from 118.65 has completed at 107.31 already. And USD/JPY should then target a test on 118.65. And in any case, outlook will remain cautiously bullish as long as 111.64 support holds.

In the bigger picture, medium term rise from 98.97 (2016 low) is not completed yet. It should resume after corrective fall from 118.65 completes. Break of 114.49 resistance will likely resume the rise to 61.8% projection of 98.97 to 118.65 from 107.31 at 119.47 first. Firm break there will pave the way to 100% projection at 126.99. This will be the key level to decide whether long term up trend is resuming.

In the long term picture, the rise from 75.56 (2011 low) long term bottom to 125.85 top is viewed as an impulsive move, no change in this view. Price actions from 125.85 are seen as a corrective move which could still extend. In case of deeper fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77. Up trend from 75.56 is expected to resume at a later stage for above 135.20/147.68 resistance zone.

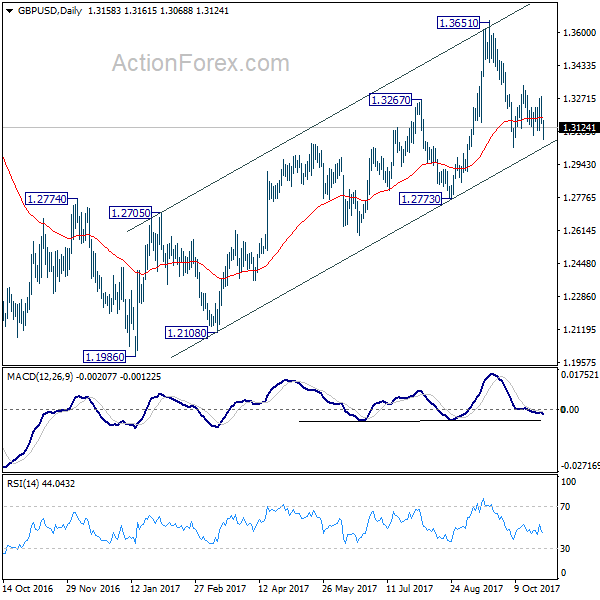

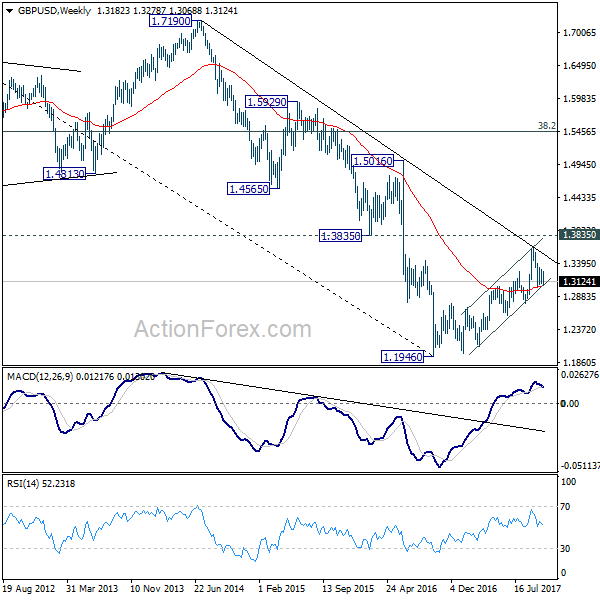

GBP/USD Weekly Outlook

GBP/USD stayed in consolidation in range of 1.3026/3337 last week and outlook is unchanged. Initial bias remains neutral this week first. On the downside, firm break of 1.3026 will resume the decline from 1.3651 and target 1.2773 key support level. This will also revive the case of medium term reversal. On the upside, in case of another rally, upside should be limited by 61.8% retracement of 1.3651 to 1.3026 at 1.3412 to bring fall resumption finally.

In the bigger picture, while the medium term rebound from 1.1946 was strong, GBP/USD hit strong resistance from the long term falling trend line. Outlook is turned a bit mixed and we'll stay neutral first. On the downside, decisive break of 1.2773 key support will argue that rebound from 1.1946 has completed. The corrective structure of rise from 1.1946 to 1.3651 will in turn suggest that long term down trend is now completed. Break of 1.1946 low should then be seen. On the upside, break of 1.3835 support turned resistance will revive the case of trend reversal and target 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466 .

In the longer term picture, long the outlook is turned a bit mixed as GBP/USD failed to break through falling tend line resistance. We'll stay neutral first and assess the outlook again and price actions unfold.