Sample Category Title

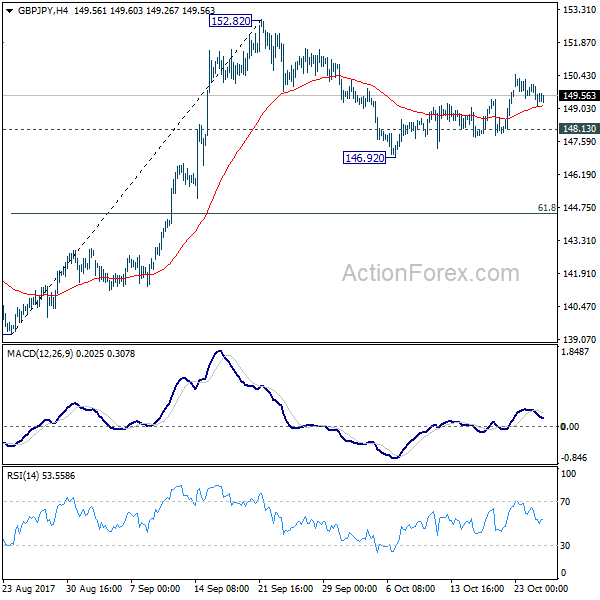

GBP/JPY Daily Outlook

Daily Pivots: (S1) 149.11; (P) 149.60; (R1) 150.06; More

With 148.13 minor support intact, further rise is mildly in favor in GBP/JPY to 152.82 high. Decisive break there will resume whole medium term rise from 122.36. On the downside, break of 148.13 minor support will turn bias to the downside and extend the correction from 152.82. In that case, we'd expect strong support from 61.8% retracement of 139.29 to 152.82 at 144.45 to bring rebound.

In the bigger picture, medium term rebound from 122.36 is still expected to resume after corrective pull back from 152.82 completes. Firm break of 38.2% retracement of 196.85 to 122.36 at 150.43 will carry long term bullish implications. In that case, GBP/JPY could target 61.8% retracement at 167.78. However, break of 139.29 will indicate rejection from 150.43 key fibonacci level. And the three wave corrective structure of rebound from 122.36 will argue that larger down trend is resuming for a new low below 122.26.

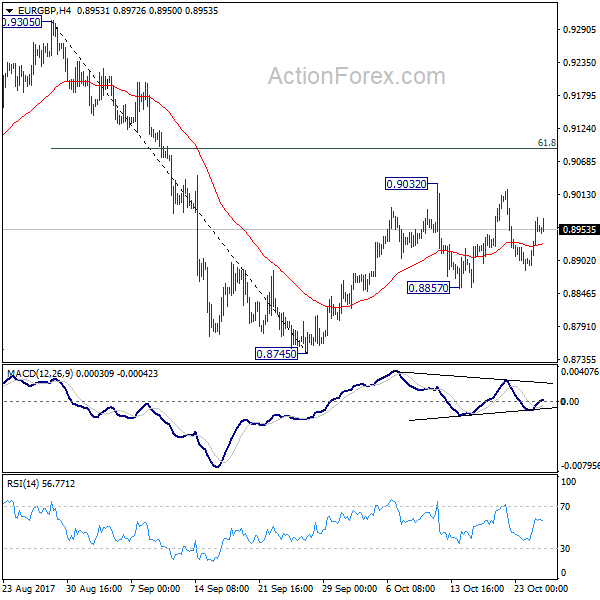

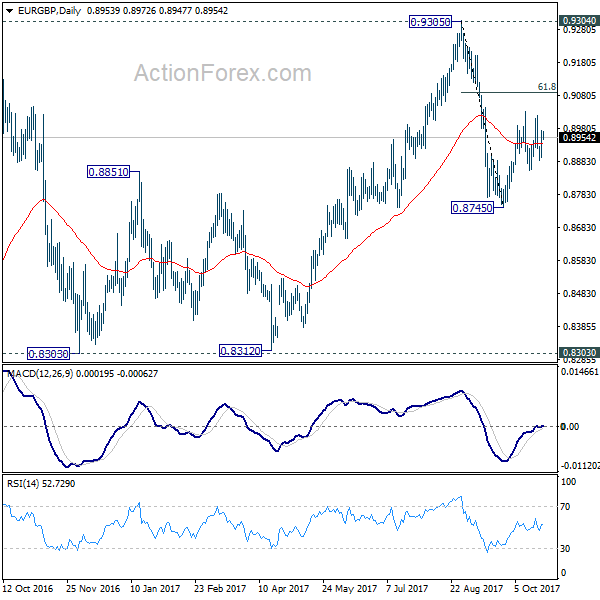

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8906; (P) 0.8941; (R1) 0.8988; More...

EUR/GBP is staying in range of 0.8857/9032 and intraday bias remains neutral first. As long as 61.8% retracement of 0.9305 to 0.8745 at 0.9091 holds, deeper fall is in favor. Below 0.8857 minor support will turn bias to the downside. Further break of 0.8745 will resume whole decline form 0.9305 and target 0.8303 key support level. Nonetheless, sustained break of 0.9091 will bring retest of 0.9305 instead.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of another fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5060; (P) 1.5098; (R1) 1.5161; More....

The strong rally in EUR/AUD and breach of 1.5241 resistance indicates that medium term rise from 1.3624 is resuming. Intraday bias is now on the upside for 61.8% projection of 1.3624 to 1.5226 from 1.4949 at 1.5939 first. On the downside, below 1.5137 minor support will turn intraday bias neutral for consolidations. But outlook will remain cautiously bullish as long as 1.4949 support holds.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term top has completed at 1.3624. Rise from 1.3624 is expected to extend to retest 1.6587. The corrective structure of the price actions from 1.5226 is affirming this view. Sustained trading above 1.5226 will target a test on 1.6587 key resistance. However, break of 1.4421 support will dampen our view and would drag EUR/AUD lower to retest key support zone around 1.3624.

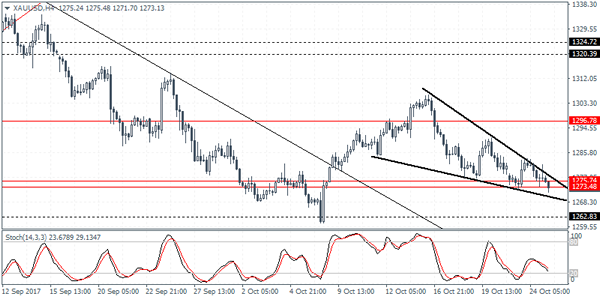

XAUUSD Intraday Analysis

XAUUSD (1273.13): Gold prices were seen giving up the gains as price action fell back to the 1275 - 1274 support level. This indicates that gold prices could see some short term upside correction. Resistance is seen at 1296 which could be tested in the near term, but further gains can be expected only on a convincing breakout above this level. To the downside, gold prices could potentially slip below the current support level which will see a test of the lower support near the 1262 handle. However, watch out for the descending wedge pattern that price has consolidated into. This could suggest an upside breakout that targets the resistance level at 1296.00.

USDJPY Intraday Analysis

USDJPY (113.94): The US dollar managed to recover against the yen as price action posted a strong reversal. This came despite price reversing just above the support level that was supposed to be tested at 113.00 level. A breakout above the previous high formed at 114.00 is requiredin order for USDJPY to maintain the gains. Failure to do so could signal another leg to the downside. This will potentially see USDJPY falling back to establish support at 113.00 which is requiredin order to validate the gains to the upside.

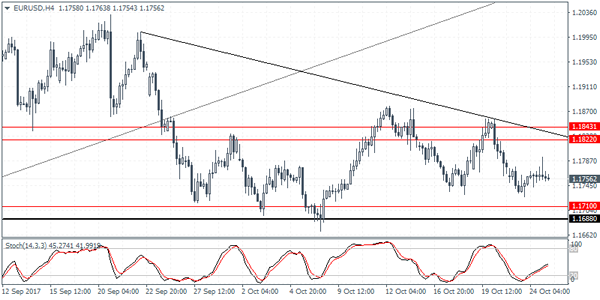

EURUSD Intraday Analysis

EURUSD (1.1756): The EURUSD was seen trading flat with price action briefly rising to intraday highs. The sideways range is expected to be maintained as price action approaches the support level at 1.1710 - 1.1688. A breakdown below this support level could signal further declines in price. On the daily chart, we notice that head and shoulders pattern that has been forming and this could be validated on a test of the neckline support. In the near term, EURUSD could remain trading within the current range, but there is a risk of an upside move. Still, as long as the resistance level of 1.1822 holds, the currency pair remains biased to the downside.

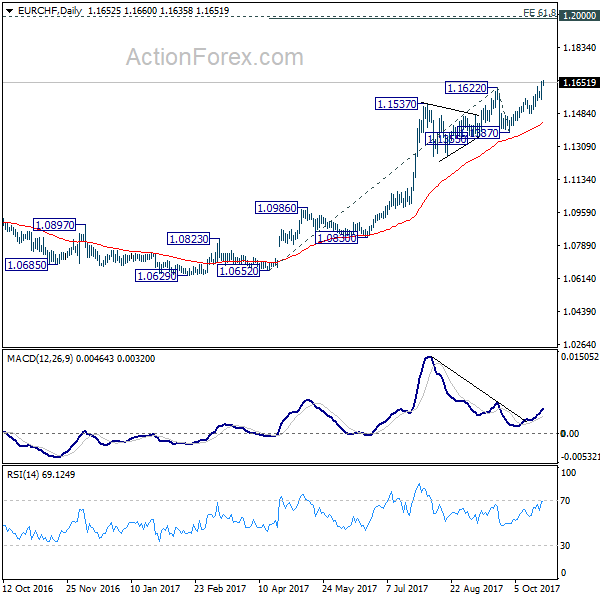

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1592; (P) 1.1625; (R1) 1.1686; More...

EUR/CHF's rally resumed after brief consolidation and reaches as high as 1.1660 so far. Intraday bias is back on the upside. The solid break of 1.1622 resistance confirms resumption of medium term rally. Further rise should now be seen to 61.8% projection of 1.0652 to 1.1622 from 1.1387 at 1.1986, which is close to 1.2 key level. On the downside, break of 1.1560 support is needed to indicate short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, long term rise from SNB spike low back in 2015 is still in progress. EUR/CHF should now be heading back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.1198 resistance turned support holds.

BoC Expected To Hold Rates Steady. Kiwi Extends Losses

The US dollar was seen maintaining its gains across the board although price action was subdued against the euro. The Kiwi dollar was seen extending losses after the new government reported that it will review and propose reforms for overhauling the RBNZ's mandate.

Earlier today, the inflation report from Australia showed that consumer prices rose 0.6% on the quarter ending July. This was weaker than the estimates of 0.8% but higher than the previous quarter's 0.2% increase. The trimmed mean CPI was weaker, rising just 0.4%.

Looking ahead, the UK's preliminary GDP data will be coming out today. Economists are forecasting a 0.3% increase in GDP on the quarter, which will put the economic expansion at the same pace as in the second quarter. Later in the day, the Bank of Canada will be holding its monetary policy meeting. No changes are expected as the central bank is expected to keep interest rates unchanged after raising rates in the previous two months.

Daily Wave Analysis: GBP/USD Bearish Momentum Reaches Key Support Line At 1.31

Currency pair GBP/USD

The GBP/USD needs to break below the support (blue) trend line before a larger bearish breakout is triggered. A break above resistance (red) could indicate that a larger wave C (orange) can take place.

The GBP/USD could be in a wave 1-2 (brown) if price stays above the 100% Fibonacci level. However, price is building a bear flag pattern which could indicate a bearish continuation.

Currency pair EUR/USD

The EUR/USD is still unable to break below the support zone at 1.17, which could indicate the potential for a bullish bounce up to the resistance trend lines (orange). A break above resistance would confirm a bullish breakout within wave C of wave X (pink).

The EUR/USD could be building a larger bullish bounce if it stays above the 78.6% Fibonacci level of wave X vs W. The targets are the Fibonacci levels of wave Y (green).

Currency pair USD/JPY

The USD/JPY is building a pause within the uptrend. A break above resistance (red) could see price challenging the 114.50-115 target zone.

The USD/JPY bounced at the 50% Fibonacci level which was part of a wave 4 correction (green). A break above resistance (red) could confirm the wave 5 (green) breakout.

Forex: Next Fed Chair: John Taylor?

USD is trading close to a 3-month high against JPY on Wednesday, as rumors circulate that many Republican Senators are favoring John Taylor to become the next Chair of the Federal Reserve. Trump hosted a lunch with Republican Senators on Tuesday to gather their views on their preference for the next Fed Chief. Apparently, Trump conducted a 'straw poll' amongst the attendees as to who is their preference between current Fed Governor Jerome Powell or Stanford University economist John Taylor for the role. Sources have revealed that the majority prefer John Taylor, who is regarded as having a strong hawkish stance on monetary policy. The markets believe that Taylor is likely to increase the pace of interest hikes which has, therefore, helped see USD gain against its peers overnight.

The rumors around Taylor helped dilute the fact that the infighting within the Republican party may impede Trump's tax reform plans. Rumors circulated that several Republican Senators may not vote for the tax bill and Trump ranted that Bob Corker, Head of the Senate Foreign Relations Committee and a dissenter of the tax bill, was 'incompetent'. With a slim, 52 to 48 Senate majority, Trump can ill-afford his own party members dissenting against the bill. House of Representatives Speaker Paul Ryan said he wants the House to pass the tax cut bill before the US Thanksgiving Day holiday on November 23rd. With in-party tussles that may be a challenge.

Oil has continued its upward trend as Saudi Arabia's energy minister, Khalid A. Al-Falih, commented that 'We are very flexible, we are keeping our options open. We are determined to do whatever it takes to bring global inventories down to the normal level which we say is the five-year average,'. Such comments are leading the markets to believe the current pact (OPEC, Russia & 9 other producing nations) will be extended past the agreed March 2018 end. The EIA will release data on US inventories later today and so the markets will be looking to see the extent of the forecasted drawdown.

EURUSD is currently trading around 1.1760.

USDJPY is currently trading around 113.92.

GBPUSD is currently trading around 1.3133.

Gold is 0.3% lower in early Wednesday trading. Currently, Gold is trading around $1,273.

WTI is currently trading around $52.50.

Major data releases for today:

At 09:30 BST, the UK Office for National Statistics will release Gross Domestic Product (QoQ & YoY) for Q3. The Quarter-on-Quarter release is expected to be unchanged from the previous reading of 0.3%, whereas the Year-on-Year release is expected to come in slightly lower than the previous release at 1.4%. Any significant deviation for the forecasts are likely to see GBP volatility.

At 13:30 BST, the US Census Bureau will release Durable Goods Orders and ex Transportation data for September. Durable Goods excluding transportation are expected to be unchanged at 0.5%, with the main Durable Goods release forecast to come in at 1.0%, a significant decline from the previous release of 2.0%. Any significant deviation for the forecasts are likely to see USD volatility.

At 15:00 BST, the Bank of Canada will release their Interest Rate decision along with a Rate Statement, which will be followed by a press conference at 16:15 BST. The markets are not expecting any change from the Bank of Canada, with Canadian interest rates expected to remain at 1.0%. Any changes in interest rates will result in CAD volatility.

At 15:30 BST, the US Energy Information Administration will release Crude Oil Stocks change data for the week ending October 20th. The previous release saw a drawdown of -5.731M and the forecast for this release is also expecting a drawdown that is lower at -2.500M. Any significant deviation from the forecast will see volatility in Crude Oil prices.