Sample Category Title

USD/JPY Analysis: Surges To 114.00 Amid Abe’s Victory

In accordance with experts' expectations, the Japanese Prime Minister Shinzo Abe and his Liberal Democratic Party secured their seats for another term.

Anticipation and confirmation of this result led to sharp appreciation of the Dollar against the Yen, allowing the pair to reach a new cellar at the 114.00 mark.

This advance signified a breakthrough through the upper resistance line of large falling wedge. This fact allows assuming that the buck is going to continue strengthening at least until the clash with the monthly R1 at 114.75.

But in shorter perspective the pair is likely to return back to the 113.35 mark and make a rebound from the bottom edge of a junior ascending channel that will be backed up by the rising 55- and 100-hour SMAs.

XAUUSD Analysis: Approaches 100-Day SMA

Previous trading week the exchange rate ended at the intersection of the 61.8% Fibonacci retracement level and the bottom boundary of two ascending channels and was ready to make a rebound.

However, an unconfirmed victory of the Japan's PM Shinzo Abe and his party strengthened the Dollar and pushed the through this combined support barrier.

This fact as well as Donald Trump's intention to complete tax reform, after successful vote on budget in the Senate, indicates that the pair might continue to move in the southern direction towards the weekly S1 at 1,270.00.

On the other hand, the fact that on daily chart the pair is facing the 100-day SMA suggests that the pair is likely to retreat for some while. Plus there is a need to take into account that market sentiment is 53% bullish.

USD/CAD: Canadian Consumer Price Index

Canadian Dollar dropped markedly against the Greenback after data showed slightly weaker-than-anticipated monthly gain in consumer inflation, while the yearly rate moved closer to the Bank of Canada's 2% target. The USD/CAD currency pair rose 88 base points or 0.70% to the 1.2571 mark and continued consolidation in the 1.2620 area.

Statistics Canada reported on Friday that the country's consumer inflation marked a 0.2% monthly increase in September, putting an annual growth rate to 1.6% in the reported period. These gains were mainly supported by rising gasoline prices, as well as higher shelter and food costs. The BoC is expected to meet this Wednesday to discuss if further monetary tightening is appropriate at this time.

EUR/USD: US Existing Home Sales

The EUR/USD currency pair revealed a modest reaction on the US economic reports showing some positive changes in the US existing home sales. The Euro lost against the US Dollar just 4 base points to continue slipping further into the 1.1770 area.

The National Association of Realtors reported on Friday that the US existing home sales gained 0.7% to a seasonally adjusted yearly rate of 5.39M in September. The increase was sustained by dissipation of the effects of Hurricanes Harvey and Irma, though an enduring dearth of available properties kept weighing on overall activity. Moreover, weak affordability is likely to keep prices high confusing considerable buyers' interest throughout the US.

Technical Outlook: WTI OIL Struggles To Break Above $52.00

WTI Oil continues to struggle at $52.00 barrier on Monday, following several unsuccessful attempts last week after upticks hit highs at $52.35 but failed to clearly break higher.

Two strong downside rejections on Thu/Fri signaled strong bullish bias but did not manage to generate stronger momentum for final break higher and test of target at $52.84 (28 Sep high).

Overall structure remains bullish with signs of US oil market tightening and rising demand in Asia being supportive for further advance.

Formation of daily Tenkan-sen / Kijun-sen bull cross underpins, but the price may stay in extended consolidation, as negative signal has been generated on reversal of slow stochastic from overbought territory on daily chart, with south-heading indicator showing plenty of room at the downside.

Extended downticks face solid supports from rising 10SMA ($51.54) and Tenkan-sen ($51.25) which are expected to contain and keep the downside protected.

Res: 51.96, 52.35, 52.84, 53.00

Sup: 51.73, 51.54, 51.25, 50.97

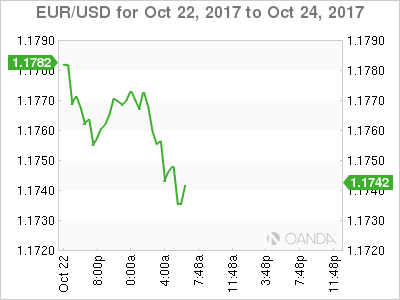

Euro Edges Lower As Investors Look For Catalyst

The euro has started losses in the Monday session. Currently, EUR/USD is trading at 1.1745, down 0.30% on the day. On the release front, we’ll get a look at Eurozone Consumer Confidence, which is expected to remain to remain at -1 point. There are no US events on the schedule. On Tuesday, Germany and the eurozone will release Manufacturing PMIs.

The standoff in Catalonia has continued this week. On Saturday, the central government said it was imposing direct rule, invoking Article 155 of the Spanish Constitution. However, there is plenty of uncertainty, as this clause has never been used and it is unclear what steps Madrid will take. Spanish media is reporting that the central government will strip Catalan President Carles Puigdemont of all his powers and take over Catalonia’s local police force. Unsurprisingly, the Catalan government has condemned Madrid and said it will not accept direct rule. The crisis has led to many companies in Catalonia moving their legal headquarters to Madrid, and investors are nervously watching as developments unfold in Spain, which is the eurozone’s fourth largest economy.

The Brexit clock is ticking, with Britain leaving the European Union in March 2019. However, negotiations between the parties have foundered, as the sides remain far apart on a number of key issues, including the size of Britain’s bill when it says goodbye to the club. Prime Minister May addressed the 27 EU leaders last week in Brussels, imploring the European to show some flexibility. This didn’t prevent the EU leaders from stating that trade negotiations with Britain would not commence until more progress was made on non-trade matters. Prime Minister May has a razor-thin majority in parliament, and adding to the mix, there are sharp divisions in her cabinet regarding Brexit, with some senior ministers in favor of taking a hard stance and leaving the EU without an agreement if the Europeans fail to soften their position.

Spain On Edge, EURO Lower

Geopolitical events again dominate market movements.

The Euro starts the week on the back foot as the market waits for the next big development in Spain, where Catalan separatists are expected to deliver a response after PM Rajoy moved on the weekend to impose federal authority on the region.

In Japan, the PM Abe's Liberal Democratic Party won big as expected, they retained two-thirds majority in Sunday's general election. Abe's win makes the reappointment of Kuroda, and hence the continuation of ultra-easy monetary policy, significantly more likely. Yesterday's victory sent the Nikkei to the longest winning streak on record and the yen to a new three month low outright.

Elsewhere, a number of central bank policy meetings begin this week – Bank of Canada (Oct 25) and European Central Bank (Oct 26). The BoC is expected to pause in its interest rate increases this time around. The bank will also publish its Monetary Policy Report (MPR), while the ECB is expected to announce a recalibration of its asset purchase program.

Also keeping investors busy will be the potential unveiling of President Trump's pick for Fed chair and his efforts to overhaul U.S's tax code. Later in the week, Q3 preliminary GDP data for the U.K and U.S also will be released.

1. Victory for Abenomics lift stocks to new record

In Japan, Abe's convincing election victory lifted the Nikkei to its highest in 21-years and world stocks to an all-time high overnight, despite an escalation of Spain's constitutional crisis. The Nikkei ended up +1.1%, while the broader Topix climbed +0.8%. Expect the market's attention to now shift to corporate earnings.

Down-under, Australia's S&P/ASX 200 lost -0.2%, while South Korea's Kospi index was little changed.

In Hong Kong, stocks fell overnight, led by banking and property shares, amid concerns of slowing economic growth in China. The Hang Seng index fell -0.6%, while the China Enterprises Index also lost -0.6%.

In China, stocks inch a tad higher, with consumer and healthcare firms lending the biggest support in the session. The blue-chip CSI300 index rose +0.1%, while the Shanghai Composite Index also added +0.1%.

Note: Quarterly earnings from a slew of Chinese companies this week will serve as a barometer of the country's economic health.

In Europe, regional indices trade mostly higher across the board with the exception of the Spanish Ibex, which trades lower on continuing worries over Catalonia as Spanish Banks weigh on the index.

U.S stocks are set to open unchanged.

Indices: Stoxx600 +0.2% at 390.9, FTSE +0.1% at 7532, DAX +0.3% at 13035, CAC-40 +0.3% at 5389, IBEX-35 -0.4% at 10184, FTSE MIB flat at 22353, SMI +0.2% at 9255, S&P 500 Futures flat.

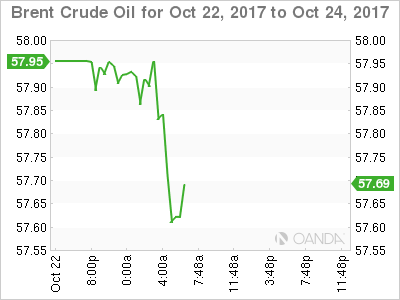

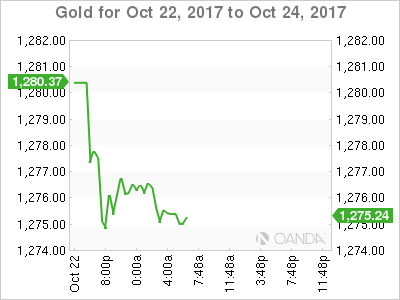

2. Oil edges higher on tighter supplies, gold falls

Oil prices remain better bid over supply concerns in the Middle East and as the U.S market shows further signs of tightening while demand in Asia keeps rising.

Brent crude futures are at +$57.87, up +12c from Friday's close, while

U.S West Texas Intermediate (WTI) crude is at +$52.04 per barrel, up +20c.

Data on Friday showed that the amount of U.S oilrigs drilling for new production fell by seven to 736 in the week to Oct. 20, the lowest level since June according to Baker Hughes.

In the Middle East, flows from Iraq has reduced due to fighting between government forces and Kurdish groups, and production still being withheld as part of a pact between OPEC and non-OPEC producers to tighten the market.

In Asia, growth remains strong especially in China and India, the world's number one and three importers.

Gold hit its lowest in over two-weeks this morning, as the dollar climbed to a three-month high versus the yen (¥114.05) after Sunday's election results have left the door open to ultra-loose monetary policy for longer. Spot gold was down -0.4% at +$1,275.81 an ounce.

3. Sovereign yields fall

Eurozone borrowing costs have eased a tad as Abe's big win gives the green light for a continuation of Japan's hyper-easy monetary policy.

JGB yield's erased an early rise as Abe's election win reinforced the markets view that his reflation economic policies will remain in place. The yield on the 10-year JGB initially rose to +0.080%, matching a 10-week high, but slipped back to +0.070% or unchanged.

All eyes will now shift to the ECB meet Thursday (07:45 am EDT) when officials are expected to signal baby steps away from their ultra-easy monetary policy stance. Germany's 10-year Bund yields fell -2 bps to +0.43%, pulling back from a one-week high at +0.46%.

With the Fed expected to hike one more time in 2017 continues to support the ‘big' dollar. The yield on U.S 10-year Treasuries has declined less than -1 bps to +2.38%.

4. Dollar is steady, supported by rate differentials

A wider spread between U.S. and eurozone bond yields, as well as political uncertainty in Spain, is weighing on the EUR (€1.1744) outright. U.S yields are being supported by market expectations of U.S tax cuts and the possibility of a new Fed chair that may be more of a ‘hawk.'

The EUR is expected to trade defensively ahead of Thursday's ECB meeting. Central bank officials are expected to outline their asset purchase reduction plan. Market guesstimates expect the ECB to begin to taper its current €60B monthly asset purchases in January 2018 with consecutive €10B monthly reductions. This means the ECB would cease balance sheet expansion by the end of Q2 2018.

The downside risk for EUR is for the ECB to announce that it will taper with lower bond purchases for longer.

5. Catalan parliament to meet on Thursday

Earlier this morning, Catalonia's parliament indicated that it would hold a complete session on Thursday morning, in which it will lay out its response to Madrid after PM Rajoy government, said it would impose direct rule.

Carles Puigdemont party is expected to launch a legal appeal against the application of article 155, which rests power from the regional government and lays the groundwork for new elections.

The Spanish senate is expected to pass article 155 this Friday

Technical Outlook: SPOT GOLD – Eventual Break Below Daily Cloud Would Trigger Fresh Weakness

Spot Gold is holding firmly below thick daily cloud base after being unable to clearly break support ($1281) in several attempts last week. Gold price hit new two-week low at $1274 on Monday after breaking below next pivotal supports at $1277 (Fibo 61.8% of $1260/$1306 upleg) and $1275 (100SMA).

Close below here is needed for fresh bearish signal after break below cloud base, to extend bear-leg from $1306.

Immediate support lies at $1271 (Fibo 76.4%) but bears may extend towards key point at $1260 (06 Oct low) as the yellow metal remains under pressure by strengthening US dollar.

Thick daily cloud (spanned between $1281 and $1321) weighs strongly and cloud base is expected to limit upside action.

Res: 1277, 1281, 1283, 1288

Sup: 1274, 1271, 1266, 1260

Technical Outlook: NZDUSD – Bears Are Taking A Breather But Focus Remains At The Downside

The New Zealand dollar bears are taking a breather on Monday after sharp fall last week when the pair was down nearly 3% on strong sell-off, triggered by political uncertainty.

Last week's fall marks the biggest weekly losses since early Nov 2016.

Fresh five-month low at 0.6930 was hit in Asia on Monday, with subsequent bounce remaining capped under broken psychological 0.7000 level.

However, stronger correction cannot be ruled out as slow stochastic is in deep oversold territory but no firmer reversal signal being generated yet.

Stronger recovery through 0.7000 should stay below falling daily Tenkan-sen (0.7070) before bears resume, as overall structure is negative.

The pair is riding on the wave C of five-wave sequence from 0.7558, which eyes its FE 123.6% at 0.6907.

Res: 0.7000, 0.7055, 0.7070, 0.7126

Sup: 0.6930, 0.6907, 0.6844, 0.6817

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.1767

The intraday outlook remains bearish below 1.1790, for a slide towards 1.1715 area. Only a violation of 1.1790 will signal a reversal of the slide from 1.1860.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.1790 | 1.1940 | 1.1715 | 1.1660 |

| 1.1880 | 1.2030 | 1.1660 | 1.1480 |

USD/JPY

Current level - 113.69

The uptrend is intact, heading towards 114.50, en route to 115.50 zone. Key support lies at 113.50 and crucial on the downside is 113.10.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 114.50 | 114.50 | 113.10 | 111.00 |

| 115.50 | 115.50 | 112.30 | 107.30 |

GBP/USD

Current level - 1.3211

A reversal has been confirmed at 1.3085 and the intraday bias is positive, with a risk of a rise towards 1.3340 hurdle. On the senior frames the current leg should be the final one of the prolonged consolidation above 1.3020, preceding a renewal of the general slide towards 1.2590. Minor intraday support lies at 1.3160.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.32220 | 1.3340 | 1.3160 | 1.2910 |

| 1.3340 | 1.3650 | 1.3020 | 1.2760 |